VTS Review –Review of Vanguard Total US Market (ASX:VTS) ETF from a long term index fund investor on the path to Financial Independence.

Vanguard offers a Total US market exchange traded fund on the ASX under the ticker code ‘ASX:VTS’, which a cross-listing of the Total US market ETF from the New York Stock Exchange ‘NYSE: VTI’. This has an incredibly low Management Expense Ratio of 0.03%. VTS tracks the CRSP US Total Market Index, which is well diversified and holds approximately 4000 underlying companies which although weighted to larger ‘bluechip’ shares, extends to both mid and small-cap companies, with a total underlying fund size of $1.7 Trillion USD.

Vanguard say that the total US market shares index ETF is suited to;

Buy and hold investors seeking long-term capital growth, some income, international diversification, and with a higher tolerance for the risks associated with share market volatility.

Vanguard, VTS fund

Read on for more information about the Vanguard VTS Exchanged Traded Fund.

The Good

- CRSP Index is an efficient system suitable for US exposure

- Diversification to largest global economy in world

- Approximately 4000 underlying holdings with minimal effort

- Vanguard automatically rebalances as per the index

- Ultra low management fee – 0.03% MER

- Capital Gains is primary method of growth – tax efficient

The Bad

- US domiciled – W8BEN form required every 3 years

- No Dividend reinvestment plan options

- Unhedged – currency fluctuations can impact returns in AUD.

- Low dividends so need to sell for income (although this is usually more tax effective)

Verdict: VTS is a US domiciled Exchange Traded Fund provided by Vanguard which provides Australian investors with US share market exposure for an ultra low MER of 0.03% as a cross-listing of the US-listed ETF ‘NYSE:VTI. It contains approximately 4000 underlying holdings. It can be a valuable asset to reach FIRE

CaptainFI is not a Financial Advisor and the information below is not financial advice. This website is reader-supported, which means we may be paid when you visit links to partner or featured sites, or by advertising on the site. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer. When it comes to investments, past performance is no indicator of future performance as returns can be volatile, reflecting rises and falls of the underlying investments. You should seek independent financial advice as to the suitability of any products to your personal circumstance and investment needs.

Vanguard manages VTS according to their three main priorities

Competitive long-term performance: Vanguard’s investment approach provides investors with an efficient way to capture long-term market performance.

Diversification: The Fund invests in a diversified portfolio of securities, which means the Fund is less exposed to the performance fluctuations of individual securities.

Low cost investing: The Fund has low ongoing fees as we strive to minimise the costs of managing and operating the Fund.

Vanguard, VTS product statement

Vanguard VTS ETF details

The VTS ETF could be thought of as a ‘growth ETF’, which aligns to the boglehead style of investing for growing capital value (share price).

The ETF provides exposure to some of the world’s largest companies listed in the United States. It offers low-cost access to a broadly diversified range of securities that allows investors to participate in their long-term growth potential. The ETF is exposed to the fluctuating values of the US currency, as there will not be any hedging to the Australian dollar

Vanguard VTS ETF overview statement

Dividend Yield of VTS

VTS provides quarterly income distributions. The dividend or equity yield fluctuates, but tallies at around 1 to 2% annually, and is currently at 1.86%. It’s nice to see the dividends hit your account, but you can see from this VTS review that it’s not really going to be enough to live off unless you have a significant holding. However, the focus of VTS is capital growth (not dividend) as US companies typically retain earnings to try and grow their company. This means in order to live off VTS post FI, you would need to sell off parcels of shares when needed – which can be incredibly tax effective for long term holders.

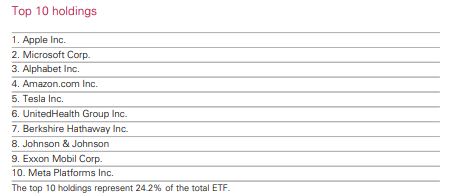

Holdings of Vanguard VTS

VTS (ASX:VTS) currently manages (AUD) $3 Billion spread across 4,059 holdings, and its underlying US fund size is approximately (USD) $1.7 Trillion. Its top holding is Apple, followed by Microsoft, Google (alphabet), Amazon and Tesla – as per the breakdown below. It offers exposure to some of the world’s largest publicly traded companies in the United States.

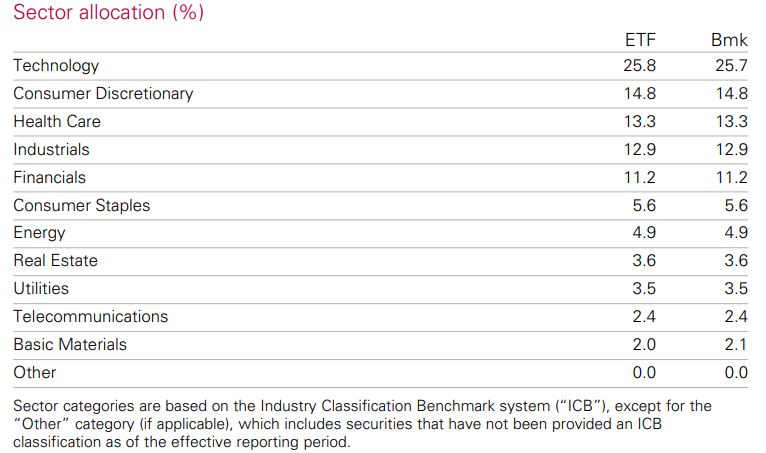

Sector allocation of Vanguard VTS

The VTS index is market cap-weighted, meaning it contains a higher percentage the larger companies. Due to the success and high valuations of many tech companies like Apple, Google, Microsoft and Amazon, the sector allocation has almost a quarter of Technology stocks

Fees of Vanguard VTS

VTS offers what I have found to be the lowest MER of any stock market ETF. This is an ultra low MER of .03% or $3 per $10,000 invested per year. Currently the BlackRock iShares IVV Total US market fund is its closest competitor, charging a MER of .04% or approximately 30% more.

VTS cross-listing onto the Australian Securities Exchange

VTS is a cross-listed version of NYSE:VTI onto the Australian Securities Exchange, meaning it is not domiciled in Australia. Accordingly, you will need to fill out a W-8BEN-E tax form every three years. This is a relatively simple task that takes under 10 minutes and can be accomplished through the VTS share registry in Australia, Computershare. Computershare offers a detailed walk-through, and individualized forms for personal investors, commercial investors and those investing through trusts such as family or discretionary trusts.

Hedging of VTS

The ETF is not hedged (it is not treated like a hedge fund) meaning that it is exposed to the fluctuating values of US vs AUS dollar (but this isn’t important, and over time the costs associated with hedging funds tend to erode any benefit that the hedging provides).

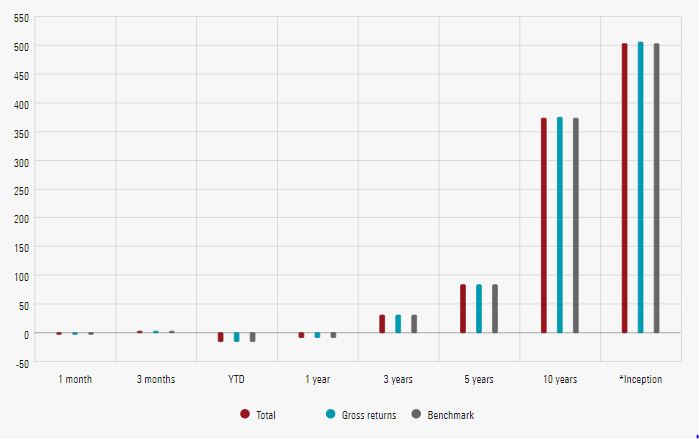

Performance of Vanguard VTS ETF

Remember that pior performance is no indicator of future performance, but the following information can provide some insight into how VTS has performed historically.

VTS has performed almost spot on in line with the index (CRSP US Total Market Index) since its inception. Check out Vanguard Investments.com for the most up to date information on this ETF.

You can see that whilst there was negative returns up to the 1 year mark, the 3 year return onward has been positive, with an annualized 10+ year return of 13.3% aligning to the long term expectations of the share market to produce about a 10% total return.

Sharesight is a very powerful platform with a great functionality in their share checker to see the performance of a hypothetical $10,000 investment in any listed share or ETF – which is a very valuable tool for market analytics, with a very straightforward interface. Below, it shows the performance of VTS along with dividend events. You can see, going back as far as they can, the total return was approximately 13.3%. I was a bit confused by the capital gain of 12.27% and dividend of 3.57% not adding up to the total return, but this must assume dividends are not reinvested (which in reality you would to get a better total return).

VTS review: Choosing VTS as a Capital growth ETF vs Dividend-yielding ETFs

VTS, or American shares in general, focus on providing higher capital growth rather than dividends to investors. For example, my shares of VTS have provided me 13.41% of capital growth, with only 1.73% in dividends for a total return of 15.11%, compared to my shares of A200 which have provided me 9.94% capital growth and 4.74% dividends (plus franking credits which boosts it to 5.87%) for a total return of 14.06% (plus franking credits which boosts it to 15.82%) according to the latest Sharesight data. Of course, these numbers are irrelevant in the short term, but I am just providing them to illustrate the breakdown of capital growth vs dividends.

Its worth doing the maths yourself or seeing an accountant or financial advisor for personalised financial advice, but the decision to invest for capital growth vs dividend yield depends on a lot of factors – mostly being your taxable income now, and projected retirement influence. This might influence your choice for your of portfolio splits between say, US, Australian and Global shares. For example, if you are earning a very high income now and plan to retire on a lower income, dividends or an income yielding share are not going to be as tax effective as growth shares (where you can choose when to cop the capital gains event when you are on a much lower tax bracket).

Vanguard suggest VTS is suitable for ‘buy and hold investors seeking long-term capital growth, some income, international diversification, and with a higher tolerance for the risks associated with share market volatility’.

Both VTS and IVV track the US index, but in slightly different ways (they are not both total market shares index funds).

VTS is slightly cheaper than IVV, now sitting at a MER of .03% vs the IVV’s MER of .04%. However, IVV is an Australian-domiciled fund, whereas VTS is just cross-listed version of VTI which is made available on the Australian Stock Exchange. This means for VTS you will need to spend approx 10 minutes every 3 years filling out a W-8BEN-E tax form to hand to the American tax system to make sure you don’t get taxed twice.

Lets put this into perspective. With a $100K holding, IVV is going to cost you $120 in management fees for every three years, whereas VTS is going to cost you $90. I am most certainly happy to save $30 for every $100K invested by selecting VTS, and spending 5 minutes approving the Computershare pre-filled out the W-8BEN-E form. But we are talking about very small amounts of money spent on management fees here.

IVV does have the benefit of simpler estate planning due to being Australian-domiciled (i.e. it is more straightforward to know what will happen to your shares if you die!) and it also offers a dividend reinvestment plan whereas VTS can not. For these reasons, a number of Financial advisors suggest going with IVV.

With the dividends on VTS, even if you submit a W8BEN form, you will still be required to pay 15% tax to the US IRS which will be withheld from your dividend. Because of the Foreign Tax agreement between the US and Australia, you get a ‘tax credit’ (for want of a better word) for this 15% tax you have already paid which is fair; however, if your taxable rate is actually below a total figure of 15%, you won’t ever get a ‘tax refund’ for this.

The funds whilst are similar are not identical, and are managed ever so slightly differently. Check out the video below for more information.

Summary of Vanguard VTS

VTS is a US domiciled Exchange Traded Fund provided by Vanguard which provides Australian investors with US share market exposure for an ultra low MER of 0.03% as a cross listing of the US listed ETF ‘NYSE: VTI’. It contains approximately 4000 underlying holdings, which although weighted to larger ‘bluechip’ shares, extends to both mid- and small-cap companies.

Holding US investments inside VTS avoids the need for market research, active deals and significant brokerage costs, and the investor/customer ownership structure of Vanguard has lower fees theoretically leading to higher profit margins for investors. Implementing VTS investments can be easily achieved with any Australian share trading platform.

Additional updates

27th April 2020: I have since sold my holdings of IVV, and now purely invest in the Vanguard VTS ETF for exposure to US stocks

20 May 2022: I have reached financial independence and stopped full time work. I have increased my portfolio asset allocation from one third VTS to one half VTS,.

Frequently Asked Questions about the Vanguard VTS Exchange Traded Fund

Answers to Frequently Asked Questions about the VTS ETF

What is VTS ETF?

The VTS ETF is Vanguard’s total US market exchange-traded fund, which contains a market cap-weighted index fund of over 3600 listed US companies.

Can you buy VTS on the ASX?

Yes, you can buy Vanguard US total Market Exchange Traded Fund on the ASX under ticker code ‘VTS”

Is VTS the same as VTI?

Yes, ASX: VTS is a cross-listed version of NYSE:VTI, which allows investors access to buy VTI without needing access to a US shares trading platform.

Does VTS have a dividend?

Yes, VTS pays a quarterly dividend, which typically results in an annual total distribution of around 1 to 2%.

Who owns Vanguard Investments?

Vanguard is owned by its customers, a very powerful platform to keep fees low.

Does VTS have a dividend Reinvestment Plan (DRP)?

No, Because VTS is cross-listed, investors can only take VTS dividends as cash distributions.

Is VTS hedged?

No, VTS is not hedged. This means it is is exposed to currency fluctuations.

Is Vanguard VTS domiciled in Australia?

No, VTS is not domiciled in Australia. It is a cross-listed version of VTI which is listed on the ASX so that Australian investors can get easier access to buy or sell it. This means you will need to completed the W8BEN form every 3 years

Financial Disclaimer

Financial Disclaimer: CaptainFI is NOT a financial advisor and does not hold an AFSL. This is not financial Advice!

I am not a financial adviser and I do not hold an Australian Financial Services Licence (AFSL). In this article, I am giving you factual, balanced information without judgment or bias, to the best of my ability. I do not know your personal circumstance or financial situation. I am not giving you any general or personal financial advice about what you should do with your investments. Just because I do something with my money (or use a particular service or platform) doesn’t mean it is automatically appropriate for your personal circumstances. I do not recommend nor endorse any financial or investment product, and my usage or opinion of any product should not be interpreted as an endorsement, advertisement, or intent to influence.

I can only provide factual information based on my journey to Financial Independence, and that is provided for general informational and entertainment purposes only. I make no guarantee about the performance of any product, and although I strive to keep the information accurate and updated as it changes, I make no guarantee about the correctness of reviews or information posted. When it comes to investments, past performance is no indicator of future performance as returns can be volatile, reflecting rises and falls of the underlying investments.

Remember – you always need to do your own independent research and due diligence before making any transaction. This includes reading and analysing Product Disclosure Statements, Terms and Conditions, Service Arrangement and Fee Structures. It is always smart to compare products and discuss them, but ultimately you need to take responsibility for your use of any particular product and make sure it suits your personal circumstances. If you need help and would like to obtain personal financial advice about which investment options or platforms may be right for you, please talk to a licensed financial adviser or AFSL holder – you can take the first steps to find a financial advisor by reading this interview, or by visiting the ASIC financial adviser register and searching in your area.

For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Hi Captain

My SMSF has 4.2 mil to invest. This was redeemed to me when Vanguard closed their managed payout fund without explanation.

I am finding it difficult to deal with with Vanguard Australia who do not respond to emails or attempts at contact.

I am interested in US shares.Do you have any suggestions?

Tony – that is epic mate! Sounds like you are set for life. Annoying when managed funds change like that isn’t it? I did not have a great experience with managed funds earlier in my investing career. There are a heap of great ways to invest your money, but it sounds like you might do best to visit a financial advisor since 4.2 mil in a SMSF is a pretty complex topic. I would hit up the ASIC Moneysmart website review page for financial advisors, and see if you can find a good, independent, fee for service advisor. I would also suggest having a read through the barefoot investor who points out some interesting facts regarding SMSF versus traditional super funds which are now offering index based products. I personally have used index based superannuation products and many of my family do – it seems to be the ‘new normal’ and is incredibly simple and easy. As for my investments, you can read where I have personally chosen to invest (split between Australia, US and other international markets) and there are of course ways to get exposure to all of these markets through both a conventional brokerage account and through a SMSF or standard super account. Don’t overcomplicate it though Tony. Youve done great to get where you are – Keep it simple and reap the benefits!

Hi Cap,

First time investor here, experimenting with $10k to start. I have 2 options. Option 1, put 100% in VDHG, option 2, equal-weighted in A200/VTS/VEU (I wanted to try option 2).

A few questions:

Is VTS and VEU cancelled on the Vanguard Personal Investor website? They were buried in a page saying “The following product can’t be bought on Vanguard Personal Investor”. I saw VTS/VEU in your Aug 2021 update, so was surprised when i couldn’t see it front and center on Vanguard’s own menu

Second, am I right in understanding I cannot buy VTS and VEU on Vanguard’s own platform, but still can buy it elsewhere (e.g. through a broker like Pearler)? So still open to trade?

Third, is there any point using the source fund’s own platform at all or just go to a broker for everything (e.g. Pearler, Superhero etc)? I noticed on your Resources page you only mentioned brokers but didn’t mention Vanguard Personal Investor etc…

Finally, I’m a NZ-citizen (living and working in Australia). I believe we are tax exempt here from capital gains? But with this US-domiciled business, and my NZ status, any resource recommendations where I can learn about tax treatment for buying funds like VTS? Quite nervous about all the tax stuff.

Thanks very much if you are able to provide any tips/pointers. apologies if I have missed it on other threads! So much content to take in, but I’m incredibly excited and inspired by your blog!