CaptainFIs financial and personal update for Q2 2025

Captain FI is not a financial advisor, does not hold an AFSL and this article is not financial advice. This website is reader-supported, which means we may be paid when you visit links to partner or featured sites, or by advertising on the site. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer

Captain FI’s personal update

Since welcoming our beautiful little baby, life has become quite different. I find my attitude towards things changing, things I used to find important seem… not so important, and even my attitude towards finance is shifting – in particular I am much more inclined to pay for convenience (probably due to my lack of sleep), things of higher quality and better condition – that function better and ‘just work’ which saves us time, and also on getting things that are safer.

It has been a season of change and contrast for us, with the sad news of three close family members being diagnosed with advanced stage terminal cancers, juxtaposed against the wonderful brightness and zeal of our growing child. We are just amazed at the leaps and bounds in early childhood development, and I suppose truly coming to terms with accepting ‘our place’ and roles as the middle generation in the prime of our lives – farewelling the older, and welcoming the new.

Most of our close friends are parents, and there are about half a dozen of us with newborns, and our group chats are often filled with celebrations about babies hitting new milestones, or commiserations about the latest ‘poo-sploshions’! We had an awesome baby shower and its been interesting seeing how everyones predictions on milestones are playing out.

Whilst I was very anxious about travelling with such a young child, we did return to Adelaide for a week in order to visit and farewell some of our family who were very sick. It was a very difficult and confronting trip, both physically tiring (baby and trying to fit everything in) and incredibly emotionally draining knowing that it would likely be the last time we would see them.

Returning to Adelaide I also felt as if a cloud was fogging up my brain, and all I can think of is that it was ‘situational depression’ due to memories of going through such difficult times there, magnified by the new parent sleep deprivation. I also never really sleep that great the first few nights in a new place either. I was also even a little embarrassed to say it was bloody chilly! I usually never get cold, but the dry, cold air was messing with all of us (dry sinuses and skin), so we must all truly be Queenslanders now haha.

Everything in Adelaide was bone dry and dusty, and the plant life all seemed dead, yellow or brown and crispy, apart from some peoples irrigated lawns. Everyone was telling us it hadn’t really rained for 6 months and they were in a drought. This really reinforced how glad I was that I moved somewhere lush where I can grow my food forest with no worry for severe drought.

We were very grateful to stay with close friends who went over and above to make us comfy during our stay, including giving us the keys to their brand new car (which was super nice to drive – I get why people want new cars). Thankfully the trip went as well as it could have, and touching down back in Queensland and then driving back up into the lush green hinterland I felt that tired, depressive fog begin to lift and once we were all home and had a shower and long sleep (baby slept all night!) we all felt refreshed, rejuvenated and rehydrated.

Anyhoo, with the focus on child rearing, temporarily we have decided to pay for a bit more help with things like cleaners, pool maintenance and getting the orchard and paddock grasses slashed to reduce our workload. Yes it does kina suck having to fork out for these things, but for now its worth it. We also paid more for some contractors to help with projects but it didn’t really work out as I had planned.

I ended up spending a lot of money on contractors in those early postpartum days – we did consciously make the decision to spend on getting projects finished but unfortunately a lack of oversight and mismanagement on my part meant we ended up haemorrhaging money unnecessarily (over $10,000), and I still have to still buy more materials and finish a couple of big projects myself (chicken coop, retaining wall and fencing).

I am really enjoying spending time with my wife and child, and it has been lovely to have our extended family visit from interstate and overseas, including having my wonderful mother in law stay with us pretty much indefinitely. After struggling through the first six weeks of parenthood alone, she has been incredibly helpful in supporting us and reducing our workload. My Mother in Law is a retired chef who used to have her own catering company, and she has a real passion and talent for cooking – so we have been very spoiled.

We are thankfully out of ‘survival mode’ and beginning to look after ourselves a bit more including healthier meals and getting back into some exercise and swimming, relaxing by the pool, and now bub has had her vaccines, beginning to invite our close friends and family up to visit the baby.

We are expecting my father in law shortly, and then also a visit from extended family including sisters and brothers in laws, nieces etc., as well as some more visits from close friends coming up from interstate. It is all happening!

I have also been able to get some stuff done around the farm including some overdue pruning and clearing, maintenance works and finishing off the chicken project….

So. The chicken project…..

I didn’t want to pay several thousand dollars for a prefab chook coop for the orchard, so I decided to build one myself out of recycled materials. I concreted a slab and bought some metal aviary walls on marketplace, but after getting stuck there I enlisted the help of a chippy to finish it – putting on the roof, building the roost and nesting boxes, doing a final snake proofing and putting in the run fencing and gate.

Despite trying to use recycled as much as possible, the materials have tallied up to over $2,000 and I’ve spent nearly $5,000 on labour. Because it was a friend, I felt awkward, and just kept giving more money to cover the ongoing work he was doing.

When we hit the $7k mark, my wife put her foot down and said that enough was enough and I would have to finish it myself.

The problem was that we didn’t have a contract, he didn’t have experience building coops, and we didn’t have aligned expectations over how long things were going to take, or even what was going to be done. It was just ‘$50 an hour to give you a hand with the coop’ – I thought it would have only taken a couple of days tops, worst case around 20 hours or about $1,000 of labour.

Obviously I feel like a silly Goose – I’m supposed to have a degree in project management ![]()

![]() so I was pretty sheepish when I had to call him and say that I wouldn’t be able to hire him anymore to finish the job.

so I was pretty sheepish when I had to call him and say that I wouldn’t be able to hire him anymore to finish the job.

Unfortunately the reality was that I still had to redo a bunch of stuff that wasn’t done right, and it still took me a few more days work before we could get the chooks in as there were a heap of unfinished bits – installing the auto door, waterproofing the nesting boxes, fencing in the run etc.

It turned out using recycled materials was costlier than just buying new fit for purpose materials due to the time taken to repair or adjust them – second hand roof sheeting needed to be waterproofed with caulk and flashing which ended up costing more than new sheets would have!

Considering my labour, this is a >$10k project, and the coop is probably way larger than we needed (3 doz bird capacity, whereas we probably will only have 1 doz at a time… but who knows!)

My lessons learend and the key take aways if you are ever considering outsourcing on a project;

– set requirements based on what you actually need

– agree on a set scope of works

– outline a schedule (even if its just a rough estimate!)

– avoid making significant changes / scope creep

– monitor work progress against the schedule

– use material that is fit for purpose (sometimes using recycled materials is a false economy).

– consider paying more for experienced trades or specialists that will ultimately work quicker and get the job done cheaper overall

Once we start getting better produce yields from the farm (plus I get better at fishing) our food bills will hopefully go down a bit, and we should be able to start properly selling our produce or bartering more for other things we need. For example we have had a bumper ginger harvest this year – over 200kg which we have been able to barter to our friends neighbours for things like fresh eggs, help around the farm and some home cooked meals.

I swapped a beehive I generated by taking a split off of one of my larger hives, and some surplus beekeeping gear I had for over $1500 worth of electrical work we needed done to a sparky friend. I also swapped a smaller hive (another split I made) for some fruit trees and pots from another friend, as well as helped another mate capture a swarm that had moved into their roof! It was rewarding to help them all get set up and do some beekeeping mentoring to help build their confidence

We also managed to get an incredible 147kg of mud crabs this season which has just finished up due to the cooler water temps. Most of the crabs ended up on our dinner table and it has been awesome to invite visiting friends and family over for some some huge mud crab feeds – its a pretty cool experience to be able to share. My wife even famously said “please stop bringing home mud crabs I’m so sick of them and it’s just so much work to eat them” – words she almost instantly regretted saying!

When my wife and I went on a trip to Singapore recently with our family last year, we paid over (AUD) $1500 for a Singapore chilli crab dinner for 11 people – I still feel queasy remembering paying that bill (and the associated bank forex fee). So we joke that crab we have caught well and truly makes up for that dinner plus the cost of the new boat!

I was very happy to be able to share a lot of them with our neighbours and new friends we have made in the area. One good thing that my Dad did teach me, was that it is important to do the ‘Auntie Run’ after a good catch – something we used to do with crayfish when I was a kid. Essentially, you gotta share the catch around with the oldies that aren’t able to get out on the water anymore or afford to buy it (especially to the widows).

In my last update I wrote a list of the expensive things we had ‘splurged on’ last year, and thankfully we have slowed down a lot on the purchases this year now that we are mostly established. There are still a couple of big (and expensive) projects I want to do, but a bigger priority at the moment is getting “Back to FIRE” – we are trying to reduce our expenses, pay down our debt (non tax-deductible), and then grow our investments to provide higher levels of passive income again (roughly in that order).

Once we are feeling a bit more comfortable, we will look to tackle some of the remaining projects such as the shed, extra tanks, orchard netting and irrigation – for now it is still just going to be me and the hand held hose in the orchard once a week during the dry season!

We did however, splurge on a second vehicle – funnily enough I was agonising over this (non essential) purchase for almost all of last year, but it wasn’t until the birth of our child did I fully realise how much we would want a newer, safer and larger car. We wanted two cars for flexibility (and redundancy) because we live rurally, and thought since we are getting a second car we may as well get a decent one that would last us for at least the next 10 years to accommodate our growing family, plus the influx of visitors we plan to have now that we live in paradise.

Yes the safest option is just not to drive as much, but there are some unavoidable trips and I fully understand this was an emotional and convenience purchase, not necessarily a ‘risk optimisation / minimisation’ purchase. I didn’t like the idea of my wife being stuck at home with baby and no car if I wanted to go out fishing for the day – not only just for her convenience if she wanted to go out, but in case of an emergency where she might need to leave with baby – medical issue, fire etc.

We opted for a second hand 2019 Kia Carnival Platinum edition in diesel – and it is awesome. Yes it is second hand, but being the top of the line model and low mileage means we got a lot of car for our money ($25k). It uses less fuel than my ’06 station wagon (despite being nearly twice the size!) and is loaded with the latest tech, safety features and creature comforts.

One of the things we love about the car is we can load the whole family at the moment – Mum, Dad, Bub, Lola (grandma), the dogs, the pram AND still have loads of room for shopping and 4 seats left for visitors! I have managed to fit sheets of plywood and my ride on mower deck comfortably inside with the seats folded down. We don’t need to use the rear row of seats yet unless we have visitors or are carpooling, but once we have more kids they will begin to fill up! Since we only do a few thousand km a year at the moment, we don’t really expect it to wear out any time soon!

Eventually down the track we will also look to upgrade our other station wagon to something with more torque for towing the boat – perhaps something like a diesel Pajero. Our priority is to pay the house mortgage off first, though (which we want to try and do in the next ten years). Thankfully this isnt really needed yet it’s only a short drive to the local boat ramps, and it’s only a 4.5m tinny so low range on the subie is more than enough to launch and retrieve to keep us on the water, as well as tow our 6×4 trailer for our random farm needs for now.

We also had expenses for an international trip and two interstate trips we will take later in the year (flights etc) as well as the week we just spent in Adelaide, which I haven’t really tallied costs for (and probably won’t bother doing).

Captain FI podcasts

I have half set up my recording room, but just been so busy with the new baby and projects to really do any recordings – I have committed to a few interviews and recordings in May, so there will be new content coming soon!

You can still check out the previous episodes of the Financial Independence Podcast on Spotify or now they have been uploaded to the CaptainFI YouTube channel!

Unfortunately spotify for podcasters has decided to remove some of my older episodes which was annoying, I think its because the intro jingle I used (from a royalty free database!) was bought out by someone and they have slapped a licence on it. Annoying, but I will go back and just edit out the intro and outro and it can just cut straight to the episode – hopefully that keeps everyone happy.

Captain FI blog articles

As I mentioned, I have been slowing down with blogging while we get settled into the new place and adjust to our new life – incase you missed it, my last net wealth update is below

- January 12th | Captain FI Net wealth Update Q1 2025

Captain FI 2025 spending figures

As I have talked about in my last few updates, our spending has drastically increased since we bought the farm and started our family. Last year (2024) we ended up spending $144K, which was a stark contrast to the $69K cost of living we had in 2023. A lot of this was one-off expenses associated with moving, setting up our new house, maintenance and farming projects, and preparing for the baby.

The tally so far for the first Quarter of 2025 is an eye watering $52,700, with an estimate of another $56,000 to spend (cost of living plus commitments to projects and travel) for an total projected 2025 spend of around $109K.

It is good to see the trend coming back down, and after factoring the $25K spend on the car as well as one off expenses on fencing, landscaping and travel, this represents a cost of living of closer to $80K which I think is pretty reasonable for our situation all things considered.

Last year I was estimating our ongoing ‘base level’ of living expenses to be around $95K for 2025 (which obviously didn’t include buying a new car!), however thanks to paying down some debt, restructuring the mortgages and tightening our belts a little, our revised cost of living estimate should be closer to $70,000 per year.

As i mentioned above, as the farm begins to produce more and I get better at fishing, I am hoping our food bills will go down and I will be able to do a bit more bartering with friends and neighbours – which should save us all money, and let us pay down our mortgage and invest faster.

Captain FI’s Investments

I don’t calculate a Net Wealth or Savings Rate Figure each month anymore, but I do try to keep a rough track of everything for these quarterly updates

My investments (outside super) are split across the following areas;

The ‘FIRE’ Portfolio of Index ETFs(SOLD Dec’23 to fund dream home – awaiting debt recycling to rebuild portfolio).- My primary place of residence – hobby farm in Queensland.

- Investment Property – Residential duplex

- My company – which runs a portfolio of content marketing websites

- Cash (mortgage offset account)

- A small Angel Investment in the investing platform Pearler

NB – A while ago I ended up divesting in various things such as RoboAdvisors, Micro investing funds, Managed funds, Metals/resources, and a few other speculative investments or experiments I had invested in, in order to simplify my finances. I had racked up a complex mix of investments as I wanted to try out and review various investing services but this became unmanageable in the end and I needed to simplify my life.

In December 2023 I also sold off the ‘FIRE’ Portfolio (mix of Index ETFs) to fund my dream acreage purchase, but I will be rebuilding this to build passive income through debt recycling over the next 10 years to reduce our families reliance on my business and my wife’s income.

The ‘FIRE’ Portfolio (Exchange Traded Index Funds)

As you may have known, my ‘Financial Independence Retire Early’ ETF Portfolio was a simple, passive share portfolio split between three parcels of low-fee, index-tracking Exchanged Traded Index Funds (ETFs) to achieve global diversification.

I began switching to this passive index approach to investing in 2018, firstly by adding new contributions, and then over time by divesting in other assets (individual shares, managed funds, LICs etc) and rolling the investments over to it.

- I tracked my share portfolio using Sharesight, which means my portfolio accounting and tax reports are completely automated.

This was sold in December 2023 to fund the acquisition of a hobby farm, after six years of passive index fund investing. Going forward I will be first building up cash again for an emergency fund in the mortgage offset, and then when we are ready to invest I will be redrawing from the mortgage to invest (debt recycling) using something like the Betashares DHHF ETF which is an ‘all-in-one’ ETF in order to keep things simple.

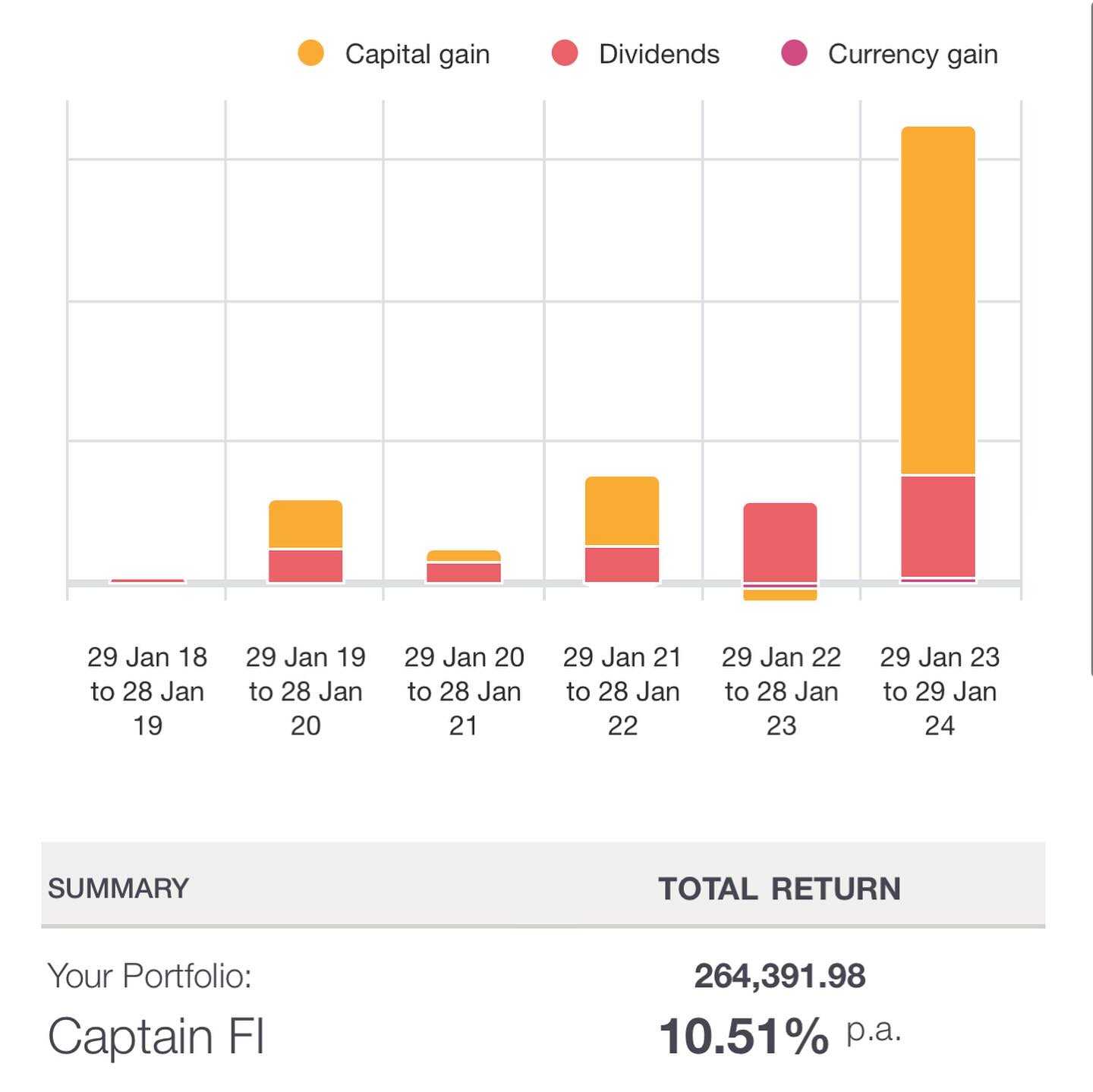

Cashing in the chips with a total return of 10.51% was a good feeling. I know the market has continued to grow in the six months since we have sold, but you know what, I achieved what I set out to do which was to become financially independent and retire early from the rat race / grind, and buy my dream acreage to start hobby farming and raise a family. I will get some skin back in the game with the share market soon!

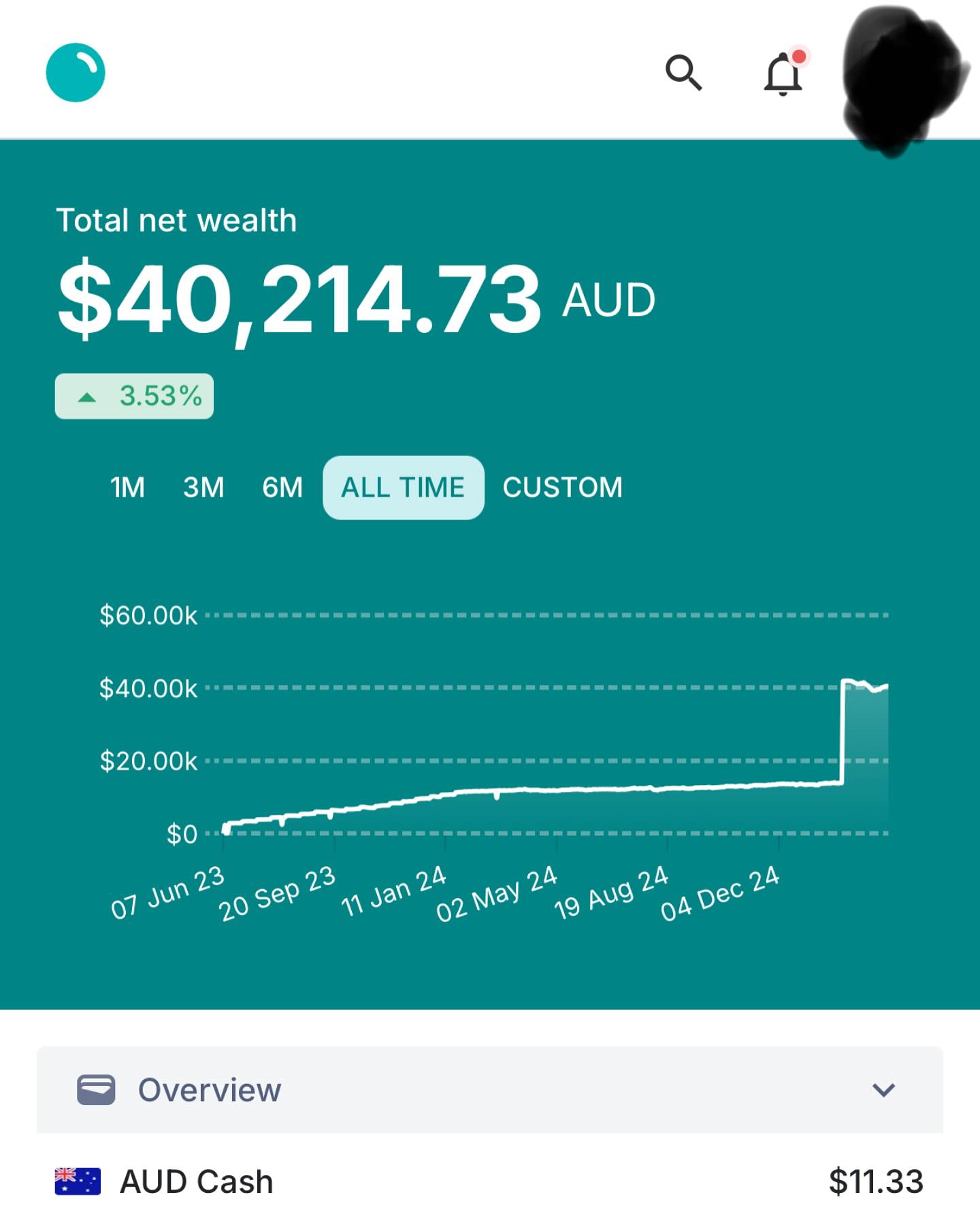

Whilst this is not my investment, my wife and I decided that we would start building up more investments in her name – this was a recent progress shot when we decided to lump sum into DHHF due to market movements. Previously she had been DCA.

Captain FI’s PPR (acreage)

To keep things simple, I just value it as a residence only and use an online valuation tool. The current PropTrack automated online valuation estimate is $2.475M, which is up $58,000 from the last time I checked it for the Q1 2025 net wealth update.

I currently owe $550K on the PPR mortgage, with $60K in the mortgage offset account. The net mortgage position is $490K (6.19% interest rate) of which I pay a $3,750 monthly repayment (about $865 a week).

I had previously been paying weekly to try to get ahead on the mortgage and reduce our debt in order to refinance to a better rate, and after this I have now switched to monthly repayments to reduce expenses and improve cash flow.

A financial advisor recommended paying down the debt, as this puts us in the best financial position when applying for government benefits like the family tax benefit (which we are eligible for now because of the birth of our child), as I was told money in a mortgage offset account is considered an assessable asset for asset tests, and deemed to produce an income for income tests.

So for our situation at the moment it was better to focus on paying down the PPR mortgage and get a risk free ‘grossed up return’ of around 8% plus potential government family tax A and B benefits.

Debt recycling plans

I had plans initially to pay down and then redraw my inheritance from the mortgage and use the money for investing (this process is called debt recycling).

That way you buy shares which provide a stream of dividend income and capital growth of the shares, and the interest you’ve paid on that portion of the loan is tax-deductible. The net effect is some more dividend income, a growing share portfolio and paying less tax, which you can then use that increased cashflow towards the mortgage.

At the moment, this plan is on hold until we can clarify what effects it might have on family tax benefits and child care subsidies, etc, and I am hoping to have a plan in place by mid year for what we will do to optimise everything. But it is looking right now like doing debt recycling and pulling out equity to buy shares would adversely affect our eligibility. Those benefits, plus the certainty of paying down mortgage (guaranteed 8% grossed up return) would ‘outperform’ the share market with none of the market risk – hence why we are focusing on paying down the debt first.

Despite my love for the VTS/A200/VEU split, I think I will probably just use something like the Betashares DHHF or Vanguard VDHG ETFs as the investment vehicle for simplicity sake.

You can play around on https://debtrecyclingcalculator.com to see what effect debt recycling might have on paying off your mortgage quicker, but you just have to be comfortable exposing yourself to market risk and the fact that you are essentially using your family home as collateral. As always, everything has trade offs. When I played around with it, it showed I could pay the mortgage off in 11.5 years if I did the whole amount available for redraw.

Unfortunately, debt recycling is just not as attractive for me now that I am not a high-income earner like I used to be, and now that interest rates are higher, and that now I am a father and my appetite for risk has reduced.

Even just keeping cash in an offset account or making extra mortgage repayments makes a huge difference to paying off your mortgage faster. Using the ASIC moneysmart calculator showed that just keeping the money I was going to debt recycle in the offset account would actually reduce the mortgage life down to 12.5 years – a 10.5 year reduction, and only one year longer than the debt recycling option, but with none of the market risk.

Its actually a pretty hard decision to make, which is probably why I have been dragging my feet on executing this plan. I may end up just debt recycling a smaller amount.

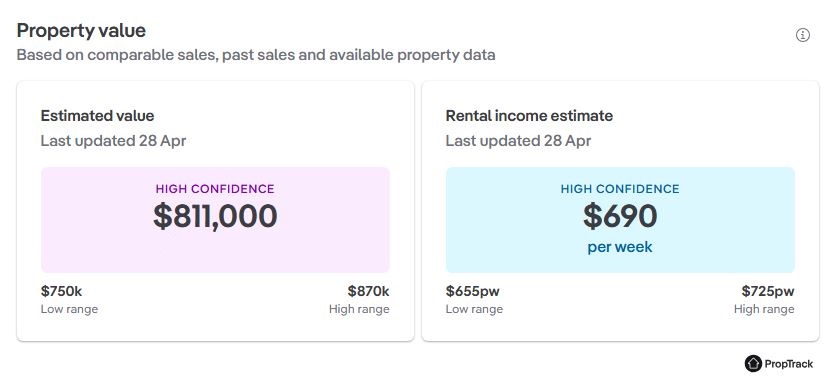

Captain FI’s Investment property

The goal of the Investment Property is to build wealth that is diversified outside of super, shares and the farm, through the capital growth of the property.

The current PropTrack automated online valuation estimate is $811K, which is up $44,000 from the last quarters estimate. I have seen sales data for nearby similar properties that have recently gone for over $800K, and some currently advertised over $850K, so I am happy to take the mid range high confidence estimate.

The property has a $533K mortgage (6.14%), for an equity position of $278K. I no longer use the offset account for the IP. Instead, I put all cashflow buffer into my PPR offset and draw expenses for both properties from that (I then just record IP expenses for tax time).

I pay a $3,317 monthly repayment for the loan and collect $700 weekly in rent. Other costs (insurance—$1500, rates—$2000, water—$500, property management fee—6%) add up to around a $9,500 shortfall per year. In other words, this property costs me $183 per week to hold, plus any maintenance issues that crop up along the way.

This means it is negatively geared (which is annoying for someone who is trying to be retired) but the interest and other costs are tax deductible, and that combined with the depreciation schedule does give me something for the tax return – although I am not a high-income earner anymore, so I don’t get much back. I remember a financial advisor telling me “don’t let the tax tail wag the investment dog” anyway.

My main reason for continuing to hold the property is that I think the capital value will go up, and property prices only have to rise by about 1.5% per annum to cover my cashflow loss. Property spectators are predicting at least 5% growth for the region, so I am confident the growth will more than account for the deficit. If we continue to see record immigration, inflation and building shortages, housing prices could go up significantly and we would benefit from that.

Over time, rents rise too, and this means it should also eventually become positively geared and provide us with a source of income. The current estimate is that the crossover point should be in a couple of years (2028). Despite the prop track upper estimate being $725/wk, our property manager told us that similar properties are going for $750 a week already, as there is a very low vacancy rate. The limited number of available rentals on the market, coupled with strong demand, is driving rental prices higher. If rental prices exceeded $885 a week, then we would be cashflow positive and the IP would begin being a source of income.

We obviously want our investment to do the best possible, but we also value having a good relationship with our tenants so they look after the place and we have less maintenance costs and tenant turnover, advertising fees etc – so we are happy to have it rented out slightly below market value. We will probably raise it a bit when the next lease agreement is due, and go with just under what the agent recommends.

Annoyingly, our holding expenses are also rising – for example I can’t believe how expensive rates and insurance have gotten. They are significantly outpacing inflation (and rental increases), which obviously cuts into the cash flow. Our council rates keep rising by over 5% every year, and the insurance is up by over 30% even with shopping around for a better deal. Unfortunately, that seems to just part of the deal with property investing – everyone involved seems to have their hand in the cookie jar and wants to get their cut along the way.

With my current income and level of debt, it’s not really possible to refinance due to serviceability issues – but if I could, I would love to access the equity to buy shares and start building up the passive income stream again.

I would also prefer to have an interest-only loan so I wasn’t paying down principle and locking up my cashflow as equity – we would still be gaining equity with the property’s capital growth anyway, as the housing market continues to grow over time. This is why we switched from weekly back to monthly repayments, with the money being kept in the PPR offset account – so we pay off as little as possible from the IP principle.

I have previously written a full separate article on the IP build if you want to know more about the process – CaptainFI’s residential property development investment.

Captain FI’s Online Business (website portfolio)

I have a small website portfolio of content and affiliate marketing sites. These make money semi-passively from display Advertising through managed ad networks such as Adsense and Mediavine, and affiliate programs such as Amazon Associates and other direct affiliate deals.

The overheads are pretty low – just some software subscriptions, and I’m pretty much just back to doing everything myself again to save on outsourcing costs – previously I used a bunch of virtual assistants and writers, but I’m avoiding this cost at the moment because I want to minimise overheads so I can maximise bottom line profit.

Actually I haven’t been publishing much at all, and the majority of the sites I am just keeping in ‘caretaker mode’ as I sell them off.

I think I also got sucked into some of the entrepreneur porn you see on social media and was getting an ego boost out of having so many staff and so many sites, when in reality it would just be more profitable and less work to do just stuff myself (at least for a while initially) on a couple of bigger sites only – reading the book ‘Profit First’ was a good wake-up call to help put the ego in check!

On one hand I want to be transparent with my investing and money, but when it comes to the websites I have to maintain privacy about SEO, traffic, contracts and cashflow as it is business in confidence. So that’s why I don’t really publish my business income or valuation anymore. I’m thankful I have an awesome accountant who helps me through the specifics of business ownership including the nightmare that is BAS lodgements!

Anyway, about a year ago I decided to shift my strategy and just work on a couple of bigger sites rather than trying to spread myself too thin on a massive portfolio – tbh it can be a lot of work to manage a large portfolio of sites. Right now my personal focus is on making as much money with as little effort as possible, so I can spend my time on the farm with my wife raising my kids (and doing things like my ridiculous chicken project…)

I’ve written a pretty detailed article here about how to make money online, and I recently published a few more articles about how to start making money online for beginners, as well as an ultimate list of blog income reports for anyone wanting a peek into the industry.

I still have a couple for sale if anyone is interested in giving this side hustle a go – price depending on how established and how much time, money and effort I have put into them. They range from 4 to 7 years old, with various backlink profiles, number of published articles, and traffic. You can check out this article on website operation if you are keen as I’ve listed all the details in there. Feel free to send me an email through the contact form or get in touch on social media if you are interested in buying one.

I originally learned these skills through the eBusiness institute over the past 5 years – I have done a pretty comprehensive review of the eBusiness institute as well as interviewed Matt and Liz Raad about this on the podcast again recently where we go over a huge list of frequently asked questions about online business if you want to learn more about this. They also provide some free introductory training for CaptainFI readers.

Check out these podcast episodes for more information

- Podcast | Q and A Session with Matt Raad – Part THREE

- Podcast | Q and A Session with Matt Raad – Part TWO

- Podcast | Q and A Session with Matt Raad – Part ONE

- Captain Fi Podcast | Online Business with Matt Raad

- Podcast | Digital Marketing with Richard

- Podcast | Entrepreneurship with Liz Raad

- Podcast | Digital entrepreneurs Matt and Liz Raad

I have also recently finished the Authority Hackers TASS (The Authority Site System) Course as well as the Making Sense of Affiliate Marketing course which has been a cool way to consolidate the skills I have learnt from the eBusiness Institute, and I have published a few comparison review articles such as Authority Hacker vs Making Sense of Affiliate Marketing and eBusiness Institute vs Authority Hacker which might help you choose between training providers.

Angel Investing

I made a small ‘Angel Investment’ into the Fintech platform Pearler in 2021. Pearler was founded in 2018 and launched in 2020. Since then, Pearler has carved out a niche market in the financial independence community as one of the best investing platforms available.

Pearler began as a low-cost CHESS sponsored brokerage platform designed for financial independence, and was first to market with some pretty exciting features such as CHESS sponsored auto-invest. They have a focus on financial education and wellbeing, long term investing (not trading!), low cost, no bullshit, and have gradually expanded to cover other areas such as micro-investing and superannuation.

I made an investment of $10,000 (which was the maximum allowed at the time) at about forty cents a share which bought over 20,000 shares. I believe this was a very small minority stake being less than 0.2% of the company’s $5.5m valuation at the time. This is a private company and so the shares are not publicly listed on the ASX or anything.

I made this investment because I truly believed in what the founders were doing, and I used and love the product. I had also previously done some SEO and advertising contracts for the company and knew the founders to be intelligent, honest, hard-working people with an aligned vision.

I’m not 100% sure if it works this way since I have never done Angel Investing before, but a recent-ish shares issue was around $1.75/share – so if that is what the shares are worth then I guess my stake would be worth around $40,000.

If I have done my workings correctly (and the above holds true), that would represent an average rate of return over the past four years of around 58% per annum – all in all a very good risk adjusted return and my best performing investment by far.

I am not sure what the end game is here, but my gut tells me that eventually when Pearler grows large enough it may either get listed on the ASX, or it might receive a buyout offer from a large bank, financial company or investment firm – at which point I may be forced to sell the share and pay some CGT, and I would likely use the proceeds pay down my mortgage and potentially later redraw to debt recycle into index funds.

Again, I am not sure if this is how it works and I haven’t received any official shares valuation or anything, so technically all I have on paper is my initial share certificate from 2021.

Cash – Mojo Emergency fund

Cash reserves are mostly deployed – I currently have $60,000 left in cash as the remainder has been used to pay off and restructure my home loan loan terms. Unfortunately for me, I have a rather large tax bill looming due to capital gains tax owing from the sale of my shares last financial year to fund my hobby farm acquisition. So that will wipe out a lot of the emergency fund and leave us with about 7 months expenses.

So, am I crazy for not having enough of an emergency fund? Well, its not as bad as it sounds as I do I still have some funds available as redraw in home loan, although it’s riskier than having it in the offset as technically the bank could gobble it up and cut off our redraw facility without notifying us. So why did I do it? Two reasons

Firstly – by paying down the loan balance significantly and resetting the loan (absorbing most of the redraw), I was able to have the bank recalculate my new minimum repayment which has massively reduced our cost of living – Mortgage repayments have dropped from $1250 a week down to $850. We also opted to switch back to monthly repayments from weekly repayments, which means while the loan takes longer to pay off (and we pay more interest), it improves my cash flow (and I could always stick any future savings into the offset anyway to reduce interest). This means we don’t need as much taxable income to support our lifestyle, and I can work less and my wife can stay at home.

Secondly – cash in an offset account is counted as an asset for government asset tests, and can be ‘deemed’ to provide an income on government income tests. With the birth of our child, we are shortly going to be looking at applying for things like family tax benefits. Our financial advisor recommended paying down the home loan over investing or holding it in the offset, as we were told equity in our primary place of residence would not be counted in government asset or income tests (AKA how boomers living in $10m inner city Sydney mansions receive the old age pension).

So the combined effect of lower income and lower assessable assets may mean we are eligible to receive certain government benefits such as Family tax benefits, and in the future our potential rate of child care subsidy or any other perks. For the same reason, in the short term we are holding off building up higher cash reserves or debt recycling until we know whether we are actually eligible for any government family benefits or not, and then it would just be a matter of working out how much we can earn / invest before we lose those benefits.

I am a firm believer in using all the entitlements available to you, although I have to say it is pretty exhausting trying to understand services australia and things like FTB. Its not a lot of income but its better than nothing and every little bit adds up.

Ms FI’s Investments

I posted earlier this year on social media about how proud I was of my wifes financial and investing journey. Since we got together three years ago, she has

- Become debt free – paying off over $100K of tuition costs for her three degrees

- Reached a net wealth milestone of $100K!

- Been granted permanent residency (Skilled Occupation Visa) and going for Australian Citizenship later this year

- Invested over $50K into low cost index funds in her taxable brokerage account

- Grown her superannuation balance to over $40K (invested into low cost index funds)

- Paid her airfares and expenses for 2 x 2 month international holidays

- Contributed to our household living expenses (initially 50:50, then 1:3)

- Saved a $10K emergency fund

- Massively decluttered, moving away from having piles of ‘fast fashion’ and instead now has a much smaller wardrobe of high quality expensive clothing, designer handbags etc.

- Having our baby and now breastfeeding

- Convinced me to buy her a Kia Carnival 🤣

All whilst we went through my mums palliative care, moving interstate to the new hobby farm and then working part-time through pregnancy, and now working full time raising our baby and breastfeeding. Which I think is just incredible.

It drew some pretty wild opinions and speculation on social media, and even some accusations from people accusing me of financially abusing her which was upsetting to read.

When we met, there was a significant wealth disparity and financial risk in the relationship – I was FIRE, with a ~$2M net wealth, and she had a negative net wealth (debt for student loans) and was living in Australia on a temporary student visa.

Thankfully we hit it off and an amazing relationship grew. After year of dating, Just as any financially savvy person would, I sought legal and financial advice before we moved in together. The outcome of which was that we made a binding financial agreement (‘pre nup’) – essentially stating ‘In the event of separation -What’s mine is mine, what’s yours is yours, and anything we buy jointly in the future is ours to be divided equally”. This was because I didn’t want to lose half my assets and lose FIRE over a brand new relationship that didnt work out.

After a period of living together where we contributed 50:50 to living costs, I was beginning to feel safe in that she was a lovely, trustworthy and responsible person who I could see myself spending our lives together and raising a family with. I wanted to help her become more financially literate and build her own wealth, so I offered to pay more of the living expenses (3:1) if she was happy to invest the difference.

This was because I wanted to incentivise her to start investing and growing her snowball. I suppose in my mind this was because I wanted to make sure she was ‘good with money’ and disciplined enough for long term investing so that we could have an aligned vision for our future, before we got married and had kids and shared in the results of my decades of hard work. It would also mean we would be better off in the future taxwise having a more even split of investments between us rather than having them all in one spouse’s name, and god forbid in the event of a separation then she would have her own passive income stream and retirement savings.

She was keen, and she decided to start investing into low cost index funds, setting up automatic investments – half into her taxable brokerage and half into additional superannuation contributions.

Since she went down to working part time and then on maternity leave, I now support all of the families expenses, and her part time or contract incomes go directly into growing her investments.

We both have access to money in joint accounts (as well as our own separate emergency funds in our own names) for our expenses, and we try and keep discretionary spending to a minimum – however anything under $100 or weekly spending up to a few hundred a week we don’t even discuss. It’s really just the big ticket items we chat about.

We frequently discuss our finances – expenses, income, investments and our goals and priorities, and how that shapes our current and future lifestyle.

I understand not everyone will like that, but that is our situation and what works for us.

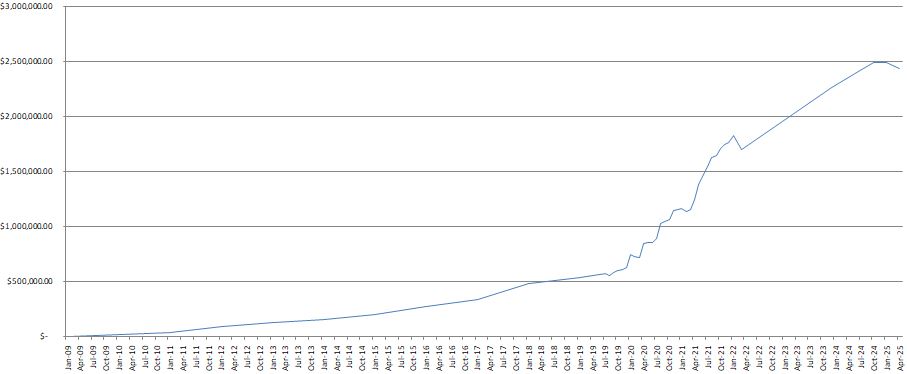

Captain FI’s Net Wealth progression

During my journey to FI I roughly documented my net wealth progression via monthly updates and a graph which was rather crudely constructed in Excel. It demonstrates the ‘somewhat exponential’ journey over my 14 year ‘working’ career. You can access the archives for my Net Worth updates here to see how it’s gone over time. Check out the graph and all the updates below to see how it has gone since the beginning.

When I FI/RE’d, I stopped putting out regular net worth updates and stopped calculating my net worth, and tried to just put out quarterly ‘updates’ but I was pretty slack. I am trying to keep up with quarterly tempo, and recently calculated my net worth after selling shares to buy my dream farm (hence the lack of data points on the graph below lately).

| Date | Net worth | Difference | Saving Rate | Notes | |

| Jan 09 | $5,000.00 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK | |

| Jan 10 | $24,000 | +$19,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 11 | $40,000 | +$16,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 12 | $92,000 | +$50,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 13 | $130,000.00 | +$38,000 | ? | Estimate NWbased on historical Super, Bank statements and assets at the time | LINK |

| Jan 14 | $161,000.00 | +$31,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 15 | $200,000.00 | +$39,000 | ? | Estimate NWbased on historical Super, Bank statements and assets at the time | LINK |

| Jan 16 | $281,000.00 | +$81,000 | ? | Estimate NWbased on historical Super, Bank statements and assets at the time | LINK |

| Jan 17 | $340,000.00 | +$59,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 18 | $482,000.00 | +$142,000 | ? | Estimate NWbased on historical Super, Bank statements and assets at the time | LINK |

| Jan 19 | $542,000.00 | +$60,000 | ? | Estimate NWbased on historical Super, Bank statements and assets at the time | LINK |

| Jul 19 | $578,900.00 | +$36,900 | 84% | Finally began tracking NW this like a proper adult. | |

| Aug 19 | $560,100.00 | -$18,800.00 (-3.2%) | 78% | Share market slight correction, Ok savings. | |

| Sep 19 | $584,744.88 | $24,644.88 | 72% | Share market rebound, savings rate not so good. | LINK |

| Oct 19 | $600,386.00 | $15,641.12 | 84% | Good saving this month. Normal salary, plus allowances, dividends from index funds, tax refund, eBay selling and was working abroad in asia where things are cheap. | LINK |

| Nov 19 | $612,917.21 | $12,531.21 | 76% | Falling short of my savings goal of 80%. Mostly domestic legs this month with higher costs. Also invested in hydroponics. | LINK |

| Dec 19 | $625,350.00 | $12,432.79 | 76% | Good savings of cash (for development) and investment, however higher spending due to Christmas period (Travel and Gifting). | LINK |

| Jan 20 | $865,212.00 | $239,862.00 | 55% | Super settlement was a HUGE boost to NW. $9K growth from stock market. Expensive month lots with lots of unexpected bills – weddings, travel, Booking flights, fines etc. | LINK |

| Feb 20 | $851,802.0 | -$16,592 (-1.9%) | 52% | Large increase in spending on myself this month, still managed to tuck away $5K to put into shares and property. Corona Virus market scare resulted in a correction and gave NW a small negative trend. Time in the market not Timing the market! Became Single again. | LINK |

| Mar 20 | $819, 354.6 | -$31,806.95 (-3.7%) | 80% | Another small step backwards in the NW due to the ‘corona crash’ in full swing. FIRE Portfolio of ETF/LICs down about 15% this month, however due to high savings rate and structure of my superannuation annuity the NW is only down 3.7%. Savings rate good at 80%, higher than usual income (with some slightly higher spending, too). Picking up shares on discount – this is the best outcome for someone in the accumulation phase with good income! | LINK |

| Apr 20 | $847,023 | +$27,668 | 85% | $11,000 in rebound of stock market capital prices alone (up 6%), plus first quarter dividends paid (heavily reduced due to banks withholding dividends). Great savings rate due to COVID-19 lock-down = no spend. Increased entrepreneurial efforts and selling down of physical possessions provided side hustle income. Two standard paychecks from flying activity; domestic day trips only so no allowances. All cash unfortunately had to go into the property development due to contract timing, I am chomping at the bit to buy some more index funds before they go back up in price too much – hence why I am selling most of my toys! | LINK |

| May 20 | $857,859 | +$10,836 | 92% | Some Great sales as I let go of my Super Sport Motorcycle, Some gym gear, expensive flying equipment and a few other various bits and bobs and invested this money. Flying still reduced, but increasing from April. The share market grew as I continued to make my fortnightly investments. I also wrote down the ‘value’ of some of my possessions (liabilities) such as my car, tools and furniture by around $10K to align them to market price (“tell him hes dreaming…!”). | LINK |

| June 20 | $858,650 | +$791 | 90% | Small Net Worth gain as I continue to declutter and simplify my life, despite being off work due to a family emergency. Share market not doing much. | LINK |

| July 20 | $888,218 | +$29,568 | 68% | Majority gain due to share market going back up, low spending due to being on the family farm and at home because of lock down. | LINK |

| Aug 20 | $1,029,293 | +$141,075 | 74% | Became a millionaire. Achieved this massive milestone I set out for myself in Dec 2019. Included unrealised gains in my property development as well as website business. Good savings rate due to not much spending, invested in Aus and total world shares. Investing in my web business. Starting to shift focus away from $$$ and more into looking after my mental health. | LINK |

| Sep 20 | S1,045,486 | +$16,193 | 60% | Officially took time off work for the rest of the year to be close and look after family during major operations. Continued to sell down physical possessions and work on digital business while at home. NW gain mainly due to valuation of websites. | LINK |

| Oct 20 | $1,064,399 | +$18,913 | 80% | Base income (retainer) and leave loading, dividend and websites provided income, as well as raiding my P2P lending capital. Significant bill for property due to design not meeting standards which effectively lowers my equity position, as well as fence being stolen. | LINK |

| Nov 20 | $1,143,433 | +$80,394 | 82% | Big gains came from share market growth (influencing both the Financial Independence share portfolio and Invested superannuation), Business gains (due to increased earnings) and a $30K boost to my annuity thanks to me logging in and checking the fine-print on the accumulation stats. I only invested around $7K. Insane that in one month, I accumulated nearly more net worth than I did in four years from 2009-2012 | LINK |

| Dec 20 | $1,152,920 | + $9,487.32 | 84% | Share market slight drop, Earnings from Business, Contract work, Selling possessions. No share market investments this month (oops! I forgot and money was tight). Invested a lot into the website business this month (way more than planned) and it is still running at a decent loss (plans to turn it cash flow positive in 3 months). | LINK |

| Jan 21 | $1,165,678 | +$12,757 | 79% | Great returns from the share market. Earnings from Business, Dividends, Flying wage, flipping items on consignment. Regular share contribution, investing in micro investing platforms, P2P lending, Investment property and big reinvestment into the business (still running at a loss) | LINK |

| Feb 21 | $1,135,272 | -$30,406 | 76% | Significant write down on property development due to council DA rejection and redesign requiring more money and creating less equity. Offset by small increase to Business value and investments. Simplified my investments and switched over to Pearler. | LINK |

| Mar 21 | $1,155,594 | +$20,322 | 71% | Continued investment into the portfolio as well as growth of investments and business. Gave my notice at work and looking for part time job at home for ‘Barista FI’ | LINK |

| Apr 21 | $1,242,220 | +$86,727 | 74% | Property development back on track | LINK |

| May 21 | $1,379,469 | +$137,248 | 72% | Massive gains in the website portfolio due to revaluation based on recent business income, big growth of superannuation due to annuity increasing (salary increment) and shares generally went up. Crypto went down by about 40% or so. | LINK |

| June 21 | $1,469,989 | +$89,757 | 41% | Quit flying role and moved to Adelaide. Great month for investments, websites producing serious income so accordingly they are valued higher. Spent a lot on furnishing the new apartment and on enjoying some more luxuries. Seeing a therapist to help deal with anxiety from leaving work. | LINK |

| July 21 | $1,543,959 | +$74,732 | N.A. | Set myself up in Adelaide. Did basically nothing for the whole month except spent time with family, relax, sleep and go to doctors appointments. Massive boost to website portfolio AdSense and affiliate incomes, as well as general share market performance. | LINK |

| Aug 21 | $1,624,116 | +$70,156 | N.A. | Relaxed again, focused on mental and physical health, and spending time with family and my partner. Big increases to spending (too afraid to calculate a ‘savings rate’) but also big increases to NW through website portfolio income growth. Finally got the slab poured on the investment property (foundation). | LINK |

| Sep 21 | 1,640,663.85 | +$16,547 | N.A. | Stocks, super etc went down, but business income from websites increased, plus business valuation increased. Property build. got to frame stage, and I also got a dog! Expenses for vet surgery well worth it. Moved into a nicer apartment | LINK |

| Oct 21 | $1,705,907 | +$65,243 | 30% | Big boost from website valuation due to securing new affiliate contracts for recurring income, shares went up nicely. No massive changes to this month. Calculated a savings rate and found myself pretty low due to spending a lot on my garden and going out quite a lot – I don’t think I will calculate this savings rate figure any more. | LINK |

| Nov 21 | $1,739,144.23 | +$33,236 | – | Great month. Relaxing (somewhat). Spent a lot of money doing ‘fun’ things like winery tours, a fine dining experience and self education. Shares moved sideways (well slightly down) but everything else went up. Building got to enclosed stage (roof, walls, windows and doors) but have had some issues with build quality and weather / covid delays. Put a $1000 deposit on the puppy. Stopped tracking Savings Rate. | LINK |

| Dec 21 | $1,764,516 | +25,372 | – | Spent nearly the whole month with family, did some work on the website portfolio. Traffic recovered from google algorithm changes. Invested $10K into Stockspot and Sixpark, $1K into ACDC, $100 into Comsec pocket and $100 into Bamboo, $260 into BTC, $4K into ETFs through pearler. Paid the $3000 balance for the puppy. | LINK |

| Jan 22 | $1,826,633 | +$62,117 | – | Stock market slightly down, Massive boost to website traffic (overall its more than doubled). Invested $10K VTS, 2K VEU through pearler, Paid for Angels cancer surgery, bought more BTC and ETH, bought a parcel of ETHI on commsec pocket. | LINK |

| Feb 22 | $1,757,210.57 | -$69,422.93 | – | Stock market down, Website business revenues down and additional spending on content and staff for business, Additional property development bills, some unexpected expenses, Wrote down the value of some of my personal property (and gave stuff away). | LINK |

| Mar 22 | $1,701,410 | – $55,799 | – | My last ‘regular’ monthly Net wealth update as I give notice at work and finish up my non-flying job. | LINK |

| Q3, 2022 | Over $2M | N.A | – | Six months of Early Retirement in Rest mode! I stopped tracking my net wealth post-FI, my dog passed away, I gave away most of my physical stuff and moved to become my mums live-in carer, met a lovely girl, bought a puppy. Had some incredible months with semi-passive website income but overall neglected the business and regular (stable) revenues decreased. | LINK |

| Q1, 2023 | Over $2M | N.A | – | One year of Early Retirement! A lot of (sad) changes, the passing of my mother and family feuding resulting in temporary homelessness, selling my ‘nursery’ of plants, and traveling overseas for a few months. Finding a new home to settle, couple of domestic trips flying to Tasmania and Queensland a couple of times, and plenty of camping and road trips within SA. Did not work much on the business at all and lost a few more contracts and had to cut staff. | LINK |

| Q2, 2023 | Over $2M | N.A | – | Getting back on top of things with podcasting and blogging more regularly. Focusing on building our ‘rich life’ and deliberately increasing spending in areas such as food, travel and convenience. Did a few interviews and went on a few podcasts. | LINK: CaptainFI Q2, 2023 Net Wealth Update |

| Q3, 2023 | Over $2M | N.A | – | Big focus on health and fitness, fixing diet and losing excess weight. Continue to sell a few websites from portfolio and focus on largest ones. Attended some FIRE events and lots of road trips | LINK: Captain FI’s Q3, 2023 Net Wealth Update |

| December 2023 | $2.26M | N.A | +$260K (21 months since last calculated) | Interim calculation due to share sales prior to purchasing property – no update published | No update published |

| Q2, 2024 | $2,417,426 | 12% – Calculated to see where we sat | +$157,426 (6 months since last calculated) | Mid year 2024 Net Wealth update. Sold shares, crypto and 5 websites, Purchased the farm in Queensland, received $250K inheritance, significant cost in setting up the property. | LINK: Captain FI’s Q2, 2024 Net wealth update |

| Q3, 2024 | $2,485,000.00 | N.A | +$67,574.00 (3 months since last calculated) | Q3 2024 update. Lots of spending on wedding and bought a boat, preparing to debt recycle. Properties saw great paper gains. | LINK: Captain FI’s Q3, 2024 Net wealth update |

| Q1, 2025 | $2,482,000.00 | N.A | -$3,000 | Q1, 2025 update. Write down of business valuation due to reducing income. PPR valuation estimate down, IP up. Slowly paying off debt. Farm life is great! | LINK: Captain FI’s Q1 2025 Net wealth update |

| Q2, 2025 | $ 2,431,487.00 | N.A. | -$ 50,513.00 | Q2, 2025 update. Property prices up, continued to pay down debt, some big spending: household help, fencing, retaining walls and chicken enclosure projects, bought second car, paid for international trip and 3 x domestic trips. |

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.