The Australian United Investment Company (ASX:AUI) is an Australian Listed Investment Company with a market capitalization of around (AUD) $1 Billion. According to their July 2020 annual report, AUI’s holdings consists of around $1,121 Million in assets spread across approximately 40 (mostly Australian) share holdings (as well as cash trusts and other short term receivables), less $223 Million in liabilities such as deferred tax liabilities and a $100 Million investment line of credit loan with the NAB bank.

AUI mostly invests in ASX50 stocks, but also holds a small holding in its sister company DUI, the Diversified United Investment Limited, as well as some outsourced holdings in smaller cap funds.

“AUI was founded in 1953 by the late Sir Ian Potter and The Ian Potter Foundation Ltd is today the Company’s largest single shareholder.“

Australian United Investment Company

CaptainFI is not a Financial Advisor and the information below is not financial advice. This website is reader-supported, which means we may be paid when you visit links to partner or featured sites, or by advertising on the site. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Australian United Investment Company (ASX:AUI)

The Australian United Investment Company is a no frills, no nonsense Listed Investment Company that is currently run by an experienced team of four directors in Melbourne, Victoria. They meet once per month to discuss the portfolio’s performance and direction with any investing decisions.

The Company’s objective is to take a medium to long term view and to invest in a diversified portfolio of listed Australian equities which have the potential to provide income and capital appreciation over the longer term. Modest exposure to the Australian equities Small Cap sector is achieved through investment in unlisted managed funds.”

Australian United Investment Company

Founded in 1952 by Sir Ian Potter, and listed on the ASX in 1974, AUI is one of the ‘Granddaddy LICs’ in Australia and operates with a low management expense ratio. It has seen many market cycles and has been able to provide solid returns for its shareholders throughout its operation. The company mainly invests in large, blue chip share holdings but also has some holdings in other funds.

“Investments are purchased on the basis of the directors’ assessment of their individual prospects for income and growth. The directors do not invest by reference to any pre-determined policy that any particular proportions of the capital will be invested in particular investment sectors.”

Australian United Investment Company

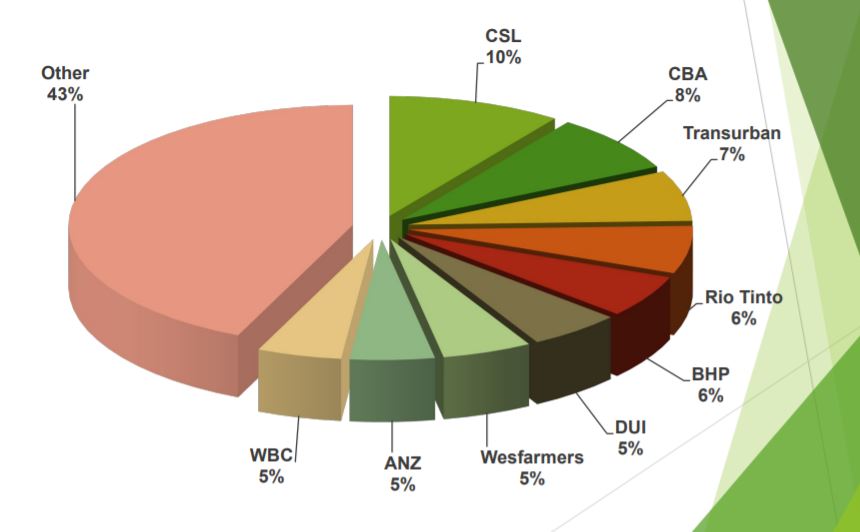

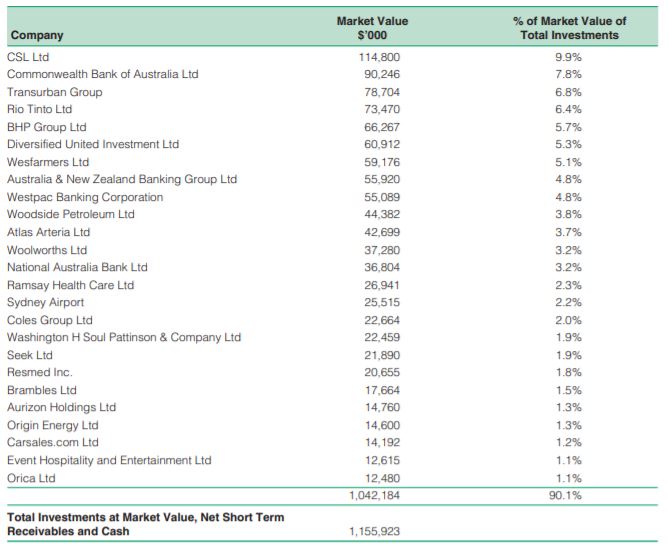

Australian United Investment Company (ASX:AUI) top holdings

The top 25 holdings of AUI currently make up over 90% of their total holdings. The biggest being;

- CSL,

- Commonwealth bank

- Transurban Group,

- Rio Tinto

- BHP,

- Diversified United Investment Limited, AUI’s sister company

The total top 25 investments as of the 2020 Annual report are as follows;

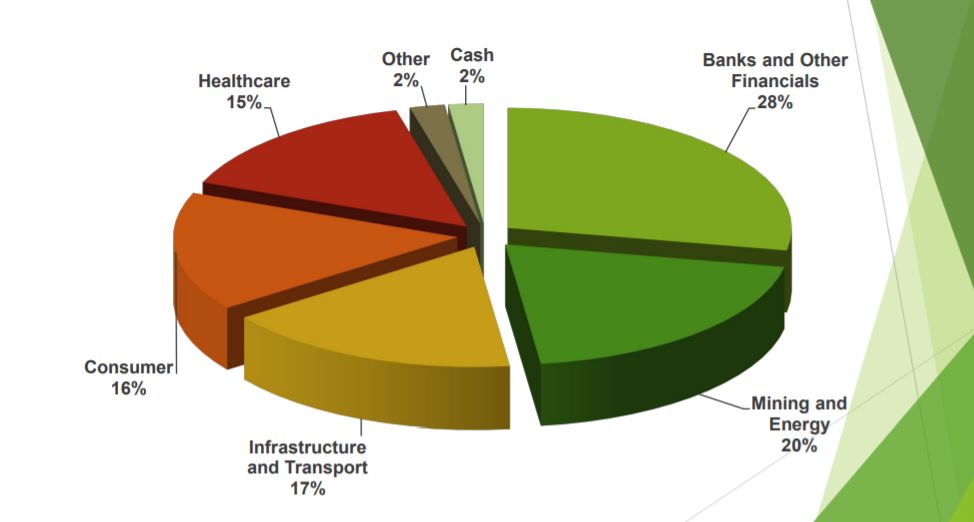

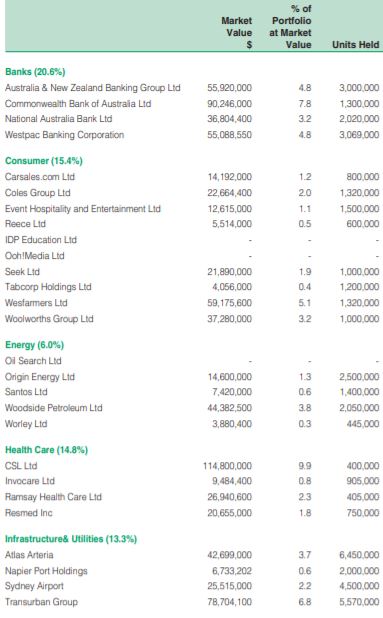

All Australian United Investment Company (ASX:AUI) holdings

The entire AUI portfolio consists of the following companies and portfolios;

Performance of Australian United Investment Company (ASX:AUI)

Performance is considered to be broken down into dividend and capital growth (capital growth is often reflected by earnings growth and so I have noticed this is sometimes used interchangeably).

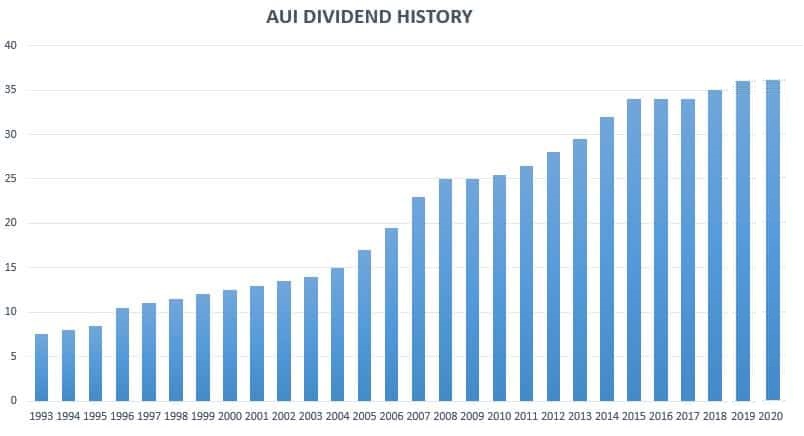

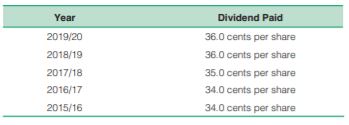

Dividend history of Australian United Investment Company (ASX:AUI)

Generally the Australian United Investment Company (ASX:AUI) has provided a pretty good track record of increasing dividend yields and earnings growth – for 26 years straight the AUI dividend has either held steady or increased, averaging around a 6% earnings growth.

COVID-19 however, has not been kind to many of AUIs constituent holdings, and AUI has resorted to paying out retained dividends from previous years to its shareholders in order to smooth this effect. This is one of the main benefits of LICs – the dividend smoothing.

With the current share price of $8.46 and a dividend of 36 cents per share, this currently puts AUI at a dividend yield of 4.25%. Accounting for the fully franked dividend, this grosses up the yield to 6.07%, which is a pretty healthy dividend.

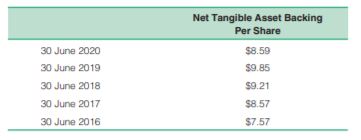

Capital Growth of the Australian United Investment Company (ASX:AUI)

General increasing earnings, or dividend growth, has seen the share price of AUI grow. Typically though, the share price has lagged the NTA meaning AUI often trades at a discount.

Australian United Investment Company (ASX:AUI) vs index

Comparing the Australian United Investment Company (ASX:AUI) to the S&P/ASX 200 (ASX:XJO) since June 2006 (the longest time period I could select) shows that AUI is up 19.49% whilst the straight ASX 200 index is up 28.3%.

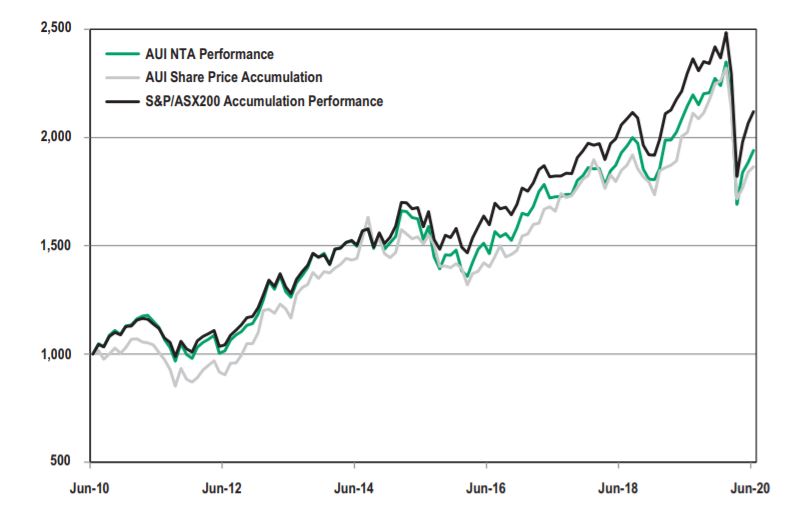

However, remember this is just capital price value, and does not account for reinvested dividends in either holdings. When comparing the reinvested dividends, this becomes an accumulation performance rather than straight share price. We can use the graph provided by AUI in their 2020 annual shareholder report which compares AUI’s Total performance against the S&P/ASX200 Accumulation Performance (ASX:XNT).

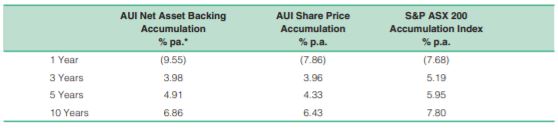

As you can see, the AUI performance has generally been quite correlated to the S&P/ASX200 Accumulation Performance (ASX:XNT), but it has under-performed it. Particularly in the past 5 years the NTA has lagged behind the accumulation performance index. This graph also shows the tendency for AUI’s share price to lag the NTA – indicating that the LIC normally trades at a discount to NTA, so I’m not rushing out to buy it when I see it trade at a discount.

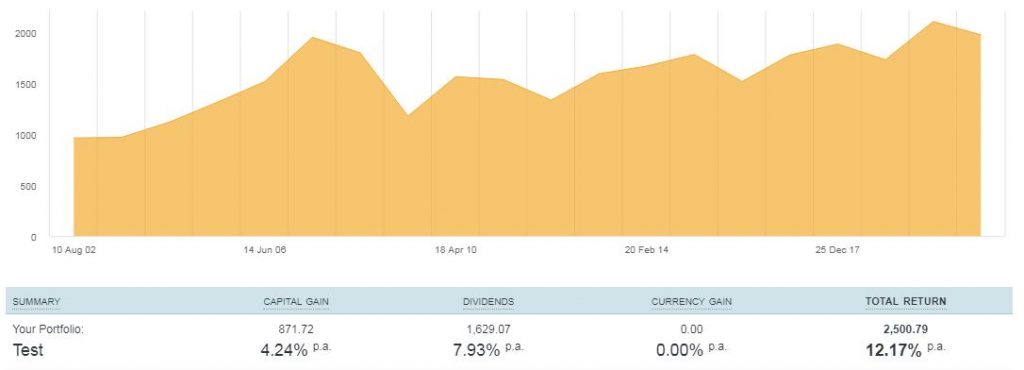

Looking at it from an independent source through Sharesight shows the last 20 years performance to date (dividends reinvested) has actually been pretty good though, with nearly a 16% annualised total return (ignore the $ values and focus on the %, this was of a notional $1000 investment).

When we compare the AUI Sharesight graph to a similar investment in STW, we see a similar general trend. However, we should note that the STW ETF index fund was only around from Aug 2001 so this graph starts from 31 Aug 2001 (about a year later from the AUI start). The returns are annualised though so it shouldn’t make too much of a difference.

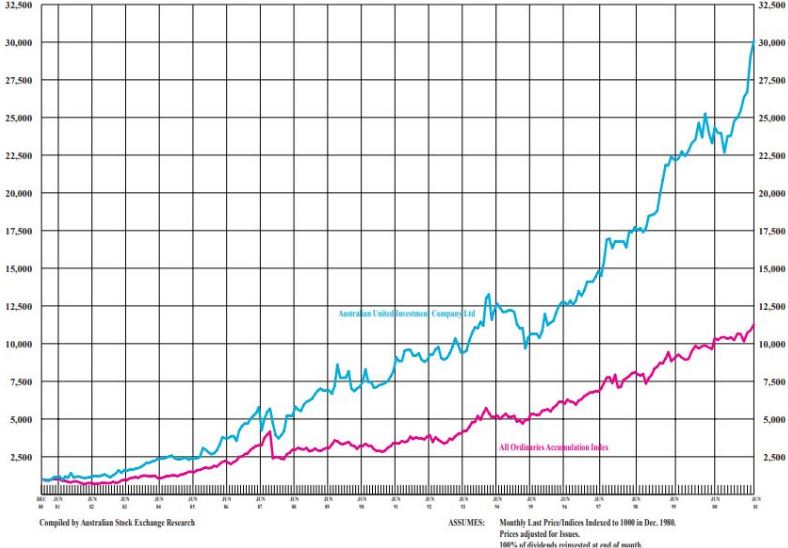

Comparing the two has shown that historically AUI had out performed the general index. If we take a look at some historical data going back even further than 20 years, this is even more true (1980-2000).

Alas, Past performance is no indicator of future performance, and we have been seeing this in the past 5 years particularly as AUI has started to under-perform a basic market cap weighted index fund. Many long term share holders in AUI don’t mind, and still maintain holdings in AUI as an attractive dividend income source with a target of a growing dividend yield (and it has had a posiotive earnings trend for 26 years).

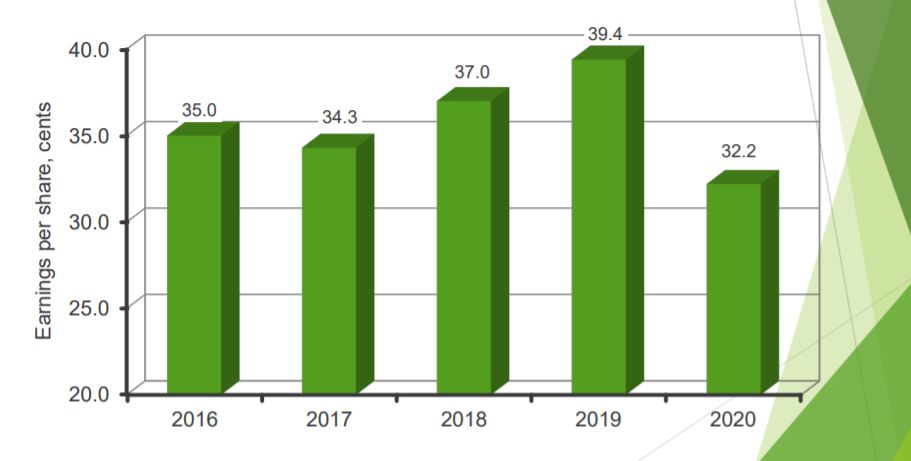

Looking ahead, due to COVID-19 many companies have slashed dividends as their earnings have slumped, which has led the AUI chairman and directors to release that AUI’s operating profit fell from $49 Million in 2019 to $40 Million in 2020, and it is likely earnings will continue to decrease in line with their constituent holdings paying out less dividends.

AUI’s share price fell, but not as much as the earnings did. This means that AUI’s earnings per share has decreased (generally in line with the market) and it is possible they may need to cut the dividend in future since they don’t hold huge cash reserves – currently $17 Million in cash and short term receivables which is about 1.5% of their portfolio. Recently AUI drew an additional $15M against their NAB loan bringing it from $85M to $100M (out of a $150M facility) to help manage cash-flows.

It is not just COVID-19 that has impacted AUI, and the AUI total accumulation figures have actually under-performed a market accumulation index over the past 1, 3, 5 and 10 years.

Management of Australian United Investment Company (ASX:AUI)

Incredibly, the Australian United Investment Company is currently run as a very ‘tight ship’ by a very small board of only four directors;

- C B Goode AC – Chairman

- J S Craig

- F S Grimwade

- D C Hershan

As well as two accountants (company secretaries)

- Andrew J Hancock FCA

- James A Pollard CA

AUI is independently audited by two analyst firms

- KPMG

- Chartered Accountants.

Management fees of Australian United Investment Company (ASX:AUI)

The Australian United Investment Company has pretty rock bottom Management fees – in 2019 this was .10% (10 basis points) putting it on par with many ETFs, however in 2020 this did increase to .12% (12 basis points). A MER of .12% means that a $10,000 investment in AUI will cost you $12 in management fees each year. This is reflected in the incredibly small management team and very spartan way the company is run (I mean check out their website, its not much better than Warren Buffets one!)

The biggest shareholder of AUI is the Ian Potter Foundation Ltd, which is a charitable organisation created by Sir Ian Potter, the funds original founder. The Ian Potter Foundation relies on earnings from AUI to fund charitable donations. Following the Ian Potter Foundation is Argo Investments, which have a size-able investment in the fund of nearly 11.5% (which makes up about 2% of Argo’s portfolio).

Gearing of Australian United Investment Company (ASX:AUI)

AUI also runs a modest borrowing facility with National Australia Bank, and as of the 2020 annual report has currently drawn $85 Million out of an $150 secured line of credit for investment gearing.

In a September 2020 update, AUI has drawn an additional $15 Million from the NAB line of credit, totaling $100M, and held $17 million in cash and short term receivables. This means they are very modestly geared, something like 9% or so of the total portfolio. The earnings received from the investment portfolio covers the interest, and as you can see from the 2020 report, the interest rates are pretty low in line with current market interest rates, less about $35M which is fixed at around 4%.

Would I own Australian United Investment Company (ASX:AUI)?

No, I don’t currently own AUI. AUI looks like it has provided a great investment in the past with some epic track records of out performing the market, and the company does align with my values of producing a growing dividend income stream over the long term, with a competitively low management expense ratio.

However, over the past 10 years they have consistently under-performed a basic market cap weighted index fund. For this reason, and to keep things simple, I think I will be sticking to my core holding of ETFs.

Whilst I do see the benefits of dividend smoothing, reliable fully franked dividends and strong earnings growth through the LICs, I can’t help but feel let down by the under-performance of AUI over the past ten years compared to the basic market index accumulation fund. It is also highly concentrated in under 50 stocks which brings with it concentration risk and human error.

If you have a high income now (getting ready to FIRE) and you get paid a dividend, even with the franking credit that comes attached to it you will still need to pay additional tax, and then you need to reinvest it and have to pay brokerage to do so (unless you use a DRP) – overall this lowers the amount you have invested and causes tax and brokerage drag. You effectively ‘lock in’ your high marginal tax rate that you are on right now, and that little bit no longer compounds for you because it has been taken away.

If you believe in an efficient market and that total return (dividend + capital growth) will be similar regardless of how it is broken down (i.e. dividends vs capital growth or dividend/earnings growth) then it might make sense to go for a more capital growth focused investment as you accumulate wealth before early retirement. Since that approach keeps your capital effectively more ‘fully invested’ and you are able to defer any tax drag until the point that you actually sell. If you do sell of parcels of shares, having held them for 12 months in your name gets you a 50% CGT discount, and if you are selling them off in the low income environment of early retirement (and potentially splitting this between two names in the household) it is likely this tax would be a fairly low tax burden anyway.

We know that selling parcels of shares can be stressful though due to volatility, and that generally in a recession the dividends tend to get cut by less than the share price drops. This means your emergency fund could typically last much longer if it is supplementing a dividend focused strategy rather than a capital growth focused strategy. So some people prefer the more reliable income and dividend smoothing that LICs provide – this peace of mind and stress free form of investing may well be worth under-performing the market by a percent or so. Like anything, the higher the risk, the higher the reward. Furthermore, I have had such a positive psychological benefit from receiving dividends (from both ETFs and LICs) that have helped me to stay the course and continue investing – its just so awesome to see the strategy working and getting positive feedback.

Of course, some oldschool LICs like AFIC and Whitefield have DSSP (bonus share plans) which can be very tax effective for people who never plan to sell the shares. You don’t pay tax on the dividends when reinvested, but this effectively lowers the cost base of your shares so if you ever did sell the portfolio you pay this tax in the form of higher capital gains taxes later – so it is a way of growing the portfolio quicker and deferring the tax burden. If you never sell the shares, you never pay this deferred tax so it can be very lucrative for high income earners on the path to FI who will always hold these shares in their name. I am not 100% sure of this but I think the cost base might even get ‘reset’ to the current market price if the shares are ever passed down through an inheritance. Also sometimes it makes sense to hold investments in a company structure but that is opening a whole separate can of worms – perhaps an accountant or financial advisor reading this can shed some light in the comments. AUI does not offer this type of bonus share plan.

Maybe an optimal approach is could be a capital growth focused strategy until FIRE, and then somehow magically switching to income producing assets post FIRE without taking a huge tax hit. I don’t know. We could probably overthink this until the cows come home, so for now I am just going to do a little of both. I have a core holding of ETFs, supplemented by some LICs – this portfolio provides some dividends and some capital growth. This is mainly in Australian shares through my Betashares A200 ETF, and internationally diversified with my Vanguard VTS and Vanguard VEU ETFs. I am not adding AUI to this list right now, but it is something I will keep an eye on.

Conclusion

The Australian United Investment Company (ASX:AUI) is an Australian Listed Investment Company founded in 1953, and listed to the ASX in 1974. According to the 2020 annual report, AUI’s holdings consists of around $1,121 Million in assets spread across approximately 40 (mostly Australian) share holdings (as well as cash trusts and other short term receivables), less $223 Million in liabilities such as deferred tax liabilities and a $100 Million investment line of credit loan with the NAB bank.

AUI mostly invests in ASX50 stocks, but also holds a small holding in its sister company DUI, the Diversified United Investment Limited, as well as some outsourced holdings in smaller cap funds. For 26 years AUI has been able to provide a stable or growing dividend to shareholders, which has made it a very attractive income source for many, especially retirees.

Personally, I am not investing in AUI. It has too much of a concentrated portfolio for my liking, and it has also under-performed a basic ASX 200 accumulation index over the past 1, 3, 5 and 10 years – growing less overall, and then dropping more sharply during the COVID-19 pandemic. AUI also does not offer the bonus share plan that AFIC and Whitefield have. The future is also looking uncertain for AUI’s dividend track record; earnings per share have decreased and AUI has recently expanded its (relatively small) debt position by nearly 20% by taking on an additional $15M in debt with NAB to assist with cash-flows (taking overall fund gearing to about 9%). My guess is that they will have to cut their dividend in the future to a sustainable level.

Further reading

Financial Disclaimer

Financial Disclaimer: CaptainFI is NOT a financial advisor and does not hold an AFSL. This is not financial Advice!

I am not a financial adviser and I do not hold an Australian Financial Services Licence (AFSL). In this article, I am giving you factual, balanced information without judgment or bias, to the best of my ability. I am not giving you any general or personal financial advice about what you should do with your investments. Just because I do something with my money (or use a particular service or platform) doesn’t mean it is automatically appropriate for your personal circumstances. I do not recommend nor endorse any financial or investment product, and my usage or opinion of any product should not be interpreted as an endorsement, advertisement, or intent to influence.

I can only provide factual information based on my journey to Financial Independence, and that is provided for general informational and entertainment purposes only. I make no guarantee about the performance of any product, and although I strive to keep the information accurate and updated as it changes, I make no guarantee about the correctness of reviews or information posted.

Remember – you always need to do your own independent research and due diligence before making any transaction. This includes reading and analysing Product Disclosure Statements, Terms and Conditions, Service Arrangement and Fee Structures. It is always smart to compare products and discuss them, but ultimately you need to take responsibility for your use of any particular product and make sure it suits your personal circumstances. If you need help and would like to obtain personal financial advice about which investment options or platforms may be right for you, please talk to a licensed financial adviser or AFSL holder – you can take the first steps to find a financial advisor by reading this interview, or by visiting the ASIC financial adviser register and searching in your area.

For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.