Vision Super is an award-winning, Australian-based public-sector super fund, open for anyone to join. When searching low fee super fund with good returns to help save for retirement, Vision Super is worth a look. Read the following Vision Super review, for plenty to think about.

The Good

- Australian-based super fund

- Initially a fund for local government employees, now open to the public

- Relatively good returns over the past 5 years

- Relatively low fees

- Offers a range of investment options

- Offers insurance products through the fund

- Offers sustainability options

- For 3 years in a row, Vision Super’s Vision Personal option has won Money Magazines Best of the Best for Best Value Superannuation Fund

The Bad

- Relatively high insurance premiums compared to other funds

- Vision Super is 22 out of 34 funds on Review My Super1, suggesting room for improvement

- Entering into a period of change due to a merger with Active Super, but it may be a good thing with eventual cost savings

- Becoming bigger may not necessarily be better, with smaller funds sometimes providing a better customer service

Verdict: Australian-based, low fees, good returns and award-winning, but higher insurance premiums – definitely a strong option for Super

Introduction

Vision Super is an Australian public-sector fund, on offer to the general public2. Vision Super started life as the Local Authorities Superannuation Fund (LASF) in 1947. Currently, Vision Super has about 85 000 members with around $16 billion in assets under management.

Compared to other super funds, Vision Super has relatively low fees. While past performance is no guarantee of future performance, Vision Super has a good track record of delivering for its members. Over the past 5 years, Vision Super has had consistently good returns.

Vision Super offers a range of premixed investment options, such as Growth, Balanced Growth and Conservative, amongst others. Vision Super also offers insurance products such as Income Protection, Death and Total and Permanent Disability (TPD) cover.

For its Vision Personal product, Vision Super has won Money Magazine’s Best of the Best, Best Value Superannuation product for the last 3 years.

To read more about Superannuation in Australia, you can read my article HERE.

Is Vision Super an industry super fund?

Vision Super3 is a public-sector fund, open to members of the public to join. It was started in 1947 as the Local Authorities Superannuation Fund4 catering to employees of local government and utilities such as water. As Vision Super, it is a not-for-profit, member-owned fund with profits benefiting members, not shareholders.

“No matter what industry you work in, whether you’re working for someone else or you own your own business, you can open a super account with Vision Super.”

visionsuper.com.au/about3

Is Vision Super an Australian company?

Vision Super is a super fund based in Australia. Vision Super is based in Melbourne, Victoria.

What was Vision Super previously called?

Vision Super was previously called Local Authorities Superannuation Fund (LASF). Vision Super Pty Ltd started life as LASF’s trustee5, however, after rebranding, the fund is now known as Vision Super.

Who owns Vision Super?

Vision Super is owned by its members, with profits benefiting the members, not shareholders.

It is run by a board of Trustee Directors6 who are responsible for making sure the financial interests of Vision Super members come first.

What are the super options through Vision Super?

Vision Super has a number of different options available for investing your super7. Premixed options comprise different asset classes such as property, cash, bonds and shares in varying allocations, to outperform the CPI per year by differing percentages, after fees:

· Growth – 3.5%

· Balanced growth – 3.0%

· Balanced low cost – 2.5%

· Balanced – 2.0%

· Conservative – 1.5%

What are Vision Super’s fees?

The following Vision Super fees and charges8 are based on the Balanced Growth investment option, which is Vision Super’s MySuper offering. The fees are for a fund balance of $50 000.

· Admin costs and fees – $1.50/wk ($78/yr), plus 0.14% of the account balance

· Investment costs and fees – 0.44%, based on a balance of $50 000 this is $220 investment costs and fees

· Transaction costs – 0.05%, based on a balanced of $50 000 this is $25 for transaction costs

This means, on a balance of $50 000 you will be charged costs and fees of $393 minimum. Which is pretty good compared to other low costs funds such as Australian Super9 ($382).

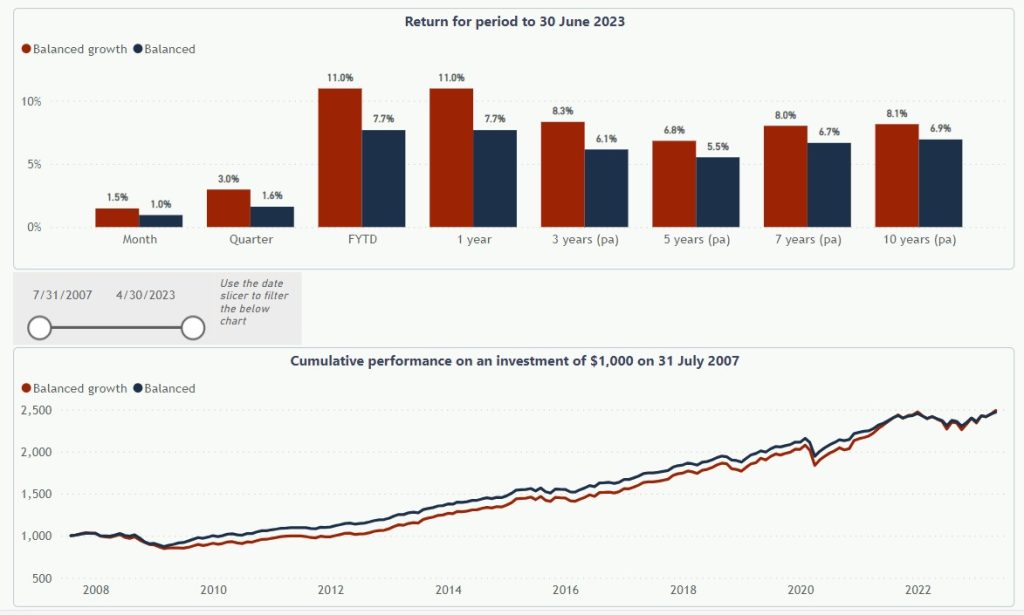

Performance of Vision Super

The following looks at Visions Super’s performance10 across some of their investment options over the past years to 30 June 2023.

· Balanced Growth returns – 1yr 10.96%, 3yrs 8.32%, 5yrs 6.82%

· Growth returns – 1yr 13.29%, 3yrs 10.31%, 5yrs 8.02%

· Conservative returns – 1yr 5.01%, 3yrs 3.96%, 5yrs 3.96%

While past performance is no guarantee of future performance, overall, Vision Super has provided strong returns across investment options.

Vision Super insurance policies

Vision Super provides insurance products through their super fund for Income Protection insurance, Death cover and TPD cover.

The following example is based on a 30 year old male, in an office-based management job, bringing in a gross income of $100 000 a year, with TPD and Death cover11 of $500,000 each.

- Death and TPD fixed cover combined – $520 per year, or about $45 per month

- Income protection – pays 75% of your gross income for a 2 year payout with different waiting periods: 30 day waiting period – around $290 per year ($22 per month): 60 day waiting period – around $135 per year ($10 per month)

That means about $810 per year will come out of your super in premiums if you have Income Protection insurance12 for the 2 years of benefits after a 30 day wait period as well as Death and TPD combined. This is higher than some other funds.

You can access the Vision Super calculators HERE: Calculators – Vision Super13

How does Vision Super invest my super?

With Vision Super investment options, such as Balanced Growth or Conservative etc, Vision Super invests your super in different asset classes, in varying allocations depending on the investment option and risk profile. This includes:

· International equities

· Australian equities

· Infrastructure

· Property – listed and unlisted

· Diversified bonds

· Cash

· Alternative debt

· Opportunistic growth

You can find further info on their website here: Our investment options – Vision Super14

You can listen to my podcasts with Vince Scully, all about Superannuation HERE for Part One, and HERE for Part Two.

Has Vision Super won any awards3?

Vision Super has won Money Magazine’s award15 for the Best of the Best for Best Value Superannuation product for the past 3 years in a row, for their Vision Personal low-cost investment option. You can find the Vision Personal PDS HERE16.

Advantages of Vision Super

- Australian-based super fund

- Initially a fund for local government employees, now open to the public

- Relatively good returns over the past 5 years

- Relatively low fees

- Offers a range of investment options

- Offers insurance products through the fund

- Offers sustainability options

- For 3 years in a row, Vision Super’s Vision Personal option has won Money Magazines Best of the Best for Best Value Superannuation Fund

“At Vision Super we never forget that your super is your money. It should be invested to help you build wealth and retire comfortably. That’s what we’ve being doing for all our members since we first opened our doors in 1947.”

visionsuper.com.au/about3

Disadvantages of Vision Super

- Relatively high insurance premiums compared to other funds

- Vision Super is 22 out of 34 funds on Review My Super1, suggesting room for improvement

- Entering into a period of change due to a merger with Active Super17, but it may be a good thing with eventual cost savings

- Becoming bigger may not necessarily be better, with smaller funds sometimes providing a better customer service

You can read more about the merger in this article on Money Management HERE: Vision Super and Active Super enter next merger stage and announce CEO | Super Review (moneymanagement.com.au)18

FAQs about Vision Super:

When was Vision Super founded?

Vision Super was started in Australia in 1947 as the LASF.

How many members are there?

Currently, Vision Super has about 85 000 members.

Is Vision Super an APRA fund?

Vision Super is an APRA fund19. This means the Australian Prudential Regulation Authority (APRA) regulate Vision Super, just as it does other super funds. APRA regulation provides some protection to members to oversee that within reason, financial institutions deliver on promises made to beneficiaries.

Is Vision Super a good super fund?

Yes, it seems Vision Super is a good super fund. It’s a low-cost fund that consistently performs well. Perhaps the only downside is their insurance premiums seem to be higher than those on offer by other funds.

Vision Super is also entering into a merger to take it from a mid-range fund to a large fund which may provide opportunities for economies of scale. There’s also a chance it will change their member-focused approach.

Conclusion

Vision Super is an award-winning Australian super fund, open for the public to join. Initially, Vision Super commenced as the Local Authorities Superannuation Fund (LASF) in 1947 for local government employees. Vision Super has over $16 billion in assets under management and around 85 000 members.

Compared to other funds, Vision Super has relatively low fees and good returns. However, its insurance premiums appear higher than some funds.

Vision Super is a mid-range fund and is in the process of merging with Active Super, another mid-range fund. While it’s predicted the move will save on costs in the long term, commentators have wondered if growing into a larger fund will change their culture of being customer-focused, but only time will tell.

You might also be interested in my following Superannuation reviews:

ART Super Review; Is It A Good Super Fund?

REST Super Review – How Do They Stack Up?

UniSuper Review – How Do They Compare?

Australian Super Review – What You Need To Know

MLC Superannuation Review: How Do They Measure Up?

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.