CaptainFIs financial and personal update for the end of Quarter 2, 2023

Captain FI is not a financial advisor, does not hold an AFSL and this article is not financial advice. This website is reader-supported, which means we may be paid when you visit links to partner or featured sites, or by advertising on the site. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer

Captain FI’s personal update

The past 3 months have been a great chance to get back into a bit more creative pursuits, so I have enjoyed doing a lot more writing and podcasting, gardening, and reading for my own self-development. It’s been great to open up the guitar case and play the guitar my mum gave to me before she passed.

As I type this, it is a chilly Adelaide morning, and I must admit I have been switching the central heating on most mornings to take the bite out of the cold after getting up to let the dog out of her crate (followed of course by a hasty retreat back under the blankets, which the pup usually beats me to, so we all snuggle down for an extra half an hour or so of toasty napping before the place heats up).

Unfortunately, a close friend of mine and ex-partner passed away. Whilst we hadn’t been close lately and had kind of naturally drifted apart over the past few years (as tends to happen with romantic relationships that don’t work out when both parties move on), we were still great friends, and it came as a huge shock. She was only 30, and passed in her sleep. It resurfaced huge feelings of loss, grief and sadness for me, and her funeral was a very tough day. It was my first experience as a Pallbearer, which I felt was a symbolic way to express my love and support to her and her family. Thinking back to the loss of my dear mum late last year, all I could think to do was to bring food, love and support to her family, so my partner and I have been dropping off home-cooked meals and trying to help out with little things without being asked.

I guess as a side note – when someone is grieving or going through a lot, don’t ask them how you can help. Instead, offer help in the form of direct yes/no endeavors – such as “I have made you a roast for dinner, would you like me to drop it off at 6pm” or “I would like to take your dogs for a walk at 9am tomorrow morning, I’ll bring you a hot coffee – would you like to come with us? This is much easier to cope with, as just generically asking how you can help puts the onus back on the person to ask for help, which can be overwhelming to even think about with such precious little mental and emotional bandwidth.

I have been catching up with the FIRE community through a few ‘FIRE meetups’ which have been awesome. Before I left Sydney we organised a few in Circular Quay, and now that I am in Adelaide it’s been great to be able to join in on some of the established meet ups, as well as organise ad-hoc events such as the Brisbane meet up in May. Actually, these events are on all the time – jump onto the Facebook group and check out when the next one is happening in your area – or just pick a date, time and location and make your own post!

I have been reading a few books lately, including Taking Stock (Jordan Grumet), My Money Journey (Jonathan Clements), Financial Autonomy (Paul Benson), Nausea, Come as you are, Ichigo Ichie, as well as a heap of others from my reading list.

One of the best books I read recently was Essentialism by Greg McKeown, which is all about prioritizing the ‘essentials’ over the daily noise. He makes some brilliant points, which I have been trying to apply to my life and my website business by cutting down on clutter and red tape, and overall just trying to simplify processes. Instead of forcing things, I am trying to just sit back and gently guide the flow of things – tapping them back into the right direction when they go off track.

No products found.

One way I apply this is by really focusing on empowering my contractors to manage themselves and for me to personally ‘step back’ to avoid micromanaging or getting down into the weeds. This has been working really well, especially with things like podcasts, content and social media production with my team of Writers, Editors and Virtual Assistants. Rather than stressing about efficiency, maximising production and erking out the most deliverables per hour with detailed work flows and guides, I have instead been setting clear top level deliverables for production and quality, and stepping back. I have also begun ‘gently tapping’ in the direction of upskilling, educating, and transitioning some of the team to roles with more responsibilities and pay.

In my personal life, from this I have also had a renewed interest in minimalism (which is basically essentialism) and took to a strong declutter, letting go of old possessions which I no longer use, and some mementos which I didn’t really need to keep. Given the loss of my close friend, I stopped ‘saving’ things, i.e. we have a few bottles of wine worth a couple hundred bucks each in the cabinet that we had been saving for special occasions, and instead, we have been enjoying them at the first opportunity. It sounds weird but I also have been keeping this candle I love the smell of, but haven’t been using it. So we started burning it. It’s nice to be able to focus on enjoying things rather than saving them for some unknown future date that might not even come!

To that extent, we have actually also actively been thinking and researching into things that will improve our lives and so far we have come up with the following upgrades/purchases;

- A Kingsize bed with 1200 thread-count egyptian cotton sheets (Our old Queensize bed has gone into the office which is now an office / guest room, and my partner and I now share only one desk)

- Upgraded our bedroom TV (which we don’t really watch much anyway) from a 32 inch to a 55 inch (second hand Sony Bravia)

- A heated electric blanket throw for the couch – great for snuggling under with a movie

No products found.

- A ‘top-of-the-range’ rice cooker (which I am ashamed to even say publicly how much it cost)

- Gym Group class memberships

- An awesome kitchen mandolin for slicing vegetables and meal prep

No products found.

- An insanely sharp kitchen paring knife –

No products found.

CaptainFI interviews I have done

I have also been doing some interviews which have been really fun and pushed me to get out of my comfort zone. Some of them include

- An interview with Michael Quan from Financially Alert – Flying Free with Captain FI

- An interview on Nomad Numbers – From Cargo Pilot to Financial Independence

- A Podcast Interview by Dev Raga on My Millenial Money Professional – Part 1 and Part 2

- An interview on Livewire Markets – Pulling the ripcord and retired at 30 – Here’s how he did it.

- An interview with Dr Jim Dahle from the White Coat Investor – Pilots Can Reach Financial Independence Too with Captain FI

Plus a few more written interviews and podcast episodes which should come out soon, including with one of my all time favourite creators Canna Campbell who I used to binge her Youtube videos. Coming up soon is also the Nicole Martin podcast and Queenie Tan.

Captain FI podcasts I have recorded

As I mentioned above I have been podcasting and writing a lot more lately and have some really awesome episodes coming up for you soon, and have recently published some awesome interviews with a couple of my FIRE idols such as JL Collins!

- Podcast | Deacon Hayes – Well Kept wallet, – For today’s podcast, I welcome Deacon Hayes from Well Kept Wallet who went from over $50k in debt, to FI and who became a financial planner along the way.

- Podcast | Jeremy Schneider – Personal Finance Club – Today I chat to Jeremy Schneider from Personal Finance Club. Jeremy chats to us about building successful businesses, about how PFC started & how he reached FI!

- Podcast | Interview with JL Collins – Welcome to my podcast with the ‘godfather’ of personal finance, and the author of the bestselling book – ‘The Simple Path to Wealth’, JL Collins!

- Podcast | J Money from Budgets are Sexy – On board the pod today is JMoney from Budgets are Sexy. Jay became a millionaire in just 10 short years reaching financial independence before the age of 40. Jay has won many awards, is no stranger to buying and selling online businesses and is full of energy! Jump on board!

Captain FI blog articles I have written

I have also published a heap of new blogs and review articles, including:

- Being a Live In Carer for my Dying Mother – A live in carer is someone who cares for someone whilst living in their home. This is my experience as a live in carer for my mother before she passed away.

- Eulogy to an Amazing Mum – It took me a while to write this… I have been processing my own emotions and learning to live with the grief. Here’s my eulogy to an amazing mum.

- Captain FI’s Residential joint venture property development investment – Captain FI’s residential joint venture property development investment – what it takes to finance and manage a subdivision and build on a small development

- Bob Andersen’s Property Mastermind review – Bob Anderson’s Property Mastermind promises to equip aspiring real estate investors – but is it too good to be true? Find out in my property mastermind review

- Webinar – How to buy & renovate websites for passive income – how to buy and renovate websites for passive income – This is designed to help you quickly learn what’s needed for success in website business and investing

- Tasmania Road Trip – Our Itinerary – My partner and I enjoyed a one-week Tasmania road trip together. Here’s our itinerary, some tips we made for next time, some of the costs and what we loved.

- Jucy Van Rental Review – a review of the Van hire company for the Camper Vans we hired on one of our recent trips to Queensland

- Slow Travel – Philippines and SE Asia – My partner and I spent 2 months traveling SE Asia in late 2022 through to early 2023. Here’s a breakdown of expenses and what really stood out from our trip!

- What is a Budget Binder and Do I need one? – Budget binders help people keep track of their finances and to work towards financial goals. So exactly what is a budget binder and do you need one?

- Save Money on Bills; Scripts to Negotiate Your Bills – There are many ways to save money on bills, but have you tried calling your provider and actually ASKING for a better deal? Here are the scripts I use..

Captain FI directory pages I fixed

and I finally sorted out my resources tabs for books, blogs and podcasts and made separate dedicated directory articles listing my favourite blogs, podcasts and books.

If you want to see what I am doing on the more day to day stuff, you can follow me on social media where I regularly post what I am up to.

Captain FI’s Spending

I previously trialed documenting my spending, but it was a bit of a mess and I didn’t stick to it. Instead, I used to calculate my savings rate which was the portion of my take home (after tax) wages that I saved and invested (you could kind of think of this as like, 100% minus my spending rate). This led to a bit of an obsession, and so I stopped tracking this closely in the second half of 2021.

Anyway!

I recently collated my spending over the past 18 months and found last year’s spending (2022) was $42,320, and so far in 2023 I have spent $17,515 with a forward projection for the next six months to finish 2023 with a total spend of $40,850.

This is basically a baseline living cost of around AUD $30,000 – $32,000 plus whatever gets spent on travel.

What this shows is that my spending is fairly stable, and that it is pretty much completely covered by my ETF portfolio according to the 4% rule. 4% of $1.05M is just shy of $42,000 per year. This is pretty handy, especially because my dividends have historically been around the 4% level (reports in the next section), which means I don’t really need even to sell parcels of shares just yet.

Because I have multiple streams of income (such as blogging), I have actually earned considerably more than I spend, and I have been able to continue to add to my investment portfolio, as well as build up a decent cash buffer (of over 2 years living expenses now) which I plan to put towards buying a hobby farm either in the Adelaide Hills or Sunshine Coast Hinterland region.

If you are interested in seeing more about my spending let me know and I will put more effort into tracking and posting it, breaking it down into categories. I recently posted about my trip around SE Asia with a breakdown of my spending and costs so if you want to see more of this let me know and I will focus more on that.

Captain FI’s Investments

As I mentioned in my last update, I don’t really calculate a Net Wealth or Savings Rate Figure much anymore. I had a realization that this was one manifestation of a somewhat chronic money anxiety borne out of my upbringing, and a desire for certainty and stability. Nevertheless, they were great metrics for tracking my journey to FI, helped my accountability, made interesting blogs and the figures showed I made exceptional progress on the path to FI (the historical summaries can be found at the end of this update). I haven’t calculated it for this update, but at the moment it is somewhere north of AUD $2M.

My most recent investments were really just continuing to build (and balance) the share portfolio with about $10K invested into the Vanguard VEU ETF (mostly the proceeds of this quarters dividends), as well as building up cash in my mortgage offset account.

My current investments (outside super) are split between 4 main areas;

- The FIRE Portfolio: Global, USA and Aussie Index fund ETFs

- Real estate – Residential duplex

- My company – which runs a portfolio of content marketing websites

- Cash (Australian Dollar, held in mortgage offset account)

I also maintain smaller investments in the following two areas

- Angel Investments – Start-up company Pearler

- Cryptocurrency portfolio – Bitcoin and Ethereum

NB – Approximately a year ago I ended up divesting in various things such as RoboAdvisors, Micro investing funds, Managed funds, Metals/resources, and a few other speculative investments or experiments I had in order to simplify my finances. I had racked up a complex mix of investments as I wanted to try out various investing services but this became unmanageable in the end and I needed to simplify

The ‘FIRE’ Portfolio (Exchange Traded Index Funds)

My ‘Financial Independence Retire Early’ ETF Portfolio is a simple, passive share portfolio split between three parcels of low-fee, index-tracking Exchanged Traded Index Funds (ETFs) to achieve global diversification. I began switching to this passive index approach to investing in 2018, firstly by adding new contributions, and then over time by divesting in other assets (individual shares, managed funds, LICs etc) and rolling the investments over to it.

- I track my share portfolio using Sharesight, which means my portfolio accounting and tax reports are completely automated.

I am considering lowering my portfolio weighting of Australian shares in A200 to 10%, and increasing the weighting to international shares in VTS to 60%, and in VEU to 30%.

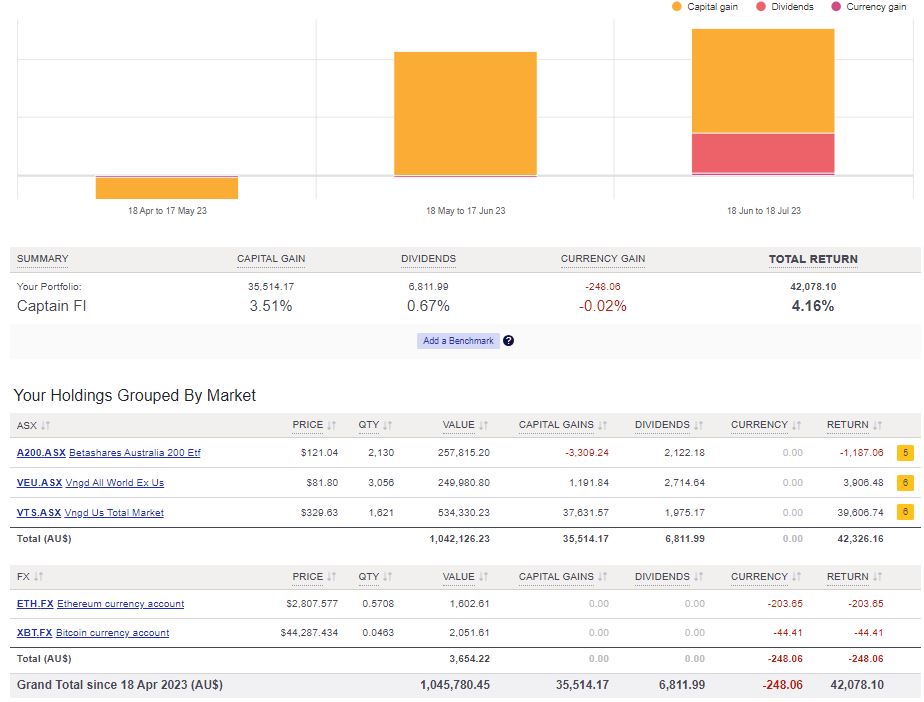

The last 3 months showing a pretty solid portfolio return of 4.16% – 3.5% capital growth and .67 in dividends, with the latest dividends about to drop into my bank account over the next couple of days – I just received the AUD $1,650 A200 distribution and am about to receive another AUD $4000 in cash dividends from the international holdings, plus tax credits (from international shares) and franking credits (from Australian shares) worth approximately $1200. Total in Cash dividends and tax credits of $6,812 over the past 3 months works out to be $2273 per month. Some back-of-the-envelope math shows that dividends are decreasing a bit (~2.6% forward projection) but I think that could mean either we will see some larger dividends in the next few quarters or, alternatively, some higher capital growth instead.

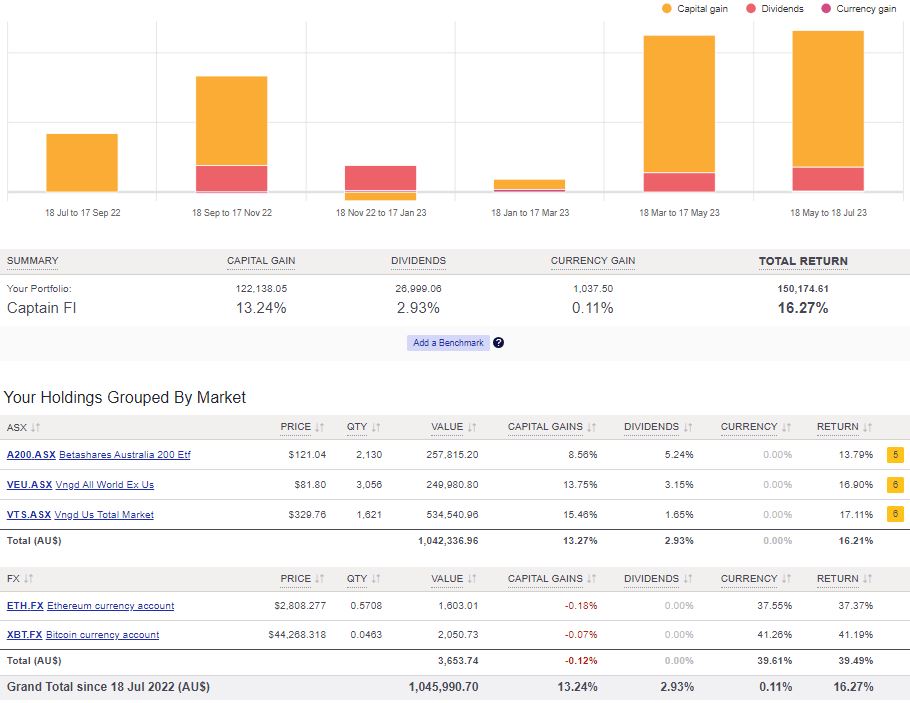

The rolling 12 monthly performance is a rocket! Woo-hoo, over 16% growth! This is actually probably in response to the share market drop last year (tech wreck?) so its naturally had some time to recover, and it just so happens that this reporting period has now moved past the drop so the last 12 months looks stellar in particular, but actually when we zoom out its a pretty “normal” return. As with the 3 monthly report above, dividends seem to be stabilising at a more “reasonable” number, or lower percentage of the portfolio, which is actually mostly because of my planned increase in asset allocation towards international stocks – targeting 75% (50% USA, 25% global).

As you can see, Aussie shares have continued to churn out huge dividends (5.24%!), but actually, even with the franking credits, my international shares have been the best performers – so I am glad I focused more on this diversification. Whilst receiving less dividends sounds ‘bad’ for an early retiree – I have multiple streams of income and a large cash buffer, so actually capital growth is my preferred vehicle for growth, which gives me more control over when I realize gains for both tax planning and asset allocation. Thankfully, I haven’t had to sell shares, and actually thanks to multiple streams of passive income I have been able to slowly keep adding to them!

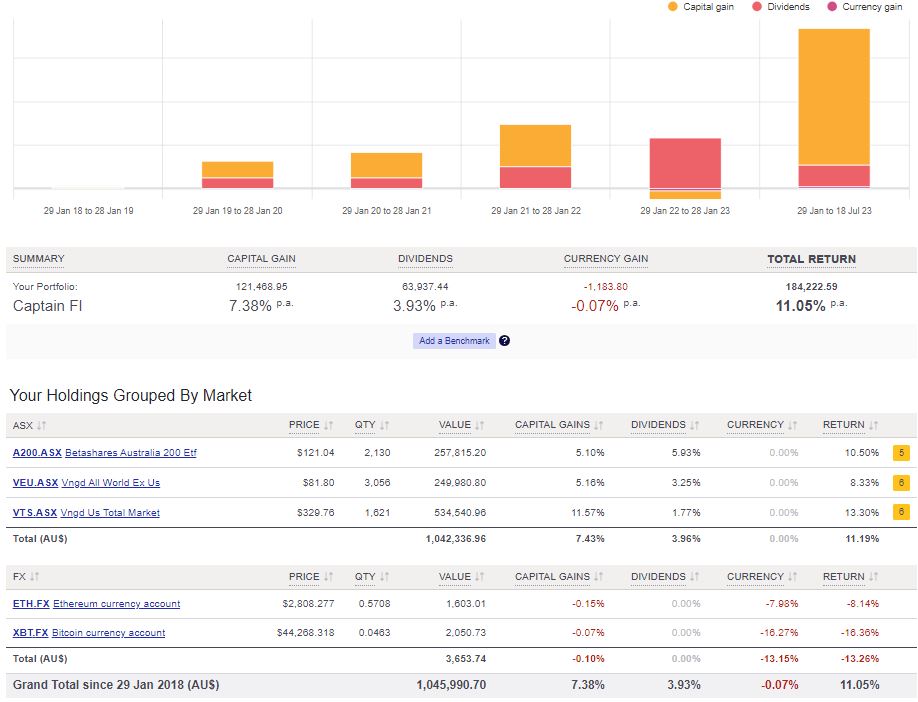

Love seeing the ‘since inception’ graph from Sharesight back to when I started adopting a purely index ETF approach to investing at the start of 2018. Now in my sixth year of passive index fund investing and having built a seven figure portfolio, I can confidently say that this is the right approach for me personally, and I feel secure knowing I have a solid base of future dividend income and the flexibility to sell parcels of shares to fund my lifestyle as required. According to the 4% rule, I can confidently now take approximately $42,000 in yearly spending and this portfolio should outlive me.

The report shows I have earned an average of 3.93% in dividends – and if this continues going forward, that is currently $41K, and actually more than my current cost of living which is a baseline of about $32,000 plus whatever is spent on additional travel i.e. airfares, cruises or holiday accommodation.

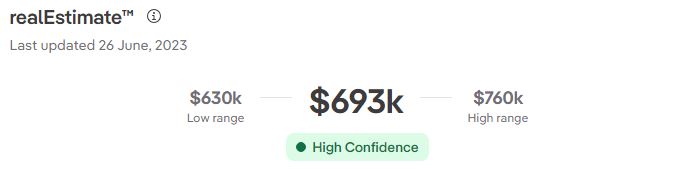

Investment property

I recently wrote a full separate article on the IP build – CaptainFI’s residential property development investment. The current automated online valuation estimate is $693K, although I have recently refinanced (getting the last of the cash bonus offers for refinancing) and the new bank has accepted an estimate of $750K. Some cursory research has shown similar properties recently sell for well over this in the area – a similar but slightly larger property went for the high 900’s, and a much larger one with an extra bedroom cracked just over $1.1 million! Whilst this is a smaller duplex and I don’t think it will quite fetch that much, it does certainly point to big growth in the area.

I currently have the IP mortgaged with a split loan, and currently have been saving up in the offset – accumulating cash for our PPOR ‘forever home’ whilst we decide what to do – as I mentioned previously, we aren’t sure we are fully set on the Adelaide Hills anymore, and are looking further afield including the Sunshine coast hinterland. Our most likely course of action will be to sell a big chunk of shares, and draw down the IP offset accounts as much as possible to fund the acquisition of a PPOR, with any difference being funded by a further mortgage.

Currently I have a 5.8% Interest rate, and with the property tenanted and the mortgage with the offset it would be cashflow neutral – although with depreciation and claiming expenses at the EOFY I will get some tax back shortly (but not heaps considering I am on a 21% tax bracket) so the property would actually be slightly positive cash-flow after all is said and done. However, as I mentioned, the offset account is growing as I accumulate cash which reduces interest payable and by definition makes it more positively geared. With strong capital growth, the LVR is also decreasing which is also giving me future options for cash out refinances to help towards the farm.

As I touched on above, to get some extra performance I am trying to ‘churn’ the mortgage through different lenders via a mortgage broker to get cash-back refinance offers, which is a similar concept to credit card churning – you basically switch lenders and do some paperwork, and as an incentive to come onto their books, they will offer you a bonus (hoping you forget about switching again and stay on with them forever) – the best one I got was $4,000, and I am set to have made over $10,000 in rewards with this next switch. To-date I have switched through 4 different lenders, and the mortgage broker does all of the leg work for me. It is becoming a bit more difficult now I have retired but between me, the mortgage broker, my accountant, and my business bookkeeper we are able to put together the documents they require.

You might think a mortgage broker would hate this because they lose their trailing (ongoing) commission from the lender – but as it turns out, the upfront commission they get from the lender is so juicy its actually in their best interest to do this regularly, so we plan to switch every year or so, unless lenders phase out their refinance bonuses.

Online Business (website portfolio)

I have a small business that runs a website portfolio of 15 different content sites that make money semi-passively from display Advertising through managed ad networks such as Adsense, Ezoic and Mediavine, and affiliate programs such as Amazon Associates and other direct affiliate deals. I’ve written a pretty detailed article here about how to make money online.

I have been doing a lot of writing and publishing on my passion sites, including podcasting here on CaptainFI.com, and I decided I enjoy this much more so will just focus my energies onto my main couple of sites rather than trying to spread myself too thinly across all of them.

As a result, I have a few sites I am open to selling to anyone who wants to get started with this side hustle with their first starter site or older, more established content site. They range from 2 to 4 years old, with various backlink profiles, number of published articles, and traffic. You can check out this article on website operation if you are keen as I’ve listed all the details in there. Feel free to send me an email through the contact form or get in touch on social media if you are interested.

I learned these skills through the eBusiness institute over the past 4 years – I have done a pretty comprehensive review of the eBusiness institute as well as interviewed Matt and Liz Raad about this on the podcast again recently where we go over a huge list of frequently asked questions about online business if you want to learn more about this. They also provide some free introductory training for CaptainFI readers.

Angel Investing

I have a small ‘Angel Investment’ in the Financial Independence brokerage platform Pearler. This was the maximum allowable private investment of $10,000 (AUD) which was made in July 2021 with the total number of ‘private equity’ shares based on their June company valuation. This was all documented, recorded and disclosed as per ASIC requirements. I also disclose it in my NW updates and my Pearler review which is a review of my use of the Pearler investing platform.

I am not tracking the exact company valuations for Pearler, but I know the company has had its valuation more than triple and has raised over $10m through VC funding rounds, with more to be raised in later rounds, so I assume the shares are worth a bit more. How much exactly, though? I am not sure. I should probably look into this.

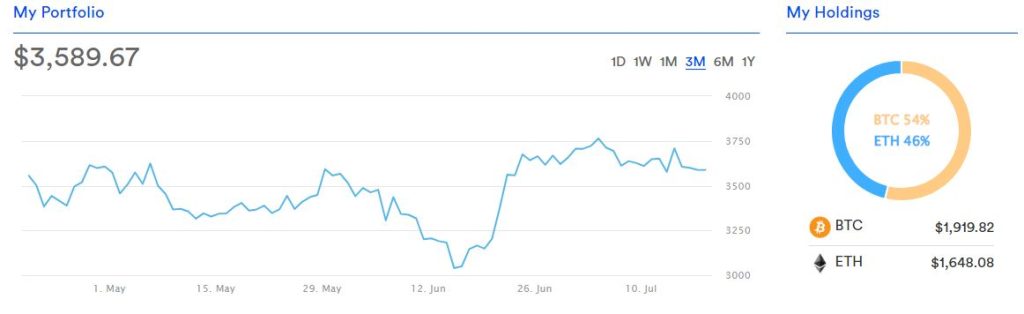

Cryptocurrency Portfolio

I recently set up my Crypto to be included in Sharesight which is great because its included with the rest of my ETF share investments, and its one less thing to log into. Currently sitting at a negative 13% annualised loss since inception, with the following breakdown below courtesy of Coinspot reporting.

Cash – Mojo and emergency fund

Cash reserves are well and truly replenished, and I currently have over 2 years worth of living expenses in cash ($100k) which I have on the mortgage offset account which reduces interest payable on the loan (and actually saves me a bit of tax that I would have to pay if it were invested).

As I mentioned I have started accumulating cash in my mortgage offset account, and haven’t drawn down any of my second split loan which was opened to let me access equity from capital growth (which I haven’t included in my cash balance). This equity, plus cash in the offset will be used for the PPOR when ready, and I will be keeping a minimum of 1 year cash balance after buying the farm property (keeping at least $50k cash), which I will then work towards topping that up to 18 months – 2 years figure.

For day to day spending, I am still just keeping a few thousand in my personal transaction account, and my partner and I have a joint bank account we each contribute to for household bills. Nothing too ground breaking

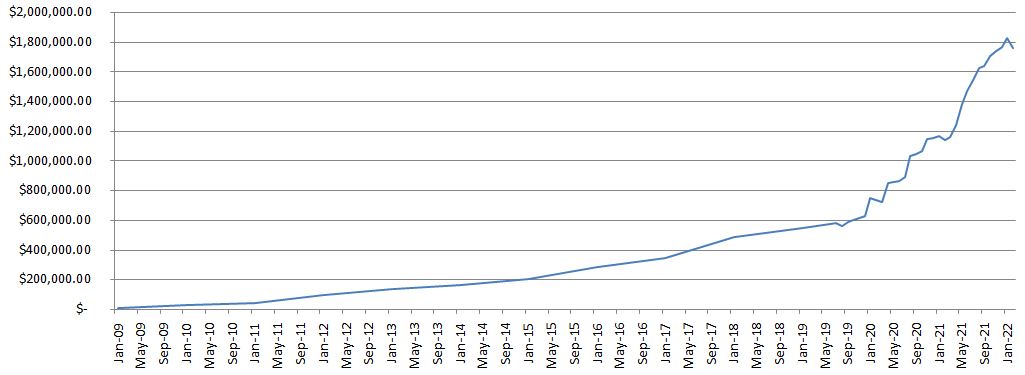

Captain FI’s Net Wealth progression

During my journey to FI I roughly documented my net wealth progression via monthly updates and a graph which was rather crudely constructed in Excel. It demonstrates the ‘somewhat exponential’ journey over my 14 year ‘working’ career. You can access the archives for my Net Worth updates here to see how it’s gone over time. Check out the graph and all the updates below to see how it has gone since the beginning.

I haven’t continued to update a Net Wealth figure post-FI because it isn’t that helpful and starts to cause me money anxiety. Instead, I will continue to put out semi-regular updates about my investments and life post-FI.

| Date | Net worth | Difference | Saving Rate | Notes | |

| Jan 09 | $5,000.00 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK | |

| Jan 10 | $24,000 | +$19,000 | ? | Estimate NW | LINK |

| Jan 11 | $40,000 | +$16,000 | ? | Estimate NW | LINK |

| Jan 12 | $92,000 | +$50,000 | ? | Estimate NW | LINK |

| Jan 13 | $130,000.00 | +$38,000 | ? | Estimate NW | LINK |

| Jan 14 | $161,000.00 | +$31,000 | ? | Estimate NW | LINK |

| Jan 15 | $200,000.00 | +$39,000 | ? | Estimate NW | LINK |

| Jan 16 | $281,000.00 | +$81,000 | ? | Estimate NW | LINK |

| Jan 17 | $340,000.00 | +$59,000 | ? | Estimate NW | LINK |

| Jan 18 | $482,000.00 | +$142,000 | ? | Estimate NW | LINK |

| Jan 19 | $542,000.00 | +$60,000 | ? | Estimate NW | LINK |

| Jul 19 | $578,900.00 | +$36,900 | 84% | Finally began tracking NW this like a proper adult. | |

| Aug 19 | $560,100.00 | -$18,800.00 (-3.2%) | 78% | Share market slight correction, Ok savings. | |

| Sep 19 | $584,744.88 | $24,644.88 | 72% | Share market rebound, savings rate not so good. | LINK |

| Oct 19 | $600,386.00 | $15,641.12 | 84% | Good saving this month. Normal salary, plus allowances, dividends from index funds, tax refund, eBay selling and was working abroad in asia where things are cheap. | LINK |

| Nov 19 | $612,917.21 | $12,531.21 | 76% | Falling short of my savings goal of 80%. Mostly domestic legs this month with higher costs. Also invested in hydroponics. | LINK |

| Dec 19 | $625,350.00 | $12,432.79 | 76% | Good savings of cash (for development) and investment, however higher spending due to Christmas period (Travel and Gifting). | LINK |

| Jan 20 | $865,212.00 | $239,862.00 | 55% | Super settlement was a HUGE boost to NW. $9K growth from stock market. Expensive month lots with lots of unexpected bills – weddings, travel, Booking flights, fines etc. | LINK |

| Feb 20 | $851,802.0 | -$16,592 (-1.9%) | 52% | Large increase in spending on myself this month, still managed to tuck away $5K to put into shares and property. Corona Virus market scare resulted in a correction and gave NW a small negative trend. Time in the market not Timing the market! Became Single again. | LINK |

| Mar 20 | $819, 354.6 | -$31,806.95 (-3.7%) | 80% | Another small step backwards in the NW due to the ‘corona crash’ in full swing. FIRE Portfolio of ETF/LICs down about 15% this month, however due to high savings rate and structure of my superannuation annuity the NW is only down 3.7%. Savings rate good at 80%, higher than usual income (with some slightly higher spending, too). Picking up shares on discount – this is the best outcome for someone in the accumulation phase with good income! | LINK |

| Apr 20 | $847,023 | +$27,668 | 85% | $11,000 in rebound of stock market capital prices alone (up 6%), plus first quarter dividends paid (heavily reduced due to banks withholding dividends). Great savings rate due to COVID-19 lock-down = no spend. Increased entrepreneurial efforts and selling down of physical possessions provided side hustle income. Two standard paychecks from flying activity; domestic day trips only so no allowances. All cash unfortunately had to go into the property development due to contract timing, I am chomping at the bit to buy some more index funds before they go back up in price too much – hence why I am selling most of my toys! | LINK |

| May 20 | $857,859 | +$10,836 | 92% | Some Great sales as I let go of my Super Sport Motorcycle, Some gym gear, expensive flying equipment and a few other various bits and bobs and invested this money. Flying still reduced, but increasing from April. The share market grew as I continued to make my fortnightly investments. I also wrote down the ‘value’ of some of my possessions (liabilities) such as my car, tools and furniture by around $10K to align them to market price (“tell him hes dreaming…!”). | LINK |

| June 20 | $858,650 | +$791 | 90% | Small Net Worth gain as I continue to declutter and simplify my life, despite being off work due to a family emergency. Share market not doing much. | LINK |

| July 20 | $888,218 | +$29,568 | 68% | Majority gain due to share market going back up, low spending due to being on the family farm and at home because of lock down. | LINK |

| Aug 20 | $1,029,293 | +$141,075 | 74% | Became a millionaire. Achieved this massive milestone I set out for myself in Dec 2019. Included unrealised gains in my property development as well as website business. Good savings rate due to not much spending, invested in Aus and total world shares. Investing in my web business. Starting to shift focus away from $$$ and more into looking after my mental health. | LINK |

| Sep 20 | S1,045,486 | +$16,193 | 60% | Officially took time off work for the rest of the year to be close and look after family during major operations. Continued to sell down physical possessions and work on digital business while at home. NW gain mainly due to valuation of websites. | LINK |

| Oct 20 | $1,064,399 | +$18,913 | 80% | Base income (retainer) and leave loading, dividend and websites provided income, as well as raiding my P2P lending capital. Significant bill for property due to design not meeting standards which effectively lowers my equity position, as well as fence being stolen. | LINK |

| Nov 20 | $1,143,433 | +$80,394 | 82% | Big gains came from share market growth (influencing both the Financial Independence share portfolio and Invested superannuation), Business gains (due to increased earnings) and a $30K boost to my annuity thanks to me logging in and checking the fine-print on the accumulation stats. I only invested around $7K. Insane that in one month, I accumulated nearly more net worth than I did in four years from 2009-2012 | LINK |

| Dec 20 | $1,152,920 | + $9,487.32 | 84% | Share market slight drop, Earnings from Business, Contract work, Selling possessions. No share market investments this month (oops! I forgot and money was tight). Invested a lot into the website business this month (way more than planned) and it is still running at a decent loss (plans to turn it cash flow positive in 3 months). | LINK |

| Jan 21 | $1,165,678 | +$12,757 | 79% | Great returns from the share market. Earnings from Business, Dividends, Flying wage, flipping items on consignment. Regular share contribution, investing in micro investing platforms, P2P lending, Investment property and big reinvestment into the business (still running at a loss) | LINK |

| Feb 21 | $1,135,272 | -$30,406 | 76% | Significant write down on property development due to council DA rejection and redesign requiring more money and creating less equity. Offset by small increase to Business value and investments. Simplified my investments and switched over to Pearler. | LINK |

| Mar 21 | $1,155,594 | +$20,322 | 71% | Continued investment into the portfolio as well as growth of investments and business. Gave my notice at work and looking for part time job at home for ‘Barista FI’ | LINK |

| Apr 21 | $1,242,220 | +$86,727 | 74% | Property development back on track | LINK |

| May 21 | $1,379,469 | +$137,248 | 72% | Massive gains in the website portfolio due to revaluation based on recent business income, big growth of superannuation due to annuity increasing (salary increment) and shares generally went up. Crypto went down by about 40% or so. | LINK |

| June 21 | $1,469,989 | +$89,757 | 41% | Quit flying role and moved to Adelaide. Great month for investments, websites producing serious income so accordingly they are valued higher. Spent a lot on furnishing the new apartment and on enjoying some more luxuries. Seeing a therapist to help deal with anxiety from leaving work. | LINK |

| July 21 | $1,543,959 | +$74,732 | N.A. | Set myself up in Adelaide. Did basically nothing for the whole month except spent time with family, relax, sleep and go to doctors appointments. Massive boost to website portfolio AdSense and affiliate incomes, as well as general share market performance. | LINK |

| Aug 21 | $1,624,116 | +$70,156 | N.A. | Relaxed again, focused on mental and physical health, and spending time with family and my partner. Big increases to spending (too afraid to calculate a ‘savings rate’) but also big increases to NW through website portfolio income growth. Finally got the slab poured on the investment property (foundation). | LINK |

| Sep 21 | 1,640,663.85 | +$16,547 | N.A. | Stocks, super etc went down, but business income from websites increased, plus business valuation increased. Property build. got to frame stage, and I also got a dog! Expenses for vet surgery well worth it. Moved into a nicer apartment | LINK |

| Oct 21 | $1,705,907 | +$65,243 | 30% | Big boost from website valuation due to securing new affiliate contracts for recurring income, shares went up nicely. No massive changes to this month. Calculated a savings rate and found myself pretty low due to spending a lot on my garden and going out quite a lot – I don’t think I will calculate this savings rate figure any more. | LINK |

| Nov 21 | $1,739,144.23 | +$33,236 | – | Great month. Relaxing (somewhat). Spent a lot of money doing ‘fun’ things like winery tours, a fine dining experience and self education. Shares moved sideways (well slightly down) but everything else went up. Building got to enclosed stage (roof, walls, windows and doors) but have had some issues with build quality and weather / covid delays. Put a $1000 deposit on the puppy. Stopped tracking Savings Rate. | LINK |

| Dec 21 | $1,764,516 | +25,372 | – | Spent nearly the whole month with family, did some work on the website portfolio. Traffic recovered from google algorithm changes. Invested $10K into Stockspot and Sixpark, $1K into ACDC, $100 into Comsec pocket and $100 into Bamboo, $260 into BTC, $4K into ETFs through pearler. Paid the $3000 balance for the puppy. | LINK |

| Jan 22 | $1,826,633 | +$62,117 | – | Stock market slightly down, Massive boost to website traffic (overall its more than doubled). Invested $10K VTS, 2K VEU through pearler, Paid for Angels cancer surgery, bought more BTC and ETH, bought a parcel of ETHI on commsec pocket. | LINK |

| Feb 22 | $1,757,210.57 | -$69,422.93 | – | Stock market down, Website business revenues down and additional spending on content and staff for business, Additional property development bills, some unexpected expenses, Wrote down the value of some of my personal property (and gave stuff away). | LINK |

| Mar 22 | $1,701,410 | – $55,799 | – | My last ‘regular’ monthly Net wealth update as I give notice at work and finish up my non-flying job. | LINK |

| Q3, 2022 | Over $2M | N.A | – | Six months of Early Retirement in Rest mode! I stopped tracking my net wealth post-FI, my dog passed away, I gave away most of my physical stuff and moved to become my mums live-in carer, met a lovely girl, bought a puppy. Had some incredible months with semi-passive website income but overall neglected the business and regular (stable) revenues decreased. | LINK |

| Q1, 2023 | Over $2M | N.A | – | One year of Early Retirement! A lot of (sad) changes, the passing of my mother and family feuding, homelessness, selling my ‘nursery’ of plants, and traveling overseas for a few months. Finding a new home to settle, couple of domestic trips flying to Tasmania and Queensland a couple of times, and plenty of camping and road trips within SA. Did not work much on the business at all and lost a few more contracts and had to cut staff. | LINK |

| Q2, 2023 | Over $2M | N.A | – | Getting back on top of things with podcasting and blogging more regularly. Focusing on building our ‘rich life’ and deliberately increasing spending in areas such as food, travel and convenience. Did a few interviews and went on a few podcasts. |

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Impressive update CaptainFI! The level of detail you’ve provided is truly remarkable! Congratulations on achieving a 2M Networth as an individual! With such savings you should be set to live a rich life!

Regarding our approach, we’ve opted not to disclose specific numbers on our blog (even though we are anonymous). Instead, we’ve focused on sharing how much money we do spent. Do you believe it would be beneficial for us to reconsider and also share our numbers?

G’day NN, thanks mate – I am definitely excited for the future. Re: Disclosing numbers, I dont know. I remember back to when I started, it was pretty intimidating seeing people with huge net wealth figures but I was still somehow attracted to reading them lol. Who doesnt love a good nose through someones finances. I think it does provide a good level of transparency and I guess does give credibility to the publisher (unfortunately there are a lot of broke people online telling people what to do with their money lol). However the old saying – once you put something on the internet, theres no taking it back. I felt more comfortable being anonymous because I disclosed my net wealth, but then slowly, some friends, coworkers and family members did discover my blog (maybe looking over my shoulder onto my laptop, however some did connect the dots or recognise some of my pictures). This has certainly impacted my relationships with some friends and family – its obviously no secret amongst my private social circle and family that I am ‘good’ with money (after a 14 year career as a pilot and always being careful and investing), however I feel that once they know my net wealth is in the millions then somehow I become the ‘bad guy’ for not ‘helping’ them more. If I were you, I would probably keep it private 🙂