Superannuation in Australia and its role in early retirement from an experienced and long term investor who has reached Financial Independence.

Most countries have a form of retirement plan or structure that gives employees a tax incentive to save for retirement. This usually takes the form of tax concessions, contribution matching for low income earners, or even being tax free altogether.

Over time, the power of compound interest works to produce a sizeable nest egg which can then be drawn down to fund your retirement in your later years.

In Australia, we have a mandatory retirement scheme called Superannuation. Super is similar to a 401K scheme, Roth, Roth IRA or an Individual Retirement Account (IRA), but there are one or two critical differences.

The superannuation portfolio or account itself is essentially a tax sheltered stock portfolio. This was designed to reduce the reliance on social security and the age pension, and put the onus on the individual to look after their retirement.

So how can we maximise the benefit of our super, and what role does it play for long term investors on the path to financial independence, who perhaps want to retire early? Read on to find out.

CaptainFI is not a Financial Advisor and the information below is not financial advice. This website is reader-supported, which means we may be paid when you visit links to partner or featured sites, or by advertising on the site. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Quick Super facts

- In Australia’s Superannuation system, government-mandated employer contributions to your super is called the Super Guarantee Rate which is currently that 11.5% (from July 1, 2024) of your salary must be deposited into your super for retirement (this figure will increase to 12% by July 2025)

- Super contributions are taxed at 15% (up to the concessional cap)

- Super growth within the fund is taxed at 15% up to a $3M balance (although your total tax payable can be less depending on what actually happens within the super account)

- CGT rate within super for assets held more than 12 months is only 10%.

- Maximum concessional contribution (15% ingoing tax) $30K per year (from July 1, 2024)

- Maximum non-concessional contribution (fully taxed at your marginal rate) – $120k per year (from July 1, 2024)

- Maximum balance cap $1.9M for a tax free pension phase account

- Above the maximum accumulation balance cap of $3.0M tax rate becomes the standard company rate of 30%

- Aim for 100 months of living expenses in your super account at retirement as a benchmark for a good place to be – this provides around 60% of your pre-retirement income.

Introduction to Superannuation

Under the Superannuation guarantee, according to the ATO (Australian Taxation Office) if you are over the age of 18, or under 18 but working more than 30 hours a week, your employer must pay superannuation contributions as a minimum percentage of your wages into your superannuation portfolio – but they can contribute more. This is usually called the employer contribution.

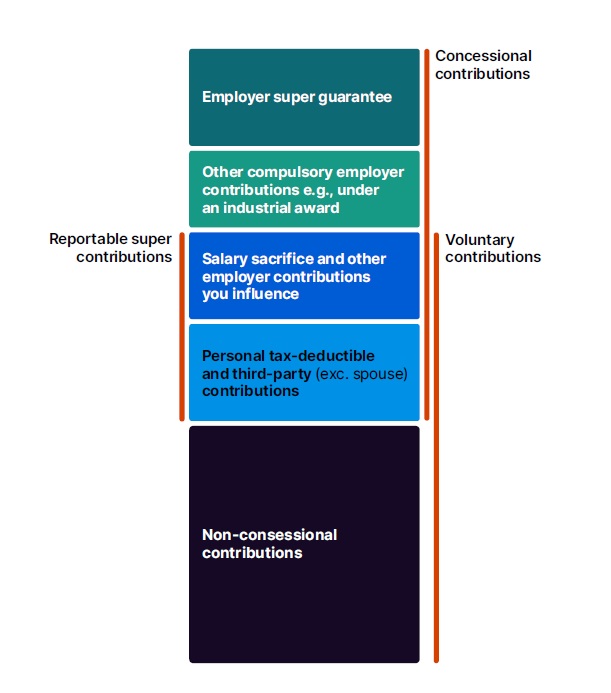

You can make voluntary contributions or salary sacrifice your own before tax dollars up to a maximum of $30K concessional (tax advantaged) contributions per year, or make a non-concessional (using after tax money) into the fund up to $120K per year.

The ATO allows some perks for people with smaller super balances to help you invest more and grow them quicker – such as;

- Carry-forward perk: Carry forward unused contribution cap amounts from up to 5 previous financial years

- Bring-forward perk: Bring forward 3 years of contributions to contribute 3 times the annual non-concessional contributions cap

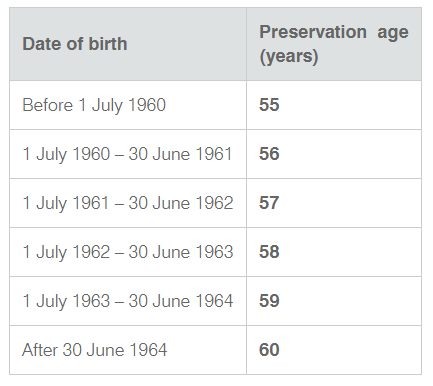

Your Retirement accounts build up during your ‘working career’, and then when you retire you can usually elect to either take it as a lump sum amount (which a lot of people do to pay off their house or any other debt they may have) or you might otherwise have the option to take it as a (hopefully indexed) pension. So what’s the catch? You can only access the funds when you hit your preservation age…

Preservation age

Types of Superannuation schemes

There are many different and varied superannuation schemes in Australia – such as;

- Pooled schemes

- Industry super funds

- Self Managed Super funds

- Wrap accounts

- Defined Benefit Schemes

Pooled employer or industry super funds

Pooled funds are one of the most common types of super and probably what you are most familiar with. These are often the ‘default’ MySuper funds when you get a job that your employer signs you up to, because you legally need to have your super going somewhere. These default funds meet some basis tests (assets, fees, insurances) but often aren’t all that appropriate for everyone’s circumstances.

Superannuation companies (like HostPlus) are the trustee for your investment, which pool your money with thousands (or millions!) of other investors and then allocate this across various investment assets (cash, bonds, shares, property, crypto etc) via a fund manager – or more commonly, via hundreds of fund managers. Most commonly, this will be a ‘balanced fund’ with something like 40% Australian shares, 40% international shares, 5% cash and 15% bonds.

There has been a growing trend towards index fund offerings within these pooled funds, with strong downward pressure on fees. Some pooled super providers even offer ‘fee free’ index offerings – but it is not as simple as that and there are some other catches! Astonishingly, the majority of pooled funds have ridiculously high fees which erode your returns.

In my opinion, you shouldn’t be paying more than about 20 basis points or 0.2% MER – anything above this is just daylight robbery. I personally believe fund management expenses above 0.5% should be considered a criminal activity and illegal as they slowly and silently steal wealth from hard working Aussies.

A massive draw-back to pooled super funds is provisioning. Because you are lumped in with millions of other Australians all at different stages of their career – people switching funds or retiring and withdrawing their ‘units’ from the fund causes Capital Gains Tax events. Whilst you might be only at the start of your career and contributing for another 40 years, you are essentially subsidising the CGT event for people retiring or ‘switching lanes’.

To account for this, the pooled funds ‘provision’ 10% of their returns to pay for this tax liability, and this gets taken out each year – for example if the assets returned 10% yield, this means you only get 9% yield, as 1% is provisioned for the capital gains tax due on it. This is a big deal.

This means you miss out on the growth benefits of deferred tax liability – similar to the discussion between dividend vs capital growth style investing. It is better to let your asset grow untaxed and simply pay your tax at the end of the period when you sell the asset and trigger the capital gains tax event. If you are constantly ‘chipping’ tax off the investment, it will not grow as fast.

The other big turn-off with pooled funds is asset allocation. You might think you are getting a certain asset allocation based on the investment choices that you submit to the fund, but pretty much every super company just does whatever they want with your money anyway. They will pay you the RETURNS and charge the fees from whichever asset classes you have selected, but ultimately they reserve the right to invest however they see fit.

Astonishingly, this is legal and is standard industry practice. Since the main driver of returns is asset allocation, it seems absurd to relinquish control over this.

If you don’t believe me read my article on HostPlus superannuation where I unpack the Product Disclosure Statement with help of some University Academics and then question their head office to find out what it all means.

In summary – Pooled super funds are easy, convenient, and can also allow you to pay for some of your insurance cover (TPI, Death and income protection) in pre-tax dollars in one simple place. However, paying for convenience and the long term returns of these funds compared to the index is questionable due to the effect of fees, asset allocation and provisioning.

Self Managed Super Funds

There are over 600,000 Self Managed Super Funds in Australia. They have a specific purpose but are not appropriate for most Australians – they have high fees and compliance costs and are often sold as an inappropriate product to hold real estate by property spruikers.

SMSF can be appropriate for small business owners (for example super fund holds the business premises etc) but only in specific circumstances. I WOULD NOT open an SMSF without expert advice from at least three different independent financial advisers.

Wrap Accounts

‘Wrap accounts’ are technically called investor-directed portfolio services. These are an attractive alternative to ‘pooled’ employer or industry super funds, since you gain more control over your investments and you are not impacted by the actions of other investors within the pool (such as capital gains tax provisioning which reduces your individual return).

Some common ones are provided by Colonial First State, Net Wealth, Hub24, BT, Macquarie, and Asguard. These companies will be the trustee of your Super fund, and give you the ability to buy exactly what you want – for example, you could replicate your ‘FIRE share portfolio‘ and have your superannuation set up to be exactly the index funds you want them to be.

Defined benefit funds

There is a special subset of superannuation packages called defined benefit funds, which allow their members to access their super at a set age regardless of when they were born. Defined benefit funds work a little differently to regular super, and are actually more like a guarantee or life insurance scheme as opposed to a portfolio that is directly invested in the stock market.

Sometimes they are referred to as Annuity schemes or annuities for short.

Defined benefit funds are actually some of the best retirement plans out there, and many have been created for government workers (by government workers…). In fact, everyone has cottoned on as to how good they are and now due to financial pressures the Aussie government is reigning in on them – there are pretty much no defined benefit funds left that you can join (unless you were already signed up as part of one previously).

Contribution match

Some superannuation packages for low income earners feature contribution matching by the federal government; that is, if you are on a low income stream, you might qualify for contribution matching. This means for every dollar that you contribute to your super, the government will contribute an extra dollar, helping boost your total retirement benefit.

Superannuation fund review

Check out my reviews to compare super funds:

- HostPlus super

- UniSuper Review

- REST Super review

- ART Super review – Australian Retirement Trust

- Australian Super Review

- MLC Superannuation Review

- Barefoot Investor Superannuation funds

- Vision Super

- ANZ Smart Choice Super

The Role of Superannuation in a Two-Tier FI Retirement

In general, when most of us turn 60 the government deems we have officially hit retirement and grants us access to our retirement nest egg. Little do they know that FIRE retirees have been living it up retired for the past 30 years somehow! Although you can’t generally access it before your preservation age, super helps FIRE retirees in a different way.

As long as your FI portfolio can last you between early retirement and preservation age, you can draw down on it until you can access your Super. And all the while, your super is growing in its tax sheltered area. Whilst you work investing and building up your FI portfolio, your employer is still investing into your super.

Further, any additional cash you’ve stashed in it along the way was only charged at 15% tax rather than your (presumably) much higher marginal rate. This is called concessional contributions and in Australia, this is currently capped at $30,000 per year for individuals.

Of course, there are ways for dodgy employers to get around having to pay super, such as hiring you as a contractor by making you get your own ABN (Australian Business Number). Some other companies blatantly refuse and break the law, hoping no one finds out, but they usually end up in court or in jail and have to pay out damages.

So, should you contribute extra to your super? That depends. I think you should aim to at least get $100K+ within your superannuation, which will really let it compound and grow between the time you decide to ‘FIRE’ and when you reach preservation age. There is a handy calculator on the MoneySmart site that can help to visualise this. Having said that, I think you need to sort out a few key areas in your personal finances before you consider making additional super contributions, such as:

- Build an emergency fund of at least $2,000

- Paying off all high interest debt (credit card, personal loans, car loans)

- Boost your emergency fund to 3-6 months cost of living

- If you plan on buying or building a house – getting at least a 20% deposit (or conversely paying your home loan down to 80% LVR)

- Build up a nice portfolio in a conventional brokerage account to give you flexibility ($20K or more)

Once you have these five things sorted, then it is probably a good time to direct that income firehouse of cash into boosting your super balance, at least to around $100K – because if the market continues to do its thing (which it has for the last few centuries) and your super investments grow at 10% per annum, after 30 years (Early retirement at 30 and preservation age at 60) you should have nearly a cool $2M in your super accumulation phase account!

Of course, if you are planning on retiring after 30 you might want to massage these numbers and have a little in your super as it will have less time to grow.

Once you’ve got over $100K (or your set figure) in your super, I would then turn the focus back onto your conventional brokerage (taxable) investments. This is the strategy I have used for Early Retirement, and I am focusing everything on outside super currently and do not contribute extra.

Other tax effective structures

I didn’t have enough invested at the start to really warrant starting a discretionary trust structure, however, since the income from the FI portfolio is starting to push me into the higher tax brackets, it is now worthwhile. By using a discretionary family trust, I can allocate the tax burden of the FI portfolio by distributing income to members of my family on lower tax brackets than me.

This tax saving more than covers the administrative burden of the trust. Whilst I’m not exactly getting the same low flat 15% taxation rate I would in Super, it’s still better than nothing, and I can control the trust meaning I can direct its distributions to me when I retire.

If you compare this 15% to the marginal tax scales above you can see that someone with an income of $45,000 is paying a total tax rate of approximately 11.3%, and any income distributed to them to take them over the $45,000 bracket would be charged at 32.5%, rather than the 37% or 45% you may be getting charged at the higher tiers.

If you can distribute to a family member not earning an income such as a non working spouse or stay at home kids (over 18) studying at college, then they will potentially pay zero tax on distributions up to $18,200, so it can be a very effective way to save tax for families.

Captain FI’s Superannuation

Personally, I didn’t make as much money as some of my colleagues flying private jets for celebrities or for various airlines. Overall though, I had a pretty good remuneration package and benefits which includes above award superannuation contributions, as well as generous allowances.

After 13 years in the workforce I currently have a healthy super balance which is made up of an annuity and a conventional invested super account (100% shares) – you can read more about it in my transition to retirement financial planning process, HostPlus review or my Net Worth updates.

I used to think contributing extra to my superannuation was a good thing, and I would try max out my contributions without physically starving or running out of money. It turns out this was probably a good thing (as discussed earlier) however I didn’t really have a strategy or even thought about why I was making extra contributions at the time.

For someone happy to work that 8-5 grind until they are in their sixties, and who wants to save a bit of tax, it probably is a good idea if they want to be more comfortable in retirement (if they didn’t work themselves into an early grave first!). It is also a great idea to max out your contributions for the first few years of your working career to really supercharge your balance and then let compound interest do its thing over 40(?) years to grow you a massive super balance.

I realised though, that when I decided I was going to aim for FIRE and retire early, I was going to need that money sooner than the preservation age.

So rather than contributing to my superannuation or any other tax sheltered retirement accounts, I just decided to build up my FIRE portfolio outside of superannuation. Whilst it wasn’t going to be as tax effective as superannuation, I could make up for this by being very mindful about spending and really paring down my cost of living. Then I just direct this torrent of savings into ETFs and LICs.

Before retiring I was regularly hitting an 80%+ savings rate when I crunched the numbers in my monthly reviews, and this frugality is my super power and offsets any tax inefficiency.

Conclusion

Superannuation and retirement accounts can be a very effective way to grow your retirement nest egg, but they can have some serious drawbacks about when you can actually access your money. Complicating things further is potential legislative change which might see the preservation age continually creep upwards as we see a global ageing population and a greater strain on social security, healthcare, and the age pension. I will be exploring Wrap accounts for my super in the future.

What are your thoughts on tax sheltered retirement accounts? Do you have Superannuation or use a 401K account? If so, do you max it out with concessional contributions? Let me know in the comments below.

Financial Disclaimer

Financial Disclaimer: CaptainFI is NOT a financial advisor and does not hold an AFSL. This is not financial Advice!

I am not a financial adviser and I do not hold an Australian Financial Services Licence (AFSL). In this article, I am giving you factual, balanced information without judgment or bias, to the best of my ability. I am not giving you any general or personal financial advice about what you should do with your investments. Just because I do something with my money (or use a particular service or platform) doesn’t mean it is automatically appropriate for your personal circumstances. I do not recommend nor endorse any financial or investment product, and my usage or opinion of any product should not be interpreted as an endorsement, advertisement, or intent to influence.

I can only provide factual information based on my journey to Financial Independence, and that is provided for general informational and entertainment purposes only. I make no guarantee about the performance of any product, and although I strive to keep the information accurate and updated as it changes, I make no guarantee about the correctness of reviews or information posted.

Remember – you always need to do your own independent research and due diligence before making any transaction. This includes reading and analysing Product Disclosure Statements, Terms and Conditions, Service Arrangement and Fee Structures. It is always smart to compare products and discuss them, but ultimately you need to take responsibility for your use of any particular product and make sure it suits your personal circumstances. If you need help and would like to obtain personal financial advice about which investment options or platforms may be right for you, please talk to a licensed financial adviser or AFSL holder – you can take the first steps to find a financial advisor by reading this interview, or by visiting the ASIC financial adviser register and searching in your area.

For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.