Microinvesting apps let you invest with as little as a couple of dollars. Complete Microinvesting review from an experienced long term investor on the path to Financial Independence.

Micro investing platforms are an educational tool that can let you break into the world of investing with as little as a couple of dollars. Investing normally has a much larger entry barrier through a conventional broker such as Pearler or Selfwealth because of the brokerage cost (small trades with high brokerage is not a smart move as it adds up quickly!), minimum trade sizes and large individual share prices. Micro-investing overcomes this through fractional investing mechanics where your money is pooled into a trust or fund with other investors, as well as reduced or no brokerage, and the ability to frequently add small amounts.

“The idea is that by linking to a debit card, micro-investing apps can suck virtual “spare change” from their pockets and funnel it directly into an investment portfolio almost without anyone noticing”

The Financial Times

This lets you grow your money by investing it, rather than having it sitting idle, inflating away (devaluing) in a savings account. Micro investing platforms let you invest in the the things we all know and love like total stock market index fund ETFs, and depending on the platform you might be able to choose individual stocks, bundles of stocks or particular themes or industries.

Just remember though – Micro investing platforms are good for initial learning but are usually not a suitable long-term investing solution due to the fees involved.

The Good

- Start making your dollars work for you

- Easy to get started and use

- Automate them via round ups for ultimate passive investing

- Helps build investor mindset and experience

- Easy to transfer money in and out of

- Many can be connected to Sharesight for tracking

The Bad

- Hidden fees can erode performance

- Most are not CHESS sponsored and thus not appropriate for large sums of money

- If you are already investing through a full service broker, don’t bother microinvesting

- Can promote anxiety if constantly checking them

- Some microinvesting themes and portfolios contain a lot of garbage bullshit like risky bonds or over hyped tech.

Verdict: Microinvesting is a good first step to Financial Independence, but usually not a suitable long-term investing solution due to the fees involved.

CaptainFI is not a Financial Advisor and the information below is not financial advice. This website is reader-supported, which means we may be paid when you visit links to partner or featured sites, or by advertising on the site. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Benefits of microinvesting

Micro investing has its place in a financial journey and investors education, because they offer a number of unique benefits and advantages over conventional investing methods.

Microinvesting is quick and easy

It is dead simple to get started micro investing, and all of the platforms I have investigated took less than an hour to set up. You can simply link these to your bank accounts – some even offer ’round-ups’ which automatically send the change from your card purchases into your investing account. You could also set up small automatic transfers every fortnight from your bank into your investing account, making it even more ‘hands off’ and boosting your investments.

Microinvesting is passive

If you invest in total stock market index fund ETFs, or nicely diversified parcels of shares, then any form of investing is passive. You can have this option through most micro investing platforms, which is nicely automated. This means over time you benefit from the growth in the market without having to manage it yourself – it just ticks away in the background, growing your investments.

Microinvesting helps you start saving and investing

By far the biggest benefit of micro investing is the education you will receive by just getting started investing and having some skin in the game. By automating and simplifying your investing, you establish the saving and investing habits that are crucial to generating real wealth over your lifetime.

You don’t need a lot of money to start microinvesting – no deposit required.

You don’t need a big deposit (over $500) to start investing using a micro-investing platform. You can start by investing as little as one dollar with some platforms: you could just be using your small change or ’round-ups’ from transactions. Most platforms and then you are ready to invest and then watch your balance grow.

Most microinvesting platforms let you choose Index fund ETF investing

As touched on before, micro investing platforms can allow you to invest in total market index fund ETF options, or other broadly diversified themes or parcels of stock. This in my opinion is the smartest option since you do away with all the stress and bullshit of trying to pick stocks or time the market, strategies which both are proven to under perform the market over the medium and long term for the overwhelming majority of investors. You don’t need to be a financial or investing expert, and anyone can benefit from index funds.

Round-up Microinvesting

Micro-investing platforms let you turn your loose change into assets. Some can even be linked to your every day bank account and let you do ’round-ups’ on your transactions – for example that $9.50 pint of beer would be ’rounded-up’ to $10, and 50 cents would be transferred into your micro-investing platform.

Whilst you might not miss that 50 cents, if it happens enough throughout the year, you could find yourself with thousands of dollars in your micro-investing account. Further, rather than stagnating and inflating away in your savings account, your money can be allocated into ETFs and be given exposure to the total stock market index, meaning it can grow and compound over time.

Fees and charges of microinvesting platforms

Beware the perils of fees and charges. These matter. A 1% difference in ongoing fees and charges can add up to many, many hundreds of thousands of dollars of total investment returns over the average investors life. If you don’t believe me, type in “fees superannuation difference” and review the many hundreds of articles and examples.

Micro investing platforms mostly make their profits from fees and charges – which covers their development and running costs, as well as profits for their owners or shareholders of the business (i.e. ComSec pocket). Some of the main fees which will sap away your micro investing return on investment will include;

- Account management fees – These are your subscription fees for maintaining an account with your micro investing platform. You usually pay a monthly account keeping or subscription fee, which may be a set amount or a percentage of your account balance. Typically, these scale (increase) with your growing account balance in tiered thresholds. These vary, but are usually less than $2.50 per month or 1% of your balance

- Transaction fees. The cost each time you make a transaction is called the brokerage fee. Making small transactions with significant brokerage fees is not a smart move, and can cause your portfolio to seriously under-perform due to this ‘fee drag penalty’. Y

You will usually be charged brokerage on any transaction i.e. buying or selling shares or ETFs, or changing investment ‘themes’ like switching asset classes i.e. shares, property or fixed interest. For example, ComSec Pocket charge $2 brokerage on a minimum transaction amount of $50 – this is 4% and IMO unacceptably high – so you would want to ensure your making transactions at least above $200 to get this transaction fee under 1%. - Miscellaneous fees. Miscellaneous fees can only be truly determined by reading the micro investing platforms full Product Disclosure statements (PDS). These might include charges for opening and closing accounts, contributions into and out of the account, and charges for closing your account.

What can I invest in using microinvesting platforms?

Micro investing platforms might let you invest in a range of asset classes and publicly listed investments on the ASX. Options include;

- Cash and fixed interest (i.e. bonds)

- Stocks (i.e. equities or shares in publicly traded companies),

- Property through Real Estate Investment Trusts (REITs)

- Commodities and Resources such as Oil, Gas or Gold using Exchange Traded Funds (ETFs)

These can be invested in directly, through Exchange Traded Funds, or through bundles of shares or ‘themes’ which give exposure to a particular asset class or sub-class (i.e. mining stocks or ‘FAANG’ stocks)

What are the risks of using microinvesting platforms

As we touched on above, micro investing gives investors exposure to a variety of ‘real-world’ investment classes for their portfolios. This means they have a very real level of risk.

Whilst asset classes like cash and fixed interest (i.e. bonds) are typically thought of as providing a safer short term investment, over the long term this is actually the riskiest asset class of all as the combined assaults of inflation, low returns and taxation destroy its long term performance.

Conversely, stocks are thought of as having the highest short term risk, but have proven over the long term to be the safest way to protect your investment from inflation and miserable returns, and grow your long term wealth. But investing in individual stocks mean you could lose it all!

There are other asset classes you can invest in such as commodities (resources such as oil and precious metals) or property (through Real Estate Investment Trusts – REITs), or combinations of assets which can be invested in called bundles or themes, which are similar to ETFs. These all have unique risks and its important that you read and understand the associated fund PDS before you hand over your hard earned dollars.

Usually your micro investing platform will help you choose an investment class (or classes) based on your own level of risk tolerance and investing time frame. Its important that you do your own independent research though, and make sure it suits your personal financial circumstances.

Other risks of micro investing could be collapse of the platform. Conventional brokerage accounts are CHESS sponsored, which is explained by the ASX here. This means even if the company or associated funds collapse, the underlying holdings are still allocated to each individual investor. You either get paid out at market rate, or the funds transition to a new funds manager / administrator. Most micro investing platforms are not CHESS sponsored, and you are relying on their ‘goodwill’ to honor their terms and conditions. If they collapse, you could lose everything.

Whilst not thought of commonly, because micro investing accounts usually have such small balances, it is also easy to simply forget about them. Your own apathy could be the highest risk you face!

In my opinion through, the fees and charges are the highest risk you will face when using micro investing platforms. These really do make a difference, and add up. This is the price you pay for being able to start investing with no minimum capital requirements, and there is a very real risk your investments will under-perform conventional investments due to these alone.

What are the returns of microinvesting platforms

Because micro investing platforms can give investors direct exposure to the stock market, your investments could go up or down. Investing is a long term game, and you realistically need to be thinking 10+ years. Beware of the fees and charges however, which can erode your returns. For this reason, you should think carefully about whether micro investing is worth it for the long term.

I usually bank on a 10% gross rate of return for diversified total stock market index ETFs. Against this you will still need to factor in in somewhere around a 2% loss in real purchasing power due to inflation, taxation due to your marginal income tax rate, and the drag penalties of fees and charges.

Microinvesting platforms in Australia

There are many micro investing platforms, however some of the most popular platforms worth looking into are;

Pearler Micro

Pearler Micro is a cost-effective micro-investing tool that helps educate investors in Australia through the offering of 8 diversified investment options.

- Low cost. The app is an incredibly cheap way to invest in the sharemarket. There are zero fees for the first $100 you invest, and above $100 the fee is $1.70 per month if you have one fund, or $2.30 per month if you have multiple funds.

- Diverse portfolio. Each fund gives you instant diversification, spreading your money (and risk) across a wide range of companies, sectors and countries.

- Easy to use. There is no minimum investment, and the web client is straightforward, letting you transact either at home or from your phone while you’re on the move.

- Making tax time easy. Pearler Micro provides you with an annual statement to help you complete your Australian tax return, and can be integrated with Sharesight (just like the man Pearler Shares platform.)

Pearler Micro has 8 funds you can choose from

- Diversify and Chill

- Global Large ESG Companies

- Aussie Large ESG Companies

- Aussie Large Companies

- Global Large Companies

- An American Buffet

- Battery Tech

- Better Future

Check out the full review of Pearler Micro here

Raiz Invest

Raiz Invest is a micro investing platform which lets you ’round-up’ your spare change from purchases into the platform. This can then be invested into six different ETF portfolios depending on your personal level of risk.

- Conservative

- Moderately Conservative

- Moderate

- Moderately Aggressive

- Aggressive

- Emerald

- Sapphire (Bitcoin)

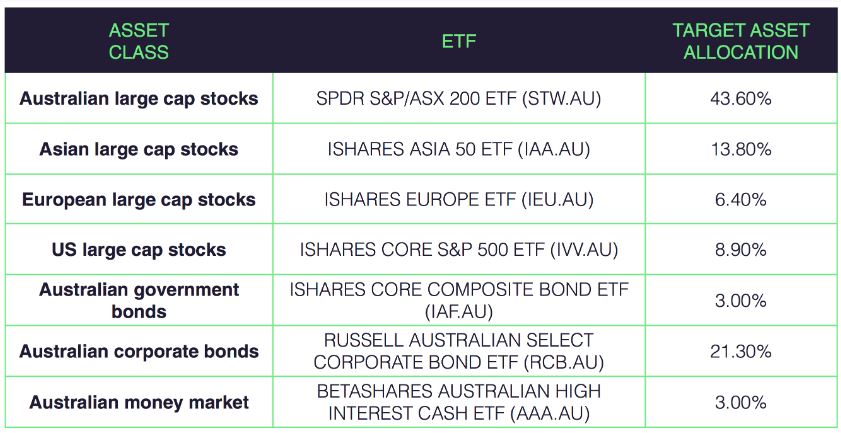

These seven investing themes are constructed from a combination of 9 different underlying ETFs (which you could invest in directly through a conventional broker)

- State street Global Advisors Australian ASX top 200 – ASX:STW

- iShares Asia top 50 – ASX:IAA

- iShares Europe to 350 – ASX:IEU

- iShares USA top 500 – – ASX:IVV

- Russel Australian Responsible Investing ETF: ASX:RARI

- Betashares Global Sustainable leaders: ASX:ETHI

- iShares Australian government bonds: ASX:IAF

- Russel Australian Corporate bonds: ASX:RCB

- Betashares Australian money market (cash): ASX:AAA

- Bitcoin crypto currency – NOT an ETF!

As an example, the Rais Moderate portfolio theme consists of;

Raiz has a fairly well designed and user friendly mobile application, with secure 256 bit encryption to protect your identity, bank account and investments.

You can also contribute extra into your account in order to boost your investments, both with regular automatic contributions or as lump sum contributions. You are never locked in, withdrawals and contributions are free, and they don’t charge brokerage (but you may pay a fee depending on the ‘buy / sell ‘ spread of the 6 ETF choices).

Raiz charge a $2.50 monthly account subscription fee on balances between $0 to $10,000 (i.e. you wont pay fees on a zero balance), and above $10,000 it switches to a .275% per annum percentage of your account balance. This means once you hit the threshold account balance of $10,000, the cost becomes $27.5 per year ($2.30 per month). Being percentage based, it then scales up from here.

Beware, once you invest into the ETFs, there is an additional ‘underlying issuer fee’ which is charged for management within the ETFs – these range from .196% to .418% depending on your investment choice, which in my opinion are pretty high for ETFs. This means your total ongoing fees (before brokerage) are probably something in the range of 0.5% to .7% – which in my opinion is ridiculously high for a passive (index) investment product. For comparison, my USA ETFs cost me .03% and my Aussie ETFs cost me .07% – around 10 to 25 times cheaper! For the full breakdown, check out their PDS

You can read more about Raiz Invest and my experience on the app by heading to the Dedicated Raiz Invest Microinvesting review article

CommSec Pocket

CommSec pocket is the Commonwealth banks response to the micro investing fintechs, and allows you to invest into 7 different ETFs, which they call investment ‘themes’. These themes are;

- Aussie top 200: ASX top 200 index fund

- Aussie Dividends: ASX-30 high dividend yield

- Global 100 index: The worlds biggest 100 blue chip companies by market capital

- Emerging markets: 800+ growing companies within Asia

- Health Wise: A combination of 100+ medical and healthcare companies

- Sustainable leaders: Top 200 ‘green’ companies

- Tech Savvy: Top 100 US technology innovators, such as ‘FAANG’ stocks (Facebook, Apple, amazon, Netflix and Google)

Each investment theme charges an issuer management fee of between 0.09% to 0.67% of the investment balance.

CommSec pocket has a minimum transaction amount of $50, and charge a $2 brokerage fee for each transaction. This means the brokerage account is 4% which is a bit high IMO, but if you make larger transactions of around $200 then this is only 1% and much more reasonable. Above $1000, brokerage is charged at .20%. If you invest but don’t actually have enough to cover the trade, you will be charged a dishonour or late settlement charge of $10.

Check out my full review on Investing through CommSec Pocket

Spaceship Voyager

Spaceship Voyager is a micro investing platform which lets you choose between two investment funds; the

- Spaceship Voyager Origin Index portfolio, or the

- Spaceship Voyager Universe portfolio.

Both the Spaceship Voyager Origin Index Portfolio and the Spaceship Voyager Universe Portfolio are a mixture of Australian shares, Global shares, and cash.

The minimum suggested investment period for both is at least 5 years, but IMO it should be at least 10. There are no brokerage fees, no buy/sell spread fees and no entry or exit fees. They charge one simple management expense ratio depending if you go for the passive or the active fund

The Spaceship Voyager Origin equal weight Index Portfolio (Passive index style fund)

The Origin Portfolio invests your money as 15-25% into an equal weight ASX 100, 70-80% in an equal weight Global 100 (that is, an equal share of the the top 100 Australian and Global companies by market capital, respectively) and the remaining 0-10% as cash.

Spaceship uses equal their own equal weight index rather than a traditional market capital index ETF to try and get less exposure to the top 10, and more exposure to the bottom 90 for example.

Balances under $5000 attract no management fees, but above $5000 you will pay .05%; for example a $10,000 portfolio will attract a yearly fee of $2.50.

The Spaceship Voyager Universe ‘Where the World is Going’ Portfolio (Active stock picking fund)

The Universe Portfolio is a mix of Australian shares, Global shares and cash in the same proportion of the Origin Portfolio. However, rather than using an equal weight index, they use their own ‘Spaceship WWG’ (Where World is Going) index.

This is a rules based stock picking index, with a maximum of 2.5% in any one company within an asset class, to try and pick emerging stocks with a good prospect of capital growth; for example FAANG tech stocks (Facebook, Apple, Amazon, Netflix and Google).

In this respect, the Universe Portfolio is an actively managed fund that tries to pick stocks (Hmmmmmmmm). The fees for the Universe portfolio are proportionately higher; double than the Origins Equal weight Index portfolio at .1% per annum. Again – the first $5,000 is ‘free’, so a $10,000 balance would attract a $5 annual management fee.

Stake

Stake is a unique micro investing trading app which allows Aussies access into Wall Street, to trade shares on the US stock exchange.

Your money is ‘pooled’ with other investors into their fund, and then through fractional investing mechanics you are able to buy and sell portions of shares – they just maintain a database which keeps track of who owns what.

Whilst Stake doesn’t charge brokerage fees, they do make their money during transfers into or out of your Stake account and various other fees like the W8-BEN tax lodgement fee. Their baseline account is free, but they also offer a premium service which is $19 (USD) per month for increased brokerage features like advanced orders (stop-loss etc) and their proprietary market research.

Check out their Product Disclosure statement, as well as their Pricing page and the Australian terms and conditions page to read the fine-print and make sure you don’t get any nasty suprises when it comes to fees and charges.

Check out my full review on investing with Stake.

Who microinvesting is not for

Micro investing is probably not suitable for experienced investors, or investors wanting to invest a lot of their capital.

- You will not achieve any diversification that you can’t get through ETFs available through your conventional broker.

- You will likely be disappointed by the lower returns achieved through micro-investing platforms due to their higher fees.

- You probably already know all you need to about investing, and the main point of these platforms is to provide some level financial / investing education through getting skin in the game and gamifying saving and investing.

- The increased ‘double-up’ on administration and tax reporting is just going to waste your time and annoy you.

- Most Micro investing platforms aren’t CHESS sponsored which makes them another possible link in the ‘failure chain’, or possible failure mechanic in you losing your money.

- The investing ‘themes’ that micro investing platforms offer could be considered just another ‘layer’ of confusing financial products to learn about. When it comes down to it, they are just combinations of ETFs that you likely already own.

Frequently asked questions about microinvesting

Answers to frequently asked questions about microinvesting

Is micro investing worth it?

Yes. Microinvesting is an effective way to build up an investment portfolio with small amounts of money. Once you build up $5,000 in your microinvesting portfolio, I recommend switching to a full service broker.

Best microinvesting platforms

Some of the best Microinvesting platforms around include Pearler Micro, Raiz Invest, CommSec Pocket, SpaceShip Voyager and Stake

Best microinvesting apps

The best micro investing apps include Pearler Micro, although Stake, Raiz Invest, CommSec Pocket and SpaceShip Voyager all have very good mobile apps.

Is spaceship CHESS sponsored?

No, Spaceship is not CHESS sponsored. Your portfolio is not held under your unique HIN (holder identification number) and your capital is at risk if Spaceship collapses.

Is Micro investing in Australia a thing?

Micro investing in Australia is becoming increasingly popular, with the 5 main platforms being Pearler Micro Stake, Raiz Invest, CommSec Pocket and SpaceShip Voyager.

Where is your Spaceship voyager review?

I have been actively researching and using spaceship Voyager – here is the review.

How does micro investing work

Micro investing works by pooling investors funds or using fractional investing mechanics. Together, a group of investors can put their money together to own shares. Various mechanics like round ups or regular deposits allow micro investors to increase their balance.

How to start micro investing

To start micro investing simply read any of the detailed reviews on micro investing platforms on the CaptainFI blog. Each review features a guide showing how I used the platform, and often features a bonus sign up code for you to get some free money for giving it a go.

How do I track my microinvesting returns?

Sharesight is a great tool which you can use to track your investment portfolio – The best part? If you have under 10 holdings its completely FREE. Check it out – I swear by it these days.

Summary of Microinvesting

Micro investing could be great way to get started investing if you don’t have a lot of capital to play with, know much about the markets or if you are not ready to start investing large sums of money.

Anecdotally, quite a few of my friends have gotten started investing through Micro investing platforms. Over time they let the ’round-up’ features and compounding returns of the stock market help them grow a size-able chunk of assets. Once it became ‘big enough for them to care’, they then they sold up, closed their accounts and used the proceeds to invest through a lower cost conventional broker like Pearler

I think this is the perfect function for micro investing platforms, and where they perfectly fit into the investing ‘spectrum’ – as an education tool to help investors get started investing. And the BEST way to do this, hands down, is to get some skin in the game!

Check out some of the providers above and see what you could get started with today. Just be sure to carefully read the PDS and understand the fees and charges structure associated so you don’t get any unwanted surprises.

Finally, don’t be surprised when your micro investing produces micro results. Micro investing is not suitable for a retirement plan and really, it is more of an educational tool than a serious financial investment.

Financial Disclaimer

Financial Disclaimer: CaptainFI is NOT a financial advisor and does not hold an AFSL. This is not financial Advice!

I am not a financial adviser and I do not hold an Australian Financial Services Licence (AFSL). In this article, I am giving you factual, balanced information without judgment or bias, to the best of my ability. I am not giving you any general or personal financial advice about what you should do with your investments. Just because I do something with my money (or use a particular service or platform) doesn’t mean it is automatically appropriate for your personal circumstances. I do not recommend nor endorse any financial or investment product, and my usage or opinion of any product should not be interpreted as an endorsement, advertisement, or intent to influence.

I can only provide factual information based on my journey to Financial Independence, and that is provided for general informational and entertainment purposes only. I make no guarantee about the performance of any product, and although I strive to keep the information accurate and updated as it changes, I make no guarantee about the correctness of reviews or information posted.

Remember – you always need to do your own independent research and due diligence before making any transaction. This includes reading and analysing Product Disclosure Statements, Terms and Conditions, Service Arrangement and Fee Structures. It is always smart to compare products and discuss them, but ultimately you need to take responsibility for your use of any particular product and make sure it suits your personal circumstances. If you need help and would like to obtain personal financial advice about which investment options or platforms may be right for you, please talk to a licensed financial adviser or AFSL holder – you can take the first steps to find a financial advisor by reading this interview, or by visiting the ASIC financial adviser register and searching in your area.

For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Wow mate. This article has all the info you could ever need on micro investing. Super in depth, and easy to read. Well done with this one.

Hi guys, for another article on micro investing which is a great quick read, head over to Fire with a Family for Blakes break down at https://www.firewithafamily.com/post/micro-investing-apps-are-they-worth-it