HostPlus super review from an experienced and long term investor on the path to financial independence. Is HostPlus superannuation the best super fund?

HostPlus is an Australian industry super fund with a choice of several investment portfolios. Established in 1987, HostPlus was originally created for people working in the Hospitality, Sport and Tourism industry, however it can be freely joined by anyone these days. It has more than one million members and $50 billion under management, giving the hostplus superannuation fund status as one of the largest super brands in Australia – Keep in mind, there are approximately 150 Australian super funds, that combined managed (AUD) $2,780 Billion in 2020 alone. This is incredibly big business.

HostPlus offer a wide range of super investment options, and have become one of the leading providers of index based superannuation investments. They also provide insurance products such as income protection, TPI and life insurance, however they also have some notable exclusions on these policies.

So, am I personally opening a HostPlus account, and what insurances am I taking out? Read on to find out!

The Good

- Focus on Low fees

- Index fund growth assets investment options

- Australian and International markets options

- High performer superannuation fund

- Easy to open an account and roll in funds

- One of Australia’s largest superannuation funds

The Bad

- Insurances have multiple exclusions

- Investment options confusing, misleading names

- Can’t access super funds until preservation

- Pooled fund: tax provisioning drag (10%)

- ‘Notional’ Investment option choice only

Verdict: The Host Plus superannuation fund is one of the best ‘pooled’ style industry superannuation fund options, but be careful of your investment choice option, and your insurance options. Make sure you thoroughly read the HostPlus product disclosure statement to confirm it suits your financial situation or needs before making any decisions.

CaptainFI is reader supported, which means we may be paid when you visit links to partner or featured sites

Introduction to the HostPlus superannuation fund

The hostplus superannuation fund is an Australian industry Superannuation fund that was originally built in 1987 for workers of the hospitality tourism and sports industries. They have had a pretty spectacular rise, and now let anyone join the fund. Because of this, they now have over one million members and manage over (AUD) $50 Billion worth of member funds. HostPlus has the status of one of the largest superannuation funds in Australia and has historically also been one of the best performing super funds.

The HostPlus industry super fund has reached massive public notoriety thanks to the Barefoot Investor, who previously worked for the company and their ‘Ka-ching Ka-ching educational programs. The Barefoot investor talks about the benefits of index-based superannuation products, and publicly praises HostPlus as well as explains that he uses HostPlus for his personal Super. This has been dubbed the ‘Barefoot effect,’ and he even got grilled about it during the Australian government Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry

Host Plus Indexed Balanced Fund

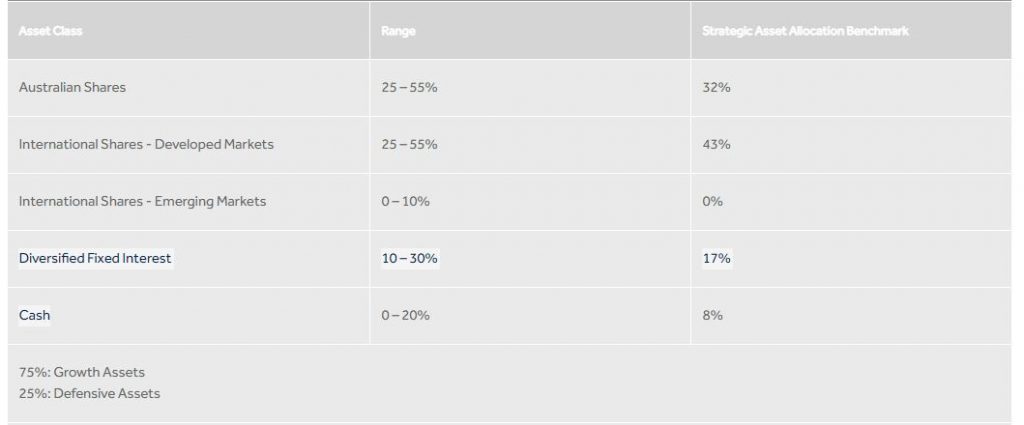

The HostPlus Indexed Balanced Fund is a ‘one size fits all’ pre-mix of asset classes that uses Index funds (ETFs) to build up the fund. This fund includes Australian shares, International shares, International emerging markets, Bonds and Cash, and currently has an asset allocation of 32% to Australian Shares, 43% to International Shares, 17% to Fixed Income and 8% to Cash.

The Hostplus Indexed Balanced Option provides members with an investment in a highly diversified portfolio that aims to achieve an investment return that closely tracks the index performance of each asset class of which it has exposure.

The Hostplus Indexed Balanced Option is ‘Passively Managed’, which means it contains no active management across any asset class. This provides members with a cost-effective means of accessing market performance across a range of asset classes.

HostPlus superannuation fund

The Indexed Balanced option is broken down into the current underlying funds

| Asset Class | Manager | Product | Benchmark | SAA |

| Australian Shares | IFM Investors | Enhanced Passive Australian Equity Strategy | S&P / ASX 200 Accumulation Index | 32.0% |

| International shares (hedged) | IFM Investors | Indexed Global Equities Hedged Strategy | MSCI World ex-Australia Index | 21.5% |

| International shares(unhedged) | IFM Investors | Indexed Global Equities Unhedged Strategy | MSCI World ex-Australia Index | 21.5% |

| Australian fixed income | BlackRock | Indexed Australian Bond Fund | Bloomberg AusBond Composite 0+ Year Index | 8.5% |

| International fixed income | BlackRock | Global Bond Index Fund | Barclays Global Aggregate Index (hedged in AUD with net dividends reinvested) | 8.5% |

| Cash | Citigroup | High interest earning at call account | Bloomberg AusBond Bank Bill Index | 8.0% |

The asset allocation within the index balanced fund can change, and HostPlus provide the following table to explain the allowable ranges the fund managers use, alongside the Strategic Asset Allocation Benchmark they are using.

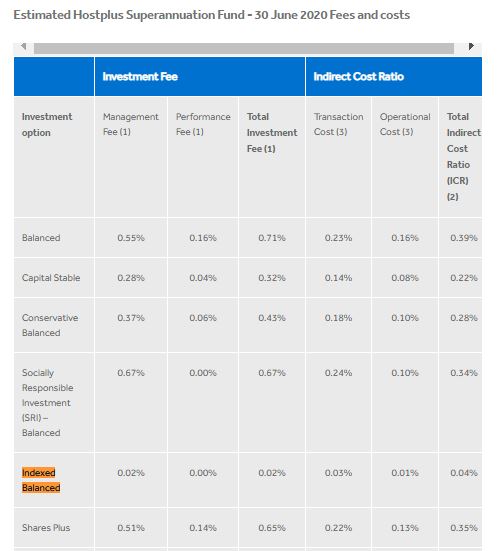

Fees: To invest in the Hostplus Balanced index fund costs .06% p.a., plus $78 per year ($1.50 per week)

The Indexed Balanced option has been specifically designed to be only exposed to asset classes which can be accessed very cheaply – such as Australian and International shares, fixed interest and cash.

HostPlus superannuation fund

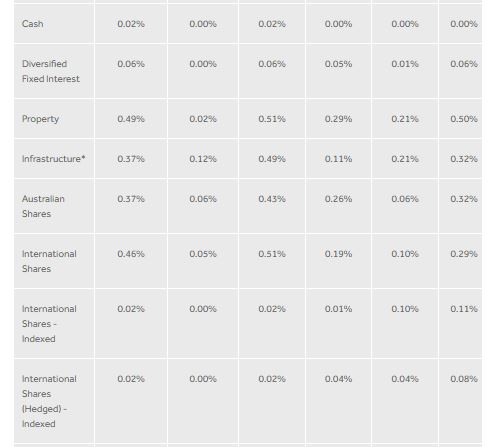

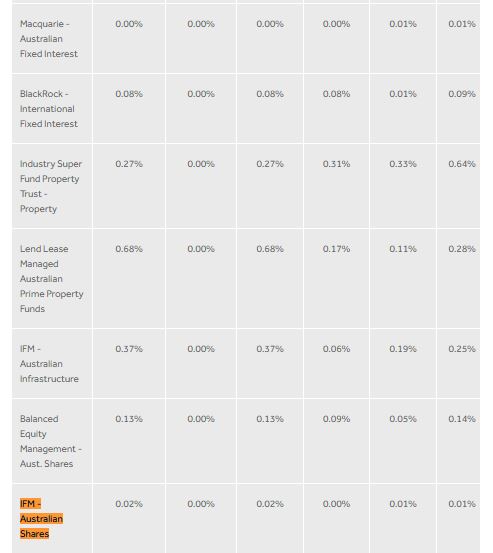

As at the 30th of June 2020 the Total Investment Cost for the Indexed Balanced Investment Option was 0.06% (0.02% investment fee and 0.04% Indirect Cost Ratio).

The trustee office has been able to negotiate extremely low and/or bespoke investment management fees due to our size and our solid relationships with these managers (across multiple asset classes).

Ensure you read the product disclosure statement pds at https://hostplus.com.au/self-managed-invest/your-tailored-investment-options/indexedbalanced

The Hostplus IFM Australian shares index fund is HostPlus’ Aussie index fund offering. Currently it is being offered incredibly cheap, and closely tracks the S&P ASX 200 accumulation index – making it similar to something like Betashares A200 fund.

“This option closely tracks the S&P/ASX 200 Accumulation index, and as such the portfolio composition closely resembles the weighting of the Top 200 ASX listed stocks by market capitalisation. As there is possibility for the fund manager to slightly deviate from the S&P/ASX 200 Accumulation index the investment style is described as “Enhanced passive management”.

HostPlus superannuation fund

Fees: To invest in the Host plus IFM Australian shares costs .03% p.a., plus $78 per year ($1.50 per week). Ensure you read the product disclosure statement pds

Host Plus International Index fund

The Hostplus International Shares – Indexed Option is managed by IFM, and tracks the MSCI World Index ex-Australia (unhedged).

“The Hostplus International Shares – Indexed Option’s underlying investment is the IFM Investors Indexed Global Equities Strategy. The portfolio invests directly in equity securities that are listed on stock exchanges in developed countries other than Australia.”

HostPlus superannuation fund

The mandate that Hostplus has with IFM in managing the IFM Indexed Global Equities Strategy applies a combined benchmark comprising;

- 50% MSCI World Index ex-Australia (unhedged in AUD with net dividends reinvested)

- 50% MSCI World Index ex-Australia (unhedged in AUD with gross dividends reinvested).

Fees: To invest in the Hostplus International Index fund costs .12% p.a., plus $78 per year ($1.50 per week).Ensure you read the product disclosure statement pds

HostPlus Super Fees and costs

HostPlus have some of the most transparent fees and costs I have found when researching super funds. Basically, they will charge you $78 per year in administration fees ($1.50 per week), plus whatever the Investment fees and costs are – these vary depending to your chosen investment option(s). As a breakdown, check out the following tables for the investment options and their Investment Fee and ICR’s are.

You need to read their Ensure you read the product disclosure statement PDS (https://pds.hostplus.com.au/6-fees-and-costs) carefully before making any decisions though

HostPlus super insurance policies

HostPlus provide insurance options policies through their superannuation – for example Total and permanent Impairment (TPI) and Life Insurance. There is actually a big list of exclusions for professions that HostPlus will not cover. Many professions such as Tradespeople, Bodyguards, Transport workers or those working with Dangerous goods aren’t able to get certain insurance cover through HostPlus – and this could be reason alone not to choose HostPlus. For example as a Pilot, I am able to get death cover (life insurance), however I cannot get TPI (TPD) cover through them. You need to check the exclusions list carefully, and consult with HostPlus about what the policy does and does not cover.

Honestly, I will just put it out there that you should talk to a professional about these, because everyone’s needs are so different. For example, if you have a low net worth or little to no savings, a risky job, significant debt or mortgage(s) to your name, and a number of dependents – then you probably might want to think long and hard about this kind of stuff. Whereas if you have a massive portfolio, little to no debt, and no dependents – then you probably won’t care as much.

As an example, I would say I fit into the latter description but through my other superannuation scheme and professional body, I still have the following insurances;

- Income protection insurance: “indefinite” period on base salary only (less overtime and trip allowances obviously) as required for treatment and rehabilitation. If I can’t return to flight duties, I can claim the next level which is TPI;

- Total and permanent Impairment : $110,000 per year income.

- Life (death) Insurance: $1.3M payout to my beneficiaries (currently this would get added to my estate and be divided between my parents and siblings).

Now I didn’t specifically pick or choose these figures, they actually were automatically calculated and ‘assigned’ based on my contractual terms of employment and the growing valuation of my defined benefit product. If I had a choice, I would choose NOT to pay for this level of cover and instead would prefer to save the premiums I would have to pay each month for this.

When I explored the HostPlus insurance options calculator, after completing the survey and entering my details the results shocked me to say the least. When I played with the calculator and coverage levels, I was able to tailor something a bit more reasonable to my circumstances. Bear in mind I am not taking out these policies (I can’t change my policies within the defined benefit scheme).

Also, be aware that many of us in the FIRE community have sizable investment portfolios and sources of passive income which are actually a form of ‘self insurance’ policy. You really need to critically analyse whether you actually need these policies or not – perhaps chatting with a qualified financial advisor might be able to help you decide.

HostPlus super Death insurance

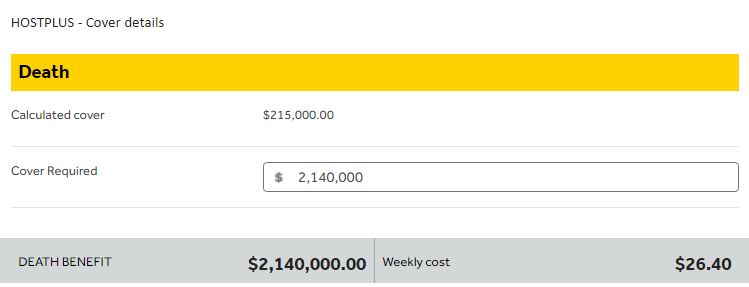

Firstly I played with the death (life insurance) cover calculator.

Firstly, It said my measly $1.3M death cover was not enough (despite me telling them I had no dependents and only a $370K mortgage on an investment property). They wanted me to crank this right up to $2.14M, and quoted $26.40 per week for this level of cover.

BRRRRT that’s a negative ghost rider – I would never take out a policy like this in my current situation. However, once I have kids though this is something I will consider – I would want this payout to go into the family trust with my wife and children as the beneficiaries.

It turns out HostPlus will not let you take out a death insurance policy that is lower than your TPI payout anyway, so you may end up with a higher level of cover than you want.

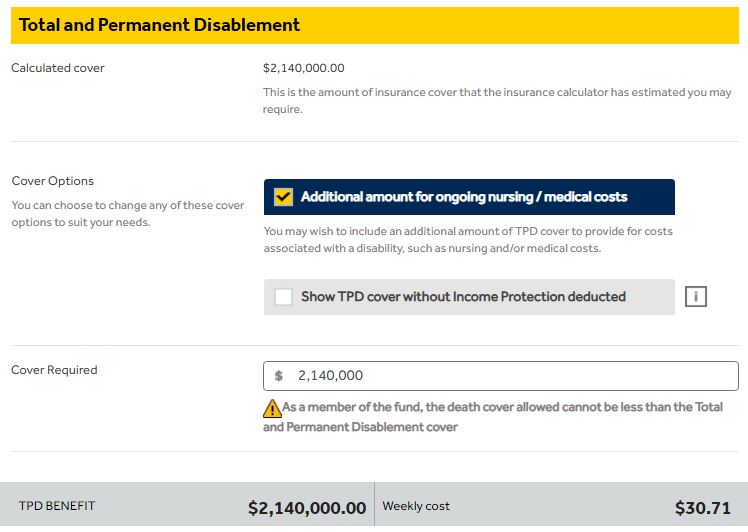

Hostplus super TPI insurance

Next was the Total and Permanent Disablement insurance (TPI or TPD). My current policy actually just has a $110K payment (salary) for the rest of my life which is the defined benefit/annuity, whereas HostPlus are quoting for a lump sum payout.

For my age (29 at the time), they suggest I need again $2.14M to tithe me over until I eventually died. This seems excessive but would cost an additional $30.71 per week.

Investing $2.14M into the family trust into index funds should produce an $85.6K income thanks to the 4% rule, which means my current insurance policy TPI that pays out $110K annually would be worth about $2.75M and so provides a higher level of cover.

I am not sure about what my costs of living might be like if I was seriously disabled, but it would damn sure be more than the $35K per year or so I am spending at the moment.

Hostplus superannuation fund Income protection insurance

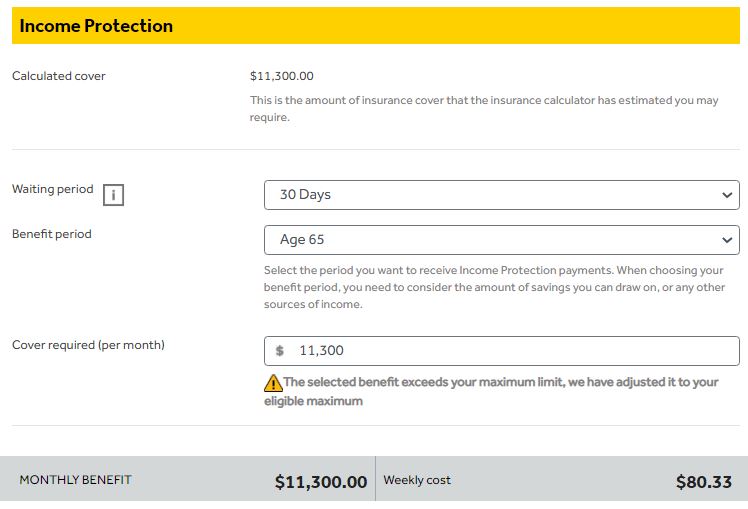

Finally I looked at income protection insurance, which to be honest is probably the most likely thing people will use of the three types of insurance available.

When I went for the recommended level of income, minimum waiting period and maximum benefit period (up until age 65). This then quoted me $80.33 a week for this cover which seemed excessive.

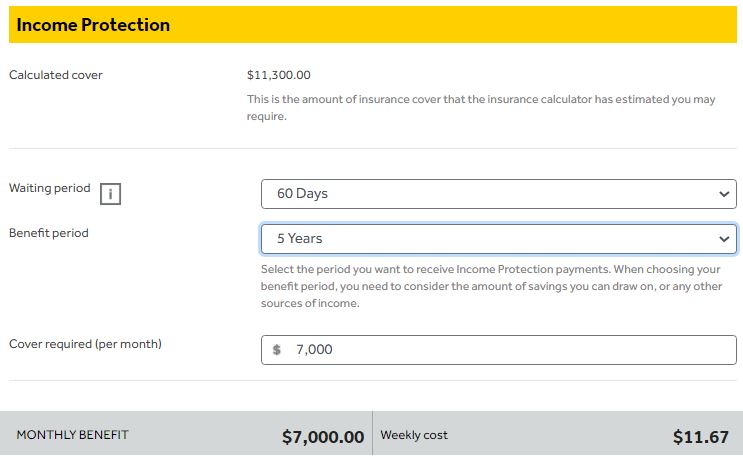

When I dialed it back to a more reasonable level of cover, a 60 day waiting period and only a 5 year benefit period the premium came down A LOT to a much more reasonable level. at $11.67 per week

To be honest, my first quote was probably a bit silly for a few reasons;

- Firstly I only really would need my ‘Family FIRE’ income figure (but not even that since my current portfolio provides a huge chunk of passive income anyway)

- Secondly my emergency fund would tithe me over the two month waiting period, and

- Thirdly having a benefit period of until age 65 seems silly because if that was the case you would either be claiming TPD or would have found another job!

How does HostPlus invest my super

Now, for those astute readers who did look up the PDS, will note something a bit fishy in chapter 5.3

This states;

“When you make a choice, HostPlus does not acquire an interest in the investment option on your behalf. Instead, you are notially invested in the investment option. As part of our investment strategy, we would have predetermined an amount to be invested with any particular investment manager. Therefore, we have pre-exsisting contractual relationships with our underlying invesment managers. We select managers and invest money with them via direct investment mandates or pooled trusts.

HostPlus Super, PDS Chapter 5.3

HostPlus Super then further expand on this with an example

“For example, HostPlus may have invested $10 million in Balanced Equity Management – Australian Shares. A member then exercises investment choice, and directs us to invest $10,000 of their account balance in that investment option. We do not invest a further $10,000 (on top of the $10 million already invested), but notionally allocate the net investment returns received from that investment option to the member’s account.”

HostPlus Super PDS, section 5

When I discussed this online on facebook, I was informed by a pretty switched-on mathematician Dr Sophie Montcrief who has a PhD in statistics, she actually outlined that this actually had some pretty big implications on how your money is actually invested;

“The key point here is that Hostplus do not actually invest your money in accordance with the option you choose in the PDS. Hostplus to give them credit tat least disclose this (although few would actually grasp the significance of the obscure paragraph 5.3). As Hostplus note, they have pre-existing arrangements with fund managers (Hostplus do not actually manage any money – its all outsourced).

These arrangements don’t change just because you elected to invest (for example in Australian shares). Your money gets tipped in with everyone else’s into whatever asset allocation arises from the fund flows and the arrangements with external fund managers.The odds of these two things aligning perfectly is close to zero – especially in the face of an avalanche of money from a Barefoot Investor recommendation.

This means that the overall return will not align perfectly with that which would have arisen if the money had been invested precisely in accordance with investors wishes. So some sort of divvy up will be required. How this is done is not disclosed. Given that the most important decision in driving long term return is asset allocation – it seems very strange to leave this bit to fate.”

Dr Montcrief

Of course, this promptly blew my mind. I did some more research into fund pooling which I found out was pretty standard – and then got back to Dr Montcrief asking for more information on pooling and its widespread use within the superannuation fund industry. She wrote back immediately with;

“Its no conspiracy – pooling is of course vital in lowering costs – this is why all publicly offered funds (and fund managers generally) pool our money so that a larger pool can be managed. With HostPlus it is different. It is how the pooling is done.

This would usually be achieved by allocating your investment to managers directly in line with your request ie if you invest $10,000 in the Aussie share option it would be given to an Aussie share manager to be managed in accordance with the relevant mandate as you would expect.

Hostplus don’t change their investment instructions (or allocate your $10,000) directly to an Aussie Fund manager (to invest in Aussie shares in the above example). They stick with their allocations which they change from time to time but not in direct response to your request to invest in Aussie stocks.

As a result, the overall asset allocation will be different from the sum of the choices made by members most the time. (that’s what paragraph 5.3 above says)

Dr Montcrief

So I cottoned on that this was a bit unusual, and wanted to know what are the implications for us all were. Dr Montcrief explained to me that;

“You just don’t get the return you were expecting from the asset allocation you lovingly crafted. Remember asset allocation is the number one driver of return. Hostplus benefit from simpler admin and an ability to claim lower fees.

Dr Montcrief

Dr Montcrief also explained to me privately that not all superannuation fund options do this – for example SunSuper and Colonial First State will invest your money directly into what you have asked for. She suggested though, that most of all of the big superannuation fund options run their pooling in a similar manner to HostPlus, however she credits HostPlus for being somewhat transparent and being one of the only funds to actually disclose this in their PDS.

Of course, I couldn’t just leave it at that, and so contacted HostPlus asking for a bit of an explanation when it came to their superannuation fund pools. This just didn’t seem right to me. I spoke to them on the phone for over an hour and got bounced between departments before finally being put on somehow to their legal team who explained for 30 minutes that she couldn’t provide me a verbal answer. thankfully though, they could write me a letter explaining the situation, but it would need to be approved by corporate before release. So here it is folks…

“CaptainFI,

Hostplus operates under a Pooled Investment Trust. This is where all money coming into the fund is pooled together and invested through our investment managers. This is an effective low-cost model that has been in operation for over 30 years.

The information in the Product guide is correct in that all money coming into the fund is notionally invested. Hostplus will allocate funds to a particular investment manager as required, However, you will receive the investment returns as per your investment choice.

In the PDS you will find the indexes the Indexed Balanced option tracks. These returns will be minus the investment costs and taxes – If you track the indexes, you will find they match up with returns. Whereas, super will generally also have taxes removed from the unit price, the pension unit values will be the actual return minus the investment costs only as there are no taxes in pension mode.

Any returns from the investment managers are also a part of the pool and the return is distributed through the entire 23 investment options based on the investment profiles for each of the investment options. Therefore, the performance of any of the investment managers do not relate to a particular investment option.

To directly invest funds as they are contributed from any source will significantly drive up the costs of using Hostplus – the pooled product and notionally investing the funds have been in use since industry funds first started with compulsory super.

During this time there has been many investment cycles and this form of investing has proven to be a cost-effective means of ensuring we get the best value and returns for our members.

Hostplus does not release the actual assets holdings of any of the investment options due business intelligence and intellectual rights of the investment managers Hostplus uses.

However, a list of assets Hostplus owns and can be found here: https://hostplus.com.au/super/about-us/investment-governance in the investment holdings tab.”

HostPlus Super Service Center

So there you have it boys and girls – HostPlus literally do whatever they want with your money, but they promise you that they will pay you out whatever you are ‘owed’ based on your particular chosen investment strategy.

Essentially, I think this means is that the fund managers at HostPlus think they are going to be smarter than you when it comes to asset allocation. For example, if everyone suddenly decided that they wanted 100% defensive assets like cash, HostPlus would just keep on investing in their pre-determined splits of Shares, Cash, Infrastructure, Propery and Bonds (fixed interest) as per their arrangements with fund managers, and then just pay you out the defensive income rates. So what happens to the difference in earnings when this happens?

Well HostPlus is a not-for-profit industry superannuation fund, which means it is run to benefit members. This means this money is fed back to benefit members, in the form of lower fees and higher rates of return on investments. This is very different to a retail superannuation fund owned by a bank, where the bank can simply pocket the difference and this profit goes to shareholders.

So ultimately – the way HostPlus invests your money is a bit of a weird quirk. I guess as long as everything keeps ‘going the way it should’, the wheels stay on the bus and the gravy train of rising equities value continues, then we shouldn’t have any major issues and we should hopefully get distributed the relative performance of our individual investment choices. However, should HostPlus stuff it up with their asset pool allocation, there may not be enough returns to fully pay out everyone’s respective investment styles. This means you are not technically getting the asset exposure you are signing up for. Is HostPlus too big to fail?

With nearly $3 Trillion of our money invested in superannuation fund accounts nationally, the government has a wide incentive to keep a slight inflationary pressure and continue to print money and devalue our currency – this keeps equity prices rising, stimulates the economy and certainly keeps asset holders happy. It also makes situations like with HostPlus money pooling less scary.

Is CaptainFI opening a HostPlus super account?

Yes, despite the weird-ass pooling mechanism discussed above, I am stillI am opening a HostPlus super account for growth assets. Initially I looked into their ChoicePlus offerings, but honestly the basic index options are perfect for my needs right now. But its not just me – I talked this through with my family, and they are following suit as well as they agree it suits their financial situation or needs too.

So which funds are we choosing to invest in personally? Well, we initially all looked at the Balanced Index fund because of its simplicity, however, both my Mum and I decided on an investment approach of a 50:50 split of International and Australian growth assets (indexed shares) for our individual superannuation fund accounts.

I decided that I didn’t want the drag effect of cash or bonds dragging down my portfolio returns for my investment approach given my 30 + year investing time frame. This is the same for my long term investment approach for my investments outside of the superannuation fund as well – I eventually want to replicate this simple asset allocation. Of course, outside super I am heavy on Australian shares at the moment because I am chasing the strong fully franked dividend yield to provide a base-line level of passive income to reach Financial Independence quicker.

In terms of insurance with HostPlus – I chose to opt out of any form of insurance because I still have all of the insurance through my employer, my other superannuation fund (defined benefit) and my professional body (aviation specific). The HostPlus superannuation fund account will just be a tax effective way to invest any cash that I don’t need before my preservation age

Mum decided that she wouldn’t need really need to hold any cash at all as she receives a stable government pension, has a paid off house and a very low cost of living (and I am also setting her up with a website she will run as a hobby in retirement as an extra little cash producer – if a 60 year old boomer can do it you can too, so check out my article on How to make money online). She will only ever ‘harvest’ from her superannuation fund growth assets if it grew to exceed her pension’s means tested ‘super cap’ of around $250,000 – and then immediately spend this on a Holiday, Car, renovations, gifts for grandchildren etc.

Mum also chose to opt out of any form of insurance since well, she doesn’t need any now she is retired. Unfortunately she has had some health issues (ovarian cancer in the past) which was expertly dealt with through the public health system and her previous super fund did provide her income protection (75% of her wage whilst she was receiving treatment). We were devastated to recently learn she has come out of remission recently meaning there will likely be more surgery soon and chemotherapy again in 2021.

Frequently asked questions about Hostplus Super

Answers to frequently asked questions about HostPlus Super?

Is Hostplus a good super?

Yes, Hostplus is a good super provider. They have index fund options with low fees, and good performance.

Can I withdraw my super Hostplus?

You can withdraw your super from Hostplus when you reach preservation age, or in accordance with early release guidelines from the Australian Tax Office.

Can anyone join HostPlus super?

Yes, Hostplus super is now open to anyone. Previously it was exclusively for members of the hospitality tourism and sport industry only.

How can I check my Host Plus super balance online?

To check your Hostplus super balance log onto your HostPlus online member portal using your member number and password.

What super fund does the Barefoot Investor recommend?

The Barefoot investor recommends the HostPlus indexed balanced investment option.

Is Hostplus the cheapest super fund?

HostPlus is one of Australia’s cheapest super funds, with index fund index ETF offerings.

What fees do Hostplus charge?

HostPlus charge a base $78 per annum admin fee, plus the underlying management fee of your investment choice.

How to transfer my super to Hostplus?

To transfer your super balance to HostPlus you must first open an account with HostPlus, and then from the online member portal request a super balance transfer.

Where can I read the hostplus product disclosure statement

You can read the hostplus product disclosure statement on the Host Plus website.

Summary of HostPlus super

The hostplus superannuation fund is an Australian industry Superannuation fund that was originally built in 1987 for workers of the hospitality tourism and sport industries. They have had a pretty spectacular rise, and now let anyone join the fund. Because of this, they now have over one million members and manage over (AUD) $50 Billion worth of member funds. HostPlus is one of the largest superannuation funds in Australia and has historically also been one of the best performing super funds.

They offer a wide range of super investment options, and have become one of the leading providers of index based superannuation investment funds and products. They also provide insurance products such as income protection, TPI and life insurance, however they also have some notable exclusions on these policies. They employ a unique investor pooling investing mechanism called a ‘Notional investing mechanic’ which provides tax efficiency and reduced costs to the fund, however which provides a reduced level of risk and exposure certainty for investors. This is overcome somewhat by HostPlus’ incredible size of nearly $50B under management.

I personally think the HostPlus index super funds are right for my personal financial situation or needs, and am in the process of setting up my HostPlus accounts with a 50:50 split of the IFM Australian shares fund and the International indexed shares fund. This is where I am going to be putting any additional salary sacrifice contributions that I make into my superannuation fund, rather than into my company-defined benefit policy ‘additional contributions’ side fund (because the additional contributions fund has ridiculously high fees). I am not taking out insurance through HostPlus, and am keeping my Life insurance, TPI and income protection insurance through my previous super provider.

Before making any decisions to switch your super, ensure you rigorously read the hostplus product disclosure statement and understand your insurance options within the policies. I strongly recommend seeking professional advice to help understand if it suits your financial situation or needs before making any decisions. Just because I use them is not a recommendation that you should.

Further Reading

Hostplus’s Indexed Balanced Fund isn’t the only cheap super fund around – Check out my Barefoot investor superannuation article for some more ideas about great superannuation, and see my facebook posts on superannuation on the facebook page and facebook group.

You can check out my other Superannuation reviews here:

UniSuper Review – How Do They Compare?

Australian Super Review – What You Need To Know

MLC Superannuation Review: How Do They Measure Up?

Hostplus Super Review – Is It Still The Best Super Fund For 2022?

ART Super Review; Is It A Good Super Fund?

REST Super Review – How Do They Stack Up?

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Hi there. Very good article about Hostplus and the way their fund works. I read the same thing about the pooling of everyone’s super contributions and thought that it was a bizaar notion instead of direct investment into the person’s desired investment choice. I understood the basic concept and figured that they must of just done a reallocation of the size of the pool for that specific investment periodically based on the amount of money targeted, which is why you can change your choice of investment daily without incurring buy/sell costs. Your article gave me greater understanding of how super contributions are handled. My main interest is their fees & costs plus returns on my investment. I have also gone down the path of 50/50 Aust/International shares due to low fees and reasonable returns. I am 52 and I know people’s advice is that you should start to reduce your risk closer to retirement. However I still have 30 plus years of life left so going to conservative to early will cost me big in the long run. I can afford another downturn or 2 before moving into the indexed balance fund. Appreciate all your time and effort that you put into both your research and articles.

G’day Russell, that is a valuable insight to see your also doing the same thing at age 52, and to be honest I think I will too. I am researching Wrap accounts and looking at something like replicating my ‘FI’ portfolio inside my super structure. I actually had a great chat to Vince Skully about this all, and will be releasing an upcoming pod on super soon. For now though, I feel like Hostplus in the index shares aus:international is a ‘good enough’ solution

Hi there Captain Fi,

Great article, thanks for the insight in to the world of Super. I’m curious, after your chat with Vince Scully, have you changed your Super plan? You certainly do have time on your side.

Thanks Yvonne, it was very educational for me too! Because my total ‘invested’ portion is less than $100K there isn’t any big rush, and as always ‘haste makes waste’. I’m currently doing the financial review with Vince through the LifeSherpa and will see what the outcome of that is and what he recommends in terms of the structure, asset allocation and underlying investment. For now I still think the 50:50 split of Aus and international index funds through HostPlus is *good enough* for me right now, but will see what an even better solution could be

Hi there Captain Fi,

1) What is the better option for hedged vs unhedged international indexed? The hedged fund has a cheaper ICR

2) Also, what are your thoughts on high-growth managed super funds like AustralianSuper Balanced. Are their performance minus their higher fees worth it in the long term versus low fee cost passive super funds like host plus index balanced? I know it is hard to compare between the two (So if you have any tips that would be great!) and past performances don’t necessarily dictate future performances but it appears in the last 5 years that high-growth managed super funds perform better.

(I’m in my early 30’s so are deciding whether it is better to go with high-growth managed super funds vs low fee cost passive super funds)

Hey mate. Personally I have been using unhedged. But the whole point of hedging is to reduce currency risk. My understanding is that over the long term, the currency fluctuations even out (just like volatility in shares) so hedging somewhat reduces the volatility and the currency risk. Some people do half hedged and half unhedged. I think more of an issue in the ‘draw down’ phase or if you are wanting a smoother ride. Hedgeding usually has higher management fee and I think is a form of active management?

As for the super stuff, my opinion (and the data!) shows that an index approach always wins long term. Just because something is being actively managed within super doesnt make it any different to being actively managed outside super. The winning active managers are the dogs of tomorrow. Don’t over think it! Many super companies offer indexed investments, do your research and find something that is appropriate for you

Thank you! Love your content

Hello Captain!

Thank you for the post,

You say that you opened a HostPlus account, and decided on a “50:50 split of International and Australian shares”. I’ve checked out the HostPlus PDS & website, and I didn’t see this 50:50 investment option? Could you explain how you went about arranging the 50:50 split? I am interested in this investment strategy myself.

Thank you!

Hey Olivia, the exact choices I went with was “International shares indexed” and “IFM Australian shares” and since I got it at 50:50, due to changes in market it is currently 51.4% international and 48.6% Australian at the moment, presumably below the rebalancing criteria for HostPlus. Had about 24% annualised growth which is great but pretty unheard of, so won’t expect this level of performance going forward. I think 10% is a more reasonable number

Hi CaptainFI,

Great article. Please can you share your source for the index balanced underlying funds and allocations. I am a member of Hostplus but cannot find this detail on their website or PDSs.

Thanks

It isn’t published, they just call it their ‘modified index fund’ – presumably a ‘commercial in confidence thing’ but certainly worries me…

Hi there. Excellent, well presented information. I have a similar question to Keiron. What is the source of Benchmark Indexes for the funds? I’ve searched all over HostPlus and cannot locate it.

Cheers

I’ll answer my own question here: Information on Benchmark Indexes is not available on the HostPlus website but can be provided if you ask. I’m not sure why they’re not publishing the indexes their funds are meant to track nor how closely they follow them. Low fees can be quickly offset if an index tracking fund doesn’t closely track it’s index.

it is a valid concern mate – one that Vince Scully from life sherpa picked up on almost immediately. Would be good to share it publicly

Thank you Captain FI for the great analysis on Hostplus super.

I was trying to compare the returns of Hostplus super International Shares – Indexed option with the MSCI World ex australia and VGS. They do not match and is off by a few percent. Your post clarifies the investment returns for super are after income tax and investment costs(minimal), and i can breath a sigh of relief.

The investment returns for the pension unit of International Shares – Indexed option almost matches the MSCI World ex australia and VGS, given no tax in pension mode.

Hi CaptainFI,

I’ve really enjoyed a lot of your posts, thank you.

Given the investment fee for Hostplus international shares indexed is now the same (0.07%) for hedged and unhedged options, I am considering an equal split of both. What are your thoughts? Are you stilled with the unhedged option and if so why if the investment fee is now the same for both options?

Thanks

Hey Mary, Thank-you. I’m still on the fence re: hedging. My understanding was that it all evens out in the wash, and hedging and exchange fees can erode returns but provide less volatility, i.e. mitigate the currency fluctuation risk. It might be more appropriate for someone who was retired and drawing a pension off their super and wanting set outflows for budgeting, but since I am only 30 im not really too fussed about it. I am still with the unhedged and I think I will keep it that way at least until I was drawing the money out.

Noticed a second fundamental mistake, this is now correct!

One thing to consider is how the Australian dollar typically behaves. When there is a ‘risk on’ period, the Australian dollar increases in value, along with global sharemarkets. So your investment return is reduced, as the international shares are converted into a stronger Australian dollar. When there is a ‘risk off’ period the Australian dollar falls in value, along with global sharemarkets. So your investment loss is reduced, as the international shares are converted into a weaker Australian dollar. Essentially the way the dollar behaves as a ‘risk currency’ itself is a natural hedge and reduces the volatility of your investments naturally, both on the upside and the downside. So somewhat counterintuitively hedging your international shares actually increases their volatility. For me, I mostly keep shares in unhedged, except during periods where the Australian dollar is quite low (mid 60s and below as a rule of thumb), and these periods usually happen during or close to market bottoms (post dot-com bubble/asian financial crisis period, post-GFC, post COVID crash, 2022 bear market etc.). If someone followed this rule of thumb in 2022 and switched into hedged below 65c AUD/USD then the initial losses last year were reduced due to the falling dollar, and when the market was in recovery the gains weren’t reduced by a rising dollar.

One thing to consider is how the Australian dollar typically behaves. When there is a ‘risk on’ period, the Australian dollar increases in value, along with global sharemarkets. So your investment return is reduced, as the international shares are converted into a stronger Australian dollar. When there is a ‘risk off’ period the Australian dollar falls in value, along with global sharemarkets. So your investment loss is reduced, as the international shares are converted into a weaker Australian dollar. Essentially the way the dollar behaves as a ‘risk currency’ itself is a natural hedge and reduces the volatility of your investments naturally, both on the upside and the downside. So somewhat counterintuitively hedging your international shares actually increases their volatility. For me, I mostly keep shares in unhedged, except during periods where the Australian dollar is quite low (mid 60s and below as a rule of thumb), and these periods usually happen during or close to market bottoms (post dot-com bubble/asian financial crisis period, post-GFC, post COVID crash, 2022 bear market etc.). If someone followed this rule of thumb in 2022 and switched from unhedged to hedged below 65c AUD/USD then the initial losses last year were reduced due to the falling dollar, and when the market was in recovery the gains weren’t reduced by a rising dollar.

Thanks for the speedy response!

I’ll take your feedback on board as I’m only 30 too.

Hello Captain,

Would you consider stake SMSF?

Hopefully vanguard release their super product soon.

I’m also with hostplus 50% aus shares index and 50% int shares index. Do we know when dividends are paid? I haven’t been able to find that info.

Cheers,

Hey Louis, I personally steer well clear of SMSF, it’s just too difficult to manage everything. Yeah, lots of people pretty keen to see what Vanguard offering will be, I think the transparency will be the best aspect. I did a pod episode with Vince Scully on Super, he is a very clever and experienced financial advisor and had some brilliant things to say, so I would almost try to defer my commentary to his points regarding the transparency of HostPlus investment options (he shared the same questions as us, which is possibly an answer in itself right there)

Thanks for your reply. I’ll stick with the hostplus 50/50 split. I’ll have a listen to the podcast with Vince Scully now.

Cheers,

I listened the podcast. It was interesting. So with the 50/50 split are they (hostplus) actually investing the funds in index international shares and IFM australian shares? or is that the grey area we don’t know about? I had a look some of the wraps mentioned in the podcast. Some of their fees are bit confusing too.

Hopefully Vince is able to help you out.

I’ve had years of dealing with Hostplus, and looking beyond the published facts and figures, i have found them to be a very poor super fund. Their customer service, and processing is abysmal. It is though the fund’s Trustees are stuck in archaically conservative times where they refuse to have administrative processes that support efficiency. I was really suprised to see best fund of 2022 in a title as i would consider them (administratively) to be the worst fund on offer.

Is there any super fund you recommend with good customer service ?

Hey mate – I can’t advise any particular fund but I reccomend you check out https://www.ato.gov.au/Calculators-and-tools/YourSuper-comparison-tool/ and https://moneysmart.gov.au/how-super-works/choosing-a-super-fund My partner and I are with HostPlus

You do need to consider customer service, which as someone else commented is abysmal. You get no communication from anyone, there is no transparency of process and you are left waiting for months. My father died 11 months ago. We are still waiting for them to release the funds. There are no issues, so no reason for the hold up. The account is now closed and empty. They won’t tell us where the money is or how long until we get it. It is more than half a million dollars. Disgraceful.