Your savings rate matters. Like it REALLY matters. Your savings rate is the number one factor for the time it will take you to reach Financial Independence. At the end of the day, it is a combined measure of how fast and efficiently you are increasing your Net Worth.

Over time the effect of compound interest on your investments will help, and in the long term compound interest from reinvested dividends can do some very heavy lifting, but in the short term and especially for those seeking FI, your savings rate is actually your Financial Super power!

So, what exactly is the saving Rate?

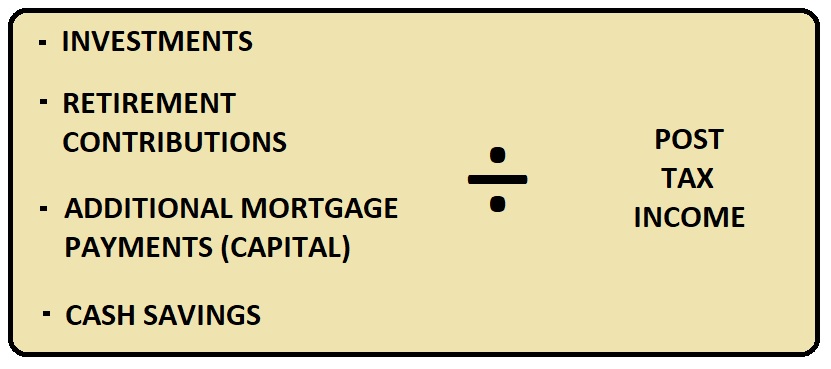

Your saving rate can be calculated really easily. Some people choose to calculate it different ways and make it quite complicated, but the overwhelming majority of those in the finance community calculate it simply as the gain in your Net worth (from investments made using your income) divided by your post tax income (whatever actually hits your accounts) over whatever time period you are choosing

- Investments: Taxable investments in Shares such as ETFs and LICs in conventional taxed portfolios bought through a discount online broker using your post income tax dollars / earnings. Also include any taxed retirement account contributions (i.e. anything above the tax free thresholds)

- Retirement Contributions: Any tax-free (or reduced) Retirement contributions you make to your 401K, IRA, Superannuation or other tax advantaged retirement investment accounts. This feels like a sneaky ‘double dip’ since the money doesn’t usually come out of your post tax income (retirement contributions are often tax leveraged such that the contribution is taken out of your earnings before income tax is applied). This is a legit way to calculate it in my mind, and in the mind of the majority of those in the FI community

- Additional Mortgage payments: Any additional mortgage payments you are making to pay down the capital value of the loan faster and increase your net Equity in the property. I personally don’t include the interest portion, as that doesn’t contribute to your equity or net worth.

- Cash savings: Any Cash you are ‘Stashing into your emergency fund, brokerage account or mortgage offset (for the love of God please don’t stash it under your mattress, even if there is a threat of negative interest rates…)

- Post tax income: Whatever hits your account! Combine wages, dividends, rental income, side hustle income and any other forms of cash getting into your hands!

Why your saving rate matters

Your saving rate matters because it is telling you how efficiently you are growing your net worth. Remember you can be earning a Million dollar salary, but if your spending it all then your not really getting ahead! This is why it can be so dangerous to fall into the Keeping up with the Jones’ lifestyle inflation trap

We all know a ‘rich’ family that does it, high income earners maybe Doctors or Laywers, or fancy pants Engineer that drives two luxury SUVs that are garaged in a mansion and who go skiing in Canada or swimming in the Bahamas, but who are drowning in personal (non productive) debt. They can’t seem to understand how their ‘poor’ neighbour who drives a 15 year old station-wagon only has to work part time, and only when they want to! (this is starting to sound like the book the Millionaire next door…)

Ideally, a high saving rate combined with a high salary would be an all star combination, and would totally smash financial independence out of the ball park! But the reason why this works is because the high salary can be used to overcome a higher cost of living. A high savings rate is so powerful by itself because of the cost of living factor; it implies you have found a very efficient way to live for your income.

Cost of living

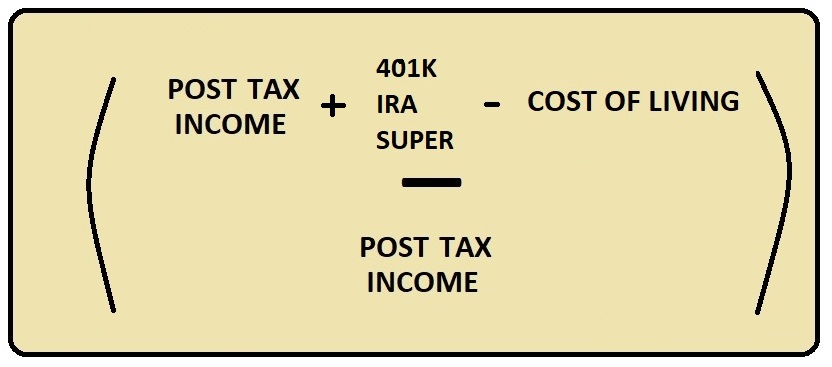

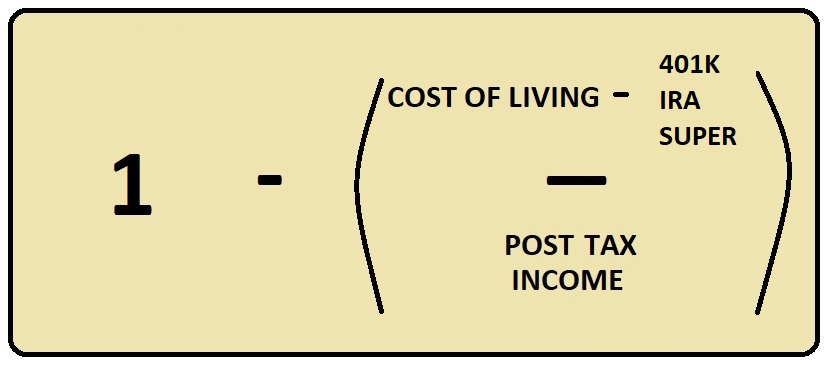

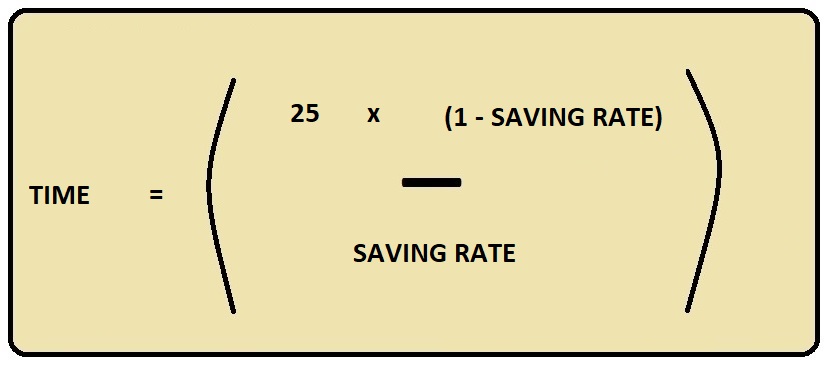

Remember your Savings rate is essentially calculated as your growth in net worth (from investments bought using your income) divided by your post tax income. Provided you are investing at 100% of your capability, another way to express the amount you invest is your income (plus tax free retirement contributions) minus your cost of living.

What this essentially shows is that your savings rate is inversely proportional to your cost of living; the higher your cost of living, the lower your savings rate. When you put it like that, it just sounds like common sense, right?

Why this matters is because if you maintain this cost of living as a percentage of your salary once you transition into ‘Financial Independence’ and remove the need to work, then you can then completely remove the income factor from the equation when determining how long it will take you to build the portfolio in the first place; it depends only on the saving rate.

Truth be told, the cost of working is substantial, and most FIRE retirees find their cost of living actually decreases significantly once they stop work (no more need for expensive commutes!) and they usually find profitable projects or fun businesses to start.

Your Saving Rate determines your required working career

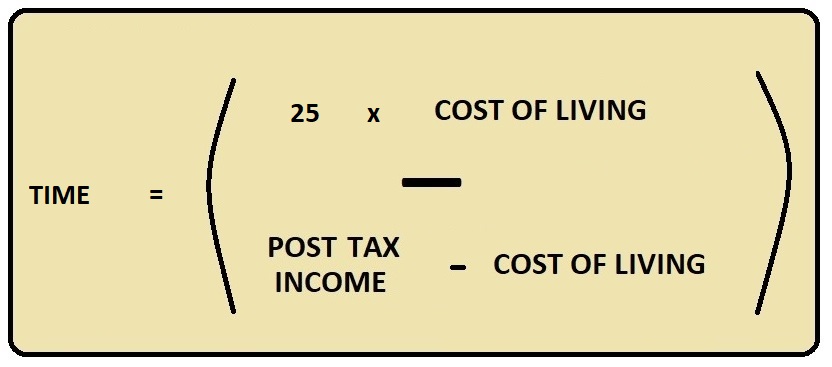

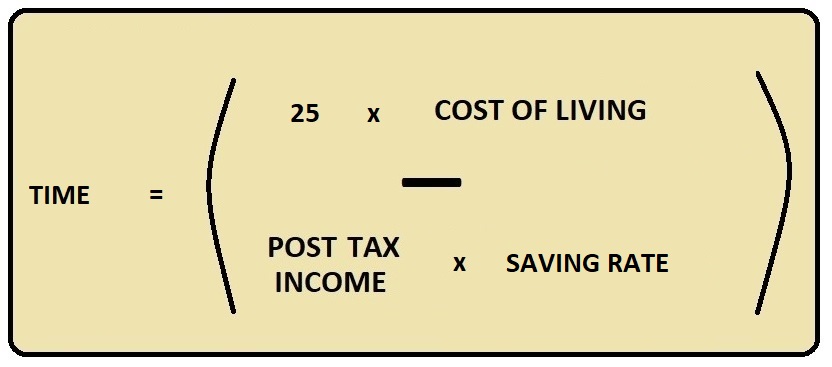

For example, if you earn $100K after tax and your cost of living is $20K, then your saving rate is 80%. Each year you are saving $80K, and that $80K can safely produce $3,200 to live off using the 4% rule. Ignoring the effect of compound interest, income tax brackets or inflation, a very simple calculation is 20,000/3,200 = 6.25, which means that after 6.25 years, you will have a half a million dollar portfolio which can generate $20K in passive returns.

This matches your cost of living – so hey presto! You’ve hit FIRE, and no longer need to work (although you may still like it and choose to do so). This is why we sometimes say your FIRE number is 25x your annual expenses (using the 4% safe withdrawal rate rule). After accounting for compound interest earned, and inflation (CPI), you can actually shave off 9 months from your required working career and have it down to 5.5 years.

The simple math is shown below;

What about a lower saving rate? Well say you only saved $20K of that $100K salary, the cost of living for your lifestyle is $80K. This means according to the 4% rule (multiply by 25) you would need TWO MILLION dollars to reach FIRE. $2M divided by $20K is 100, which is clearly a bit ridiculous because over such a long time frame compound interest has a massive effect. After plugging this into an excel spreadsheet with some more complex math (I wont bore you with the details) using an 10% return adjusted for 2% inflation (real ‘purchasing’ return of 8%) it comes out to just over 37 years. Almost four decades!

OK so that 6 figure salary might sound like an unrealistic example, so what about the average person with a presumably lower saving rate? If you made the average Aussie wage of $50K, you’d pay $9K in tax, and with an average cost of living of $34K you could manage to tuck away $7k per year or a savings rate of 17%. Your cost of living is $34K so you’ll need an $850K portfolio (25 times annual expenses). Using the Excel spreadsheet, you would need to work for 40 years to achieve this! 40 years is a long time!

Whats insane here, is that the average Aussie only saves about $400 a month or less than $5K a year – making the average saving rate around 11%. The figures are even crazier for the US, which work out to be 7%. This either tells you the cost of living is too high, or people are just wasting their money on dumb shit (I’ll let you decide which factor is really at play)!

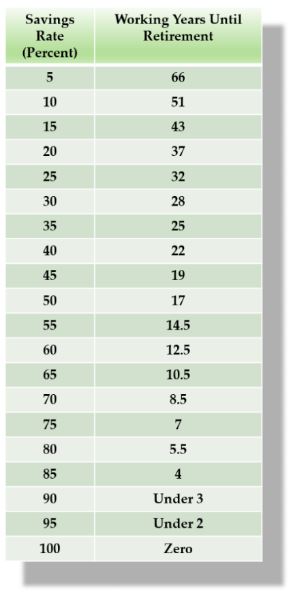

Mr Money Mustache has crunched the numbers and produced this very informative table below (sometimes seen in graph format) your viewing pleasure. It plainly relates savings rate (in percent) to working years until retirement. Take a good hard stare at it. Check out where the average saving rates correspond to working years until retirement. Where do you rank?

How to boost your saving rate

Earn more

One way to boost your saving rate is to try and earn more. The boosted income means you can direct more into your savings and investments, provided you don’t inflate your lifestyle. Earning more is what most people tend to think you need to do to become wealthy, but beware: earning more can sometimes be a trap!

Yes that’s right, earning more can be a trap. This is because as you earn more, you pay more income taxes. Not just more, but a higher percentage of your earnings as you rise in the incremental income taxation tiers. Most countries have an incremental income tax system (which I believe is fair), but the top tiers can be as high as nearly 50% of your income!

Some might call this a perfect example of ‘the law of diminishing returns’ and would wonder why you would spend all of your time and effort in order to earn more to pay income taxes. The other aspect of this trap is that not only will you paying more taxes, but as you will likely be working harder or longer hours you will be more tired, and therefore more prone to spend your money ‘because you deserve it’. Don’t have time to cook my own dinner because I’ve been working hard? Uber Eats! Don’t have time to service my car because I’m side hustling on weekends? Call a mechanic! You get the idea..

As long as you don’t lifestyle inflate or burn yourself out, earning extra money can be a massive boost to your savings rate and help you get up into those high rates so you can reach Financial Independence sooner! Examples include negotiating a raise at work, starting a profitable side hustle, picking up extra shifts or a second job, or even as simple as selling your old stuff!

Check out these posts on awesome ways to earn more money

- Earning more: Side hustles and passive income.

- Earning more: How to make more money.

- Selling your unwanted stuff: Selling online to reach FI.

Spend less

To boost your savings rate you essentially just need to spend less. Some people write out a budget to help them spend less and save more, but for me it is a fundamental mindset shift into a philosophy about efficiency.

I always am seeking out ways to do things better, more efficiently and with less waste. For example I ride my bicycle to get my weekly groceries (which is mostly whole food plant based stuff like fruits, veggies, nuts and grains) which saves me from having to wastefully burn petrol pushing around over 1600kg of metal in the form of my car!

Start by listing all your expenses – go through a years worth of your bank statements (stop using cash if you can). Go through the list, work out what is essential and what is not – what can you substitute? Could you switch your gas guzzler for a more efficient smaller 4 cylinder car? Could you substitute an expensive animal based meal with a much cheaper and healthier plant based one? Could you ride your bike or catch public transport rather than drive? Could you read a library book rather than paying for a movie? You get the idea!

Check out these posts on awesome ways to save money.

- Rules of thumb: Rules of thumb for FIRE

- Save money on housing: Rent or Buy?

- Save money on Groceries: Food shopping for FI

- Save money by gardening: Growing Financial Independence

- Save money on your Car: Driving to financial independence

- Write a budget: How to Budget for investing

A comprehensive list of all of my saving tips can be found here: Captain FI’s saving tips

Remember, cutting your spending is FAR more powerful than boosting your earning. Each dollar you save 1. increases the amount of money you have to save and invest (which will then immediately start working for you forever to produce investment returns) and 2. is a dollar less of income you need, reducing your required portfolio size to sustain you and 3. Reduces the amount of income tax you need to pay (both now when earning it, and in the future on your investment profits!)

Geographic arbitrage

Geographic arbitrage sounds fancy, but it just means living somewhere more affordable! This means somewhere where the difference between your income and the cost of living is the greatest. This is probably my number one tip for how to boost your Savings Rate!

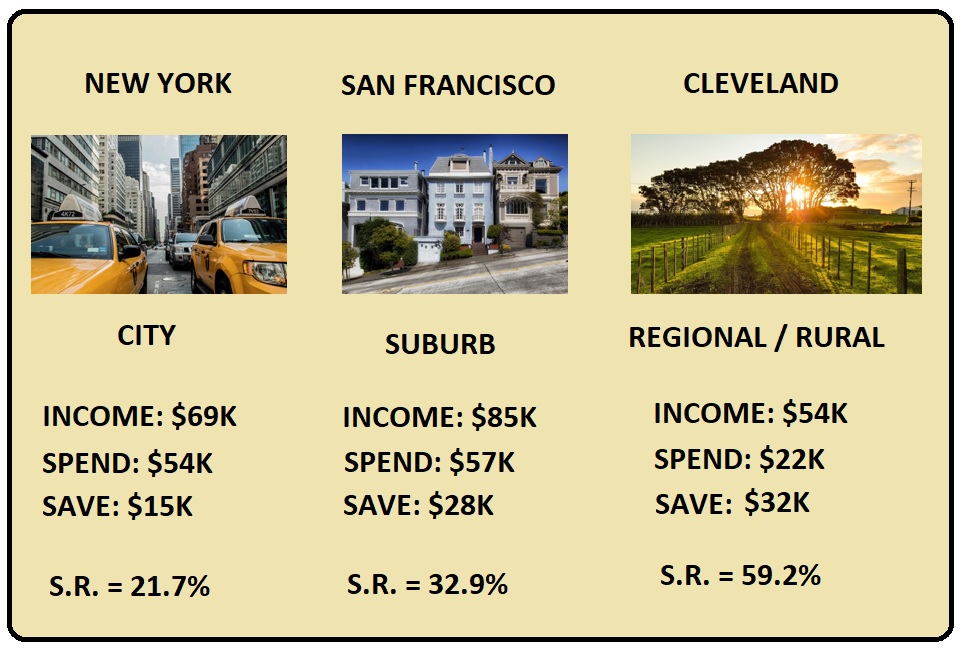

For example, if you lived in New York and had a the typical high salary that is earned there, you might think your pretty wealthy. However, considering the extremely high cost of living there and the high likelihood that you are spending the majority of your pay, your net worth might not actually be growing as fast as it could be!

The average New Yorker could be achieving a savings rate just over 21% without breaking a sweat. (Remember these are average numbers and the average person has probably never heard of FIRE so they are likely pretty spendy and wasteful!). This would give them a working career of about 36 years!

For Aussies, the parallel here would probably be Sydney or Melbourne. I’m sure with a bit of mindfulness, even New Yorkers or my fellow Sydney-siders could increase their Savings Rates and wind down their years until reaching FI…

If you decided to move in order take a higher paying job in San Francisco, your spending for cost of living could even increase – San Francisco is listed as an extremely high cost of living area – over double the average US cost of living! But, your earning proportionally more so as long as you don’t lifestyle inflate, your savings rate gets a hefty 11.2% boost up to almost 33%, and your working career is down to 26 years – an entire DECADE shorter!

But what you mightn’t have considered is that if you lived in a Regional or rural town near Cleveland, Ohio you might be earning less, but statistically your cost of living is much lower too. When you crunch the numbers, this actually works out as a better place to live if you care about your Net Worth and reaching financial independence! The average Cleveland resident living out of the main city area (or congested suburb) is able to save a cool 59% without breaking a sweat, giving them an estimated working career of 13 years, knocking off over a decade compared to San Francisco, and over two decades compared to New York! With some FIRE coaching and reading of this blog, they would be sure to be able to bump that up to into the 80+% region and reach Financial Independence in under 5 years!

Summary

Thanks for reading. By now you should fully understand just how important your Saving Rate is, and why it matters for reaching Financial Independence. What is your savings rate, and how long will it take you to reach FI? If you have any fantastic tips on boosting your Saving Rate whether that be through earning more, spending less, or maximising your investment returns, be sure to let me know in the comments below so we can all benefit!

Further reading

Pete Adeney, Better known as Mr Money Mustache is a big proponent of maxing out your Savings Rate as high as possible. He even wrote an article titled The Shockingly Simple Math behind early retirement, where he discusses the Saving Rate and time to reach Financial Independence

Don’t believe him? Check out the ChooseFI podcast and blog, where you can even enter your own details to calculate your own savings rate, FI number and your time to reach Financial Independence!

For more Tips on Saving, check out all of Captain FI’s saving tips here: Captain FI’s saving tips

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.