What are the options when it comes to investing for kids? There are more options than you may realise. What are the tax implications when it comes to investing for kids and what is the best way to teach kids about investing?

Introduction to Investing for Kids

When it comes to investing for kids, giving them money management skills and financial literacy can give them a head start, setting them up for life. With time on their side, investing for kids can take advantage of compound interest and it can help foster life-long financial literacy and money management skills.

When developing an investment plan, consider timeline, asset class and tax implications. You could consider direct shares, LICs, ETFs, Investment Bonds, Education Bonds and Trusts. You could set up a minor account in your brokerage account or microinvesting options can get them started sooner. Remember, the following is general advice, not financial advice, you need to consider your own particular circumstances and financial situation before acting.

Disclaimer: CaptainFI is reader supported, which means we may be paid when you visit links to partner or featured sites.

Why should we encourage investing for kids?

When it comes to investing for kids, things have come a long way since the pink piggy bank with a bit of pocket money rattling around inside it.

If Robert Kiyosaki’s ‘Rich Dad’ taught us anything, it’s that you don’t need to earn a lot of money for money to work for you. Another lesson from the Rich Dad Poor Dad author, is that Kiyosaki didn’t learn about money at school.

Teaching kids about money management starts at home. And if we start them on the right path early enough, they have the greatest asset of all. Time. With time on their side, they can harness the power of compound interest and from little things, big things can grow.

After time, perhaps one of the greatest assets when it comes to investing for kids, is having parents that understand the how, what and why, to steer them on the right investment path. Investing early teaches kids to have a healthy relationship with money, enjoy the freedom of passive income, the benefits of waiting until you can afford what you want and how to avoid falling into the debt trap later in life.

“You’ve got to tell your money what to do or it will leave.”

DAVE RAMSAY

Is it legal for kids to invest?

Generally, in Australia, a person under 18 years does not have the legal capacity to enter a contract and requires a trustee or guardian to do it for them. While kids can’t enter a contract for themselves, it is legal for kids to hold investments in their own name. That said, putting an investment in your kid’s name is not usually a good idea. It’s a complex area with pros and cons, but the main reason why not is the potential for sky-high tax rates. Tax rates up to 66% act as a deterrent to prevent the wealthy from dodging tax by putting assets in their kids’ names.

The alternative is for an adult to invest money on a child’s behalf. This allows kids to have some skin in the investment game, while also being tax-effective, so as not to erode the gains.

When it comes to investing for kids, it’s important to think about the legal structure it will take and the tax implications on investment returns, not only for yourself year to year, but also down the track if it triggers a capital gains tax event that impacts what your child actually gets at 18.

How can we invest for kids? What are the options?

When it comes to investing for kids, there are a few options out there.

Savings accounts

There’s a reason why school banking programs exist because if they can get them young, it fosters customer loyalty. However, banks are not educators and the products they sell, such as debt, are not always in the individual’s best interest. Educating your kids on money management, including setting them up with the best bank account to save into, is a great way to start investing for kids. Being willing to change banks to get a better deal at different times in your life is also an important lesson to learn. Just remember not to leave the savings in there for too long. In real terms, the money will be going backward when it comes to the low interest earned and high inflation.

Investing for kids in the stock market is one way to go. The International and Australian (ASX) stock markets offer many options for investment such as individual shares, Listed Investment Companies (LICs) such as AFIC and Exchange Traded Funds (ETFs). Directly buying individual company shares is an option, however, diversification can be difficult if only buying small amounts. Australian shares are always a great option for the franked dividends too.

Listed Investment Companies (LICs)

Investing in the share market via LICs such as AFIC, is another way to invest for kids. Unlike holding shares directly, LICs allow you to buy into a company that holds interests in shares, property and bonds. Managers actively manage the LIC to try and outperform the index, so fees are higher, but the upside is diversification.

Exchange Traded Funds (ETFs)

Another alternative is ETFs such as Vanguard or Betashares, which are investment funds listed on the stock exchange. Again, diversification is the key, with a focus on a specific industry or market. Unlike LICs, they’re not actively managed, so fees are low and the ETF usually mirrors the rise and fall of the market.

How to buy and sell shares – Moneysmart.gov.au

Investment Bonds

Investment bonds, also known as insurance bonds, are another option. They’re sort of like a managed fund, with their own rules and structure. Investment bonds are for long-term investing, you can start with $1000 and put money in every year. Initially, the tax rate is a flat 30%, but over 10 years the gains become tax-free if you’ve followed the contribution rules. For families on a low income, this product may not be tax-effective on an income tax rate of 19%. Also, Some investment bonds can have high fees, so look for fees below 1%.

Education Bonds

Education funds like ASG provide an investment-savings product that has a flat 30% tax rate. Basically, you pay into it when your child is young, then when they are older, they get a “scholarship” for their high school or uni years – if they end up going. However, they tend to be high fee, complex products that lack flexibility. A regular investment bond offers the same tax benefit, with more flexibility.

Minor accounts

When it comes to investing for kids and buying shares, LICs or ETFs, the easiest way to hold them in trust for your child is in a minor account. First of all, you’ll need to set up an account with a broker. There are lots out there to choose from. The big banks like CommSec and NAB have offerings, but brokerage fees are an important factor.

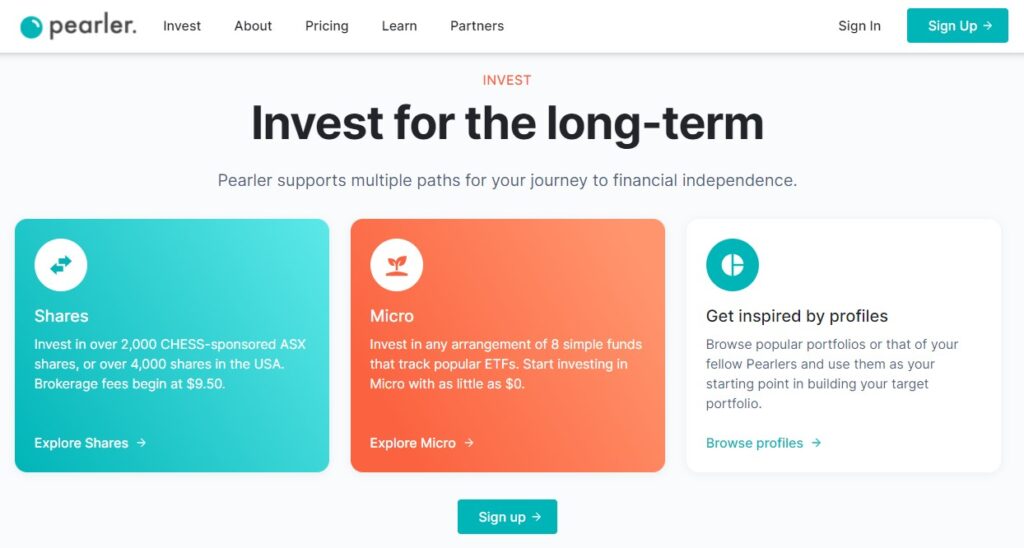

There are plenty of apps with low overheads, like Pearler, SelfWealth and Stockspot that provide brokerage at a low cost and also offer a minor account for you to invest in for your kids.

If you haven’t set up a brokerage account before, there’s a bit to it, with identification and verification. It’s not like you can just jump on the ASX and snap up some BHP. Give yourself time to sit down and work through it. It can also take a few days for the account to be activated. Just ensure you know and understand the tax implications of investing in minor accounts, as once the account in a child’s name is earning more than $416 per year, the tax rate will be 66%.

Investing for kids – without the fees | Stockspot

Microinvesting

One thing that always amuses me is when articles say you can get started with as little as $1000. The fact is, to most families even with just one child, $1000 is a lot of money! The good news is, there are microinvesting options that can help get kids investing with just a few dollars. They are accessible, low cost, easy to automate and educational!

Pearler Micro have a choice of 8 different ETF funds, they have pretty low fees compared to others on the market ($1.70 per month, or FREE for balances under $100), and they have round up and auto invest features.

Raiz Kids is part of the Raiz platform for microinvesting with small amounts. When an adult opens an account, they can select the Raiz Kids option. For balances under $15,000 there is a monthly fee of $3.50, which may eat into the earnings.

Superhero is another app with a minor account. You can invest from as little as $100, but the shares are pooled under Superhero’s Holder Identification Number (HIN), rather than you owning them under yours.

BrickX Minors is for investing in properties. With a start of $250, and $50 per month, you can build your portfolio, and receive a portion of rent in return.

CommSec Pocket is an app that allows investors to be more hands-on when investing in ETFs. It’s cheap at $2 per trade under $10,000. However, it does not auto-invest your deposits.

Spaceship and Sharesies currently don’t have minor accounts but are working on it. However, 16 is the minimum age to open an account with Spaceship.

Just keep in mind that you may only be able to have one minor account attached to your adult account, so your partner may need to open an account with a different email address if you’ve got more than one child.

There is also the option of just microinvesting in your own name, using one of these platforms and keeping that money as just belonging to your child. You can always sell at a later stage or transfer over to them when they are older.

5 Investment Products Designed for Kids | Canstar

Trust accounts

When we think of trust accounts, it’s usually within the context of a rich kid with a trust fund.

For the more cashed-up investor, a formal trust for investing for children can take the shape of a Family Trust. Its main advantage is it’s flexible with the types of investments and property it can hold. With a trust account, there’s flexibility with the trustee deciding who the beneficiaries are year to year, and what they’ll receive. The main disadvantage is cost. It’s expensive to set up, and there are ongoing tax obligations.

Keeping it in your name

When it comes to investing for kids, putting it in your name may be the most obvious choice, but there may be other options.

Alternatively, relatives such as grandparents may hold investments for their grandkids, while Family Trusts may also hold investments that benefit the child. Green Taylor Partners have some interesting information as to why we shouldn’t put shares in children’s names. You can read more info here: Don’t give shares to children – Minor Shareholders – Green Taylor Partners

How are investments for kids taxed?

The way investments for kids are taxed depends on who’s name they are in. The ATO allows minors $416 untaxed income. Above that, a tax rate of up to 66% can apply. This is to stop rich parents using their kids as a tax haven. In comparison, adults can earn up to $18,200 tax free.

If you were to invest for your child in shares on the ASX, you are able to buy them in your name, but hold them in a minor account, making you the trustee. When your child reaches 18, the ATO considers the child as the beneficial owner all along, avoiding capital gains tax.

You would still be liable for tax every year from dividends, so it’s best for the parent with the lowest income to buy the shares in their name.

If you held the shares in your name alone, tax on earnings would apply, plus CGT would have to be paid at transfer. Children’s share investments | Australian Taxation Office (ato.gov.au)

“The best way to teach your kids about taxes is by eating 30% of their ice-cream”

BILL MURRAY

What are the best investment plans for a child’s future?

Identifying the best investment plan for a child’s future is a bit like asking how long is a piece of string? It depends.

In order to head in the right direction, you need to consider the investment timeline, what you are planning to invest in and the bigger picture when it comes to tax. Add a dash of diversification, and you’re headed in the right direction.

How do I teach my child about investing?

When it comes to teaching kids about investing, the usual rules apply. Make it age-appropriate. Teaching financial literacy can start young with a toy cash register and pretend money. Barefooters would also include the spend, save, share model of money management when it comes to pocket money, money received as presents and earnings from odd jobs. Barefoot for Families has some great advice for teaching kids about money – you can read my review here.

Then as kids get older, get them involved in selecting their investments. If they’re interested in trains or planes, consider the transport sector. If they’re computer wizards, look at dot coms. If they like gardening, perhaps choose an agricultural focus.

Spend time with them, checking the progress of their investments. This helps turn the intangible stock into a tangible experience. It will also provide an opportunity to teach them to manage their emotional responses to how their investment is going. Teach them about the highs and lows of the stock market. Teach them about past performance and the fact that past performance doesn’t always indicate future performance. For teens, get them involved in managing a virtual portfolio.

Of course, that all assumes the parent’s head is in that space. If not, be willing to travel the learning journey with your kids. After all, when it comes to investing, we all started at square one.

Conclusion – Investing for Kids

In conclusion, kids have time on their side, so when it comes to investing for kids, they can reap the rewards of compound interest. Kids can’t invest on their own, so having parents to help them is important. Investing for kids is not just about shares and bonds, teaching your kids financial literacy and money management skills will help set them up for life.

Always consider your own personal circumstances and your own objectives when it comes to investing, and seek advice from a financial advisor if you want more individualised assistance.

CaptainFI is reader-supported, which means we may be paid when you visit links to partner or featured sites.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.