It is well into January so a Belated Happy New Years is in order! Earlier this week I was typing this up however I was delayed because I spilled a boiling hot bowl of MiGoreng (Ramen noodles) all over myself and my keyboard. I had to jump in the shower and I needed a new keyboard but all I could really do was laugh at how much of a dumb-ass I am. Accidents happen and you can’t really control most things, but you can control how you react to the situation.

2019 in review

2019! What an incredible year. I visited and worked in 14 different countries, racking up over half a million kilometres travelled by air in the process. I started this website (as well as a few others), began my first property development and jointly started two businesses (Digital marketing and Property Management). I started social media management for CaptainFI as well as three other websites in the portfolio, all of which have an amazing viewer base which is slowly growing and getting some fantastic organic traffic thanks to the detailed content and reader base interaction.

I learnt a lot through two gruelling semesters of graduate university study, as well as multiple online courses on Marketing, Property and Finance. I spent time with the amazing Miss FI – which she says stands for Miss FINE because she is so damn fine… or should that be FINE because girlfriends are expensive?!?

I grew a fantastic balcony garden which is providing me with handfuls of amazing fresh produce every day (saving me money on groceries). I also managed to grow my Net Worth towards FI by over $130,000 through disciplined, regular investing in the stock market through ETF stock and a market which somehow just kept going up.

Unfortunately we have seen some horrific weather conditions as bone dry and super hot air circulates around Australia’s deserts before eventually pushing onto the coast. Because of how dry its been with the drought over the past years there is shit loads of tinder dry fuel all through the scrub and this unfortunately has lead to an unprecedented level of severe bushfires throughout the state. This is not just limited to New South Wales, and my family throughout the country have all been impacted by the bushfires, particularly in Victoria, New South Wales and Victoria.

The last few weeks in particular have been pretty scary, with people just down the road from family in both NSW and SA losing homes just up the road. After spending many days in a fireproof suit waiting to put out ember attacks, the current cooler weather is a bit of a reprieve. Travelling home (driving interstate) there was some sombre sights, including a lot of dead animals as well as escaped livestock forming a traffic hazard. The latest estimates show that 500 Million animals have been killed directly as a result of these fires (which is about double the amount killed everyday by humans for consumption… If that doesn’t sit right with you perhaps check out how a whole food plant based diet will make you wealthier)

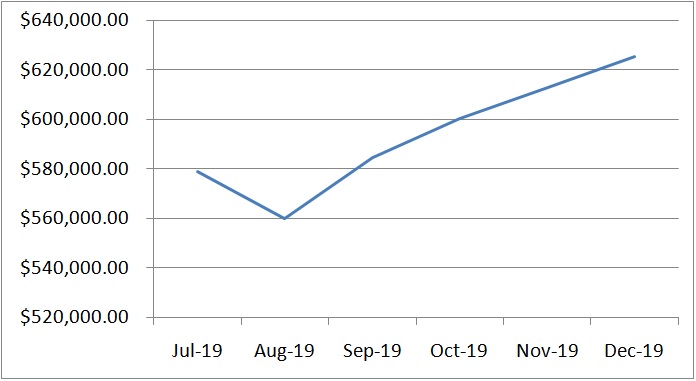

Net worth

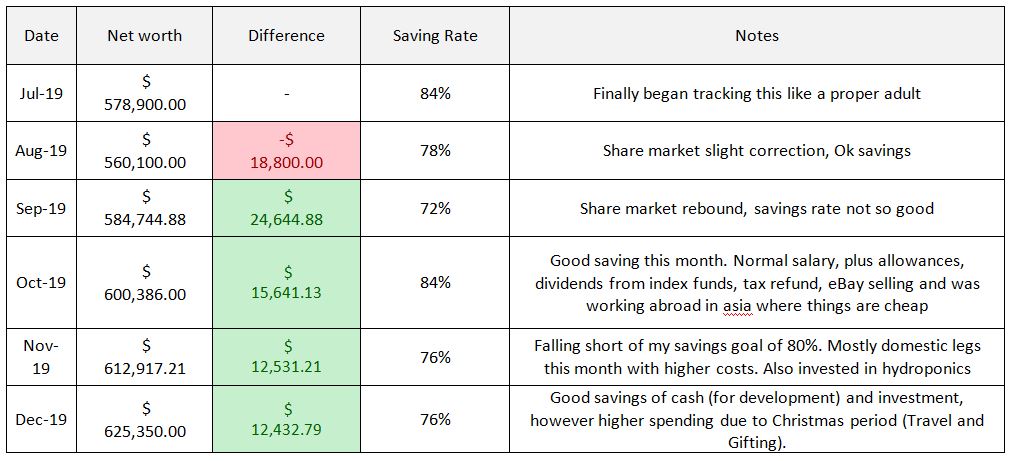

The Net worth this month has still managed to climb despite some recent drops in the market, coming in at a figure of $625,350 with a savings rate of 76%.

Unfortunately I did not reach my FI goal of a 80+% savings rate this month, which was due to some higher expenses such as Christmas travel and increased spending/Gifting on holiday (which I am totally cool with and had an amazing time back home). It was annoying to see it almost reach $640K earlier in the month and then drop, so I think I will limit myself to only calculating this at the end of the month for this segment. I have to set myself limits or this becomes a borderline obsession.

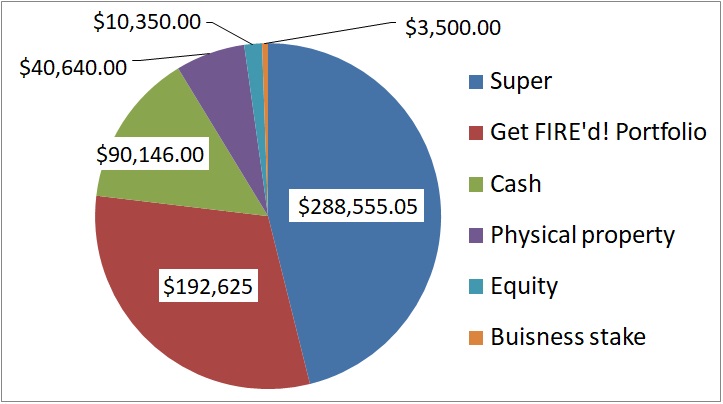

The breakdown is shown below as a split between investing in the Get FIRE’d! Portfolio, Superannuation (Australia’s version of a 401K / Individual Retirement Account scheme), Cash, Physical property (possessions), Equity in a duplex and a business stake (property management company).

As you can see from the graph below, all areas have increased slightly as I continue to work towards my goal of reaching Financial Independence. I have continued to split my income between a high interest savings account (HISA) and mortgage offset and investing in index funds. Some of the cash from my HISA is now being drip fed into the construction process which is reflected in an increasing Equity share of the duplex.

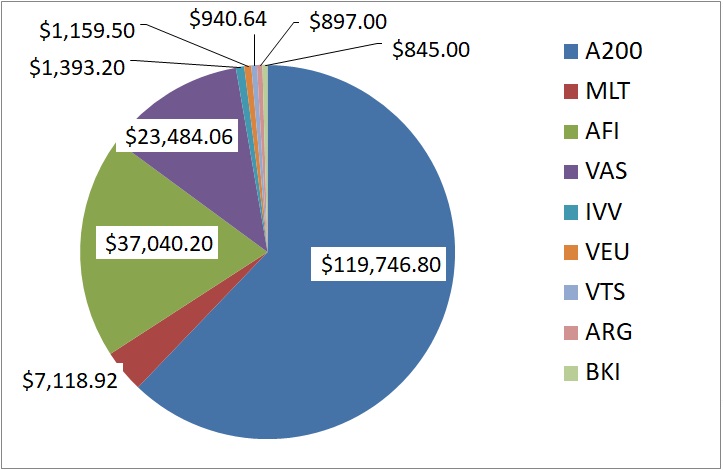

Get FIRE Portfolio stock investing

Despite investing $3K this month into Milton Corporation (ASX:MLT) stock , Mr Stock Market has decided to only give me a $1900 raise to the Get FIRE’d Portfolio – So where did the $1100 go?! Just Kidding, This is OK and is very normal due to volatility. I’m happy because my investment reasoning is solid – I am sticking to my plan of ‘DCA the Dip and Hold’. If these investment strategies are good enough for Warren Buffett, its good enough for me!

This money will likely come back as the stock market swings and fluctuates anyway, but ultimately though the capital value of the stocks doesn’t really matter much to me. What does matter to me is the growing dividends and compounding returns, which account for statistically nearly ALL of the long term wealth generated in the stock market. ETF dividends are a crucial factor for reaching FI (If you don’t understand this, a quick Google of John (Jack) C. Bogle and his economics research can help you).

Investing Decisions

The Investing decisions this month were pretty bog standard. And ultimately that is what getting rich slow is all about; boring, repetitive and thoroughly unexciting behaviours.

The winning stock for me this month was Milton Corporation (ASX:MLT stock ticker for Aussies), because I got it for 3% discount delta (further discount under its regular discount) to its Net Tradeable Assets / Net Asset Value (NTA/NVA).

Milton is an Aussie listed investment corporation which mostly tracks the stock market index but is slightly heavier on financials (off the top of my head). Now before you all bash me again about Milton under performing the Index, I’ll just say that past performance is no prediction of future performance. I think it has as as good of a shot as any to achieve the Index performance, and taking a sweet discount buying the stock makes it much more attractive to me. I may even sell these LICs in the future when they tick over to being sold at a premium rather than discount (of course, after holding for 12 months to achieve a 50% Capital Gains Tax discount). I would then shuffle this money into whatever was at a discount at the time, or otherwise into bog standard Index fund ETFs.

The other half of this months investment decisions was CASH. This is NOT because I am predicting a crash or hoarding currency for the upcoming Apocalypse! I am needing to have cash on hand for the Duplex build, as we need to drip feed it into the builders (I am learning a lot about the process as this is my first development, but my takeaway so far is essentially none of it makes sense and everyone tries to screw you). So whilst the Cash reserves have increased, the amount that is needed is now covered and all future paychecks will be directed straight into the market to try and achieve my goal of a $3000 purchase of index fund ETFs and LICs every fortnight.

Property

As discussed above, money has started drip feeding into the build of the Duplex on the NSW Central Coast. The Land has been settled on and most of my equity is just in the land value on a 95% LVR deal. The surveys have all been completed (exciting to see the little flags everywhere) which marks the first stage of setting the foundations. I am enjoying playing around with mortgage calculators and home loan calculators almost as much as I like investing in the stock market now. More ‘Developments’ to come on this as it happens, but I am pretty excited for some stable dry weather which will let the concrete cure optimally.

The recent bushfires have led me to think more about insurance, particularly fire and heat damage insurance, and I will write more about it when I have a better understanding and have completed insurance contracts for the property.

Superannuation

Nothing juicy to add here. Approximately $700 in contributions to my superannuation as well as growth within the fund which has seen it rise by approximately $1821. At the end of the financial year I will review this and see how it performed against my expected performance.

Budget and Expense Tracking

OK so coming in with a slightly disappointing 76% savings rate this month has meant again I have fallen short of my 80+% savings rate goal. Whilst frustrating, I am more mindful than ever on where I spend my money, so its important to put this rate into perspective. December had a lot of expenses due to interstate Travel, and increased leisure and gifting. I also spent more than half the month working in the US, where the cost of living as a tourist (Restaurants, Food, Beer!) is much higher than at home. I still feel like this hasn’t been the most successful month towards FI, but its the best I got right now.

Income

Income was a combination of my flying salary, Allowances, Side Hustle and Bank interest. No stock market dividends from investing this month (unfortunately) but they will come in time. The Side Hustle income mostly came from selling items on eBay and FBMP, but I also made a record breaking $.01 on AdSense! ?

In all seriousness though, I have configured AdSense for this website to help cover the costs of Domain registration and hosting. This helps me grow the site and keep providing you with content without a financial penalty, and fits in line with my investment strategies. If its really pissing you off please let me know in the comments below, because if enough of you complain I will just turn it off – its not worth inconveniencing all of you for a couple of cents.

I recently tracked my income and actually worked out I have 12 streams of potential income

- Flying Salary

- Company meal / overnight Allowances

- Casual Flying Instruction

- Website portfolio income (adsense and affiliates)

- Property Management Business (Air BnB)

- Share dividends (Get FIRE’d! Portfolio)

- Rental income (still under construction)

- Arbitrage (buying and selling)

- Bank interest

- Intellectual Property (Rights) to my Book and courses

- YouTube revenue (waiting to reach threshold size)

- Digital Marketing (website creation and ongoing SEO services)

Diversifying your income stream is one of the most important things I have learned from reading finance books and the courses I have completed over the past few months.

Spending

Spending this month was my usual staples such as Rent, Petrol and vehicle registration, but also included a much higher cost of food due to time spent working in the US and living/eating like a tourist on an unfavourable exchange rate. I spent approximately $1000 (AUS) over two weeks which was just insane for me, but this was partly due to terrible exchange rates and long flights meaning late dinners out with my crew. I also indulged in a bit of touristy spending as I had never been to some locations before and wanted to make the most of it (snorkling, beach beers, local attractions and nightlife).

I also spent a significant amount of money ($800) on petrol this month during driving to visit family interstate for Christmas, racking up nearly 5000km on my old (but pristine!) station wagon’s Odometer. She just ticked up 105,000km at 14 years old! Thankfully I’m pretty savvy when it comes to my car, since I do all my own maintenance and drive a manual transmission. Overall ‘investing’ in that car has given me a great return… (just kidding folks, buying a car is NOT an investment unless your collecting vintage cars which go up in value and you can safely garage them in your mansion)

Giving

With the Christmas season I wanted to provide thoughtful gifts to family and friends, and with prior planning and mindful spending the total I spent on gifting was only $400 this year (which is down from the thousands in previous years). One of the ways our family has collectively achieved this is by implementing a ‘Secret Santa’ where you only end up buying one gift for someone else which really helps to cut down on all the waste and impulse spending on inappropriate gifts. Also due to the recent fires I donated $100 to the Australian Bushfire appeal, which hopefully will make its way to the bushfire victims and less fortunate.

Retirement Income estimations

Although I am actively working on building income streams through a web portfolio and multiple businesses amongst other things, the traditional share portfolio is doing the heavy lifting for the retirement income stream at the moment. The rental income will increase as rents gradually increase and the effect of inflation erodes the ‘value’ of the interest only loan on the property.

These two items will be my fall back during FI and provide the necessities of accommodation, food and the like in early retirement. Whilst it isn’t much at the moment, a continued focus on building up the investing portfolio over the next few years will help it provide a higher draw down factor prior to accessing my retirement account.

Stage one – Get FIRE’d! Portfolio

- 7% draw down over 25 years = $13,483 ($1,123/month), and;

- Rental positive cash flow: $1,440 ($120/month).

Stage two – Superannuation retirement account

- One time lump sum payout of $80755. Represents an investment opportunity to earn $3,230 ($269/month) at 4% sustainably forever.

- Superannuation annuity = $8,312 ($693/month), and;

- Social Security Aged pension = $18,122 ($1510/month)

Net Worth Table

Conclusion

So that closes it off for 2019. Looking forward into 2020, my goals are to continue towards FI by working hard and building flying seniority and increasing my pay at work, investing $3000 every payday fortnight into the stock market, and to continue working on my businesses, website portfolio and education in my down-time. 2020 is the year I want to turbo-charge my assets and investment portfolios to build up a higher retirement income and reduce my risk in early retirement. Thank you for being a part of my 2019!

Get FIRE’d!

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Wow that’s a really good NW, how old are you? Obviously in your 20s. I have no idea how you are able to make that much savings rate, I live in Sydney too and I barely have anything left over after I pay rent, bills etc. Do you just not leave the house??

Hi Karen, thanks for the encouragement. I guess I am just really mindful about how I spend my money and I still live like a uni student in some regards haha! I have a few articles specifically about how to save money on topics such as Mobile phone plans, Cars and transportation and Groceries. For example I used to spend almost $300 a week on luxury foods and whatever looked good at the shops; after transitioning to a predominantly whole food plant based diet that number went down to $40, and then after starting a decent veggie garden that’s down to $30 now! As far as never leaving the house haha I did laugh – its probably not too far from the truth. I travel the world for my job as a professional transport pilot, so month to month I might be hanging out in the USA, Dubai or Asia and its a lot of fun, I always try to pack in as much as possible and make the most of the opportunity. This means when I come home I am usually needing to recharge my batteries so a Book, glass of wine and a comfy couch is pretty appealing. I also love getting out on the downhill trails on my bike in the fresh air, hiking and camping and getting out in the garden… I guess they are all free or low cost activities which might help explain the saving rate! (I recently turned 28 by the way!)

Hey Buddy,

Really solid effort so far. Im 29 and been on a very similar journey for some years now. Been reading through your posts, curious as to what you FIRE number is?

Keep up the great work!

G’day Steve,

It’s an interesting one because the FIRE number can depend on so many things. My current lifestyle (which is pretty kick ass) translates to a FIRE number of $1668 per month, which at a 7% safe drawdown before I can access my super translates to about $310K of ETFs. Thats pretty insane, and living pretty frugal. Realistically, I know that there will likely be some additional costs and I might want to lifestyle inflate a little bit, so I am allowing for an additional $300 per week spend to reach ‘Fat FIRE’, which again corresponds at 7% to $533K of ETFs. I also have started property development to own some rentals to diversify, and these will be cash flow positive so provide some additional cash flow to live and capital growth on the units which I will likely eventually refinance to get a deposit on more rentals. I have chosen 7% initially as this is the rate I will draw down my taxable portfolio before I reach preservation age, with a safety buffer. I will likely also continue to work part time teaching people how to fly and running my other businesses so its entirely likely I will have a good chunk of it left over when I get my super payout and annuity which keeps me going to remaining 40 years!

Cheers,

Capt. FI