OK! So I have decided to go public, and include a net worth tracker on here to help document by way to Financial Independence (FI). Eventually I will get some nice flashy visuals, some pie charts and graphs – but for now it will just be some boring text and number based stuff.

My hope is that I can provide more transparency in my investing strategy, and lead by example for those wishing to follow along. I am also using this as a way to keep myself accountable for my actions, including budget overspends. And we all talk the talk about if there is a market crash that we will tighten the purse strings and double down on more investments, so lets see how I go when there is a downturn! Each month, I will be baring all detailing my financial decisions and overall financial health. This will include

- Get FI Portfolio breakdown: Whats in it, how it performed over the month and what the two fortnightly investment decisions were with my reasoning (plus any bonus investments made).

- When I settle on the property I will also include a paragraph on how the property is doing, what rental yield I am getting, how much it is cash flowing and what it is currently valued at, the outstanding loan and therefore my equity in the property.

- Superannuation: I will take the base figure I receive reporting on each financial year and simply add the payments which are made into it each fortnight. This will become the ‘lump sum’ figure, but its also important to note I have the option to take an ongoing pension instead which works out to be a draw down rate of around 10%. Its a no brainer to take the pension, as you just have to live longer than 15 years or so for it to work out – and I plan to live past 70. Also, the longer I fly for the company the larger this pension gets – although of course, FIRE is still the plan. In this respect, adding the lump sum figure isn’t strictly speaking the best measure of net worth, but rather than try to ‘inflate’ this figure onto the 4 percent rule, I will just leave it as is. I also don’t want to exclude it all together, as including it helps to communicate the unique two-phase retirement system in Australia.

- Income stream: Salary, allowances, side hustles and any dividends. Note I won’t be including any owed income or future benefits, this will purely be included when the cash hits my bank accounts. Also I KNOW its better to use the DRP and automatically reinvest your dividends. There is just something I love about seeing those dividends hit my account… free money! In all seriousness though I will be switching the DRP’s all back on for all of my ETF/LICs, so I will be accounting for those dividends as extra cash which got invested to boost the FIRE portfolio.

- My budget and expense tracking – how well did I stick to the budget. I will be including expenses as I pay them, and the money leaves my account.

- My two phase retirement base income streams. This will be based on the planned draw down of the Get FIREd portfolio over 25 years (age 30 to 55), and then the pension I will receive from my Superannuation (from age 55 onward), with no additional income. Obviously I will still be tinkering with projects and its unrealistic to say I won’t earn any future income other than these base amounts.

- Net Worth overview

Get FI Portfolio

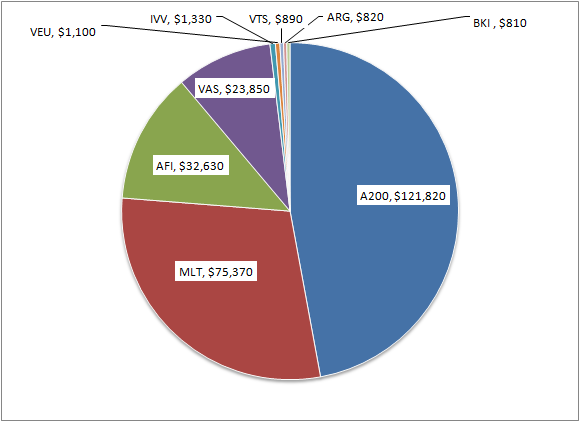

The Get FI Portfolio is now sitting at approximately $258,600. The portfolio breakdown is as follows (rounded to the nearest $10). When I get properly sorted I will use screenshots from SelfWealth to show its growth and performance properly, but in this financial year (since 1 July 2019) its sitting at a touch under 4% (capital growth + dividends).

Investment Decisions

I have added $3000 of investments to the mix in September with a mix of ARG, BKI and IVV – since I had some free SelfWealth trades left over I was happy to spread the money out across these two LICs and ETF. Both LICs were trading at approximately 3% discount to NAV, and the IVV was down about 1% the previous day and I managed to buy it on the dip and it has since gone back up by that fluctuation.

I did not follow my own rules this month! Argh! I needed some extra cash towards the deposit on the Investment Property development, so I skipped one of my fortnightly investment decisions and pocketed the cash directly into my high interest savings account (I also took the juicy dividends I received last month and stashed them there, too…)

Its for a good cause, and I will also be putting this years tax return into there too. All going to plan, this will lead to a cash flow positive rental property which should be well positioned for capital growth (although this and the tax depreciation aspect are both just icing on the cash flow positive cake for me)

Property

As I mentioned above, currently the property development is still under negotiations. As a rough overview, I am working on developing some Duplexes which I will retain as cash flow positive rentals. This will be done using my company within a trust structure using interest only loans and an offset account.

We are negotiating the land sale at the moment and are working through contract negotiations with a builder. Unfortunately its looking like I will need to sell a parcel of some of my shares to raise funds for a deposit for a conventional loan from a bank. I cant justify paying 15-20% to an unsecured money lender (P2P lending) and don’t really want to give anyone a profit share of the development at this stage.

So it looks like I am breaking my number one rule of buy and hold, and I am looking to sell off a parcel of my oldest holding AFIC *wipes tear from eye* as this will give me the lowest capital gains tax bill. Having held the shares for over 12 months means I will only pay 50% of the tax as I qualify for the capital gains tax discount. Thankfully the share market is doing pretty well right now, and I ‘doubled down’ during the latest market dip so I don’t really feel like I am selling at a loss (false confidence perhaps??).

Superannuation

OK – so first up I have two super funds. I know this is stupid and I have tried again and again to roll them into the same fund (ideally rolling the smaller fund into the larger one) however my employer wont let me! Grr ??. The larger fund is from my current employer, and the smaller fund is from my side hustles – money I earned from flying instruction, contract/seasonal flying as well as joy-flights and warbird adventure flights.

My little fund has about $18,900 in it, and its going backwards. YEP you heard it – its going backwards. The fees I am being charged are slowly eating away at the super, because it doesn’t get any ‘new’ money put into it to feed the fee machine. It will probably all get chewed up in fees over the next 5-10 years. This is because I do all my side hustles now as a contractor rather than as an employee so I don’t have to pay any of my wages into super, and I keep my tax until the end of the financial year when I do my return. If you can sense a rant coming on then you’ve guessed right, so feel free to skip to the last paragraph if you just want the bottom line on what my super balance is.

The fact that my little fund just keeps getting eroded away seriously pisses me off, especially in the wake of all the financial scams that have been brought to light in the wake of the recent Australian Royal Commission into banking (which was a massive joke by the way – slap on the wrist and the banking machine roars right back into gear). It just goes to show, that most Superannuation schemes are scams designed to suck fee’s and charges and provide unnecessary insurance to the working class.

Oh yes, I’ve tried ringing them several times to inform them my current employer fully insures me – I can’t change the policies on my little fund! What scares me is that if I ever need to claim, I’m SURE that this double up on policies will frustrate the legal process and provide some wiggle room for the insurers to scam me out of entitlements (because you always get paid the LESSER of your insurance entitlements if you have multiple overlapping policies).

I have seen a financial planner and tried to roll over my little fund into another super scheme (ideally a low fee index fund ETF based fund) however it would seem I am powerless to change it. The best I’ve been told is to just forget about it, and when it hits a zero balance they will close the account. I’m not usually one to give up so I have written to my local member of parliament. Unless something big happens, its probably gone through so I have debated whether or not I should even include it in my Net Worth.

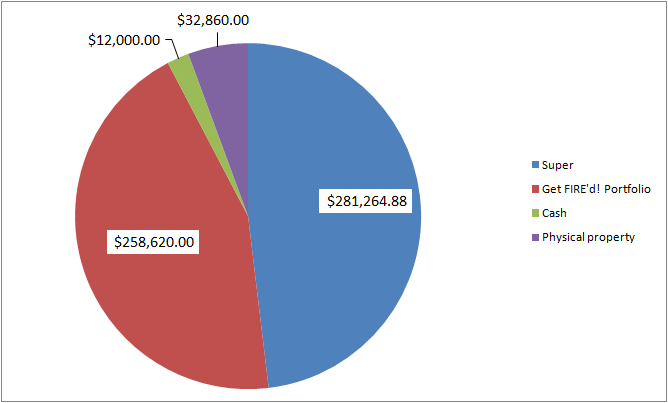

My superannuation ‘Big fund’ balance as stated in my official yearly member statement as of July 2019 was sitting at just under $260K. Between then and now, I received a decent promotion at work and as well as received the scheduled super benefit from staying with the company longer. The longer you stay in the more they pay into super, as an enticement to stay rather than say, jumping ship to an airline with higher pay. Although this is not an official figure, my calculations have the balance of my Super ‘Big Fund’ now at $281,200, ‘Little fund’ at $18,900 with a total balance of $300,100.

Income stream

Income for the month of September was fairly standard. I received my standard paychecks, and some of my allowances. We are having some issues with allowances getting paid on time, so I didn’t receive some of my overnight and meal allowances this month, but it all comes out in the wash eventually. I maintain $1000 in my checking (chequing?) account anyway to overcome this and any other ‘Lumpy’ bills. Side hustle income from eBay selling came in at $200, and I made nothing from T-shirt/sticker sales. I’ve stopped doing online surveys as it just isn’t worth the time, and I was paid about $40 in dividends from the portfolio. Revenue from Affiliate marketing and ad-sense from the website portfolio has been reinvested into the company to help pay for domain registration, hosting and paying for editors.

Budget and expense tracking

This month has had a few unexpected expenses on the social front. I spent a about $150 on food and alcohol on overnight work flights (which strictly speaking is EXACTLY what meals and overnight allowances are for), and $160 on tickets to a formal dinner and the pilots association reunion. Although I wasn’t really planning to spend this much, I was still glad that I did. I had a great time, caught up with some old friends, listened to some great stories from the older generation of pilots, had some good beers and I even won the raffle at the reunion. The prize was an incredibly detailed and sizeable scale model of one of the aircraft I fly – I’ve seen them on eBay for over $500!

I had a win this month on the groceries with a spend on average $26 per week versus a planned $40 per week. Part of this was possibly due to being away for work for a week. I don’t buy pea protein powder for post gym shakes anymore, which is why my budgeted spend went from $52 to $40 per week. Having said this, Last month in August I was at a slight overspend at $47 per week. I currently have my deep freezer well stocked with delicious home made frozen meals (breakfasts, early lunch, late lunch and dinners) as well as my pantry bursting full of cans of tomatoes, beans, lentils, containers full of different varieties of rice, oats and pasta, plant based milks and loads of other healthy snacks like rice puffs, nuts, chia seeds, pepitas, sunflower seeds and coconut pieces. My Fridge is full of fresh fruits and vegetables like potatoes, squash, carrots and baby spinach and snacks like hummus. I also have loads of condiments, herbs and spices to last me a lifetime. Definitely well stocked in case of nuclear war, which is probably excessive but kind of how I like it. I just slowly replace the things I need which keeps the kitchen stocked and the food bill below the budget.

This months fuel bill was reasonable coming in at $70, which is exactly what I budget for. Truth be told I could have filled my car up with an extra litre or two of petrol to completely fill the tank, but I actually had just sold something on an online classified so had $70 cash on me which I thought was convenient to use rather than having to deposit it at the bank. The $60 monthly direct debit also came out for monthly registration of the car.

Retirement Income streams

The following income stream calculations are an approximate of how much passive income I am expecting to receive as a base retirement income if I retired right now. Obviously I am still going to work on some projects in my retirement (such as web development, property development, property management and online arbitrage) so its unrealistic that this will be all I have to live on.

Get FI portfolio (up to age 55)

- 4% sustainable draw for ever = $10,400 per year ($866/month), or;

- 7% draw down over 25 years = $18,200 ($1516/month)

Superannuation (age 55 onward)

- Super pension / retirement benefit = $7,980 ($665/month), and;

- Australian govt means tested Aged pension = $18,122 ($1510/month)

Net worth

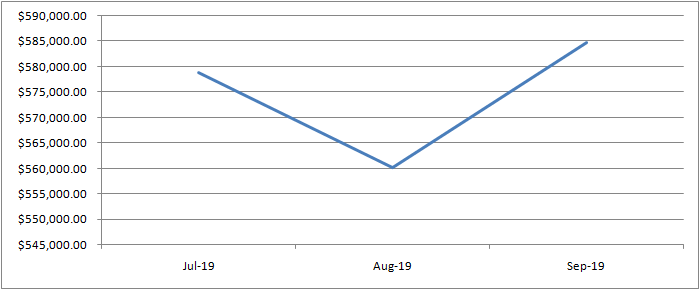

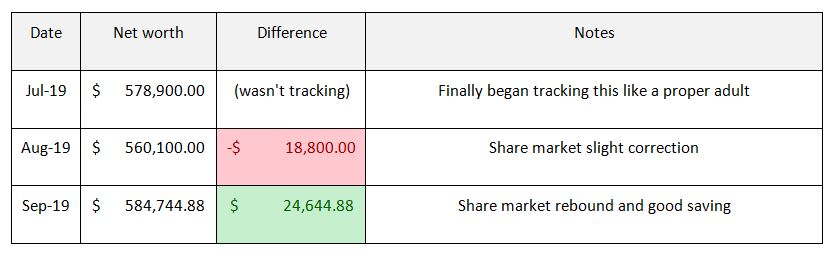

At the end of August 2019 my net worth was approximately $560K. At the end of September, it is now approximately $585K. The jump of $25K was mainly due to share market fluctuations which dropped the value of the get FI portfolio in August, and of course the ongoing contributions from my wages.

I am including the value of my vehicles (station wagon, trailer and sportsbike), specialist equipment (flying helmet, headsets, electronic flight bag tablets etc) and tools because they are significant expenses which are linked to my employment, and may be sold or replaced with a decent amount of cash changing hands. These are listed as ‘physical property’ which is the best name I could think up at the time.

I am not including any of my smaller household items like electronics (desktop, laptop, phone, personal tablet etc), furniture, appliances or clothing because its just too hard to factor it all in, and they don’t really have any relevance to a FIRE discussion once they are already bought.

Conclusion

There is is! my first net worth update. Sorry its not as flashy as it could be, but I will be working to add some better visuals such as pie charts and graphs, as well as some screen grabs from SelfWealth to give you a better appreciation for how the Get FI portfolio is tracking.

I hope you got something out of it and it helps you towards FIRE and developing your very own Get FI portfolio! Let me know in the comments below if there is anything you need clarifying or want me to include for Octobers update. Cheers

Get FI !

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Great post, I love reading it. One thought on your small super fund, since you are taking a sabbatical are you able to withdraw any of the money due to Covid? Just a thought?

Hi Mel, thanks! Yep the super withdrawal scheme is something I have considered

Hey Captain

I loved reading your post. I have created a personal finance blog myself and it really motivates me looking back through your early income statements seeing how little you earned compared to how well your blog is going now.