Review of Up Bank from a long term customer. Read on to find out if this bank account and banking app is suitable for those pursuing financial independence.

Up is an innovative Australian digital banking app that offers entirely digital, cloud based personal banking through the Up mobile application. Because of this, and their strong focus on technology and rapid development, they are often categorized as a ‘neobank”. With over 500,000 customers, Up is targeted at a millennial audience and has had six years of proven functionality with outstanding reviews, winning Up several industry rewards such as ‘Digital disruptor of the year’ and ‘Best digital bank’.

This article will explore Up and my experience using its services to determine whether I will personally remain a long-term Up customer and move away from traditional banks.

“Up is a digital bank designed to help you organise your money and simplify your life.”

Up

Up: The Good

- Excellent banking app with 24/7 chat support

- Features instant PayID, OSKO and BPAY

- Supports Mobile pay: Apple, Google, FitBit, Samsung pay

- Bank @ Post available

- Unlimited savings accounts

- No monthly fees, no international transaction fees

- Does not support fossil fuel companies like traditional a banking system

- Now features Up Home for home loans

Up: The Bad

- Only one debit card is issued – can’t do Barefoot buckets physical card strategy

- No physical branches (like most neo banks)

- Have to contact customer support to get your sign-up bonus

- ATM fee applies at non ‘big 4 banks’

- No Credit cards or personal loans

Verdict: Up and the Up banking app is great – safe and easy to set up and use your transaction and savings accounts. Get $10 for FREE to try it out here.

CaptainFI is not a Financial Advisor and the information below is not financial advice. This website is reader-supported, which means we may be paid when you visit links to partner or featured sites, or by advertising on the site. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Introduction to Up Bank

Up was co-founded by Dominic Pym and Grant Thomas under a Melbourne based tech development company called Ferocia. Partnering with Bendigo Bank and Adelaide Banks for their financial licences, as well as Google for their cloud based system, Ferocia developed the Up platform in 2017/18 and begun offering banking services through the Up mobile application in 2018.

The team behind Ferocia knows a thing or two about developing mobile banking applications since they were the ones who previously designed Bendigo and Adelaide Banks’s mobile banking applications – making them ideal business partners to work with.

Up offers basic bank account services with debit card transaction services through MasterCard, great customer service, and innovative features like Apple and Google Pay, Samsung pay, Round Up, and expense tracking. Users over 16 can sign up and be using Up in under 5 minutes by downloading the app and providing very basic identification. With now over 800,000 active users, Up has been a revolution for online banking, as younger people flock to it for its simplicity, value, features and good support team.

UP Accounts

Up offers two types of accounts for their online banking app;

- Transaction accounts: ‘Up Everyday Account’ and ‘Up 2Up account’

- Savings accounts ‘Up Saver account’ and ‘2Up Saver account’

In addition to individual bank accounts, Up introduced the ‘2Up’ which is similar to a joint account for you and ‘Player 2’ ! Rather than one single joint account, You each maintain an individual account with total control over your own account, but you have connected abilities such as splitting shared bills.

Up does not offer any credit cards or personal loans.

Transaction account: ‘Up Everyday Account’

Up provides a standard no-fee transaction account linked to a MasterCard debit card (fees for overseas transactions are processed via MasterCard in a similar conversion rate to Visa).

They provide an awesome level of spending tracking – They provide Automatic Merchant ID (Vendor identification), spending categorisation as well as location and time stamps – you will never be left clueless reading through your bank transaction history ever again!

Like a handful of modern banks, Up provides a round up feature on their everyday account – you can choose automatic round ups on purchases and have the change transferred to your linked Saver Account.

The Up Everyday account also has all of the standard features you would expect from a bank account – Automated transfers, as well as modern instant transfer payment options including;

- PayID instant transfer

- Osko instant payments

- BPAY

- Apple Pay

- Google Pay,

- Samsung Pay

- Fitbit Pay

- Garmin Pay

- Transferwise overseas payment integration

Realistically, this means you don’t even need to take your wallet with you, and can link your phone or smart watch!

Savings account: ‘Up Saver Account’

If you make five eligible card transactions per month using your linked everyday Account, you will qualify for ‘bonus interest’ – the highest interest rate on your Saver Account up to a maximum balance of only $50,000. This has historically been one of the highest available online savings accounts rates across all of the banks – which fluctuates according to the RBA interest rate.

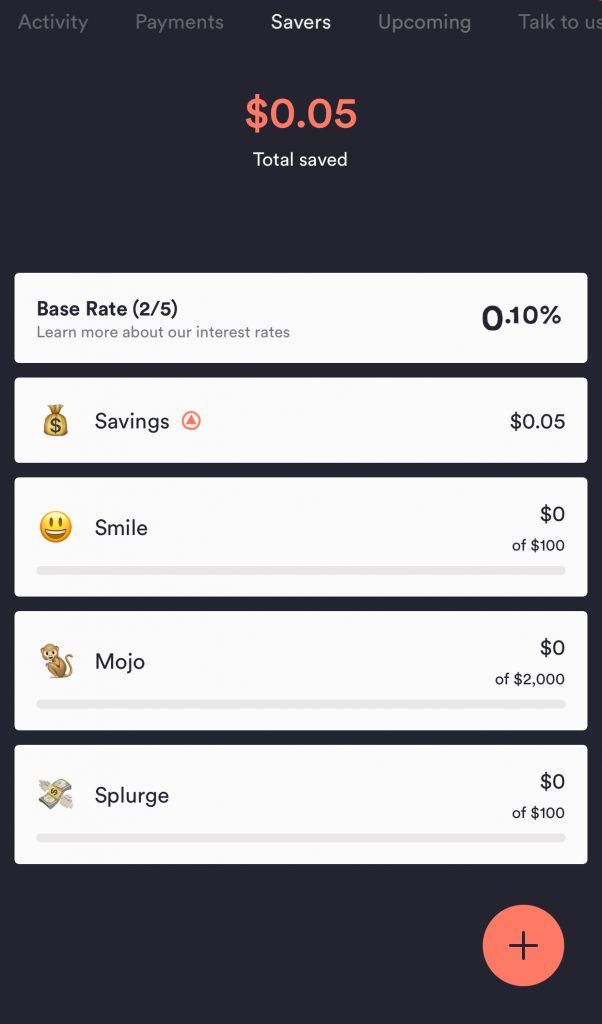

Within Up, you can have multiple savings accounts – this makes it very easy to set up your ‘Barefoot buckets’, ‘Ramsay splits’ or your sinking funds (such as Holiday savings, Emergency fund, Christmas savings etc). All of these individual savings accounts qualify for the same high interest rate by making the five transactions on your Everyday Account card. You can customise each of these with specific goals, as well as automatic transfers and the round up functionality from purchases to help you save quicker.

Up Savings accounts make it easy to set a savings goal and work towards it, with a ‘gamification’ of saving, rewarding you for making deposits and reaching milestones on the way.

Up Home

Up now offers home loans and there is a Home loan calculator on the website too.

“Up Home loans are owner-occupier loans for Upsiders buying in a capital city or major regional centre. You can get one for a home you already own, or a home you’ve fallen in love with.”

up.com.au/home-loans

Want to make more money for your Up account?

Before we go any further, if you are interested in knowing how to make more money then check out my detailed article on How to Make Money Online.

Up mobile app review

As mentioned, almost everything through Up is done through the Up mobile application, which is pretty game changing. Up is entirely cloud based with their whole corporate infrastructure managed by Google, and the app is the only user interface – there are no branches, no website log in and even no phone banking.

You can do everything in the app that you could possibly think you might need to. Setting up Apple Pay, Google Pay etc on supported phones is quick and easy, and with the tap of a button (or facial recognition) you can use your phone just like a debit card.

Clearly a lot of thought has gone into this applications development – The app presents itself cleanly and very well, providing an awesome graphical User Interface (UI). I found it intuitive and easy to learn how to use, setting up my linked accounts and texting with their support team via their in app live chat function.

Overall, it was a great User Experience (UX) and clearly the team behind Up know a thing or two about mobile banking application development.

This is clearly an app developed with tech and user experience in mind foremost, rather than a traditional bank just wanting a mobile app with user experience as an afterthought. And you would hope so too, since there aren’t any alternative options to use Up.

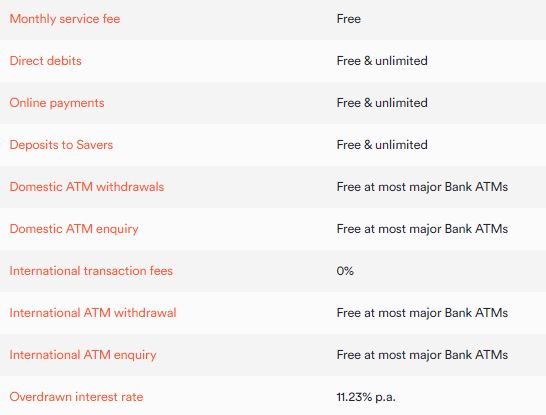

UP account fee and charges

UP don’t charge an account fee or transaction fees (except overdrawn accounts), and you won’t pay an ATM fee overseas or at most Major Aussie ATM’s either. They do not charge foreign transaction fees – these purchases are also facilitated through MasterCard, and use MasterCard’s competitive foreign exchange rate with no additional FX spread charged.

“Protip: When using Up overseas, we recommend choosing to pay in the foreign currency as opposed to AUD when given the choice. This lets you take advantage of the great rate you get by being an Upsider, instead of the rate the merchant terminal chooses to give you.”

Up

Up also doesn’t charge ATM fees overseas (however they will not reimburse you if the ATM operator charges you a fee, like ING bank will reimburse you)

For the full list of terms and conditions, you need to read their Product Disclosure statement here.

Up customer support

With no face-to-face option (because they don’t have branches,) customer support with Up is a little different. Whilst not having physical branches is nothing new in the modern banking community, Up only offer limited phone support.

This means the best way to contact customer support is email or via their inbuilt live chat function in the Up app. Having said that, the app works really well with an average support time of under 5 minutes because they have employees available 24/7.

There is a support number though, which is on the back of your card that you get when you sign up.

Up also have brought in Bank@Post, so if you have physical currency or cheques, these can be deposited at Australia Post.

What I like about Up

I love how innovative, efficient and sustainable Up’s business model is. By transitioning to a digital only service, they cut out significant cost overheads (as well as annoying in branch time wasting) and ultimately pass the savings onto you in the form of higher interest rates, better product features and great customer support. It is like ING Bank on steroids.

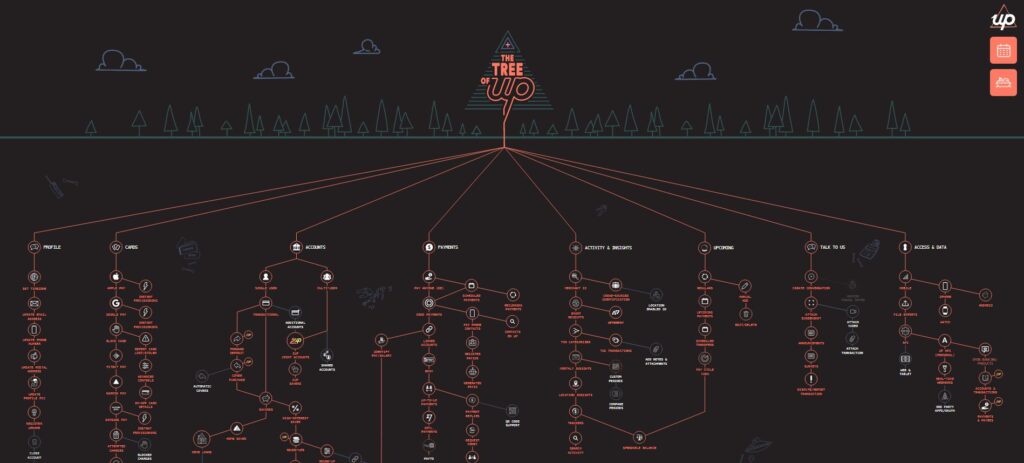

I personally love their Fee free structure, round up feature, multiple savings accounts that all get the high interest rate, as well as PayID and Osko functionality – although these should probably all be considered standard in modern online banking systems. They also publish ‘The Tree of Up’ which is Up banks feature development tree ‘Dev Tree’ showing users what new features and functionality will come soon.

I have used their expense tracking and categorisation system for a few years, and whilst its pretty good it doesn’t always work perfectly, allocating expenses sometimes hilariously wrong sometimes. Thankfully, you can adjust this. It does somewhat eliminate the need for third party expense tracking software like PocketSmith or WeMoney. This ultimately will simplify your personal finances, and is a good thing. However, it does not fully replace their functionality when it comes to tracking your net wealth, credit score or paying down debt.

Lastly, they listened to customers and finally introduced a bank@Post system. You can now use your Up bank card and pin to deposit cash and cheques through Australia Post. This is super important for someone on the path to Financial Independence since we are often participating in the second hand economy (and we might get paid in cheques for certan side hustles).

What I don’t like about Up

The biggest thing I don’t like about Up bank is their limited phone support. I find ringing up and negotiating to be one of my most successful strategies for getting better deals on things – including when I am dealing with my bank.

Having said that, it probably doesn’t matter too much, and their in app support has been good so far. When they expand, however, I would like to see phone service added.

Finally, a point of contention is that they aren’t strictly ‘ATM fee free’. They claim that you won’t pay ATM fees on all ‘Major bank owned ATMs’ but this leaves to question what is a major bank? Is it the big four only? Or does it include subsidiaries?

I much prefer ING bank’s blanket statement of ‘No ATM fees, ever!’ and hope that Up will follow suit soon. They also don’t explicitly state there are no ATM fees overseas, and say that overseas operators ‘might’ charge you – what do you think? Of course they will bloody charge you!

Does CaptainFI use Up?

Yes. I have been an Up customer for the past few years, and I have been very satisfied with their transaction and savings accounts.

As most of you will know, I have currently been WeMoney to track expenses, but something that Up does really well is expense tracking and categorising – you may not even need to use a third party expense tracking app if you are using Up and are satisfied with their trackers.

I do still keep a separate bank account with ING bank which I like to keep my emergency fund ‘Mojo Account’ in.

Signing up to Up Bank

It took me 5 minutes to download the app, fill out the details required (Drivers licence information and Tax file number) and verify my account. They said it might take 10 business days, but it only took 4 days before my snazzy, fluorescent orange card turned up in the mail.

Keen to test out my snazzy little card, I carried it in my hot little hands down to the shops to make a transaction. I was still a bit behind the times and didn’t use Apple Pay, so I queued up with a handful of blueberries and brandished my card – awkwardly waiting the few moments that the card reader took to process its first transaction.

Up then neatly categorized this purchase as ‘Home’ since I bought it from a grocery store, and it was automatically tagged as groceries. Which is close enough.

Up also provided a timestamp, location and logo of the grocery store, alongside the purchase amount, and how much of my change had been ’rounded up’ into my savings account (5 x $1.99 punnets cost $9.95 and the remaining 5 cents was transferred to my linked savings account). This is way more information than ING tells me and is in a very useful format (ING, like all conventional banks, spits out something that looks like its come out of the matrix). It is super handy for understanding your spending habits for your budget, and I thought it was a unique banking experience when compared to traditional banking.

I am also currently exploring their different account structures and pay split features, which can be used to automate my income splits (i.e. the Barefoot investor buckets).

Frequently Asked Questions

Answers to Frequently Asked Questions about Up Bank:

Who is Up Bank owned by?

Up was founded by Dominic Pym and Grant Thomas from Ferocia. They operate as a subsidiary of Bendigo and Adelaide Bank

Is Up bank a real bank?

Yes, Up is backed by Bendigo and Adelaide Bank limited. Their ABN is 11 068 049 178, and their AFSL and Australian Credit Licence is 237879 which can be checked out on the ABR and on ASICs website.

Are Digital banks safe?

Neo banks use encryption software and two factor authentication for their bank accounts. It has been recognised that digital and mobile banking and payment can actually be safer than carrying around debit cards. This does not make you completely safe from fraud and scams however, so you still need to follow basic security protocols.

What is an Up account?

An Up account is an account with Up – either an everyday account or a bonus saving account, which are both managed via the Up mobile app.

Is Up bank good?

Yes, Up bank is great. Fast, easy to use and secure. They offer low fees and a competitive interest rate, and the mobile app has many great features including spending trackers.

Does Up offer credit cards?

No, Up does not offer a credit card.

Does Up offer a home loan?

Yes, Up now offers Up Home. You can apply through the Home Zone in app and they even have a Home loan calculator on the website.

What is Up bank?

Up is an innovative Australian digital bank that offers entirely digital, cloud based personal banking through the Up mobile application. Because of this, and their strong focus on technology and rapid development, they are often categorized as a ‘neobank”.

Is Up bank safe?

up Bank features next-generation security features and encryption, and the safety of accounts backed by Bendigo and Adelaide Bank.

How does Up bank work?

Up Banking works through the Up mobile app, and users get an everyday transaction account and a bonus saving account. Up manages the money like a conventional bank – aggregating balances and lending it out in accordance with fractional lending practices to generate credit in the economy. Up bank can also sell your aggregated spending data to investment firms.

How much can you withdraw from Up?

Up has a default daily limit of $1,000 but you can contact customer support through the app to have your family limit increased.

How many savings accounts can you have with Up?

Savings account options within Up are unlimited.

Do Up charge an account fee?

No, Up does not charge an account fee

Is Up Bank covered by the government guarantee?

Yes, as an Authorised Deposit-taking Institution (ADI) with a banking licence that under the FCS is authorised by the Australian Prudential Regulation Authority (APRA), your deposits in Up are protected by government guarantee up to $250,000 for each account holder.

Up Bank promo Sign up code

If you’re keen to give it a go yourself, you can head over to their website and use the promo code ‘CFI’ – or alternatively you can use the Hook a Mate Up code URL below. This should give you $10 – $5 immediately, and another $5 after you make some transactions (like buying 5 punnets of blueberries which is what I did!)

Up Bank Captain FI promo code: CFI

Conclusion

Up is an innovative Australian neo bank backed by Adelaide and Bendigo bank that offers entirely digital, cloud based personal banking through the Up mobile application. With over 800,000 customers, including me, they have a proven track record and a very easy to use platform. The Up mobile app is great and it is very easy to link to Apple Pay, Google Pay, Samsung pay, etc. It tracks your bank accounts and spending history, making it easier to understand your budget and work towards a savings goal.

Up does not support fossil fuel companies like a traditional banking system such as Commonwealth Bank, and Up provides competitive interest rates in line with the RBA official cash interest rates.

This review covered some of the functionality of Up, why I like it and a few of the things I don’t like, however overall I am pretty impressed with the Up banking experience. I think it’s a great option for anyone on the path to Financial Independence looking for an online personal bank. In the interests of full disclosure I still hedge my bets with a secondary more ‘conventional’ bank account (ING bank), but I have been really happy with my service through Up so far.

….plus their orange card is even more obnoxiously fluorescent orange than INGs card, so that way when I flash it people REALLY know that I have read the Barefoot Investor.

Want to know where Captain FI Banks?

Check out my Personal Resources Page and my Net Worth Updates.

Further reading – other Bank reviews

Check out my list of bank reviews here to see how the competition stacks up, and to find the right bank for your journey to Financial Independence

- Commonwealth bank

- NAB Bank

- ANZ Bank review

- Westpac Bank review

- ME Bank review

- ING Bank review

- UBank review

- HSBC Bank review

- Up Bank review

- 86400 Bank review

- Finspo review

- Spriggy review

Financial Disclaimer

Financial Disclaimer: CaptainFI is NOT a financial advisor and does not hold an AFSL. This is not financial Advice!

I am not a financial adviser and I do not hold an Australian Financial Services Licence (AFSL). In this article, I am giving you factual, balanced information without judgment or bias, to the best of my ability. I am not giving you any general or personal financial advice about what you should do with your investments. Just because I do something with my money (or use a particular service or platform) doesn’t mean it is automatically appropriate for your personal circumstances. I do not recommend nor endorse any financial or investment product, and my usage or opinion of any product should not be interpreted as an endorsement, advertisement, or intent to influence.

I can only provide factual information based on my journey to Financial Independence, and that is provided for general informational and entertainment purposes only. I make no guarantee about the performance of any product, and although I strive to keep the information accurate and updated as it changes, I make no guarantee about the correctness of reviews or information posted.

Remember – you always need to do your own independent research and due diligence before making any transaction. This includes reading and analysing Product Disclosure Statements, Terms and Conditions, Service Arrangement and Fee Structures. It is always smart to compare products and discuss them, but ultimately you need to take responsibility for your use of any particular product and make sure it suits your personal circumstances. If you need help and would like to obtain personal financial advice about which investment options or platforms may be right for you, please talk to a licensed financial adviser or AFSL holder – you can take the first steps to find a financial advisor by reading this interview, or by visiting the ASIC financial adviser register and searching in your area. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Hey Captain FI

Top blog and this is a great and, typically thorough, review of financial instrument. On the back of your research, I am recommending an UP card for my son for an impending overseas adventure. Your site is fantastic and a must read. Cheers, Slack Investor

I downloaded the uBank app a few days ago and have been using it regularly. I have to say that I’m really impressed

Great review! As a fellow digital banking user, I completely agree that Up bank has been a game-changer for me. The app is incredibly easy to use and the security measures are definitely impressive. I love that I can easily track my spending and set budgets for myself. Thanks for sharing your experience!

I’m getting rid of my Big 4 bank accounts; they are more concerned these days about shareholders than they are about their customers. Shut my ANZ and CommBank and now i use Wise and Up. I will open a Bendigo bank account as backup, but mainly so I have a facility to deposit cash if the need arises.

Up is great, with low to no fees and great FX rates and the speed of transfer is terrific.

I also use Wise for traveling and in Australia and can transfer between Wise and Up in about 5 to 10 seconds,

Bendigo bank for cash deposit or withdrawal, Up for normal spending and transfers and income in, and Wise for normal spending travel with still Up for travel also.

The only con for Up is I don’t think you can ring them, but their chat has been excellent.

Up is the way to go, it is very intuitive, love the 2up too. It beats Ubank and ING anyday for. Categorisation of payments is easy and can change it easily if it’s not correct, use it to track expenses love the spending insights can easily swipe to yearly, monthly, weekly, financial year. Have not had problems with it overseas. Ubank declines some transactions end up having to use Up instead. ING conditions for receiving interest seems to be outdated I hardly use it now.