The Bank of Melbourne1 are an Australian financial institution that primarily serve Victorian residents. They offer various financial products and services, including personal and business banking, credit cards, insurance, and superannuation. In this article, I explore the pros and cons of being a Bank of Melbourne customer, list Frequently Asked Questions (FAQs) and discuss home loan products. Read on for my full bank of Melbourne review..

The Good

- A growing network of branches and ATMs throughout Victoria

- Competitive interest rates on savings accounts and home loans

- Digital banking services, including online banking and a mobile app

- A full range of financial products and services, including accounts, credit cards, loans, home loans, super, insurance and investing.

- The BOM are committed to supporting the local community and sponsors a range of events and initiatives across VIC.

- A serious approach to the security of its customers’ accounts

- Owned by one of the big 4 – Westpac Bank.

- Winner of several awards, including Mozo’s award for an excellent banking App.

The Bad

- No branches or ATMs outside of Victoria

- Not as many ATMs or branches as those of the ‘big 4’ banks

- Fees for certain transactions, such as ATM withdrawals or international money transfers

- Some customers have reported issues with customer service

Verdict: Great features for online banking, and a full range of financial products available, but may be mostly beneficial for Victorian residents.

Introduction

As a modern-day Australian, it can be a difficult task to choose a business to bank with, given the large number of available financial institutions. According to the Australian Prudential Regulation Authority (APRA2),, 144 banks were operating in Australia in 2021, including traditional banks, credit unions, building societies, and online-only banks. With so many options to choose from, it can be challenging to know which bank is right for you.

In this article, we shine the spotlight on the Bank of Melbourne, a well-established Australian bank that have been serving the people of Victoria for several decades. With a variety of products and services designed to meet the needs of individuals, families, and businesses, the Bank of Melbourne could be a popular choice for those Victorians looking for a reliable and trustworthy bank.

In this article, we will take a closer look at the Bank of Melbourne, discussing their product offerings, important factors to consider when choosing a bank and the positives and negatives of transacting with the Bank of Melbourne.

CaptainFI is not a financial advisor and this article is not financial advice. This website is reader-supported, which means we may be paid when you visit links to partner or featured sites, or by advertising on the site. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Which bank owns the Bank of Melbourne?

The Bank of Melbourne1 is a division of Westpac Banking Corporation, one of the big four banks in Australia. Westpac3 acquired the Bank of Melbourne in 1997 and relaunched them as a local brand in 2011. Despite being owned by Westpac bank, this Melbourne bank operates as a stand-alone business, with its own brand and management team.

Is the Bank of Melbourne a good bank?

As with any financial institution, there exist both positive and negative customer opinions of the Bank of Melbourne. However, overall, The Bank of Melbourne has a good reputation and they are generally well-regarded in the Australian banking industry. They have won several awards for their products and services, including winning Mozo’s4 award for an Excellent Banking App. They offer a range of products and services, including home loans, credit cards, savings accounts, personal loans, and business banking.

Despite their awards and goodwill, it’s important that new customers carefully review and compare the bank’s products and fees with other banks before making any decisions. Additionally, it’s always a good idea to read reviews from other customers and seek advice from financial professionals before opening an account or taking out a loan.

How many Bank of Melbourne branches are there?

While The bank of Melbourne doesn’t explicitly state the number of branches they have on their website1, they do assert that their goal is to grow to over 100 branches (with 300 ATMS) in the next five years, implying the current number of branches is less than this.

Compared to the Big 4, which have between 550-800 branches each, 100 branches isn’t a lot. If you’re a Victorian resident looking for a bank, and you like to do your banking in person, it would be wise to check that there is a branch location near you before opening an account with the Bank of Melbourne.

Is the Bank of Melbourne a safe bank?

The Bank of Melbourne are subject to the regulatory oversight of the Australian Prudential Regulation Authority (APRA), which oversees various aspects of a bank’s operations including risk management, capital requirements, liquidity, and governance, thus ensuring banks have sufficient financial resources, management systems, and controls in place to manage risk effectively and maintain financial stability. The bank is also a member of the Financial Ombudsman Service (FOS), which provides dispute resolution services for consumers.

“We take the protection of our customers personal and financial information very seriously. We have rigorous security measures in place, as well as security teams working to protect our customers details and accounts. Our Fraud and Scams teams are monitoring 24/7 for any suspicious activity, using industry best practice security and fraud detection techniques.”

bankofmelbourne.com.au/online-services/security-centre1

Additionally, as discussed earlier, the Bank of Melbourne are owned by Westpac, which is one of the largest banks in Australia and has a long-standing reputation for financial stability and security. The Bank of Melbourne also offer deposit protection for eligible deposits up to $250,000 under the Australian government’s Financial Claims Scheme (FCS)5. In layman’s terms, if the Bank of Melbourne were to fail, depositors would be able to recover their deposits up to this amount.

The FCS is designed to promote confidence in the banking system and protect depositors’ funds, which are a critical source of funding for banks.

Based on these factors, the Bank of Melbourne can certainly be considered a “safe” bank to manage your money. However, with any financial institution, there are always risks involved and it’s important to be informed about the products and services you are using and their associated risks.

What kind of accounts does the Bank of Melbourne have?

The Bank of Melbourne offer a range of industry-standard bank accounts1 and products. Some of the most common account types offered by the bank include:

➢ Transaction Accounts designed for everyday use, allowing customers to deposit and withdraw funds, make payments, and manage their finances.

➢ Savings Accounts to help customers save money and earn interest on their balances.

➢ Term Deposits, a type of savings account that offers a fixed interest rate over a set term, typically ranging from 1 month to 5 years, with a possible bonus interest rate on top as well.

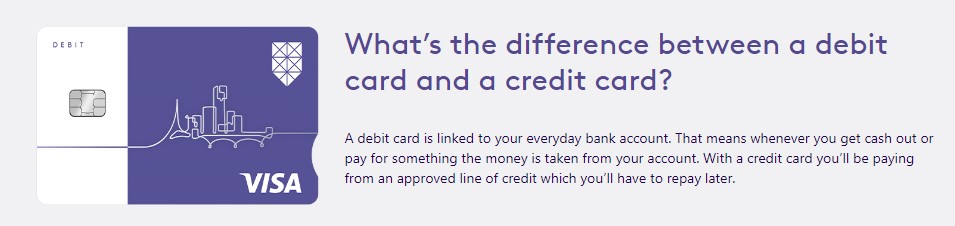

➢ A range of credit cards with different features and benefits, including rewards programs, interest-free periods, and low annual fees, and a Visa debit card for use online, in stores, over the phone and at ATMs.

➢ Several home loan options, including variable rate, fixed rate, and line of credit home loans, as well as construction and investment loans, most with an offset account available.

The above are the standard products and account types offered by the Bank of Melbourne, but they also offer other types of accounts, such as business accounts and personal loans, depending on the needs of their customers.

Does the Bank of Melbourne have an App?

For those customers less concerned with branch locations and more interested in the convenience of online banking, the Bank of Melbourne do have a mobile banking app for both iOS and Android devices. The app allows customers to perform various banking tasks such as checking account balances, transferring funds, paying bills, and locating ATMs and branches.

Customers can also use the app to view their transaction history and manage their account settings. To download the app, customers can visit the App Store or Google Play Store and search for “Bank of Melbourne.”

Advantages of using the Bank of Melbourne

There are many perks to banking with the Bank of Melbourne, including:

➢ A growing network of branches and ATMs throughout Victoria, making it easy for customers to access their accounts and conduct transactions.

➢ Competitive interest rates on their savings accounts and home loans, helping customers to maximize their returns.

➢ Digital banking services, including online banking and a mobile app, allowing customers to manage their accounts and conduct transactions from anywhere, at any time so long as they have an internet connection.

➢ A full range of financial products and services, including personal and business banking, credit cards, insurance, and superannuation.

➢ The Bank of Melbourne are committed to supporting the local community and sponsors a range of events and initiatives across Victoria, which can help customers to feel good about banking with a socially responsible institution.

➢ A serious approach to the security of its customers’ accounts, using industry-standard encryption to protect their data. The bank also offer a range of security features, such as two-factor authentication6 and biometric login, to help keep customers’ accounts safe.

“As your local bank, our team will work with you to find the way forward. We want to see your ambition – modest, medium or sky–high – become a reality. We do this through our dedication to customer service, by being small enough to get to know you so we can plan together, with our network of branches and our handy mobile banking app.”

bankofmelbourne.com.au/about1

Disadvantages of using the Bank of Melbourne

Like most things in life, the aforementioned pros aren’t without their cons. Some potential downsides to banking with the Bank of Melbourne include:

➢ No branches or ATMs outside of Victoria, which may not be convenient for customers who travel frequently or live outside the state.

➢ Fees for certain transactions, such as ATM withdrawals or international money transfers, which could add up over time.

➢ Some customers have reported issues with the Bank of Melbourne’s customer service, including long wait times and difficulty reaching a live representative.

It’s worth noting that not all of these factors may be relevant to everyone and many customers may find that the advantages of using the Bank of Melbourne outweigh any potential disadvantages.

FAQs about the Bank of Melbourne:

The Bank of Melbourne have many Frequently Asked Questions (FAQs), which are common amongst most banks, including questions about opening and accessing accounts online, the fees they charge, reporting lost and stolen cards and how to contact their customer service.

If you have a question for The Bank of Melbourne, you can contact them here.

Is the Bank of Melbourne good for home loans?

While the Bank of Melbourne offer an array of home loan products with potentially lucrative interest rates, whether or not they are the best selection depends on the needs and circumstances of each customer. If you’re searching for a home loan provider, ensure you carefully consider factors such as interest rates, fees, loan features and the customer service available.

Additionally, it’s always a good idea to compare home loans from several lenders and consult with a mortgage broker or financial advisor before making any important financial decision.

Is the Bank of Melbourne good for VIC residents?

As the name implies, the Bank of Melbourne primarily serve Victorian residents. As such, their business is tailored to the needs and values of Victorians by way of accessibility of branches and ATMs, local knowledge and a strong community focus. By objective standards, this would make the Bank of Melbourne a reliable choice for most Victorians, however, the final decision for most customers will come down to how the bank’s specific products suit their individual requirements.

Can I open a Bank of Melbourne account online?

For most of the bank’s products, you can certainly open an account or apply for a product online. Simply navigate to their website, use the drop-down tabs at the top to select the product you’re interested in, click on it and after doing your own due diligence, press the “open now” or “apply now” button. Whether or not you will have access to the product immediately following your application will depend on the specific product you have applied for, and several other factors including current postage times and customer service wait times.

Does the Bank of Melbourne have ATMs?

Yes, the Bank of Melbourne have a network of ATMs across Australia available to their customers. Bank of Melbourne ATMs can be used for transactions including withdrawals, deposits as well as balance inquiries and more. Bank of Melbourne customers can also use ATMs operated by other banks in Australia and around the world, although additional fees may apply for using non-Bank of Melbourne ATMs.

Conclusion

The Bank of Melbourne are a highly regarded bank that offer a range of services to meet the banking needs of Victorians. While there are certainly advantages to banking with them, including their community focus and competitive financial products, there are also some downsides, like potentially high fees and some reported customer service issues. Whether the Bank of Melbourne are the right choice for you depends on your individual requirements, values and goals, but it may be worthwhile to explore their products and compare them to those of other financial institutions.

Do you have a bank account with the Bank of Melbourne, or would you consider them for everyday banking? Why/why not?

Further reading – other Bank reviews

Check out my list of bank reviews here to see how the competition stacks up, and to find the right bank for you..

- Commonwealth bank

- NAB Bank

- ANZ Bank review

- Westpac Bank review

- ME Bank review

- ING Bank review

- UBank review

- HSBC Bank review

- Up Bank review

- 86400 Bank review

- Finspo review

- Spriggy review

Financial Disclaimer

Financial Disclaimer: CaptainFI is NOT a financial advisor and does not hold an AFSL. This is not financial Advice!

I am not a financial adviser and I do not hold an Australian Financial Services Licence (AFSL). In this article, I am giving you factual, balanced information without judgment or bias, to the best of my ability. I am not giving you any general or personal financial advice about what you should do with your investments. Just because I do something with my money (or use a particular service or platform) doesn’t mean it is automatically appropriate for your personal circumstances.

I do not recommend nor endorse any financial or investment product, and my usage or opinion of any product should not be interpreted as an endorsement, advertisement, or intent to influence.

I can only provide factual information based on my journey to Financial Independence, and that is provided for general informational and entertainment purposes only. I make no guarantee about the performance of any product, and although I strive to keep the information accurate and updated as it changes, I make no guarantee about the correctness of reviews or information posted.

Remember – you always need to do your own independent research and due diligence before making any transaction. This includes reading and analysing Product Disclosure Statements, Terms and Conditions, Service Arrangement and Fee Structures. It is always smart to compare products and discuss them, but ultimately you need to take responsibility for your use of any particular product and make sure it suits your personal circumstances.

If you need help and would like to obtain personal financial advice about which investment options or platforms may be right for you, please talk to a licensed financial adviser or AFSL holder – you can take the first steps to find a financial advisor by reading this interview, or by visiting the ASIC financial adviser register and searching in your area. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Reference List:

- https://www.bankofmelbourne.com.au/

- https://www.apra.gov.au/

- https://www.westpac.com.au/

- ‘Banking Apps & Tech 2022 Mozo Experts Choice Awards’, Mozo. Accessed online at https://mozo.com.au/expertschoice/banking-apps-tech on Feb 21, 2023.

- ‘Financial Claims Scheme’, APRA. Accessed online at https://www.apra.gov.au/financial-claims-scheme-0 on Feb 21, 2023.

- ‘Multi-factor authentication’, Australian Cyber Security Centre. Accessed online at https://www.cyber.gov.au/mfa on Feb 21, 2023.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.