Welcome to 2021! Even though 2020 was a crap year, I did have a pretty amazing year financially, gaining nearly $300K on my net worth progress due to a combination of earned income, side hustles, investment returns, business growth and manufactured equity on the property development build (which continues to prove tedious and expensive in terms of short term cash flow).

January update

January has been a bloody tough month for me. Especially having to set alarms to go to work for the first time in six months – I did not realise there was a 5AM in the morning! I’ve been getting put through my paces in the simulator training section, and to be honest some of it has been a bit of a struggle. I have scraped through a couple of simulator assessments by the skin of my teeth, and will be conducting the first few of my route checks in the actual aircraft soon.

My dad’s health has continued to deteriorate, resulting in another major surgery which unfortunately ended with him losing a leg. I don’t know what is going to happen to the farm, but one of the properties up the road from dad’s was looked after by a bloke with one leg for nearly ten years before he finally fell of the perch. However if he dies, the property thing will be a nightmare (I am from a large family and my dad has had multiple marriages).

Mum’s chemo treatment has continued, which is pretty heartbreaking to not be home for. We have been calling and FaceTiming every few days to stay in touch, but I truly wish things were different and I could be there. The more I think about it, the more I contemplate whether I should ‘pull the pin’ on my career and FIRE earlier than planned. Of course this exact thought coincided with my seniority increment date meaning an $8500 payrise to try and tempt me into staying in my job.

I’ve continued to see a therapist about work, family and finance, which has been really awesome to help get some perspective. I have also gotten some great calming techniques – so if anyone is having issues with stress or anxiety, then there are a heap of awesome techniques you can use. Personally, some of the things I’ve found effective have been:

- Cutting back majorly on alcohol consumption

- Ditching the caffeine (this was hard since I relapsed and had to go cold turkey again)

- Putting my phone in the bedside drawer at 9pm to try and help with sleep hygiene

- Ditching junk food and going back to a mainly plant-based diet

- Breathing techniques (4/7/8 method and belly breathing)

- Visiting the physio twice a week (to help manage neck/back pain from a work injury)

- Reducing my gym training weights, but increasing the number of reps and intensity

- Aromatherapy with oil diffusers

- Soaking in the spa bath at home

- Reducing screen time and working out / running without music (this one was a bit of a shock to me, but the psychologist said that a brain that is continually stimulated with screens, music, loud noises, vibration etc is one that is harder to relax and unwind – give it a go!)

- Stopping obsessively tracking my expenses (instead I am loosely tracking my investments once per month for these updates)

On the finances side of things, this month I finished my experiment with Apple shares. I ‘killed my darling’ to take a ‘nice’ 10% profit (14% capital gain less 4% currency loss on the USD to AUD front) and then shoved it into index funds.

But how did that actually work out?

- AUD $1000 transferred through SelfWealth turned into USD $725 – fee USD $6

- Bought 6 APPL shares for USD $683.34 – fee USD $9.50

- Sold 6 AAPL shares for USD $801.36 – fee USD $9.50

- Exchanged USD $824.21 for AUD $1,056.10 – fee USD $5

So what was my profit? In the end it was AUD $56.10 (USD $43). It started at USD $118 in terms of the actual trade profit – which should have been AUD $153.

After factoring in USD $19 of brokerage (AUD $25) since SelfWealth didn’t let me use my free trades for US trading, $11 in currency conversion fees of 60 basis points (0.6%), and then a currency fluctuation of USD $45 (strengthened Aussie dollar), I actually walked away with USD $43 profit, or about AUD $56.

Now I am liable to pay full capital gains tax on this event – roughly $20 or so. So my net profit is $36, and an accounting nightmare, for about an hour worth of work. Bottom line – don’t bother stock picking or trading shares – it is a total mug’s game and most of the time you lose money.

Monthly question from the Captain

Have you tried micro-investing? Do you think it’s a good way to get started investing or a waste of time?

Last year’s tax return

Finally now that I am back home I have printed my Sharesight tax summary for the 2019-2020 financial year and have handed this to my accountant, along with a shoebox full of receipts and various demands about how much money I want back… lol. Fingers crossed it works out. I am hoping for $5,000. If I get this money, I’m going to be putting it all into the property development as there will be some large expenses coming up soon.

Saving rate: 79%

My saving rate across all of my accounts was 79%. I shifted my focus away from unhealthily trying to maximise my savings rate, and I am now loosely targeting a 75% rate (versus 85%) which I feel removes a bit of extra pressure for me. As I mentioned earlier, I have a lot of stressors at the moment, and one thing a therapist suggested was that I didn’t need to set myself additional significant goals and introduce financial pressure. So I am dialling it back a bit.

Income

Income was back to my healthy pre-sabbatical levels (it was starting to get a bit tight towards the end there!). Income consisted of my regular flying wage, no allowances (no trips until I am line checked!), website income and dividends. Due to seniority incrementation my wage went up by about $8500 per annum, which means about an extra $200 per pay after tax. My plan is to of course add this to my regular investment plans, and not inflate my lifestyle.

Spending

Spending was back to normal levels in January. A few big shops to re-stock my fridge and pantry as well as increased driving of my car meant I did spend a bit more than usual (for being at home), although it was reassuring to know I only spent around 21% of my income on rent, food and petrol. Included in this have been some fancy picnics and hosting a dinners to catch up with friends.

Investing decisions: $10,639

This month I invested $10,639 across the investment property, shares, micro-investing, P2P lending and the websites.

Using up some of the free trades I have with SelfWealth, I picked up 13 shares of VTS or $3,393 worth. This is great, because long term it represents a yearly effective salary increase of $339 (approx 10% long-term returns).

In terms of the FI portfolio, this is a yearly additional drawdown (at 7%) of $237, or $20 per month. Whilst $5 per week might not sound like much – remember my meal prep costs me roughly $2.30 per meal (luxe meals!) so this represents nearly a whole day’s worth of food (per week), or otherwise more than covers my monthly phone bill of $12.50. Such is the power of a low cost of living and regular investing!

For those following the blog, you will know I am slowly transitioning to using Pearler for my purchases of ETFs for the FI portfolio, and soon I am aiming to have this process fully automated with them using the auto-invest feature.

Property – $3,000

I paid $3,000 into the property project. This was my regular $1,000 mortgage payment, plus an additional $2,000 of buffer to cover costs such as fencing, rubbish removal etc.

Micro-investing – $200

I had lots of requests to review micro-investing platforms Stake, Raiz and Spaceship. I initially wrote these off as a waste of time however since completing the reviews I have seen the benefits of micro-investing for those just starting out. Of course I didn’t want to review anything without first-hand experience, so I am putting my money where my mouth is and have chucked $100 into both Raiz and Spaceship (Spaceship review coming soon!).

P2P lending – $100

I chucked in a spare $100 into my Plenti Peer to Peer lending account to start the ball rolling on this again. While the returns aren’t spectacular, it is a form of diversification, and I want to see how this goes long term so I can report about it on the blog.

Business – $3,946

$3,946 went back into the business. This month I invested in a bunch more awesome tools, anti-spam software, contractor wages and start-up funds for the company bank account. In my spare time I’m continuing to learn from Matt and Liz’s videos on the eBusiness Institute. The majority of the money is going into this website, followed by one other specialist site, and then the remainder is equally spread into three ‘starter sites’.

Financial Independence Portfolio

This is basically just exchange traded index funds and listed investment companies. In my mind, this is a ‘defensive’ asset that I am building as ‘insurance’ (ironic, given most financial advisers say that shares are aggressive) so that I can then go ahead and invest in other, more risky ventures such as the websites and property development (spoiler alert – probably avoid property development).

The aim of the Financial Independence portfolio is to provide a solid base of income to cover my cost of living from early retirement until the time I can get my annuity and superannuation benefits. Through a combination of dividend income and selling small parcels of shares (roughly 4% dividend income, and then to sell 3% of the portfolio value each year to supplement dividends).

The Financial Independence share portfolio is split across the two Australian CHESS share trading platforms that I use (the links below will take you to my dedicated review of each):

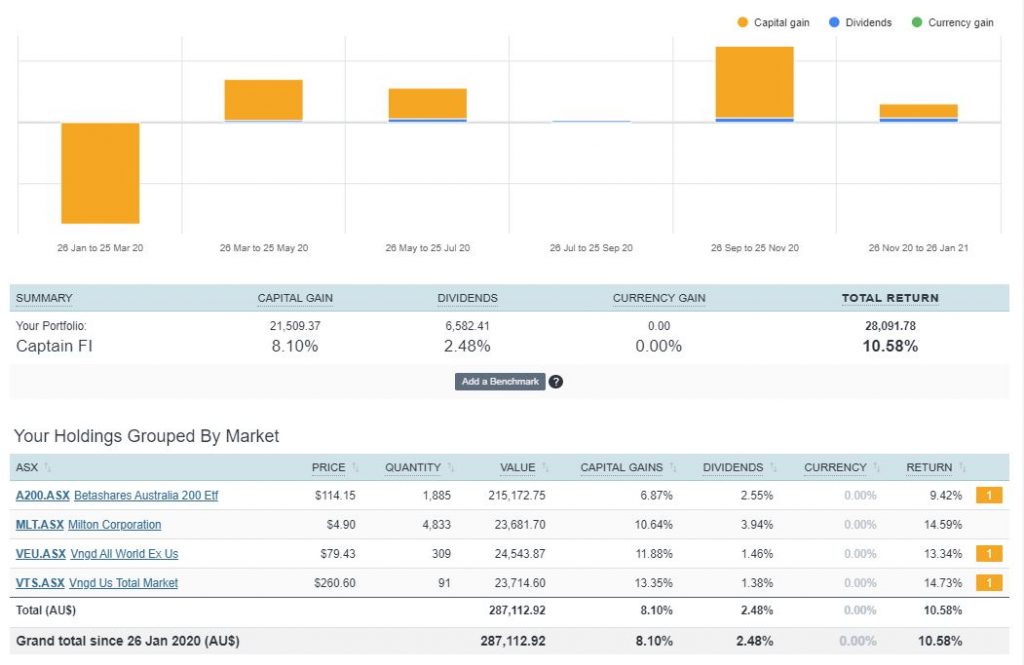

I track my share portfolio using Sharesight, which means my portfolio accounting is completely hands free. I have automatic trade confirmation emails set up with SelfWealth, and am using the API plugin with Pearler. This means I pretty much only need to log in to confirm all the trades and dividends over the year when needed for my tax return, and also to produce these monthly updates for you guys. The following section contains Sharesight reports for:

- Monthly

- Rolling 12 months

- Since inception (since I started tracking it with Sharesight)

I had some nice returns this month, with $1,503 in dividends.

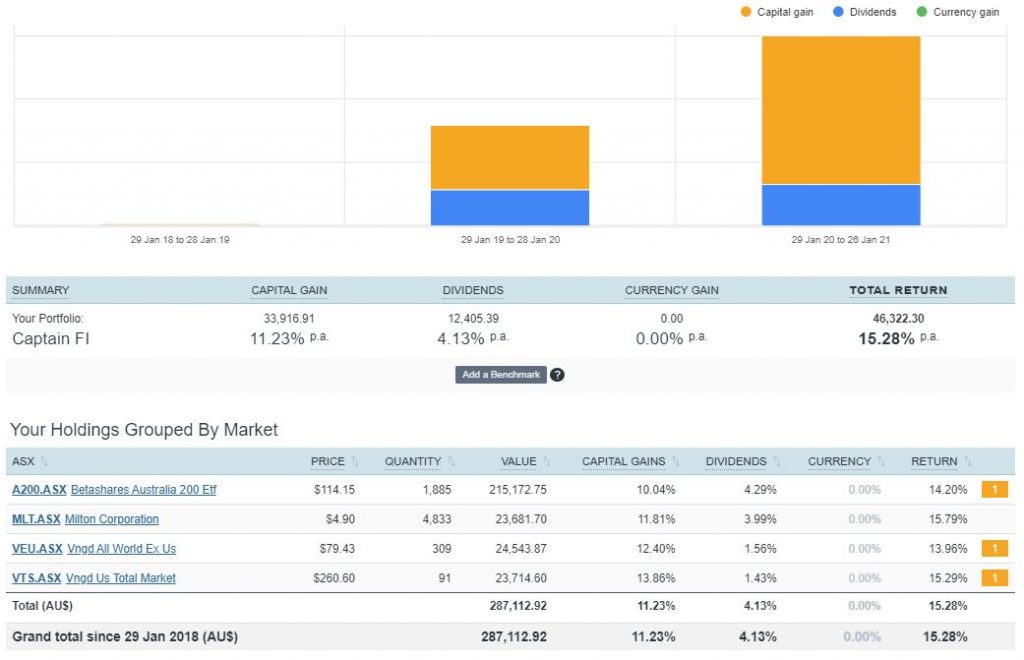

The rolling 12-month figure shows market returns roughly in line with the long-term average of around 10%. But what a wild ride it was in 2020! The figures show roughly 8% capital gain and 2% dividends – which I think is probably because dividends got cut due to the COVID issue (and this was mostly Australian banking dividends due to government regulation). I am sort of expecting the long-term dividend split to probably be closer to 4% and capital growth to be another 6% on top of that – but who knows!

This is the total return since I started using Sharesight to track my portfolio, and switched to a core holding of A200, VTS and VEU complimented by LICs (currently Milton). Don’t let the returns on this graph fool you – history is written by the winners here. What you don’t see is me underperforming the market prior to 29 Jan 2018 when I was trying to pick stocks. Overall I expect the long-term trend to be a bit less and closer to 10%, so I won’t be surprised if the markets pull back a bit.

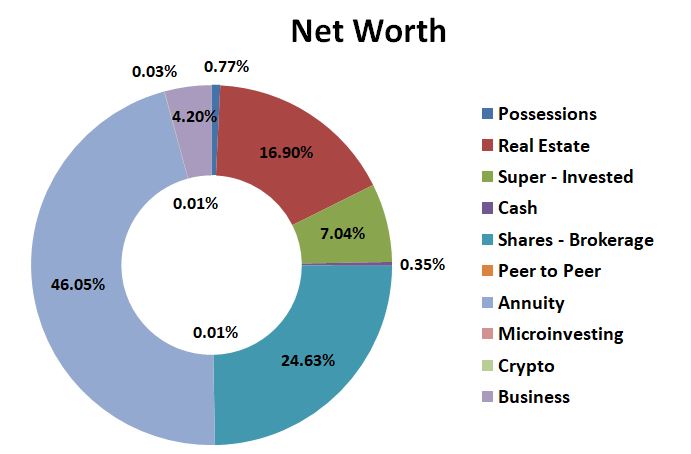

Pie chart

Because sometimes you just need a pie chart to visualise what the portfolio looks like. You will notice the removal of NDQ:AAPL (because I sold it) as well as NDQ:VTI which I have through Stake and have moved to the micro-investing section.

Investment property

Still waiting for DA, I am hoping this comes in February so we can start breaking ground. Otherwise, I just continue to throw money into the black hole of the ‘investment property’ and hope for the best. Does feel a bit uncomfy and wouldn’t recommend anyone does this unless they have experience or know what they are doing. It has been a huge source of stress/anxiety for me.

P2P lending

Earlier this year I withdrew all of my P2P funds from Plenti. This was because my budget was a bit tight and I needed to deploy those dollars. I also don’t really need any ‘fixed interest’ at the moment and if I am honest, it was more of an experiment than anything. I do like P2P lending because it gives me a higher interest that I would get from my online bank account, and investing in the long-term markets can actually be a way to create your own income stream.

My total balance with Plenti is AUD$100.

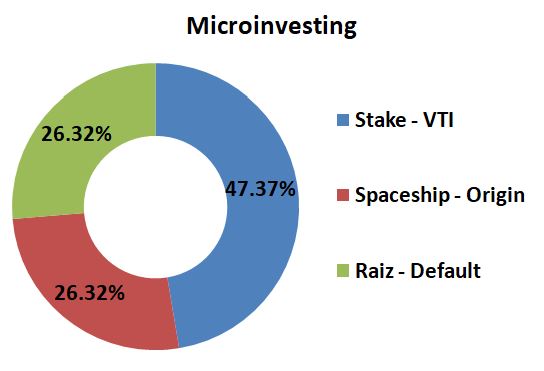

Micro-investing

This is how my micro-investing portfolios currently stand:

USD$110.90 (about AUD $145) invested in NDQ: VTI which is the total US stock market index ETF

Raiz – Microinvesting

AUD$100 invested in the Raiz Default fund

Spaceship Voyager Microinvesting

AUD$100 invested in the Spaceship Origin portfolio

Business

This has been a hot topic and the source of some great debates over the past few months since I let the cat out of the bag. I also wrote a dedicated article about how I make money online, as well as interviewing Matt and Liz Raad from the eBusiness Institute on the CaptainFI podcast about online business and how I started and am growing mine.

I have created a separate company to hold the websites, and am working to untangle the mess of personal vs business expenses. This will make tracking my net worth a bit easier I think, and makes everything nice and clear from a tax and accounting point of view. Currently I am paying for lots of stuff out of my own pocket which is making it a bit tricky to track everything. A 6-month goal of mine is to have every expense shifted over to the company account and not coming out of my name, and then when I am ready I can take dividends out of the company.

Currently I am spending a lot more on the business than it is making, but this is pretty normal with a new business. The revenue fluctuates a bit and I did get worried I might have overcapitalised or ‘stretched myself’ when the revenue dropped a bit over Christmas, but it is starting to recover. I think it will recover to a strong positive cashflow in 3 to 6 months, and I’m happy with that. A big part of these expenses is automation and outsourcing, because I just cannot continue the current trajectory of doing everything myself (especially as it expands).

Cash and emergency fund

Ok so confession – I don’t really have an emergency fund. Due to cashflow issues recently I boosted the amount of cash I keep on hand to just over $4,100, but this is basically just in my checking account earning practically zero interest.

Thanks to compassionate leave I have about 3 months of leave on my balance. Since my savings rate is on average north of 75%, this means the 3 months of leave effectively represents 12 months worth of living costs. This is a massive backup / buffer and is the main reason why I don’t keep a huge emergency fund of cash right now.

Secondly, I have nearly $300K in ETFs sitting in a brokerage account which I can access at T+2 days after sale. So I am not concerned about liquidity and know this alone could keep me going for at least 10 years.

Further to these two points, I have more than adequate income protection and TPI insurance through both my superannuation and the union, so in the event of a temporary accident/illness/injury or dismissal I will have a couple of years worth of income (albeit reduced to my normal wage and obviously no allowances).

In the event of a permanent impairment I will get something like 80% of my normal wage for the rest of my life (which is WAY WAY more than I would need able bodied, but still more than covers worst case a high-need care facility).

If you have high debt or rely on your PAYG wage to pay the bills, you would be crazy not to have income protection and TPI insurance.

Retirement

I am still working toward my ‘Family FIRE’ goal of $6,000 per month (after tax). When looking at the future trust structure, to earn $6,000 per month after tax it will more or less take $6,800 of gross portfolio income. Conservatively I am sitting at around $3,500 out of the $6,800 passive income goal, or over halfway to ‘Family FIRE’!

At the advice of my therapist, I’m going to distance myself from that goal. It is still there, and I am still working towards it, but for now I am going to congratulate myself on smashing my ‘Single FIRE’ goal of $2,000 per month. Sure, I would love to meet someone special and start a family, but I’m taking the pressure off myself and giving myself time to just enjoy the rest of my 20s without constantly eyeing off Kia Carnivals and bulk baby food specials. 🤣

Reflecting on the fact that I am now Financially Independent and worst case if I lose my job – it doesn’t actually matter, has been an important revelation for me and my mental health as I go through my return to work package. I think I am sometimes my harshest critique and put a lot of pressure on myself.

It is worth noting though, I am not actually taking any money out of the business (or my share portfolio for that matter). I am reinvesting this money to grow this revenue stream faster to secure Financial Independence sooner – as you can read my dedicated transition to retirement financial planning process article. I am actually doing the opposite with both, and investing significant amounts into each.

However, as a good quick and dirty, I plan to live off a 7% draw-down of my Financial Independence share portfolio (4% dividend and 3% selling parcels of shares each year) from when I choose to start early retirement, through to when I am eligible to receive my superannuation lump sum payment and my annuity starts paying me.

So how do I value my superannuation? Well it is an interesting topic and up for debate (let me know your opinion!).

The invested portion is super easy – it is literally just all invested in shares (Australian and international shares) in index funds. If I contribute nothing more and let it tick away, I will have just under $1M by preservation age. To get to the $1.6M cap, I could either stuff in another $50K to super right now, or closer to $70K of contributions over the next 2 years or so (which I am on track to do and reach before FIRE thanks to compulsory 9.5% wage input).

My annuity component is a pension that is indexed to CPI for life, and it is a bit trickier to value. The Australian average male life expectancy is 82 years, and I think I can eke out a few extra years based on my health and lifestyle habits of weightlifting, cardio exercise, a (mostly) plant-based diet, minimal alcohol consumption and yearly comprehensive medicals. I think at least 30 years of the annuity payments is a safe bet. When I looked online and got some quotes for this, the prices ranged from 25x to 30x annual payments. Interestingly, the Australian Tax Office values my annuity income stream product much less than this, and I am not sure if this is counted towards my $1.6M super cap or not.

I therefore conservatively value my annuity at 25x annual payments, which coincidentally is also in line with the 4% rule from the Trinity Study regarding investment portfolio balances and retirement.

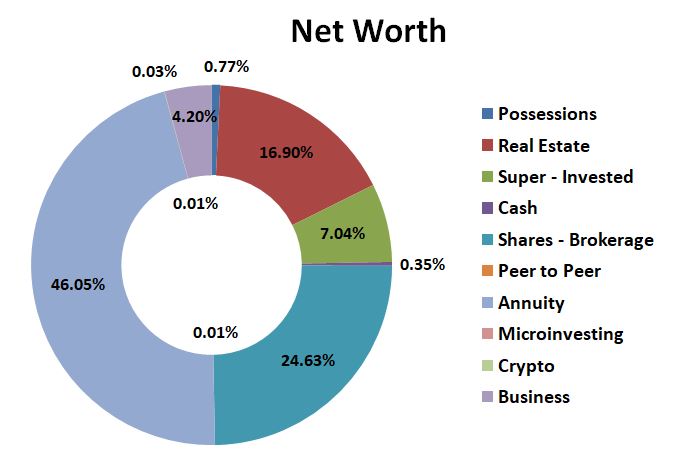

Captain FI net worth Jan 2021

The net worth pie chart is a great visualisation of my total financial portfolio breakdown. Weirdly enough, these splits seem to stay roughly the same, despite each sector growing at a different rate (bearing in mind these are rounded up to the closest percent for ease of visualisation). I have added the sectors ‘Micro-investing’ and ‘Crypto’ as I am now opting to take a very small holding in each.

Captain FI net worth progression

Tracking your net worth over time is one way to monitor and compare your progression to FIRE. A better way though, is to track your passive income – such as dividend income. Because that’s what you’re going to be using to live off if you do choose to retire early.

Because of how I have my finances structured as an Australian investor with a significant amount invested in superannuation, my net worth number isn’t really all that reflective of my ability to FIRE, but I still think it is an important metric to track since its growth is representative of performance – the rate of change of net worth is more important than net worth by itself, in my opinion.

Eventually, I will produce a second graph below which will track my passive income over time – something I don’t have data on (except for perhaps going back over these blog posts maybe).

CaptainFI net worth progression – graph

The net worth progression graph is rather crudely constructed in Excel, but still demonstrates the ‘somewhat exponential’ journey over the past 12 years.

CaptainFI net worth progression – table

To finish up this post, here’s my net worth table, which provides a bit more information on my journey for anyone wanting to go back and see how individual years or months went at a quick glance.

| Date | Net worth | Difference | Saving Rate | Notes | |

| Jan 09 | $5,000.00 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK | |

| Jan 10 | $24,000 | +$19,000 | ? | Estimate NW | LINK |

| Jan 11 | $40,000 | +$16,000 | ? | Estimate NW | LINK |

| Jan 12 | $92,000 | +$50,000 | ? | Estimate NW | LINK |

| Jan 13 | $130,000.00 | +$38,000 | ? | Estimate NW | LINK |

| Jan 14 | $161,000.00 | +$31,000 | ? | Estimate NW | LINK |

| Jan 15 | $200,000.00 | +$39,000 | ? | Estimate NW | LINK |

| Jan 16 | $281,000.00 | +$81,000 | ? | Estimate NW | LINK |

| Jan 17 | $340,000.00 | +$59,000 | ? | Estimate NW | LINK |

| Jan 18 | $482,000.00 | +$142,000 | ? | Estimate NW | LINK |

| Jan 19 | $542,000.00 | +$60,000 | ? | Estimate NW | LINK |

| Jul 19 | $578,900.00 | +$36,900 | 84% | Finally began tracking NW this like a proper adult. | |

| Aug 19 | $560,100.00 | -$18,800.00 (-3.2%) | 78% | Share market slight correction, Ok savings. | |

| Sep 19 | $584,744.88 | $24,644.88 | 72% | Share market rebound, savings rate not so good. | LINK |

| Oct 19 | $600,386.00 | $15,641.12 | 84% | Good saving this month. Normal salary, plus allowances, dividends from index funds, tax refund, eBay selling and was working abroad in asia where things are cheap. | LINK |

| Nov 19 | $612,917.21 | $12,531.21 | 76% | Falling short of my savings goal of 80%. Mostly domestic legs this month with higher costs. Also invested in hydroponics. | LINK |

| Dec 19 | $625,350.00 | $12,432.79 | 76% | Good savings of cash (for development) and investment, however higher spending due to Christmas period (Travel and Gifting). | LINK |

| Jan 20 | $865,212.00 | $239,862.00 | 55% | Super settlement was a HUGE boost to NW. $9K growth from stock market. Expensive month lots with lots of unexpected bills – weddings, travel, Booking flights, fines etc. | LINK |

| Feb 20 | $851,802.0 | -$16,592 (-1.9%) | 52% | Large increase in spending on myself this month, still managed to tuck away $5K to put into shares and property. Corona Virus market scare resulted in a correction and gave NW a small negative trend. Time in the market not Timing the market! Became Single again. | LINK |

| Mar 20 | $819, 354.6 | -$31,806.95 (-3.7%) | 80% | Another small step backwards in the NW due to the ‘corona crash’ in full swing. FIRE Portfolio of ETF/LICs down about 15% this month, however due to high savings rate and structure of my superannuation annuity the NW is only down 3.7%. Savings rate good at 80%, higher than usual income (with some slightly higher spending, too). Picking up shares on discount – this is the best outcome for someone in the accumulation phase with good income! | LINK |

| Apr 20 | $847,023 | +$27,668 | 85% | $11,000 in rebound of stock market capital prices alone (up 6%), plus first quarter dividends paid (heavily reduced due to banks withholding dividends). Great savings rate due to COVID-19 lock-down = no spend. Increased entrepreneurial efforts and selling down of physical possessions provided side hustle income. Two standard paychecks from flying activity; domestic day trips only so no allowances. All cash unfortunately had to go into the property development due to contract timing, I am chomping at the bit to buy some more index funds before they go back up in price too much – hence why I am selling most of my toys! | LINK |

| May 20 | $857,859 | +$10,836 | 92% | Some Great sales as I let go of my Super Sport Motorcycle, Some gym gear, expensive flying equipment and a few other various bits and bobs and invested this money. Flying still reduced, but increasing from April. The share market grew as I continued to make my fortnightly investments. I also wrote down the ‘value’ of some of my possessions (liabilities) such as my car, tools and furniture by around $10K to align them to market price (“tell him hes dreaming…!”). | LINK |

| June 20 | $858,650 | +$791 | 90% | Small Net Worth gain as I continue to declutter and simplify my life, despite being off work due to a family emergency. Share market not doing much. | LINK |

| July 20 | $888,218 | +$29,568 | 68% | Majority gain due to share market going back up, low spending due to being on the family farm and at home because of lock down. | LINK |

| Aug 20 | $1,029,293 | +$141,075 | 74% | Became a millionaire. Achieved this massive milestone I set out for myself in Dec 2019. Included unrealised gains in my property development as well as website business. Good savings rate due to not much spending, invested in Aus and total world shares. Investing in my web business. Starting to shift focus away from $$$ and more into looking after my mental health. | LINK |

| Sep 20 | S1,045,486 | +$16,193 | 60% | Officially took time off work for the rest of the year to be close and look after family during major operations. Continued to sell down physical possessions and work on digital business while at home. NW gain mainly due to valuation of websites. | LINK |

| Oct 20 | $1,064,399 | +$18,913 | 80% | Base income (retainer) and leave loading, dividend and websites provided income, as well as raiding my P2P lending capital. Significant bill for property due to design not meeting standards which effectively lowers my equity position, as well as fence being stolen. | LINK |

| Nov 20 | $1,143,433 | +$80,394 | 82% | Big gains came from share market growth (influencing both the Financial Independence share portfolio and Invested superannuation), Business gains (due to increased earnings) and a $30K boost to my annuity thanks to me logging in and checking the fine-print on the accumulation stats. I only invested around $7K. Insane that in one month, I accumulated nearly more net worth than I did in four years from 2009-2012 | LINK |

| Dec 20 | $1,152,920 | + $9,487.32 | 84% | Share market slight drop, Earnings from Business, Contract work, Selling possessions. No share market investments this month (oops! I forgot and money was tight). Invested a lot into the website business this month (way more than planned) and it is still running at a decent loss (plans to turn it cash flow positive in 3 months). | LINK |

| Jan 21 | $1,165,678 | +$12,757 | 79% | Great returns from the share market. Earnings from Business, Dividends, Flying wage, flipping items on consignment. Regular share contribution, investing in micro investing platforms, P2P lending, Investment property and big reinvestment into the business (still running at a loss) |

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

I’m interested with your ETF mix between Australia and international. I see you go with a 75/25 split whilst a lot of reading I do suggests to go the other way as Australia’s market is only about 2% of the world market. Just interested in your thoughts with that

Hey Matt. Very good pick up mate. I have to be honest here – Massive home bias initially as I took on big home risk to get more dividends and access to franking credits to try and build a baseline level of dividend income to live off. Thats just why I went hard with the aussie funds first. The more efficient way is definitely to go global in ‘high growth’ assets so you dont get dinged for tax on dividends. Also, you are correct its way safer to be the opposite way around. Going forward, my end state will look something like an equal weight core portfolio of 1/3 A200 1/3 VTS 1/3 VEU, and then some satellite investments elsewhere. So i am looking to invest in more VTS and VEU going forward

Hi Cap,

Do Franking credits make much diff in your income levels?

Can you explain more about the annuity, as that makes up a large chunk of your portfolio?

Awesome savings rate

G’day Baz. Yes I find the franking credits useful as it means I dont get whacked with tax when I do my tax return as a result of the dividends I get paid (about $15,000 a year currently). Because I am taxed higher than the company rate (27%) I have to pay a small ‘top up tax’ on the difference. As for the annuity, it is a defined benefit fund style arrangement – essentially I continue to accrue experience with my employer then the value of the defined benefit (the annuity) goes up. Basically its like an old school retirement scheme, when I reach my preservation age the annuity will start paying out. I value it by multiplying this annual payout value by 25 (similar schemes are available for purchase but they cost around 30x annual payout, so i figure this is conservative). I also have a standard invested super scheme too (index funds 100% shares), but I track this separately.

Hi mate, I am a finance student so reading your blog is very interesting and fascinating. I would like to invest $1000 in one index fund through Selfwealth. Which fund would you choose? My aim is to see how things work and move, I still don’t have an investing strategy since i’m flogging my mortgage and should be done in 7/8 years. Thank you 🙂

G’day Chiara, Hey thats awesome mate. Appreciate you stopping by. Perhaps you can run my ‘strategies’ past your professors and see what they think, about my levels of risk and diversification. In response to which fund you should pick… mate thats the $64,000 question. It would be irresponsible for me to just tell you a fund, but if you are just interested in seeing how things move, I think getting some skin in the game is a great idea – and why I changed my ‘wealth steps’ to include micro investing. If I was you and just wanted to test out for research, I would probably pick a few different ETFs and see how they compare against each other. Think hard about what exposures you want etc, and your timeframe… Personally I go with the A200/VTS/VEU split and I am targetting an equal 1/3 weighting (Obviously I am massively overweight A200 currently). I am also shifting away from LICs and more into just ETFs. A good one size fits all is these new ‘diversified high growth funds’ like VDHG and DHHF, I have a review on VDHG and another one on DHHF coming out soon. Do some reading and see what conclusion you come to. Good luck with it all – let us know how it goes.

Sorry to hear of your family’s struggles! Hoping everything turns out OK!

Great article as always, super detailed. Was interested to read about you jumping back into the P2P lending space. That’s something we haven’t really looked at so we’ll be interested to hear how it goes!

Thanks guys… its been a bit of a rough patch, but I am still super grateful for all the wonderful things in my and my families lives. Everyone seems to go through these tricky times at some point. With the P2P lending, I would say its more of an educational experience for me. I pulled my money out earlier because I was desperate for a bit of cash and needed to use it for the business, some people swear by this stuff, but at the moment I am just using the rolling 1 month window – which yields not much more than a conventional bank account currently. The real juicy worm is the 5+ year fixed markets – its almost like creating your own annuity or ‘reverse mortgage’ for generating a nice level of baseline income stream – potentially similar to how a bond fund could be used I guess. I am still playing to get familiarised with how it all works, and contemplating chucking some in the long term fund. The only issue is committing large chunks of money at the moment isn’t something I want to ‘lock up’

Hi Captain. Thanks for this post. Well done on the psychological aspects. You’ve blitzed your single FI number (in fact almost doubled it). Little point (sanity-wise) busting your brains at this point worrying about funding a partner (who may have her own money) and children who don’t even exist yet. 😉

On the Apple experiment, I agree with your conclusion that stock-picking is riskier than funds. However, I don’t think your experiment is an example of that (after all, you picked a winner). Your experiment shows:

(1) why fees are a drain on returns – $25 brokerage and fees on a $1000 investment means you have to make a 2.5% gain just to break even (perhaps about 4% including currency fees).

(2) why it’s sometimes better to accumulate more savings to invest in larger chunks (the same brokerage fees on $10,000 would have been a mere 0.25% drag).

(3) why this sort of investment is suited to buy-and-hold. If someone holds for longer, the same fees would form a much smaller proportion of their gains (eg a stock that grows 30% over several years makes the one-off 0.6% currency fee insignificant).

(3b) Also the long-term investor can choose to sell at a time of a weak Aust Dollar, and use currency variation to increase their gain.

(3c) Longer-term (even just over a year) means a 50% capital gains tax discount. In your example, that alone would have increased your return from 3.6% to 4.6%.

Overall, I understand your reason for ending the experiment (just too many small things to manage and focus on). For the hassle it may not have been worth it (even though you had a ‘win’).

Sidenote: From a tax perspective, if you’re buying shares (or ETFs) it may worth considering holding them until you FIRE. If you’re looking at retiring in a couple of years, you may be in a much lower tax bracket at that point – making it advantageous to take your capital gains then, rather than now.

Thanks again for your post. You are amazingly open and vulnerable about life as well as the numbers.

G’day David, You bring up a heap of really great points – which for me personally all point to buying and holding long term, and I totally agree down the track there might be a much more optimised time to sell the stock. I probably just sold it early due to frustration lol. And Apple probably will continue to do really well, but I just wanted to simplify the holdings – thankfully I do have some exposure to the good stocks like AAPL within the ETFs I hold, but without the concentration risk of individual shares.

Appreciate the kind words and feedback too mate. I think I have been using the blog as a bit of an avenue to vent my frustrations lately, but I also want to set the context for my FIRE journey and share both the highs and lows. It is a really interesting and challenging journey and I see similarities with so many others on their paths to FI – so wanting to normalise the less than glamorous side of the house 😅