Blackrock iShares USA S&P 500 (ASX:IVV) ETF review by a personal finance expert and long term investor.

IVV is one of iShares (by BlackRock) most popular ETFs – which tracks the total US market. IVV seeks to track the investment results of large-cap US stocks against the S&P US 500 index. This particular fund is domiciled in Australia (ASX:IVV), and has over (AUS) $3.2 Billion under management in it. Because it’s domiciled in Australia (switched from a cross-listing to a dedicated local Australian ETF in 2018), Australians won’t have to submit any foreign tax forms to the US (like you need to with Vanguard total US market ASX:VTS ).

The Good

- Australian Domiciled fund

- More clear estate planning implications

- Has Dividend Reinvestment plan

- Holds 500 biggest USA companies

- Doesn’t require a W8BEN form

The Bad

- Only tracks 500 US companies rather than the ‘whole index’ of 3601 investable companies like VTS

- Higher management fee than Vanguard VTS

- Companies are picked by an S&P committee to represent US large caps, so large companies could still be excluded.

Verdict: Blackrock iShares USA S&P 500 (ASX:IVV) tracks the top 500 companies in the US share market, and is a simple way for Australians wanting to get US exposure.

CaptainFI is not a Financial Advisor and the information below is not financial advice. This website is reader-supported, which means we may be paid when you visit links to partner or featured sites, or by advertising on the site. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Blackrock investments

Blackrock is an American global investment management corporation based out of New York and is one of the world’s largest investment asset managers, with over (USD) $6.84 Trillion in assets under management as of 2019. They operate globally in over 100 countries, and their largest division is iShares – a group of over 800 exchange traded funds, which is the largest ETF provider in the world, beating Vanguard for the top spot.

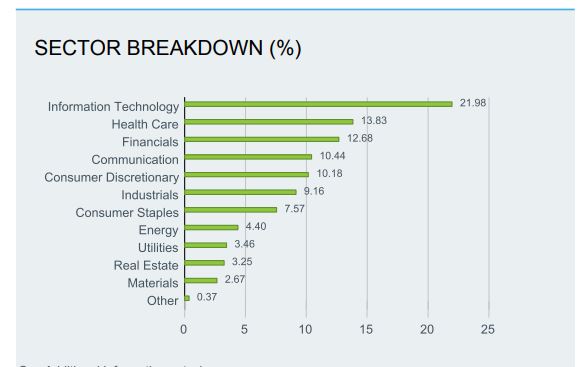

The Top ten holdings of IVV are Microsoft, Apple, Amazon, Facebook, Berkshire hathaway, Alphabet (google), JPMorgan Chase, Johnson and Johnson and Visa, which combined account for 21.57% of the total portfolio. This demonstrates the portfolio diversification, despite the naysayers which coo the absolute opposite. The Management fee is a ‘black’Rock bottom at .04%, matching the Vanguard fund VTS.

The S&P 500 index incorporates approximately 77% of all publicly traded US securities (companies). IVV aims to fully replicate the index, which has a minimum market cap of around $5B. This means IVV might do slightly better if small caps are struggling such as in a bear market, or otherwise, it should go down less, compared to managed funds or ETFs that hold more smaller capital securities.

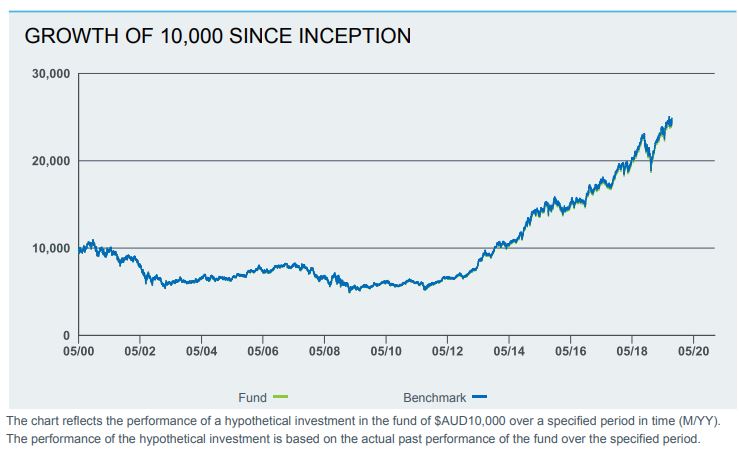

As of October 2019, over the past year IVV has returned 10%, over 5 years 17.43% and since inception (20 years – including GFC) the return was 4.78%.

The dividend yield on IVV is currently at 1.66%, so it’s clear that the IVV ETF is more suited for a Boglehead style investor looking for capital gains, than a Thornhill style dividend investor looking for increasing dividend income.

To fully live off this stock, you would need to sell down portions of it in retirement (and if you held this over 12 months, you would receive a 50% CGT reduction).

IVV gives me exposure to the US S&P 500 at an incredibly low price. It has very good liquidity with approximately 800M+ shares trading hands each day.

Whilst I don’t get the same juicy dividends or franking credits that chasing Aussie shares would give me, IVV gives me great global exposure to some of the biggest US companies which provide long term passive capital gains.

I plan to cash in on this later, and potentially sell off these shares for future spending money in retirement (noting that after holding these shares for 12 months, you are eligible for a 50% reduction in payable capital gains tax in Australia).

IVV and VTS are essentially the same thing, or rather, they give investors a similar amount of exposure risk to the US – they both broadly track the US stock market index. There are a few slight differences between the two (explained below and them summarised in the video).

Whilst they are both broadly speaking US stock market index funds, the BlackRock iShares IVV ETF tracks the S&P 500 (top 500 stocks – blue chips) wheras Vanguard VTS ETF tracks the CRSP US total market index (about 3500 stocks, but heavily weighted to the blue chips because it’s weighted by market cap).

Another consideration in the IVV vs VTS debate is estate tax and inheritances. Because VTS is a cross listed fund, you will need to fill out a W-8BEN-E tax form for the IRS and there can be some complications where the US will actually tax your estate when you die, which obviously isn’t ideal for overseas investors. It’s worth exploring this little complication, and this is not an issue for the BlackRock iShares fund IVV, which is domiciled in Australia.

Furthermore, since IVV is domiciled in Australia, you can participate in a Dividend Reinvestment Plan (DRP) which for some investors helps to simplify and put their investing on autopilot. This feature is not available to the VTS fund; potentially reflected in Management Expense Ratio (MER) difference of IVV being .01% more expensive.

Why not have both!?

I have no problems whatsoever holding both funds, and I figure they are essentially the same thing. My thinking was then that I have decided to buy US stocks (because Aussie stocks are too expensive and the Aussie dollar is high), I will just buy which ever one has dropped in value the most lately and therefore I’ll pick up slightly better value. What do you think? Have you made the choice between VTS or IVV?

*Edit I have since rolled my IVV holdings over into VTS due to the lower management fee and broader diversification, despite estate taxes, filling out the W-8BEN-E form for the IRS and there being no DRP*

Summary

To wrap up, IVV is an incredibly simple fund. It’s just a straightforward S&P500 index tracker, with an incredibly low MER of .04%, a DRP option and a large amount of money under its management. It automatically buys or sells companies based on changes to the Standards and Poors S&P500 index, and will keep doing so, slowly ticking away in the background. As an Australian domiciled fund, it makes getting US share market exposure more clean for Aussies in terms of estate planning (what happens if you die) and you can also elect to use a dividend reinvestment program rather than receiving cash dividends.

Addendum

27th April 2020: I have since sold my holdings of IVV, and now purely invest in the Vanguard VTS ETF for exposure to US stocks. This is because of the lower management fee and wanting to simplify my investment portfolio!

1st April 2022: I no longer manually purchase shares and have my investing Automated between a split of three ETFs, effectively removing any purchase point decisions.

Financial Disclaimer

Financial Disclaimer: CaptainFI is NOT a financial advisor and does not hold an AFSL. This is not financial Advice!

I am not a financial adviser and I do not hold an Australian Financial Services Licence (AFSL). In this article, I am giving you factual, balanced information without judgment or bias, to the best of my ability. I am not giving you any general or personal financial advice about what you should do with your investments. Just because I do something with my money (or use a particular service or platform) doesn’t mean it is automatically appropriate for your personal circumstances. I do not recommend nor endorse any financial or investment product, and my usage or opinion of any product should not be interpreted as an endorsement, advertisement, or intent to influence.

I can only provide factual information based on my journey to Financial Independence, and that is provided for general informational and entertainment purposes only. I make no guarantee about the performance of any product, and although I strive to keep the information accurate and updated as it changes, I make no guarantee about the correctness of reviews or information posted.

Remember – you always need to do your own independent research and due diligence before making any transaction. This includes reading and analysing Product Disclosure Statements, Terms and Conditions, Service Arrangement and Fee Structures. It is always smart to compare products and discuss them, but ultimately you need to take responsibility for your use of any particular product and make sure it suits your personal circumstances. If you need help and would like to obtain personal financial advice about which investment options or platforms may be right for you, please talk to a licensed financial adviser or AFSL holder – you can take the first steps to find a financial advisor by reading this interview, or by visiting the ASIC financial adviser register and searching in your area.

For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Hi CaptainFi thanks for the article. I actually prefer VTS due to the lower management fee and since they are the pretty much the same thing I’m going to go for the lower cost fund any day of the week.

G’day @StartingFIRE, thats kind of what I was thinking too – at the end of the day we can’t control the market – only the fees we pay along the way. I think both VTS and IVV are fantastic products though, so I don’t have any issues owning both. I kind of like that I have each of the two dominant players in the financial game.

Hi Captain FI – My inclination towards IVV is purely due to estate tax. Also IVV gives flexibility of reinvesting divideds (although we might not see much of it post covid but who knows)

Hey Maz, those are actually both massive points that I didn’t really cover in the article, I am going to put this comment up into the body of text! I guess for me personally I haven’t really considered estate tax and inheritance considerations – from reading a bit more online this is an important issue for a lot of people, especially when choosing a US ETF fund. Also the dividend reinvestment plan DRP is a big requirement for a lot of investors. Personally I get a little rush when I see the dividends being deposited into my brokerage account, and I enjoy figuring out where to direct them next with my monthly investment decisions. Do you think its better to simply use a DRP and instead rebalance once a year or so? How frequently do you rebalance?

Hi CFI, would now be a better or worse time to buy IVV or VTS with the aussie dollar trading low. However could this be offset by the lower price per share? Would love to hear your thoughts

Hey Dan thats a great question – I have found myself sitting on the fence with international shares ATM and been loading up on A200 and MLT, but I know this is a form of ‘timing the market’ which I may regret later, so I think I will force myself to buy some VTS on the next pay cycle just to keep it growing in proportion to the aussie shares I hold. I haven’t reached the stage where I am doing asset allocation seriously enough to sell aussie shares to buy international, but it is a consideration. I think its a good reminder to buy some international shares despite the performance of the AUD, but it would certainly be an easier decision if we were at parity I would say 🙂

Hey there

So if I buy IVV ETF today and keep buying every month for 20 years, when I cash out I pay CGT on interest at 50%?

Thannks

Hi mate, I am not an accountant or financial advisor so take this with a grain of salt, but my understanding is that stocks you hold for over 12 months (in aus) will get a 50% CGT reduction. Youll have to pay tax on your dividends (income tax) if they are in your name, and then if you ever sell the shares you take your sale price, minus cost base, half it and then add it to your income for income tax purposes. Hope that helps