Just shy of $2000 in dividends was an awesome start to the year, but through predictions of doom and gloom and market crashes, I have continued to do the same thing I always do which is to slowly invest what I can afford into the markets. I bit the bullet on launching over a dozen new content websites to add to the website portfolio, enjoyed spending time with the newest addition to our family, and nursed my dog back to health after she had major cancer surgery. I’m still struggling to get to grips with the fact that my parents are going to die, and it’s been really shit watching their health deteriorate further this month.

CaptainFI is reader supported, which means we may be paid when you visit links to partner or featured sites

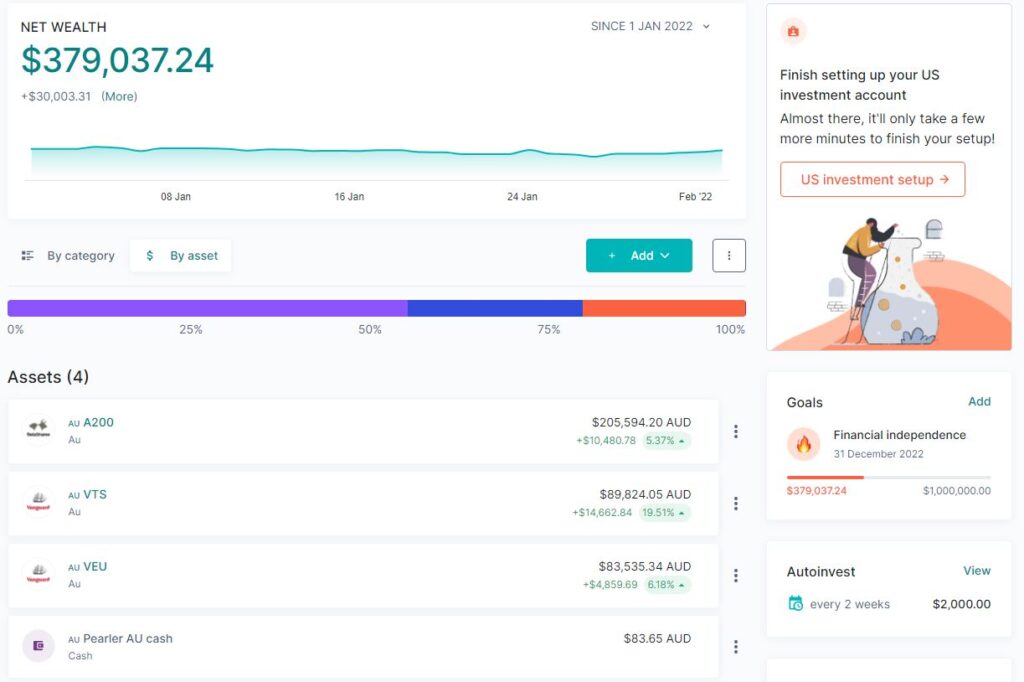

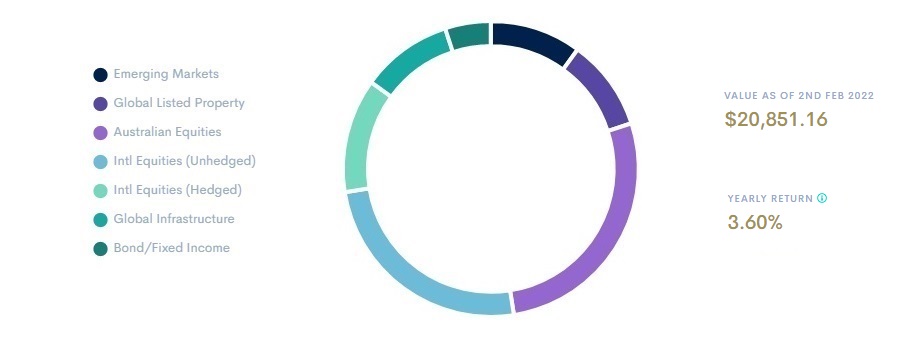

CaptainFI Total Net Worth

CaptainFI Financial progression

CaptainFI personal update: Early Retirement?

I actually write these articles in reverse, starting with the financials, and then I finish up with some photos. Its actually taken me most of the afternoon to write this article so far with all the new graphics so I am going to keep this section brief. Before we get started though, if you really like this personal segment then consider subscribing to your preferred social media feeds because I publish pretty regularly what I am up to, as well as share links and information I find interesting

January was a month full of both happiness and sadness for our family. We got to spend a lot of time playing with the puppy as she grew ever-increasingly more confident, and she has already doubled in size to 5kg (12 weeks old) and is ready for her vaccinations and puppy training.

I accepted that the cherry tomatoes had finally done their dash in the Sky Garden, and it was time to take them out. Slowly I pruned them back and mulched them up to use as a mulch in the 200 grow pots I have on the balcony. I like this idea of ‘chop and drop’ as they just molder down and turn into soil, providing food for microorganisms and fungi which recycle the nutrients to the next crop I plant. Plus the worm warm was full. It’s hard enough getting soil and plant matter up onto the roof, so I am not going to waste it when it’s finally up here!

I also taught my nephew some valuable business skills harvesting honey. It was a great haul for the little fella – approx 24kg of honey. We sat down with a plan to be able to sell it for about RRP $400 as ‘premium organic backyard honey’, so he’s hoping to get $270 selling it “wholesale” as one big batch to a local shop. This pays for his equipment ($190 – $60 second-hand bee suit $20 bee gloves $40 bee boots $40 smoker $15 hive tool $15 hive brush) as well as the consumables for this batch ($40 for the containers (some saved for next time) $20 labels from office works, $10 petrol (uncle tax) and a $10 centrifuge fee (again, uncle tax)).

He is all set for his next batch and is now safe with all the required PPE and equipment. He even has enough from his previous honeycomb sales to afford his very own hive (took some convincing to get his mum on board) so he is expanding his empire. The only annoying thing about this is all the regulatory stuff and paperwork – annoying but has to be done for food safety!

I have been trying to do things ‘just For me’ lately and part of that has been going out to a cafe somewhat regularly. I found a lovely creperie called Colada Kiosk in Rymill Park, Adelaide city parklands (they are on Facebook and Instagram go check them out). The owner Tess is lovely and I just can’t believe how she is still working whilst 9 months pregnant! What an amazing person. She makes the best crepes and has a huuuuge list so I have been working my way down the menu. Things will get hectic with the upcoming Adelaide Fringe festival 2022 because this is smack bang in the heart of Gluttony. I’m interested to see how it works out with COVID, because fringe usually has a heap of awesome food and quirky attractions and it is super popular meaning the streets and parks are totally packed out every afternoon and evening.

I also tried my hand at craft, not wanting to throw out the tailings of wax from the honey harvest I made beeswax wraps to use at home which has reduced my reliance on clingwrap and aluminum foil. Just one small step to be more sustainable at home and reduce, reuse, recycle. It is actually super easy to make beeswax wraps and I will publish an article on how I did it sometime in the next few months. I am thinking about adding them to the monthly giveaway – what do you think, are these a decent prize?

I also bought myself this barbecue because I wanted to review it for a website, which was actually pretty cool.

No products found.

You can get it from Bunnings, or directly from the manufacturer Jumbuck.

Angel was a fan and even offered to guard the rotisserie for me whilst it cooked. I am not usually a big meat eater, but I got this lamb roast for $5 from woolies on Christmas eve because it was marked down heaps and had it in the freezer. It was a bit of fun to light a fire and cook it with just some salt, and Angel and I sat out there listening to music and ate the whole thing. We also grilled up some tomatoes, zucchini and pumpkin that I grew in the sky garden. I don’t think I will be using it all that often though, as meat is expensive and bbq isn’t all that healthy. I also like it because I can use the ashes to condition my worm farm if it gets too acidic from the compost, and I can also sprinkle the carbon and ashes into plant pots to help balance pH and to give microbes a place to hide.

I’ve also spent a lot of time with both of my parents. Unfortunately, both are going downhill. Mum has been referred to the palliative care unit but there is no way she wants to leave home, so we are exploring options for at-home care. She seems to have good days and bad days, but the real problem at the moment is getting her to eat food (it’s hard to eat when you don’t feel like it and keep throwing up!). Thankfully I am able to just pop over and stay with her for a few days at a time when needed and try and offer her delicious little morsels. A little, a lot, has been my tactic. Dad is now set up in a little unit near the city, which is good. He is pretty depressed and doesn’t really do much on account of not having legs anymore. He is waiting for the Department of Veterans Affairs to give him an electric scooter/gopher-type thing, which will be good for his independence.

I also said to myself I wouldn’t really talk about my romantic relationships on here because well, inevitably they get discovered by my S.O. and it causes issues, so I won’t say much other than to say, I bought her a copy of the barefoot investor and whilst she did sigh she didn’t immediately turf it, which in my mind is a good sign. Fingers crossed she gets something out of it and we can go on a version of the ‘ barefoot Date nights’.

Captain FI Investments

My investments are split between nine investment ‘areas’. I decided to start reporting on the progression and performance of each of my investments separately so we can find the best way to Financial Independence once and for all.

- ‘FIRE’ Portfolio (Global, US and AUS Index fund ETFs)

- Hands-free Automated Investing (Roboadvisors)

- Cryptocurrency

- Microinvesting (multiple platforms, including Stock picking)

- Real Estate (investment property)

- Peer to Peer lending

- Website Portfolio (Online businesses)

- Angel Investing (Pearler)

- Precious Metals (Gold and Silver)

‘FIRE’ Portfolio (Exchange Traded Index Funds)

My Financial Independence ETF Portfolio is a simple, low-fee passive portfolio that is split between three index-tracking Exchanged Traded Index Funds (ETFs):

- I now have this portfolio fully automated through Pearler which has been a huge gamechanger for me and a massive weight off my mind

- I track my share portfolio using Sharesight, which means my accounting is also completely hands free using the Pearler API plugin.

- This means I pretty much only need to log in to confirm all the trades and dividends over the year when needed for my tax return, however I also choose to log in each month to produce these monthly updates for you guys.

- I have had questions about the tax efficiency of VTS and VEU due to the double tax or withholding tax drag because they are US domiciled funds. This is something I will be looking into over 2022. My limited understanding at the moment is that this tax drag creates an ‘effective MER’ of closer to 0.5% which might mean there may be a lower cost alternative that is better than these ETFs – potentially the Vanguard VGS ETF – something I will be investigating.

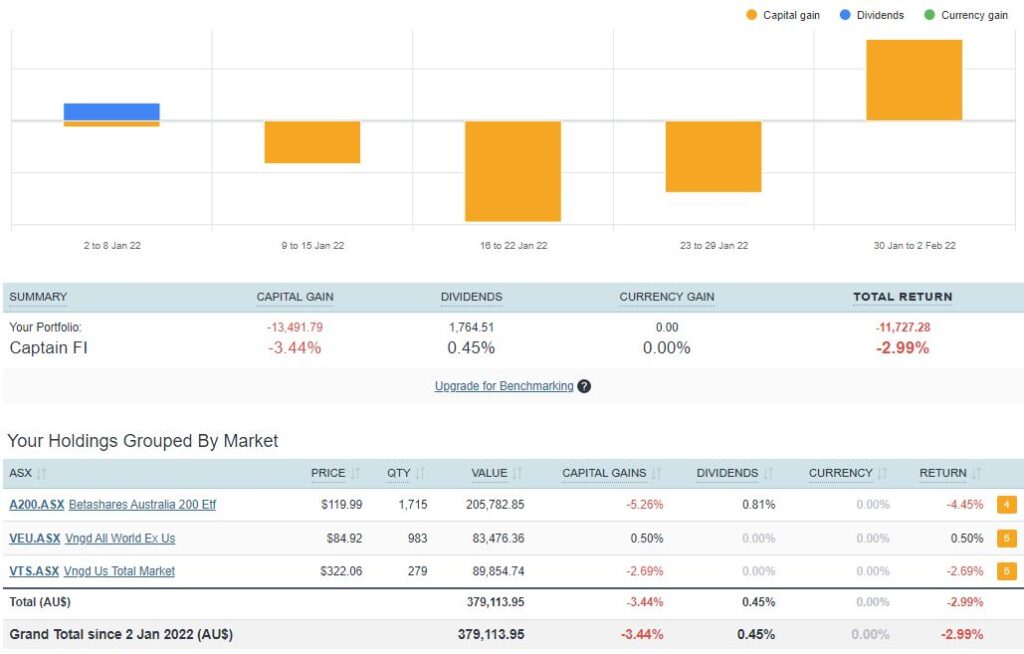

A nice start to the year with some solid dividends getting churned out of A200, VTS, and even VEU (smaller though), followed by some good old fashioned ‘the sky is falling in’ clickbait articles all over every single media outlet that somehow manages to sneak its way into my life. Sure, we ended down 3% for the month, but ce la vi – volatility is the admission price we pay to the stock market (Patt Garratt, Financial Independence podcast episode 27). I’ve been concerned by how rapidly the market has been growing for some time now, so I am somewhat relieved to see a minor correction. For peace of mind though, let’s zoom out.

2021 was a big year of change for me, ‘Hitting FI’ and leaving my flying job, moving from Sydney back home to Adelaide, and getting a dog. But the great news was that it was actually pretty average for the stock market – as shown below. Nice mix of capital growth and dividends, with approximately $13,300 in (mostly franked) dividends paid out to me. Sure, $255 per week in dividends isn’t going to have you living in the Ritz, but it definitely can cover things like rent or mortgage repayments for reasonable living conditions. Thankfully I am making a reasonable income off the website portfolio so I haven’t had to start using them just yet, and have reinvested them as part of my automated fortnightly investment. If I am picky though, this was probably a good year for the market, I personally expect long-term returns to be closer to 10%.

What 2020 Covid crash? What 2022 market crash? When you zoom out enough the volatility reduces and all we see is a slow steady upward march of the equities market. It is too much effort and stress worrying about everything, but thankfully we have a whole economic system designed around this, and chaired by (supposedly) very clever people – so I have found the best strategy for me is to just sit back and let my index funds do their thing, whilst I focus on things I can control like my income shovel, or sitting back with a cocktail!

Portfolio vs Target – Pearler chart

I am still heavy on Australian shares through the A200 fund because early on in the journey I was chasing the franked dividend yields for a baseline level of stable, tax effective income for Financial Independence. I am now working to balance this home bias concentration risk by an automated purchasing of VTS and VEU through Pearler, using income from my website portfolio, side hustles (which I guess you could call part-time work now that I don’t have a real job??) and dividends. I don’t really want to sell A200 to rebalance (although in hindsight, if I had of done this earlier I would be in a much better position due to the growth of VTS).

I had a bit more of a dive into the whole VTS and VEU versus VGS debate regarding tax inefficiencies, and I came to the conclusion after reading some pretty well thought out and written articles and forum entries (such as this forum), that the VTS and VEU foreign tax inefficiency drag brings the total effective MER for a VTS+VEU combination up to around .20% or 20 basis points for most people (above a 15% tax bracket, which most of us are).

Given the VGS has a MER of .18%, it means there really isn’t much of a difference – 2 basis points is .02% and on a $200,000 balance works out to be $40 a year – or less than a carton of beer. I also think you get better diversification with the VTS+VEU combination rather than VGS (otherwise you need to start looking at things like VISM and it gets complicated). Quite frankly I feel like I have wasted my time even spending a few hours on this haha – its almost like the A200 versus VAS debate that Aussie HIFIRE put to rest most eloquently.

I have also a $10,000 ‘Angel Investment’ into Pearler. This is a private equity investment into the actual brokerage tech company itself. This should hopefully go up as the company gets larger and has higher valuations. Up to you whether you consider this a conflict of interest, and I wanted to make sure this was disclosed, but IMO it is the best investment solution for me at the moment which is why I am using it. Appreciation for the company and staff aside, I am always going to ruthlessly chase the best and most cost-effective solution for my portfolio. I have not kept close tabs on how this stake gets valued over time but I am fairly confident it will keep going up.

Hands-free Automated Investing Portfolio

The Hands-free Automated Investing Portfolio is a combination of the two largest Online investment advisors (roboadvisors) in Australia – Stockspot and SixPark. I think they are both pretty damn good, I have been fortunate enough to meet and interview the CEO’s of both companies and I don’t say this lightly but I trust both of them.

So, the difficult decision – which one did I go with? Well I couldn’t fault management, and both companies provide a fantastic user experience. To stay accountable and provide insights for the blog, I wanted to hedge my bets with an investment in both. This way I can analyze the performance of each against one another – comparing the results of asset allocation, and Chris Brycki’s choice to diversify with gold, against Pat Garratts’ choice to diversify with property and infrastructure.

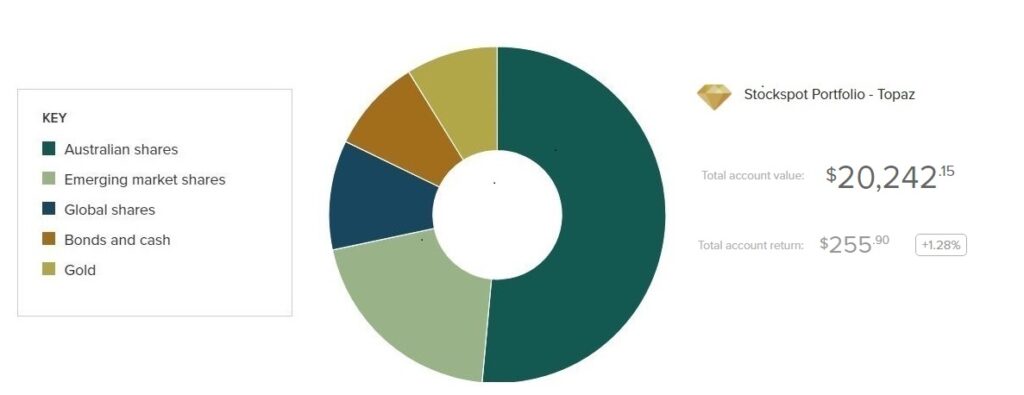

Stockspot

After a successful trial with the Stockspot roboadvisor platform where they allocated me the Topaz portfolio (which is their most aggressive portfolio), I have increased the balance to $20K by investing another $5000 in December. One thing I would like to see is a total annualized return feature rather than just a total return (which may already be available and I haven’t just figured out where it is yet) because it will make a comparison with other investments a bit easier.

I won’t lie I am a tad disappointed in the overall performance which is showing 1.28% this month due to the latest market movements but having said that I have only been investing with Stockspot for about a year now which is only really a very small amount of time. If you go back up to the sharesight rolling 12 month period, you can see how for me, my ETF portfolio has massively outperformed my stockspot topaz portfolio achieving 12.9%. Having said that, the effect of timing your contributions also can vary the effective return you get – Stockspot publishes that the Topaz portfolio fund has had a 10.2% return over the past 12 months. This means I might have invested a lump sum right before a market downturn and this could have dragged my total performance down.

On average since I am in the ‘silver’ fee tier, I am paying a 0.66% Management fee to Stockspot, which is about $132 per year in fees. But you also have to factor in the MER for the underlying ETFs within the fund which ranges from .10% for Vanguard Australian shares VAS, to .69% for IEM – iShares MSCI Emerging Markets ETF. Back of the envelope maths estimates this at about a total MER of .3%, so in total, I am paying close to 1% in fees (.69% to Stockspot and .31% to the ETF fund managers), or a total of about $200 per year on my current balance. You don’t see the fees though because they are always subtracted from your total returns before you see the total returns, which means my total return should in theory be around $455.90 ($255.90 total return plus the estimated $200 in fees), meaning the fees are actually something like 44% of my total return, which sounds pretty alarming.

Feel free to chime in in the comments below if you think I have calculated something wrong here!

If you want to learn more about Stockspot, check out the dedicated review I did on Stockspot – which I will be keeping updated with all the lessons from my personal use trial. I am trying to get the Stockspot podcast out this week too, which will be great to have live.

SixPark

SixPark works much the same as Stockspot, except they don’t use gold and choose instead to diversify with real estate (global listed property and global infrastructure). I proposed that SixPark might then outperform Stockspot slightly, but have higher volatility. I have only been invested in both funds for about a year so it will probably will take a few more years or a market cycle to tell which fund manager performs best (both in terms of total returns but also in terms of risk-adjusted return). But again, no one has a crystal ball, and this is why I decided to split my eggs into these two baskets to diversify and see how the experiment plays out.

SixPark has produced an annualized return of 3.6% which is approx 3 times the total account return I have had from Stockspot, returning a total of $650 from an investment of $20,200 in the Aggressive growth fund. Sixpark publishes they have achieved a return of 10.2% for their Aggressive growth fund, which means again market timing has put a dampener on my returns.

I am in the 0.5% fee tier for Sixpark, ($20k plus) meaning I pay $104 per year in fees to sixpark, plus the fees for the underlying MER of the funds. SixPark have slightly more expensive funds in the aggressive growth fund, again just eyeballing it, they look to be a total of around .40%. so overall I am paying about .90% in fees, or about $187. Because my $650 total return figure is net of fees, that means my ‘before fee’ return is about $837, which means the fees chewed up 22% of my total returns.

For comparison, in 2021 I received approx. $13,300 in dividends from my ~380K ETF portfolio. The effective MER of A200, VTS and VEU is .06%, so I paid $228 in Management fees to the fund managers, and my total return was $13,528, so my effective fee as a percentage of my dividend was 1.68%. In terms of total return, it was 12.9%, or $49,020 (capital gains and dividends), so the effective fee as a percentage of my total return was 0.46%.

Cryptocurrency Portfolio

I kept DCA into crypto through Coinspot despite the correction, with three transactions in the month – I purchased $270 of Bitcoin, $200 of Ethereum, and then finished with another $100 of Ethereum. I am trying to just do it monthly, but I noticed the market going down so kept jumping in to buy small parcels to ‘ride the knives’ down.

The correction is most likely due to concerns over interest rate rising but as the graph shows it is still overall roughly heading in the right direction – but can be misleading. When I tally my total investment so far it is just shy of $4535 money I put in, meaning I have had a total return of about -15% based on today’s figure.

I would like to see an ‘annualized return’ function on the crypto so will be pestering Sharesight soon to connect this for me (because the native graph in Coinspot only shows total accumulation and doesn’t factor in that you have kept adding money along the way).

I did a podcast episode on Bitcoin with Stephan Livera if you are interested to learn more about it, and also recently did an interview with Andrew Fenton from the CoinTelegraph where we talked a lot about crypto and its application on the Financial Independence Journey.

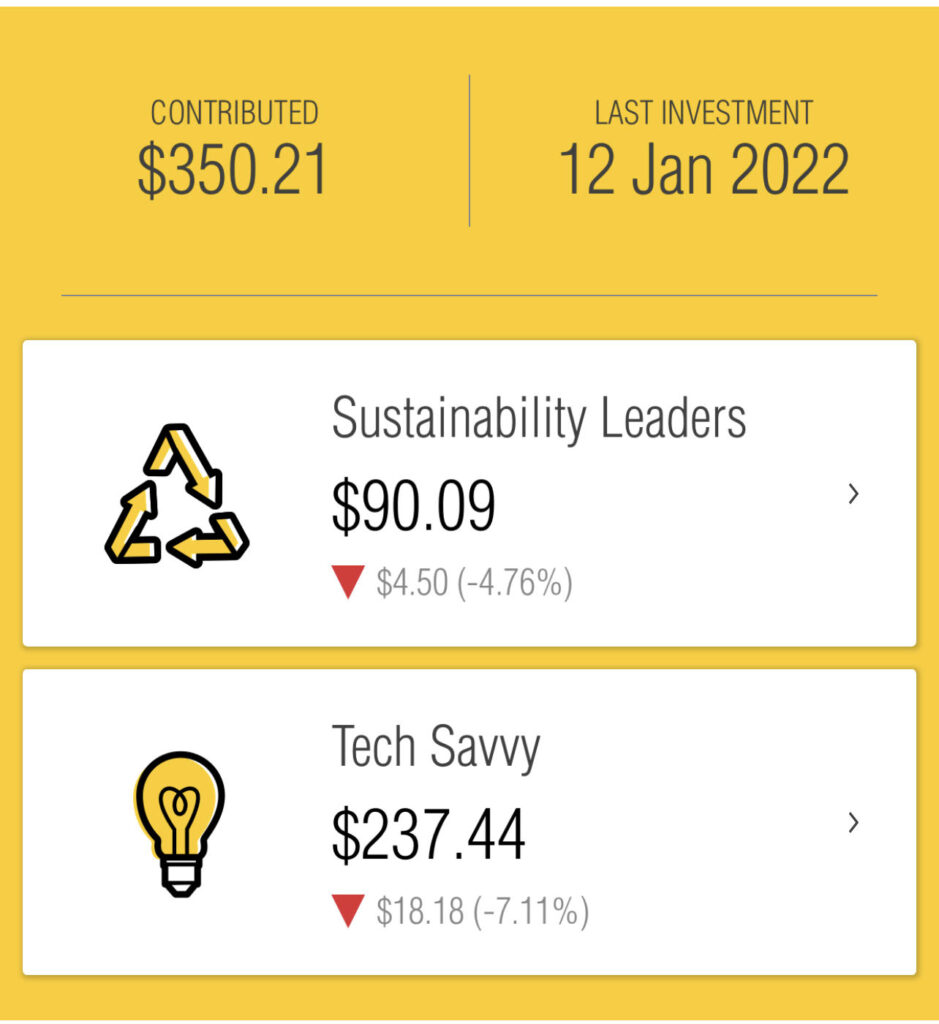

Micro-investing Portfolio

I have been playing with a few of the biggest micro-investing platforms mainly just as research for the blog because I want to see how they all stack up against each other, and against the other portfolios in terms of % gains. It is now really starting to add up – especially because of the Tesla stock pick! I purchased a parcel of Sustainability leaders through Commsec pocket

Stake Invest

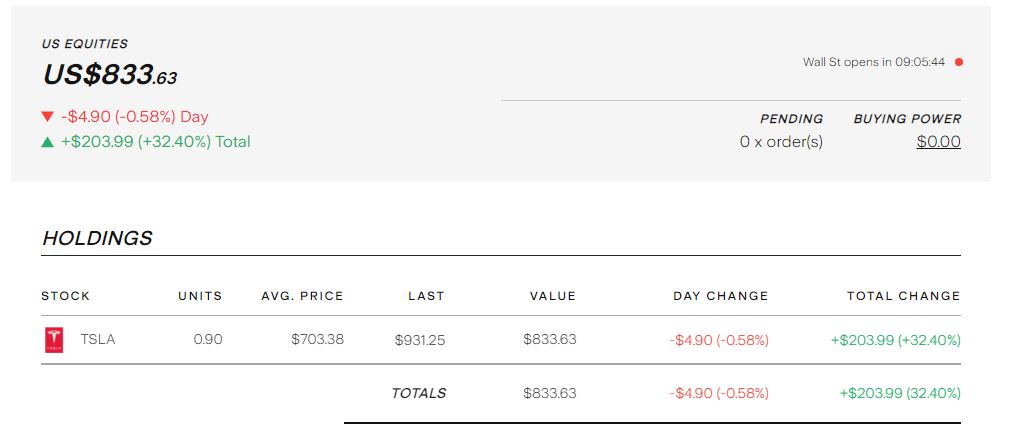

Stake has been an easy way to buy US shares brokerage free, however, I am not really a stock picker. I got lucky on Tesla and I am glad I own a huge chunk of it with my VTS index fund through Pearler. I will keep adding to my Tesla stock when I earn in USD so I don’t have to pay the currency conversion fee (which is .7% for both deposits and withdrawals).

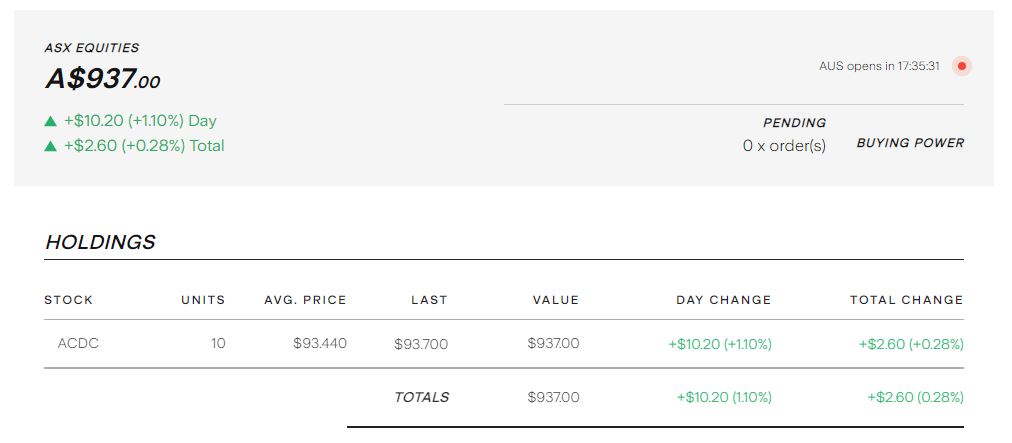

Recently I tested the Australian trading function of Stake which now only costs $3 for CHESS sponsored trades. Whilst this technically makes them $1.45 cheaper than Pearler per trade, they need to add an auto invest function. Stake is definitely more geared toward someone who wants to trade rather than invest for the long term, and there isn’t anything wrong with that – AUS share trading is pretty slick and easy to use on Stake (but I find the US share trading frustratingly slow and clunky because I just have the basic free version which takes a few days to settle).

I opted for the Lithium ETF ‘ASX:ACDC’ because of a group consensus recommendation on the Financial Independence Australia Facebook group. I saw how well Tesla was doing and I personally think the Lithium industry should be well placed for the EV revolution. Whilst this goes against my core index ETF investing strategy, it forms part of my satellite thematic investing. I still benefit from the ETF model and diversification which reduces some of the risks of individual stock picking, but it is a much higher risk investment than a basic total market index-tracking ETF.

Raiz Invest

Raiz aggressive portfolio – good split of ETFs, and a cheap option for small-ish balances at only $3.50 per month. To be honest, the fee’s are more than my investment return, but it is worth it just for the Raiz rewards – you get discounts on various things, plus round-ups from spending and the occasional affiliate click sign up bonus usually more than covers any fees, making it a weird pseudo-investment-pseudo-savings kind of account for me. I’m going to keep going, and once I reach about $1000, I think the investment returns should start to cover any fee’s and it will grow quicker. I like Raiz as a way for people to ‘get their foot in the door’ with investing, as it can be really helpful for beginners.

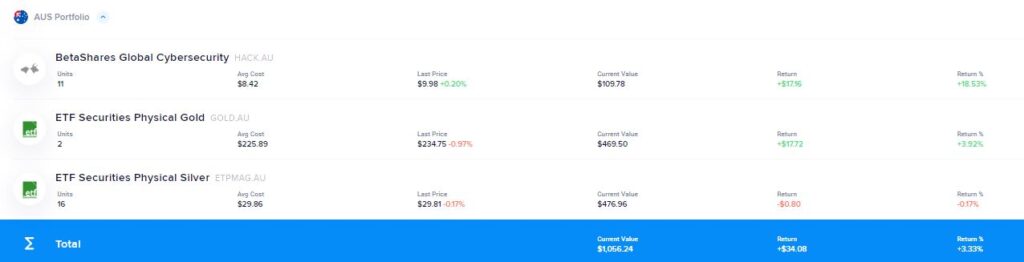

Superhero Trading

I didn’t do any trading on Superhero this month, just let these ETFs do their thing. Everything is up this month, with the silver down a bit, and the HACK shares in the lead. This screenshot can be misleading however as it doesn’t give a true reflection of total performance. No brokerage firm really do this properly, so you have to use Sharesight to make it properly count for dividends and capital growth (and quirky things like share splits or franking credits) to get an accurate annualized return figure.

Spaceship Voyager Invest

Spaceship Origin portfolio: Top 100 Global Blue chip ETF. This seems to be chuffing along pretty awesomely with nearly 12.6% seeming fairly closer to long term expected averages.

Commsec Pocket microinvesting

I added a parcel of Sustainability leaders (ASX:ETHI) to my commsec pocket account, plus I doubled down on Tech Savvy when it was down in the significant double digits percentage loss. It has somewhat recovered since then, but still down a bit. Since I am a long-term investor I am not worried as I will just reinvest dividends and likely just keep adding small amounts whenever I have them.

Bamboo cryptocurrency

I also experimented with Bamboo, a cryptocurrency and precious metals micro investment platform. Since I have gold and silver ETFs directly, I figured I would use this app for Bitcoin and Ethereum. I put in $100 and got a referral credit, but then the crypto markets went down a bit. I also got stung with higher than expected fees.

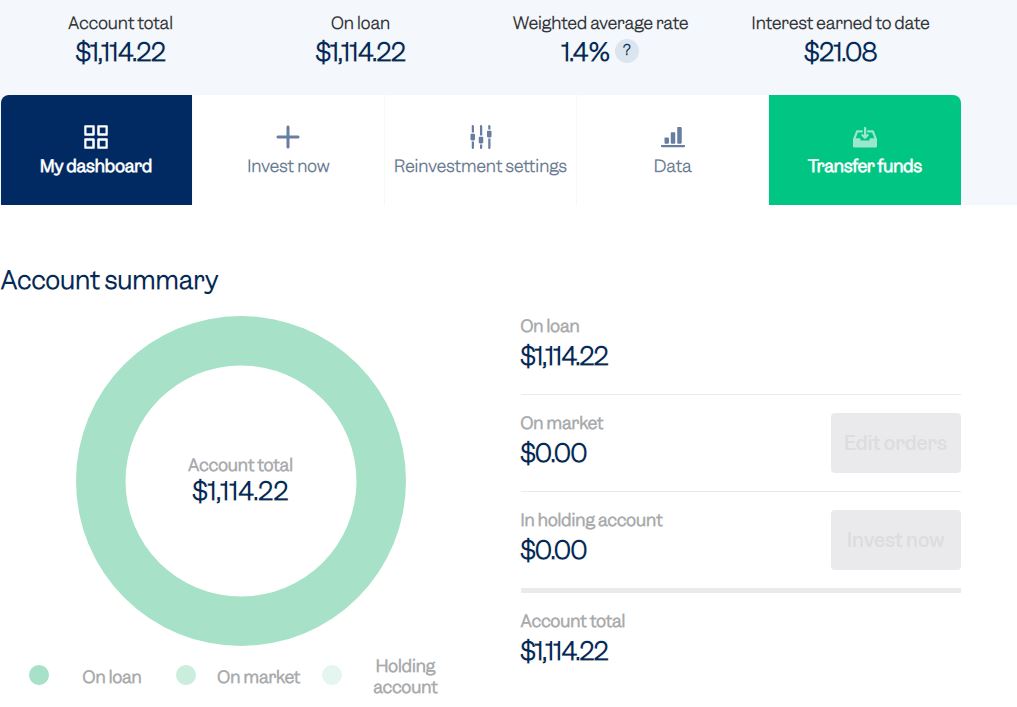

Plenti P2P lending

Plenti Peer to Peer lending account. I backflipped on my decision to axe Plenti, and instead reinvested all my holding account out at 1.4%. You can pick the rate you want to lend it out at. Whilst I was frustrated at a lack of performance, I still think its a good idea to keep a little bit of cash and my bank is basically paying zero interest so at least in Plenti its better than nothing. If you decide to lock it up for longer periods you get a higher rate of return, but I just do the rolling monthly option so I can get access to it quickly as part of my emergency fund (I keep some in physical cash, some in my bank account, some in Plenti, and then the rest invested in my brokerage account).

Investment property

Not much to talk about here, got an awkward $1400 variation bill slapped in my inbox from the builder claiming more COVID-19 delays from lockdowns which we apparently need to still pay them whilst they were in lockdown and not working on our site… sounds fishy!

Expecting to reach the fixing stage invoice to be billed towards the end of this month after an inspection milestone, which will then trigger the internals of the houses to get fitted – plasters, ceilings, doors, kitchen and cabinets, as well as waterproofing the wet areas, fitting the plumbing and electrical and then putting in appliances. I’m pretty keen to see all this get done as it will really transform it from a shell into a proper home and get us ready to rent.

The broker has said that completion should be May-June (So I take that to mean July lol) but that due to COVID there could be delays with getting that done and then we have to sort strata out

I’m currently paying $1000 a month for an interest-only mortgage, which is slightly more than it actually costs and the surplus is going into an offset which is being managed by my friends in the JV (we both pay that, and at the end we will both get one property to rent out).

Rolling lessons learned:

It has taken a long time to get to this point, and boy have we made some embarrassing mistakes. Rolling lessons learned include but are not limited to…

- Thinking we could save money by NOT using an architect on a house and land package we bought from a developer *WITHOUT DA* from council

- Falling for the oldest trick in the book re: portable fencing hire (the fencing hire company stole the fences back and then tried to charge us for having them stolen)

- Endless delays by not having DA and needing to relodge with council three times meant we were one of the last blocks to be built on, and hence became the neighbourhood ‘free rubbish dumping ground’ when the fence was “stolen” (we then had to pay to get the rubbish removed and pay tip fees for – a big fuck you to any dodgy builders reading this who have ever engaged in this practice)

- Because we were the last to build, the ‘new neighbours’ objected to our build being two story due to shadowing – and we were forced to build single story instead at a reduced profit margin.

- COVID-19 delays, subsequent supply restrictions and union activity meant the builder essentially got a free pass to break contract schedule, putting us back by an extra six months+ with no penalty, compensation or damages payable (they even billed us for this extension!!) – this further took money away from the ‘bottom line’ as we had to pay more interest, had capital tied up, and was not earning rental income – all making the build less profitable (would have been more profitable to stick money into index funds)

- Lots of small (but not insignificant) expenses such as council fees, independent inspection fees and rates (even though the house isn’t build apparently you still have to pay rates…) add up to significant amounts over the project lifetime. I was amazed to see just how everyone gouges you for things you don’t even think about, and brokers / builders don’t mention these costs so you just have to cop them when they arrive.

- Independent inspections and checks are worth their weight in gold. I am talking design and plan reviews, soil tests, site inspections, construction and building inspections etc. Do not cheap out or try to skip these, and don’t trust anyone or any builder – they are very cheap insurance and great piece of mind and give you (legal) leverage over the builder, especially if someone is trying to pull the wool over your eyes.

- Pay a lawyer to read the contract. You think you can read through it yourself and spot everything but you can’t. The builders make it their BUSINESS to know how to weasel their way out of things as well as suck more money out of you.

- Be careful if there is a project manager appointed by the lender or the builder. Because they are actually not working for you, they are working for the builder. Fairly self evident how important that last bit is, as they will put the other parties interest ahead of yours (i.e. you pay more, and project gets delayed more).

I have not changed any of the valuations, still going off the banks final completed estimation of $560K, and with the mortgage the way it is at $370K leaves me with about $190K of equity in the build, meaning we currently make just under $70k of ‘manufactured equity’ with an investment of $120K over two and a bit years (not all of the cash was required upfront). This is an approximate projected annualized return of about 13%.

This will come in handy after completion and tenancy as I will likely be able to access some of this equity during a refinance towards buying the dream farm in the Adelaide Hills. Not sure how refinancing is going to go given I am not getting a full time flying wage anymore (but hopefully may be able to finance based off website income). When the build is finished and tenanted I will do a full article explaining everything and try to calculate the total costs and profit.

With the general upward trend of property values in the area, I am hoping we can get it revalued on completion at higher than $560K (I believe some similar properties in the area have been going for $600K+) which would be awesome and would offset some of the pain and suffering of building an IP during COVID-19 pandemic.

Online Business (websites)

It was good to see a strong traffic growth across the portfolio this month again, this site up 40% and my aviation site up over 220% to take the lead as the largest site (and now the source of my attention to properly monetize).

I am slowly launching another 13 websites, I have finally registered the domain names, done basic keyword research and am now migrating the template across to each site and then uploading the new logos and slowly completing the required structure pages. Once these are set up I will just follow the cookie-cutter bouncing ball approach to content generation and get writers to produce great content to publish one 1000 word article a week per site.

It is exciting but it is also a lot of work at this stage setting them all up. Thankfully I have income from my current portfolio of websites which I can use to pay outsourcers to make my job a little bit easier this time around. Having a techie, VA, writers and a graphic designer make it a lot easier than when I launched my first five sites!

I conservatively value my sites at 30x monthly earnings, plus modifiers for things such as large emailing lists, content stocks and large social media pages.

I learned these skills through the eBusiness institute – I have done a pretty comprehensive review of the eBusiness institute as well as interviewed Matt and Liz Raad about this on the podcast about online business and websites if you want to learn more about this lucrative side hustle. They provide a free introductory course for CaptainFI readers. I have also recently interviewed Liz Raad again on the pod about entrepreneurship, which is live now.

Angel Investing

Currently I have made an ‘Angel Investment’ in the Financial Independence brokerage company Pearler. This was the maximum allowable private investment of $10,000 (AUD) made in July 2021 with the number of ‘private equity’ shares based on their June company valuation.

This helps to fund Pearler’s capital investment pool and lets them grow and build their business – which is great for me since I have nearly $400K invested through them and I trust them to automate my investing for me.

As Pearler grows and builds its revenue, it will get an increasingly higher company valuation and my private equity will grow accordingly (i.e. it is not a free $10,000 loan, it is a $10,000 investment where I am buying a slice of the company).

Whilst this doesn’t align with my general investing philosophy of index investing and diversification, I feel I have a unique insight into Pearlers organisational and company structure and build a great rapport and trust with their executives, and I believe in this company and its genuine intentions to help people reach financial independence.

Also realise that while $10,000 does sound like a lot of money, but this is a small overall percentage of my total investments so my personal risk is actually quite low, and I would not encourage anyone to go out and make $10,000 Angel investments into tech startups. It is generally quite high risk (high risk = high reward). Make sure you don’t compare your financial ‘race’ with others (just think of it like a time trial where you are only competing with yourself).

The valuation of Pearler has gone up which is good, although I am not really sure what that means for my investment, I guess it has gone up, but I haven’t been told anything ‘official’ from Pearler yet.

Precious Metals

These really haven’t done anything. Gold is up a few percent, silver is down, and lithium has gone sideways.

Cash / emergency fund

Sitting on a total of about $7K in the EF split across the various bank accounts, P2P lending and bond. During the recent market dip I took all the cash I had and invested it into VTS, and since then have replenished my cash stocks a little bit. I can never seem to have enough cash on hand to invest, its quite funny really.

Captain FI net worth progression

The net worth progression graph is rather crudely constructed in Excel, but still demonstrates the ‘somewhat exponential’ journey over the past 14 years. You can access the archives for my Net Worth updates here to see how its gone over time.

Again I feel incredibly privileged that this started from ZERO, rather than from a negative. Unfortunately, a lot of people need to overcome a negative net worth whether that is due to student loans for their education or perhaps poor decisions with credit cards etc. This is a huge testament to how amazing my mum is and all of the sacrifices she made to support our family and prioritise our education, which allowed me to achieve so well during my final years of high school and ultimately score a scholarship at university (I got paid to study!).

| Date | Net worth | Difference | Saving Rate | Notes | |

| Jan 09 | $5,000.00 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK | |

| Jan 10 | $24,000 | +$19,000 | ? | Estimate NW | LINK |

| Jan 11 | $40,000 | +$16,000 | ? | Estimate NW | LINK |

| Jan 12 | $92,000 | +$50,000 | ? | Estimate NW | LINK |

| Jan 13 | $130,000.00 | +$38,000 | ? | Estimate NW | LINK |

| Jan 14 | $161,000.00 | +$31,000 | ? | Estimate NW | LINK |

| Jan 15 | $200,000.00 | +$39,000 | ? | Estimate NW | LINK |

| Jan 16 | $281,000.00 | +$81,000 | ? | Estimate NW | LINK |

| Jan 17 | $340,000.00 | +$59,000 | ? | Estimate NW | LINK |

| Jan 18 | $482,000.00 | +$142,000 | ? | Estimate NW | LINK |

| Jan 19 | $542,000.00 | +$60,000 | ? | Estimate NW | LINK |

| Jul 19 | $578,900.00 | +$36,900 | 84% | Finally began tracking NW this like a proper adult. | |

| Aug 19 | $560,100.00 | -$18,800.00 (-3.2%) | 78% | Share market slight correction, Ok savings. | |

| Sep 19 | $584,744.88 | $24,644.88 | 72% | Share market rebound, savings rate not so good. | LINK |

| Oct 19 | $600,386.00 | $15,641.12 | 84% | Good saving this month. Normal salary, plus allowances, dividends from index funds, tax refund, eBay selling and was working abroad in asia where things are cheap. | LINK |

| Nov 19 | $612,917.21 | $12,531.21 | 76% | Falling short of my savings goal of 80%. Mostly domestic legs this month with higher costs. Also invested in hydroponics. | LINK |

| Dec 19 | $625,350.00 | $12,432.79 | 76% | Good savings of cash (for development) and investment, however higher spending due to Christmas period (Travel and Gifting). | LINK |

| Jan 20 | $865,212.00 | $239,862.00 | 55% | Super settlement was a HUGE boost to NW. $9K growth from stock market. Expensive month lots with lots of unexpected bills – weddings, travel, Booking flights, fines etc. | LINK |

| Feb 20 | $851,802.0 | -$16,592 (-1.9%) | 52% | Large increase in spending on myself this month, still managed to tuck away $5K to put into shares and property. Corona Virus market scare resulted in a correction and gave NW a small negative trend. Time in the market not Timing the market! Became Single again. | LINK |

| Mar 20 | $819, 354.6 | -$31,806.95 (-3.7%) | 80% | Another small step backwards in the NW due to the ‘corona crash’ in full swing. FIRE Portfolio of ETF/LICs down about 15% this month, however due to high savings rate and structure of my superannuation annuity the NW is only down 3.7%. Savings rate good at 80%, higher than usual income (with some slightly higher spending, too). Picking up shares on discount – this is the best outcome for someone in the accumulation phase with good income! | LINK |

| Apr 20 | $847,023 | +$27,668 | 85% | $11,000 in rebound of stock market capital prices alone (up 6%), plus first quarter dividends paid (heavily reduced due to banks withholding dividends). Great savings rate due to COVID-19 lock-down = no spend. Increased entrepreneurial efforts and selling down of physical possessions provided side hustle income. Two standard paychecks from flying activity; domestic day trips only so no allowances. All cash unfortunately had to go into the property development due to contract timing, I am chomping at the bit to buy some more index funds before they go back up in price too much – hence why I am selling most of my toys! | LINK |

| May 20 | $857,859 | +$10,836 | 92% | Some Great sales as I let go of my Super Sport Motorcycle, Some gym gear, expensive flying equipment and a few other various bits and bobs and invested this money. Flying still reduced, but increasing from April. The share market grew as I continued to make my fortnightly investments. I also wrote down the ‘value’ of some of my possessions (liabilities) such as my car, tools and furniture by around $10K to align them to market price (“tell him hes dreaming…!”). | LINK |

| June 20 | $858,650 | +$791 | 90% | Small Net Worth gain as I continue to declutter and simplify my life, despite being off work due to a family emergency. Share market not doing much. | LINK |

| July 20 | $888,218 | +$29,568 | 68% | Majority gain due to share market going back up, low spending due to being on the family farm and at home because of lock down. | LINK |

| Aug 20 | $1,029,293 | +$141,075 | 74% | Became a millionaire. Achieved this massive milestone I set out for myself in Dec 2019. Included unrealised gains in my property development as well as website business. Good savings rate due to not much spending, invested in Aus and total world shares. Investing in my web business. Starting to shift focus away from $$$ and more into looking after my mental health. | LINK |

| Sep 20 | S1,045,486 | +$16,193 | 60% | Officially took time off work for the rest of the year to be close and look after family during major operations. Continued to sell down physical possessions and work on digital business while at home. NW gain mainly due to valuation of websites. | LINK |

| Oct 20 | $1,064,399 | +$18,913 | 80% | Base income (retainer) and leave loading, dividend and websites provided income, as well as raiding my P2P lending capital. Significant bill for property due to design not meeting standards which effectively lowers my equity position, as well as fence being stolen. | LINK |

| Nov 20 | $1,143,433 | +$80,394 | 82% | Big gains came from share market growth (influencing both the Financial Independence share portfolio and Invested superannuation), Business gains (due to increased earnings) and a $30K boost to my annuity thanks to me logging in and checking the fine-print on the accumulation stats. I only invested around $7K. Insane that in one month, I accumulated nearly more net worth than I did in four years from 2009-2012 | LINK |

| Dec 20 | $1,152,920 | + $9,487.32 | 84% | Share market slight drop, Earnings from Business, Contract work, Selling possessions. No share market investments this month (oops! I forgot and money was tight). Invested a lot into the website business this month (way more than planned) and it is still running at a decent loss (plans to turn it cash flow positive in 3 months). | LINK |

| Jan 21 | $1,165,678 | +$12,757 | 79% | Great returns from the share market. Earnings from Business, Dividends, Flying wage, flipping items on consignment. Regular share contribution, investing in micro investing platforms, P2P lending, Investment property and big reinvestment into the business (still running at a loss) | LINK |

| Feb 21 | $1,135,272 | -$30,406 | 76% | Significant write down on property development due to council DA rejection and redesign requiring more money and creating less equity. Offset by small increase to Business value and investments. Simplified my investments and switched over to Pearler. | LINK |

| Mar 21 | $1,155,594 | +$20,322 | 71% | Continued investment into the portfolio as well as growth of investments and business. Gave my notice at work and looking for part time job at home for ‘Barista FI’ | LINK |

| Apr 21 | $1,242,220 | +$86,727 | 74% | Property development back on track | LINK |

| May 21 | $1,379,469 | +$137,248 | 72% | Massive gains in the website portfolio due to revaluation based on recent business income, big growth of superannuation due to annuity increasing (salary increment) and shares generally went up. Crypto went down by about 40% or so. | LINK |

| June 21 | $1,469,989 | +$89,757 | 41% | Quit flying role and moved to Adelaide. Great month for investments, websites producing serious income so accordingly they are valued higher. Spent a lot on furnishing the new apartment and on enjoying some more luxuries. Seeing a therapist to help deal with anxiety from leaving work. | LINK |

| July 21 | $1,543,959 | +$74,732 | ??? | Set myself up in Adelaide. Did basically nothing for the whole month except spent time with family, relax, sleep and go to doctors appointments. Massive boost to website portfolio AdSense and affiliate incomes, as well as general share market performance. | LINK |

| Aug 21 | $1,624,116 | +$70,156 | ??? | Relaxed again, focused on mental and physical health, and spending time with family and my partner. Big increases to spending (too afraid to calculate a ‘savings rate’) but also big increases to NW through website portfolio income growth. Finally got the slab poured on the investment property (foundation). | LINK |

| Sep 21 | 1,640,663.85 | +$16,547 | ??? | Stocks, super etc went down, but business income from websites increased, plus business valuation increased. Property build. got to frame stage, and I also got a dog! Expenses for vet surgery well worth it. Moved into a nicer apartment | LINK |

| Oct 21 | $1,705,907 | +$65,243 | 30% | Big boost from website valuation due to securing new affiliate contracts for recurring income, shares went up nicely. No massive changes to this month. Calculated a savings rate and found myself pretty low due to spending a lot on my garden and going out quite a lot – I don’t think I will calculate this savings rate figure any more. | LINK |

| Nov 21 | $1,739,144.23 | +$33,236 | N.A. | Great month. Relaxing (somewhat). Spent a lot of money doing ‘fun’ things like winery tours, a fine dining experience and self education. Shares moved sideways (well slightly down) but everything else went up. Building got to enclosed stage (roof, walls, windows and doors) but have had some issues with build quality and weather / covid delays. Put a $1000 deposit on the puppy. | LINK |

| Dec 21 | $1,764,516 | +25,372 | N.A. | Spent nearly the whole month with family, did some work on the website portfolio. Traffic recovered from google algorithm changes. Invested $10K into Stockspot and Sixpark, $1K into ACDC, $100 into Comsec pocket and $100 into Bamboo, $260 into BTC, $4K into ETFs through pearler. Paid the $3000 balance for the puppy. | LINK |

| Jan 22 | $1,826,633 | +$62,117 | N.A | Stock market slightly down, Massive boost to website traffic (overall its more than doubled). Invested $10K VTS, 2K VEU through pearler, Paid for Angels cancer surgery, bought more BTC and ETH, bought a parcel of ETHI on commsec pocket. |

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

I’m so sorry to hear about the health of your parents – that’s very difficult. I’m loving that your nephew is learning some important entrepreneurial skills there – he’s lucky he has you to guide him! Good on him for showing an interest and learning about business, making money and sustainable practices too! All so important for young kids his age!