Happy New year! Ending 2021 with a cheeky $25K gain was a pretty nice finish to a year with ten monthly net worth increases in a row, as Feb ’21 was the only month this year with a negative return. I have strong plans for 2022, and hope this trend continues to get into the 2 Milli club. I made a few unusual investments this month (testing the waters and conducting research), as well as stashing as much as possible into my index fund portfolios. Read on for all the details.

CaptainFI is reader supported, which means we may be paid when you visit links to partner or featured sites

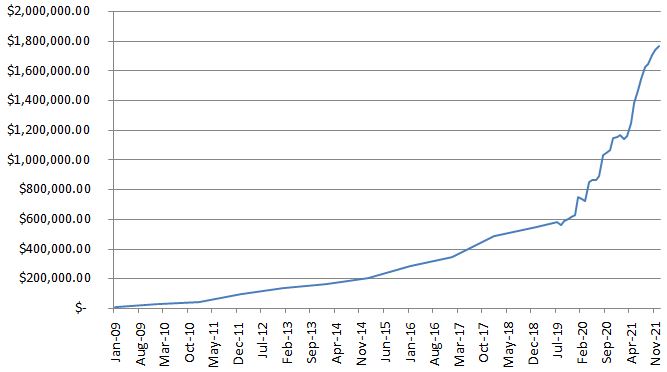

CaptainFI Total Net Worth

CaptainFI Financial progression

CaptainFI personal update: Early Retirement?

Who doesn’t love December right? Specifically the period between Christmas and New Years. I haven’t actually known what day of the week it is for some time now, existing in a kind of ‘timeless black hole’ where all I seem to do is eat, sleep, watch movies, garden and hang out with family. Its been great. Is this what early retirement feels like?

Strangely, before the end of year Christmas period, I found myself having to be productive to occupy myself and pass the time – because most of my friends and family had to go and work their jobs and couldn’t hang out! I finished a few books I wanted to get through, worked a few days on the websites and released a podcast episode. I still have a few more to punch out over the next few months that I need to just bite the bullet and edit.

I also managed to get my first successful harvest of honey from my hive in the city, and honeycomb from my mums hive in the Adelaide foothills. I think the honeycomb from my mums hive tastes better, probably because she has placed hers in the orchard and is surrounded by huge gum trees, wheras I suspect my bees are collecting nectar and pollen mainly from flowers in the city and surrounding parklands.

Uncapping and draining the honey out of the honeycomb was a bit messy but totally worth it. We were all standing around licking our fingers and when the honey was done, everyone got an implement to lick clean. Way better than licking the egg beaters when you were a kid and someone made a cake!

The honeycomb from mums hive was much easier to harvest. Because she has foundation less frames (with wires going across) all you have to do is shake the bees off, bring it inside and then cut out slabs that you want to tub up. I found I could fit about 700g of honeycomb into these take-away containers.

All up I got about 3kg of honey out of one frame from my hive, and we got 7kg of honeycomb out of mums hive. And it is nearly already all gone! Friends and family loved it, but thankfully there is about 10kg of honey left in my hive and about 20kg of honey left in mums hive so there is plenty more to harvest later on. If anyone in Adelaide wants any honeycomb then get in touch through the facebook group.

Financially planning, the websites have been producing decent income which I have been using to cover not only my cost of living, but enabling me to continue growing the investment portfolio. If you had told me this a year ago, I would not have believed you.

Looking back over 2021, I have also been speaking to a lawyer about potentially making a claim on my super as a result of workplace injuries. I haven’t spoken about it much, but I have some pretty shitty injuries to my neck and back as a result of my flying career resulting in chronic pain and an ongoing need for medical support – pain killers and physio. Ultimately it will require surgery but we are going through trying all other options before then. Unfortunately these are pretty common issues for pilots and a lot of my colleagues and work mates have similar injuries.

The irony is I am currently covered through private health (as the injuries occurred at work) despite the fact that I said I previously that personally I would not bother with private health (unless my employer paid for it). When I ‘hit FIRE’ I was planning on ditching it – apart from any insurance designed to reduce applicable tax and thus be a net saving as advised by my financial planner.

This means I am currently getting my pain treatment paid for, which has included tens of thousands of dollars worth of scans, consults with doctors and surgeons with many impressive post nominals, ongoing physio, exercise physiology and health coaching – but I am having to pay for extras that aren’t covered such as additional remedial massage, equipment (like the sit stand desk I am currently writing on), complimentary therapies and supplements.

I have been pretty open about my attitude towards mental health, and how important I think it is to talk about mental health and reduce the stigma around it. A few years ago I was assaulted at work which was a pretty rough time for me. I can look back now and see it was a really damaging period for me where a lot of other things started to unravel in my life – my relationship failed, I became borderline obsessive compulsive about FIRE and berated myself for spending any money, I started to resent flying and my job, my friendship circle shrunk down to only a handful of very close friends, chronic pain, fatigue and insomnia started to become unmanageable, and workplace cliques and a bullying culture became totally overwhelming for me. Add two parents with terminal cancer, my dogs dying of old age, a miscarriage endind a new relationship (her decision to leave) and I was totally fucking over working my arse off flying both routine and custom ‘one-off’ domestic and international flights during a pandemic for a measly wage (including COVID relief flights).

In the psychiatrists words… Depression, PTSD and anxiety set in. I’m super glad to be out of a toxic workplace and on the path to recovery, and whilst I possibly over did the whole FIRE saving rate and investing thing and placed additional stress on myself, it was my saving life boat as without those assets behind me I just would have felt so trapped in that environment (and stuck working with the perpetrators of the assault with obvious implications to mental health). I’m working my way through CPT and talk therapy, and proud to say I am not on SSRI’s (antidepressants) anymore, but there is still a long way to go. Again, I am grateful to have this covered under my private health as this would be much more difficult and expensive through the public system.

Even though I used FIRE to escape the workplace, the solicitor is encouraging me to seek a compensation settlement and early release of super due to flying incapacity. Unfortunately, at the moment it is looking like I won’t ever fly commercially ever again. the Civil Aviation Safety Authority is extremely sensitive and draconic when it comes to anything mental health, back or neck related when surgery is on the cards, or especially if antidepressant and opioid medications have been prescribed.

I am no stranger to legal action, and the company probably sees me as a massive pain of the arse because I fought tooth and nail a few years ago to be back paid when I discovered I was being underpaid for years. Accessing my super and having my annuity paid out early would be a massive leg up in buying the hobby farm and paying the mortgage down on the investment property, but I just don’t know if I have the energy to even think about this now. I’m not even sure if I am entitled to a claim given I am earning money on the website portfolio and the rest of my investments… which just seems unfair (punishing me for my own discipline and diligence in future planning) but hey, I have a roof over my head, food in the fridge and an awesome garden, so I cant complain!

I wrote how I initially was planning for Early Retirement in the transition to retirement financial planning process article, but given the website portfolio and investments are performing so well right now, I am just taking a little off the side to pay my bills and reinvesting as much as possible.

My father has stabilised somewhat medically, and has been forcibly evicted from living on his farm by the government due to medical reasons. As a double amputee there is no way he could survive there alone, let alone look after the property, but he is still fighting this transition every step of the way. After being discharged from hospital, as he is an ex-serviceman, he has been provided a rent stabilised disability accommodation in Adelaide, and whilst we wait for it to be suitably modified and for his mobility equipment to be installed he has been staying with me.

I forgot how good living alone was!

I had done the whole house hacking communal living thing for the better part of a decade, but in the past 4 years in Sydney I have had my own (albeit single bedroom) apartment which had always been my safe space / inner sanctuary. Now that I have moved back to Adelaide I decided to splurge on a larger penthouse apartment (since I am working part time from home on the websites and really wanted additional room for an office, guest bed, garden and potentially a nursery). So when you are used to living alone and then every time you turn around and there is a wheelchair blocking your path with a someone muttering misogynistic shit, cursing and swearing, pissing into a bottle on your couch or all over the bathroom floor, demanding food or sitting with the fridge door open beeping away and staring into it for an eternity, you tend to get over it pretty quickly.

It has been pretty confronting seeing my dad regress into more child-like behaviour, and I wonder what permanent brain damage was done when he was in the coma for so long. But every now and then he will whip back into reality and say or do something incredibly insightful or intelligent – he disassembled and reassembled his laptop on my kitchen table with only a screwdriver and multi-meter in order to replace a tiny electrical component which I could barely even see myself, let alone solder. I’m pretty sure he made his own mini soldering iron using a battery and a paperclip or something to tack up the circuitry, which is pretty impressive given how extreme his hands shake. 50 years ago he used to work on maintaining fighter jets in the Air Force, and back in the 70s they didn’t have the same maintenance procedures we do in aviation today (back then they actually used to repair shit rather than just swap components out), and I guess that training has never left him!

Mum has unfortunately been pretty crook this month, and they have doubled her morphine dosage to keep her comfortable. She was able to get her COVID booster which she was pretty keen to get given the surge in COVID cases we have been having recently. We enjoyed a nice big Christmas breakfast at the family home with my sisters and all the nieces and nephews (our family tradition is to break out the good china for this meal), exchanging of presents and a swim. Thankfully all the dogs got on (mostly), then my uncle came to visit my dad and I later at my apartment in town.

Unfortunately it turns out my uncle was a close COVID contact, so he has since been doing the full on isolation and my father and I had to isolate and get tested ourselves. Thankfully we were both double vaccinated and the tests came back negative on day 3 so we were able to leave isolation. I think if he caught COVID it would probably knock him off the perch, so I think we were very lucky. I am super appreciative of all the hard work of all our frontline testing and medical staff, as well as all the people working behind the scenes to keep us safe.

I am so excited for is January – on the 4th my dad gets his own apartment and I get my inner sanctum back, then the next milestone is the 6th – this is when I get the cocker spaniel puppy we have all been waiting for! The family is very excited, and mum is looking forward to having a companion to cuddle. I am also nervous for January 7th as that is when my Dog goes in for surgery to get her cancer tumours removed (her breast cancer been causing her nipple to bleed and make her uncomfortable so we have to sort it for her quality of life). So there is a lot on the cards for 2022 already!

Anyway, enough rambling and on with the investment updates!!

Captain FI Investments

My investments are split between nine investment ‘areas’. I decided to start reporting on the progression and performance of each of my investments separately so we can find the best way to Financial Independence once and for all.

- ‘FIRE’ Portfolio (Global, US and AUS Index fund ETFs)

- Hands-free Automated Investing (Roboadvisors)

- Cryptocurrency

- Microinvesting (multiple platforms, including Stock picking)

- Real Estate (investment property)

- Peer to Peer lending

- Website Portfolio (Online businesses)

- Angel Investing (Pearler)

- Precious Metals (Gold and Silver)

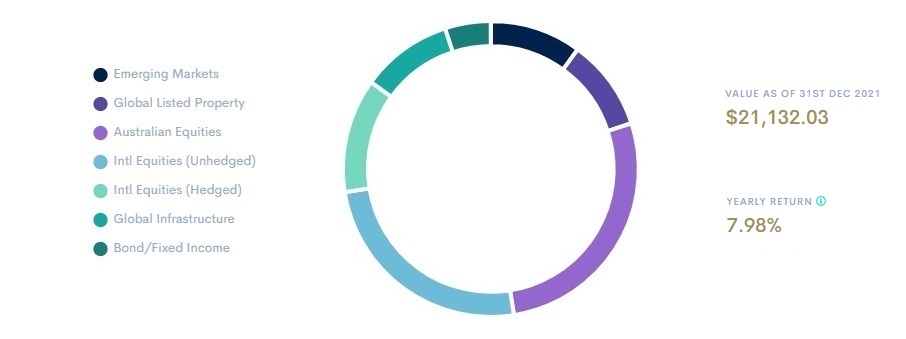

‘FIRE’ Portfolio (Exchange Traded Index Funds)

My Financial Independence ETF Portfolio is a simple, low-fee passive portfolio which is split between three index tracking Exchanged Traded Index Funds (ETFs):

- I now have this portfolio fully automated through Pearler which has been a huge gamechanger for me and a massive weight off my mind

- I track my share portfolio using Sharesight, which means my accounting is also completely hands free using the Pearler API plugin.

- This means I pretty much only need to log in to confirm all the trades and dividends over the year when needed for my tax return, however I also choose to log in each month to produce these monthly updates for you guys.

- I have had questions about the tax efficiency of VTS and VEU due to the double tax or withholding tax drag because they are US domiciled funds. This is something I will be looking into over 2022. My limited understanding at the moment is that this tax drag creates an ‘effective MER’ of closer to 0.5% which might mean there may be a lower cost alternative that is better than these ETFs – potentially the Vanguard VGS ETF – something I will be investigating.

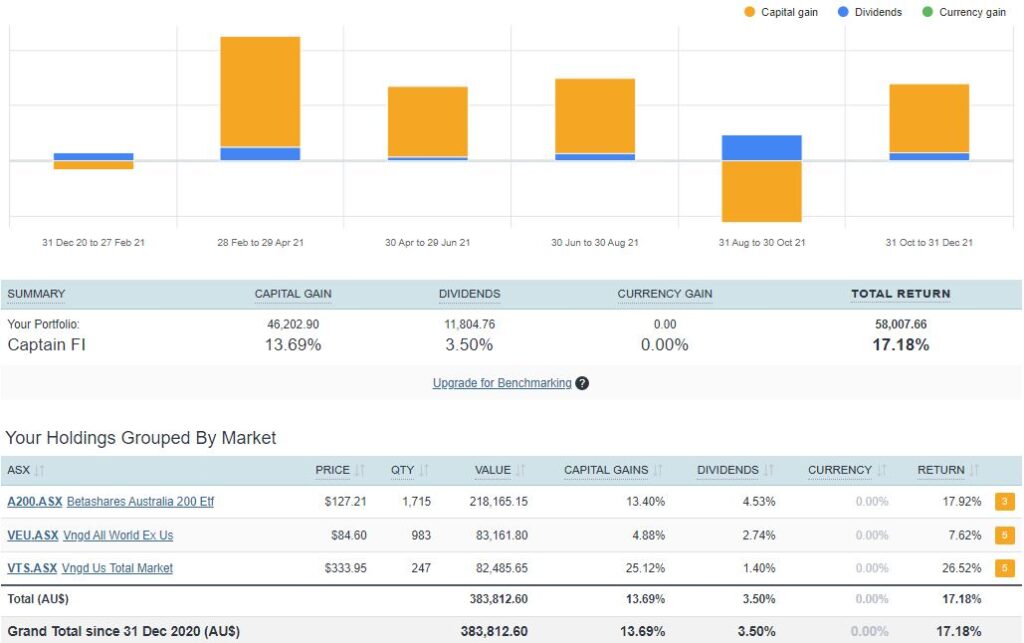

A pretty solid gain for the month with $7K in capital gains and $1.4k in dividends, or a 2.25% gain. I always think to myself, ok if this continues every month it will be a 2.25 x 12 = 27% annualised return with for me doesn’t seem sustainable based on long term averages, so I am expecting a correction back to a more sustainable growth level of around 1% per month. the ASX was the strong earner this month with just under 3.5% growth – helping to offset a down turn in the global (ex US) market.

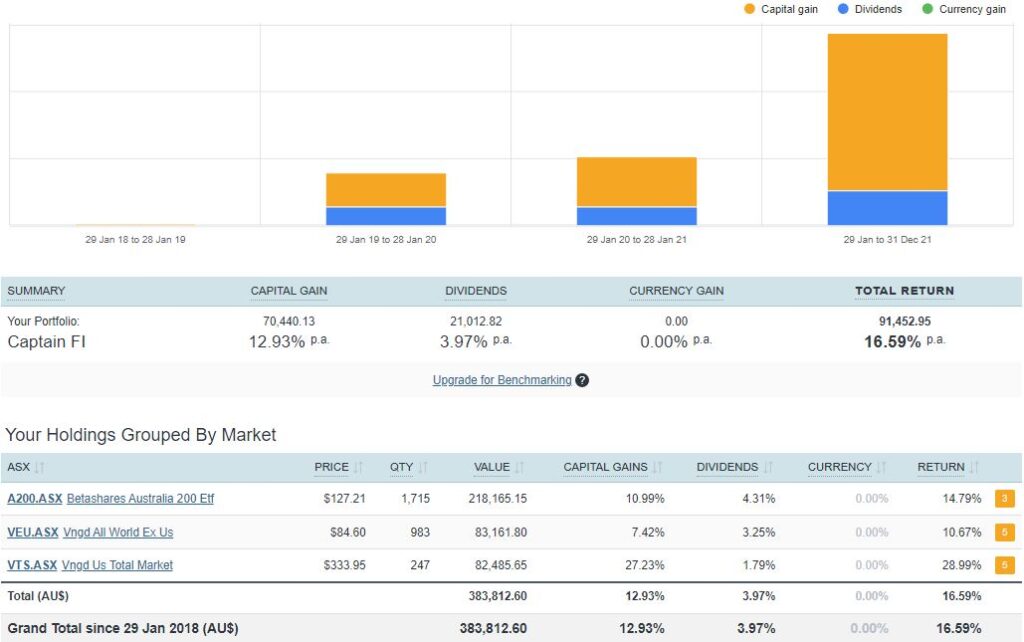

A pretty solid wrap for 2021 with a total return of 17%. US shares really performed amazingly at 26.5%, Australian shares at just shy of 18% and global (ex US) shares dragging behind at only 7.6%. I think this is obviously because the US and AUS governments have been very proactive in managing COVID, national advantages such as size, healthcare and immigration control as well as managing the 2020 financial dip with money printing and economic stimulus, whereas I think many of the worlds smaller countries have not been as fortunate – especially emerging markets, Pacific and Asia which are big chunks of the VEU ETF.

Watch out for inflation though, I have seen some pretty crazy high figures kicking around – some in the US as high as 5.8%! (this means you realistically need to subtract this from your return AFTER accounting for applicable taxes to get a real growth figure).

What 2020 Covid crash? When you zoom out you can see the markets chugging along as they always do, as this is how our capitalist economic system works. Assets always go up due to inflation and human ingenuity as we continue to invent new things and everyone gets wealthier, so you need to invest your money into productive assets or else it slowly becomes worthless. I’m glad to see both the blue (dividend) and yellow (capital growth) columns increasing each year, showing about a 4% and 13% annualised total return respectively. Lets hope that trend continues into 2022 as I continue to invest and reinvest dividends into the portfolio.

Portfolio vs Target – Pearler chart

I am still heavy on Australian shares through the A200 fund because early on in the journey I was chasing the franked dividend yields for a baseline level of stable, tax effective income for Financial Independence. I am now working to balance this home bias concentration risk by an automated purchasing of VTS and VEU through Pearler, using income from my website portfolio and dividends. I don’t really want to sell A200 to rebalance (although in hindsight, if I had of done this earlier I would be in a much better position due to the growth of VTS).

I am considering switching by strategy of buying VTS and VEU into something a bit more simple like VGS. This will still allow me the option to invest in global (ex Australia) index funds so I can get my portfolio balance correct, but it would be a bit easier than bouncing between VTS and VEU. Having said that, the stellar performance of VTS is seriously giving me some recency bias as I am tempted to just go hard on VTS shares hoping they will continue their current trajectory.

I have also a $10,000 ‘Angel Investment’ into Pearler. This is a private equity investment into the actual brokerage tech company itself. This should hopefully go up as the company gets larger and has higher valuations. Up to you whether you consider this a conflict of interest, and I wanted to make sure this was disclosed, but IMO it is the best investing solution at the moment which is why I am using it. Appreciation for the company and staff aside, I am always going to ruthlessly chase the best and most cost effective solution for my portfolio.

Hands-free Automated Investing Portfolio

The Hands-free Automated Investing Portfolio is a combination of the two largest Online investment advisors in Australia – Stockspot and SixPark. I think they are both pretty damn good, I have been fortunate enough to meet and interview the CEO’s of both companies and I don’t say this lightly but I 100% trust both of them

So, the difficult decision – which one did I go with? Well I couldn’t fault management, and both companies provide a fantastic user experience. To stay accountable and provide insights for the blog, I wanted to hedge my bets with an investment in both. This way I can analyse the performance of each against one another – comparing the results of asset allocation, and Chris Brycki’s choice to diversify with gold, against Pat Garratts’ choice to diversify with property and infrastructure.

I added $10,000 to this portfolio in December, with a clean 50:50 split between the two.

Stockspot

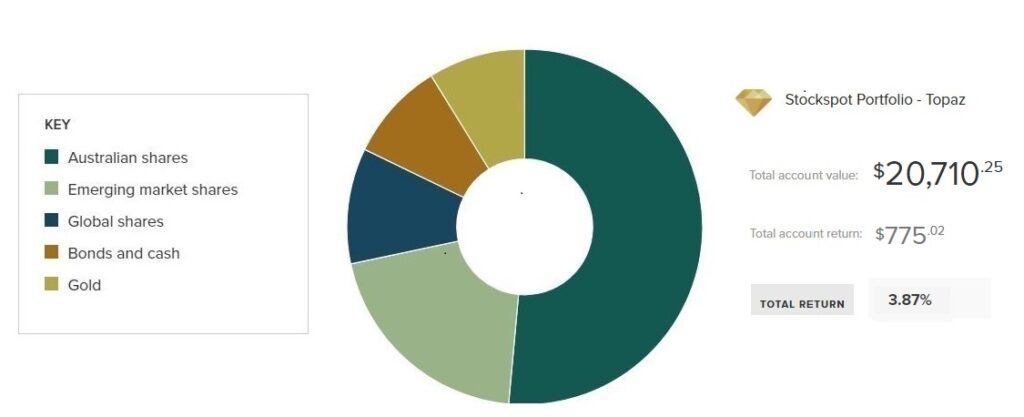

After a successful trial with the Stockspot roboadvisor platform where they allocated me the Topaz portfolio (which is their most aggressive portfolio), I have increased the balance to $20K by investing another $5000 in December. One thing I would like to see is a total annualised return feature rather than just a total return (which may already be available and I haven’t just figured out where it is yet) because it will make a comparison with other investments a bit easier.

If you want to learn more about Stockspot, check out the dedicated review I did on Stockspot – which I will be keeping updated with all the lessons from my personal use trial. I am trying to get the Stockspot podcast out this week too, which will be great to have live.

SixPark

The Six Park online investment is going well too, this month again showing higher returns than Stockspot – now over double the total return of Stockspot. I expect SixPark to outperform during bull markets where stocks and property go up, but potentially to underperform Stockspot in Bear markets because Stockspot will likely use their gold to strategically rebalance and buy shares at a discount. So it probably will take a few more years or a market cycle to tell which fund manager performs best (both in terms of total returns but also in terms of risk adjusted return). But again, no one has a crystal ball, and this is why I decided to split my eggs into these two baskets to diversify and see how the experiment plays out.

Cryptocurrency Portfolio

I purchased another $270 of Bitcoin through Coinspot, there has been a correction but as the graph shows it is still growing nicely from the start. I would like to see an ‘annualised return’ function on the crypto so will be pestering Sharesight soon to connect this for me (because the native graph in Coinspot only shows total accumulation and doesn’t factor in that you have kept adding money along the way).

I did a podcast episode on Bitcoin with Stephan Livera if you are interested to learn more about it, and also recently did an interview with Andrew Fenton from the CoinTelegraph where we talked a lot about crypto and its application on the Financial Independence Journey. The Aussie Firebug has just released a great episode with Vijay Boyapati (Author of the Bullish Case for Bitcoin) which is well worth listening to – https://www.aussiefirebug.com/vijay-boyapati/

Micro-investing Portfolio

I have been playing with a few of the biggest microinvesting platforms mainly just as research for the blog, because I want to see how they all stack up against each other, and against the other portfolio’s in terms of % gains. It is now really starting to add up – especially because of the Tesla stock pick!

I have added Commsec pocket to the mix (where I opted for the Nasdaq tech ETF NDQ) as well as Bamboo where I opted for the cryptocurrency 50:50 BTC:ETH option, with an $100 investment in both. I am still waiting for the accounts to finalise so I can get screenshots etc which I will provide in the next months update.

Stake Invest

Stake has been an easy way to buy US shares brokerage free, however I am not really a stock picker. I got lucky on Tesla and I am glad I own a huge chunk of it with my VTS index fund through Pearler. I will keep adding to my Tesla stock when I earn in USD so I don’t have to pay the currency conversion fee.

This month I also wanted to explore the Australian trading function of Stake which was free to use at the time (and will only cost $3 for CHESS sponsored shares from 1 Jan 2022 onward). Whilst this technically makes them $1.45 cheaper than Pearler per trade, they still lack the proprietary ‘Auto invest’ automated investing feature that Pearler developed which makes long term investing much easier and more likely to succeed. Stake is definitely more geared toward someone who wants to trade rather than invest for the long term, and there isn’t anything wrong with that – AUS share trading is pretty slick and easy to use on Stake (but I find the US share trading pretty slow and clunky because I just have the basic free version).

I opted for the Lithium ETF ‘ASX:ACDC’ because of a group consensus recommendation on the Financial Independence Australia Facebook group. I saw how well Tesla was doing and I personally think the Lithium industry should be well placed for the EV revolution. Whilst this goes against my core index ETF investing strategy, it forms part of my satellite thematic investing. I still benefit from the ETF model and diversification which reduces some of the risks of individual stock picking, but it is a much higher risk investment than a basic total market index tracking ETF.

Raiz Invest

Raiz aggressive portfolio – good split of ETFs, and a cheap option for small-ish balances at only $3.50 per month. To be honest the fee’s are more than my investment return, but it is worth it just for the Raiz rewards – you get discounts on various things, plus round ups from spending and the occasional affiliate click sign up bonus usually more than covers any fees, making it a weird pseudo-investment-pseudo-savings kind of account for me. I’m going to keep going, and once I reach about $1000, I think the investment returns should start to cover any fee’s and it will grow quicker. I like Raiz as a way for people to ‘get their foot in the door’ with investing, as it can be really helpful for beginners.

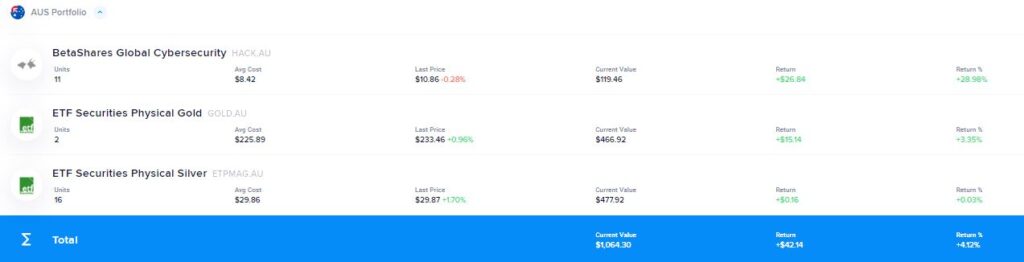

Superhero Trading

I didn’t do any trading on Superhero this month, just let the ETFs do their thing. Everything is up this month, with the silver basically moving sideways, and the HACK shares in the lead. This screenshot can be misleading however as it doesn’t give a true reflection of total performance. No brokerage firm really does this properly, so you have to use Sharesight to make it properly count for dividends and capital growth (and quirky things like share splits or franking credits) to get an accurate annualised return figure.

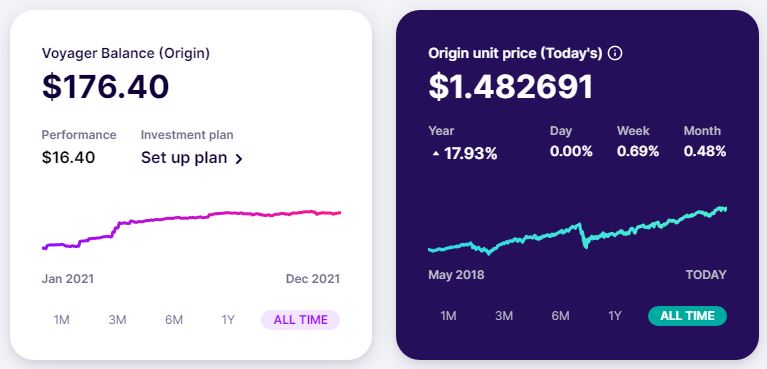

Spaceship Voyager Invest

Spaceship Origin portfolio: Top 100 Global Blue chip ETF. This seems to be chuffing along pretty awesomely with nearly 18% return, but If I am honest, for a speculative punt I should have probably gone for the Universe portfolio which seems to be growing faster (but it is volatile) – I am hoping the origin portfolio might be more stable. Still, not complaining about 18%!

Plenti P2P lending

Plenti Peer to Peer lending account. I backflipped on my decision to axe Plenti, and instead reinvested all my holding account out at 1.5%. You can pick the rate you want to lend it out at. Whilst I was frustrated at a lack of performance, I think its a good idea to keep a little bit of cash and my bank is basically paying zero interest so at least in Plenti its better than nothing. If you decide to lock it up for longer periods you get a higher rate of return, but I just do the rolling monthly option so I can get access to it quickly.

Investment property

OK we have progress – the building is enclosed! This means we have four walls, a roof, windows and doors, and last months defects are being corrected.

The project manager is telling me that it will be completed in the first half of 2022, so I am assuming I can have a tenant in by the end of the financial year, which will be awesome.

Having a year or so of rental returns will make it easier to apply for finance for when I buy the farm, and I may be able to effectively borrow against the IP and ‘suck out’ the equity from the IP so I don’t have to stump up such a high cash deposit (I will probably need at least a $200,000 deposit).

No photos this month, but I did have the pleasure of starting to pay more interest as the building company has started to be awarded progress payments by the bank.

I won’t say I am super confident about the rest of the project given all the high stress SNAFU’s encountered to date, but I think we are beginning to see the light at the end of the tunnel as it nears completion.

Rolling lessons learned:

It has taken a long time to get to this point, and boy have we made some embarrassing mistakes. Rolling lessons learned include but are not limited to…

- Thinking we could save money by NOT using an architect on a house and land package we bought from a developer *WITHOUT DA* from council

- Falling for the oldest trick in the book re: portable fencing hire (the fencing hire company stole the fences back and then tried to charge us for having them stolen)

- Endless delays by not having DA and needing to relodge with council three times meant we were one of the last blocks to be built on, and hence became the neighbourhood ‘free rubbish dumping ground’ when the fence was “stolen” (we then had to pay to get the rubbish removed and pay tip fees for – a big fuck you to any dodgy builders reading this who have ever engaged in this practice)

- Because we were the last to build, the ‘new neighbours’ objected to our build being two story due to shadowing – and we were forced to build single story instead at a reduced profit margin.

- COVID-19 delays, subsequent supply restrictions and union activity meant the builder essentially got a free pass to break contract schedule, putting us back by an extra six months with no penalty, compensation or damages payable – this further took money away from the ‘bottom line’ as we had to pay more interest, had capital tied up, and was not earning rental income – all making the build less profitable (would have been better to stick money into index funds)

- Lots of small (but not insignificant) expenses such as council fees, independent inspection fees and rates (even though the house isn’t build apparently you still have to pay rates…) add up to significant amounts over the project lifetime. I was amazed to see just how everyone gouges you for things you don’t even think about, and brokers / builders don’t mention.

- Independent inspections and checks are worth their weight in gold. I am talking design and plan reviews, soil tests, site inspections, construction and building inspections etc. Do not cheap out or try to skip these, and don’t trust anyone or any builder – they are very cheap insurance and great piece of mind and give you (legal) leverage over the builder, especially if someone is trying to pull the wool over your eyes.

I have not changed any of the valuations, still going off the banks final completed estimation of $560K, and with the mortgage the way it is at $370K leaves me with about $190K of equity in the build, meaning we currently make just under $70k of ‘manufactured equity’ with an investment of $120K over two and a bit years (not all of the cash was required upfront). This is an approximate projected annualised return of about 15%. This will come in handy after completion and tenancy as I will likely be able to access some of this equity during a refinance towards buying the dream farm in the Adelaide Hills. Not sure how refinancing is going to go given I am not flying anymore (but hopefully may be able to finance based off website income). When the build is finished and tenanted I will do a full article explaining everything and try to calculate the total costs and profit.

With the general upward trend of property values in the area, I am hoping we can get it revalued on completion at higher than $560K (I believe some similar properties in the area have been going for $600K+) which would be awesome and would offset some of the pain and suffering of building an IP during COVID-19 pandemic.

Online Business (websites)

It was good to see traffic recovering across the portfolio. Whilst this blog got smashed with traffic down to about half of its peak (mostly due to me being lazy – not spending enough time updating articles or posting new content or podcasts because I have been too busy with other ‘life’ stuff and working on other sites). Some of the other sites went crazy good and quadrupled their traffic (and thus earning with AdSense and affiliates) which was awesome, but I still want to diversify the income by adding more websites such that if any of them do get hit by algorithm updates, the income supply is still somewhat stable from other sites. Diversification in the same way I get from using index ETFs to invest.

I am building a template site, have done my keyword research for the next ten sites and am ready to buy the domain names and upload the ‘generic template’. After that, I will get the graphic designers to do up all the logo and design work, and begin outsourcing the work of converting the template into a functional site by the addition of unique content. Hopefully in 12 months, these sites will all have traffic in the thousands per month and be ready to monetise.

I learned these skills through the eBusiness institute – I have done a pretty comprehensive review of the eBusiness institute as well as interviewed Matt and Liz Raad about this on the podcast about online business and websites if you want to learn more about this lucrative side hustle. They provide a free introductory course for CaptainFI readers. I have also recently interviewed Liz Raad again on the pod about entrepreneurship, which is live now.

Angel Investing

Currently I have made an ‘Angel Investment’ in the Financial Independence brokerage company Pearler. This was the maximum allowable private investment of $10,000 (AUD) made in July 2021 with the number of ‘private equity’ shares based on their June company valuation.

This helps to fund Pearler’s capital investment pool and lets them grow and build their business – which is great for me since I have nearly $400K invested through them and I trust them to automate my investing for me.

As Pearler grows and builds its revenue, it will get an increasingly higher company valuation and my private equity will grow accordingly (i.e. it is not a free $10,000 loan, it is a $10,000 investment where I am buying a slice of the company).

Whilst this doesn’t align with my general investing philosophy of index investing and diversification, I feel I have a unique insight into Pearlers organisational and company structure and build a great rapport and trust with their executives, and I believe in this company and its genuine intentions to help people reach financial independence.

Also realise that while $10,000 does sound like a lot of money, but this is a small overall percentage of my total investments so my personal risk is actually quite low, and I would not encourage anyone to go out and make $10,000 Angel investments into tech startups. It is generally quite high risk (high risk = high reward). Make sure you don’t compare your financial ‘race’ with others (just think of it like a time trial where you are only competing with yourself).

The valuation of Pearler has gone up which is good, although I am not really sure what that means for my investment, I guess it has gone up, but I haven’t been told anything ‘official’ from Pearler yet.

Precious Metals

Gold has gone up by about 4% and silver has gone sideways – Kinda wishing I had put this into Tesla stock instead! But this will be a long term play, so we will see how it goes, the theory being when stocks do eventually correct or crash below 20%, I will sell the gold and silver and buy shares. Vice versa, whilst shares are doing really well I should technically be buying more gold and silver (or even selling shares to do so), but I haven’t worked out my ‘buy’ side of the equation yet.

I need to sit down and do a proper plan and asset allocation – a few percent to gold and silver, a few to bitcoin and ether, and then just do a quarterly or biannual rebalancing. Because I haven’t had to sell any shares yet I am continuing to rebalance by purchasing.

I added ACDC which is a lithium stock – not technically a ‘precious metal’ but a very useful one nonetheless with the EV revolution going on in the automotive word.

Cash / emergency fund

Sitting on a total of about $10K in the EF split across the various bank accounts, P2P lending and bond. This has been helpful as I have had a few big expenses lately such as the puppy, and my dogs upcoming cancer surgery. I recently had an epiphany / moment of clarity where I realised I pretty much have enough money to cover almost anything and everything I ever want, without resorting to taking on debt. Which I am very appreciative and grateful for.

Captain FI net worth progression

The net worth progression graph is rather crudely constructed in Excel, but still demonstrates the ‘somewhat exponential’ journey over the past 14 years. You can access the archives for my Net Worth updates here to see how its gone over time.

Again I feel incredibly privileged that this started from ZERO, rather than from a negative. Unfortunately, a lot of people need to overcome a negative net worth whether that is due to student loans for their education or perhaps poor decisions with credit cards etc. This is a huge testament to how amazing my mum is and all of the sacrifices she made to support our family and prioritise our education, which allowed me to achieve so well during my final years of high school and ultimately score a scholarship at university (I got paid to study!).

| Date | Net worth | Difference | Saving Rate | Notes | |

| Jan 09 | $5,000.00 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK | |

| Jan 10 | $24,000 | +$19,000 | ? | Estimate NW | LINK |

| Jan 11 | $40,000 | +$16,000 | ? | Estimate NW | LINK |

| Jan 12 | $92,000 | +$50,000 | ? | Estimate NW | LINK |

| Jan 13 | $130,000.00 | +$38,000 | ? | Estimate NW | LINK |

| Jan 14 | $161,000.00 | +$31,000 | ? | Estimate NW | LINK |

| Jan 15 | $200,000.00 | +$39,000 | ? | Estimate NW | LINK |

| Jan 16 | $281,000.00 | +$81,000 | ? | Estimate NW | LINK |

| Jan 17 | $340,000.00 | +$59,000 | ? | Estimate NW | LINK |

| Jan 18 | $482,000.00 | +$142,000 | ? | Estimate NW | LINK |

| Jan 19 | $542,000.00 | +$60,000 | ? | Estimate NW | LINK |

| Jul 19 | $578,900.00 | +$36,900 | 84% | Finally began tracking NW this like a proper adult. | |

| Aug 19 | $560,100.00 | -$18,800.00 (-3.2%) | 78% | Share market slight correction, Ok savings. | |

| Sep 19 | $584,744.88 | $24,644.88 | 72% | Share market rebound, savings rate not so good. | LINK |

| Oct 19 | $600,386.00 | $15,641.12 | 84% | Good saving this month. Normal salary, plus allowances, dividends from index funds, tax refund, eBay selling and was working abroad in asia where things are cheap. | LINK |

| Nov 19 | $612,917.21 | $12,531.21 | 76% | Falling short of my savings goal of 80%. Mostly domestic legs this month with higher costs. Also invested in hydroponics. | LINK |

| Dec 19 | $625,350.00 | $12,432.79 | 76% | Good savings of cash (for development) and investment, however higher spending due to Christmas period (Travel and Gifting). | LINK |

| Jan 20 | $865,212.00 | $239,862.00 | 55% | Super settlement was a HUGE boost to NW. $9K growth from stock market. Expensive month lots with lots of unexpected bills – weddings, travel, Booking flights, fines etc. | LINK |

| Feb 20 | $851,802.0 | -$16,592 (-1.9%) | 52% | Large increase in spending on myself this month, still managed to tuck away $5K to put into shares and property. Corona Virus market scare resulted in a correction and gave NW a small negative trend. Time in the market not Timing the market! Became Single again. | LINK |

| Mar 20 | $819, 354.6 | -$31,806.95 (-3.7%) | 80% | Another small step backwards in the NW due to the ‘corona crash’ in full swing. FIRE Portfolio of ETF/LICs down about 15% this month, however due to high savings rate and structure of my superannuation annuity the NW is only down 3.7%. Savings rate good at 80%, higher than usual income (with some slightly higher spending, too). Picking up shares on discount – this is the best outcome for someone in the accumulation phase with good income! | LINK |

| Apr 20 | $847,023 | +$27,668 | 85% | $11,000 in rebound of stock market capital prices alone (up 6%), plus first quarter dividends paid (heavily reduced due to banks withholding dividends). Great savings rate due to COVID-19 lock-down = no spend. Increased entrepreneurial efforts and selling down of physical possessions provided side hustle income. Two standard paychecks from flying activity; domestic day trips only so no allowances. All cash unfortunately had to go into the property development due to contract timing, I am chomping at the bit to buy some more index funds before they go back up in price too much – hence why I am selling most of my toys! | LINK |

| May 20 | $857,859 | +$10,836 | 92% | Some Great sales as I let go of my Super Sport Motorcycle, Some gym gear, expensive flying equipment and a few other various bits and bobs and invested this money. Flying still reduced, but increasing from April. The share market grew as I continued to make my fortnightly investments. I also wrote down the ‘value’ of some of my possessions (liabilities) such as my car, tools and furniture by around $10K to align them to market price (“tell him hes dreaming…!”). | LINK |

| June 20 | $858,650 | +$791 | 90% | Small Net Worth gain as I continue to declutter and simplify my life, despite being off work due to a family emergency. Share market not doing much. | LINK |

| July 20 | $888,218 | +$29,568 | 68% | Majority gain due to share market going back up, low spending due to being on the family farm and at home because of lock down. | LINK |

| Aug 20 | $1,029,293 | +$141,075 | 74% | Became a millionaire. Achieved this massive milestone I set out for myself in Dec 2019. Included unrealised gains in my property development as well as website business. Good savings rate due to not much spending, invested in Aus and total world shares. Investing in my web business. Starting to shift focus away from $$$ and more into looking after my mental health. | LINK |

| Sep 20 | S1,045,486 | +$16,193 | 60% | Officially took time off work for the rest of the year to be close and look after family during major operations. Continued to sell down physical possessions and work on digital business while at home. NW gain mainly due to valuation of websites. | LINK |

| Oct 20 | $1,064,399 | +$18,913 | 80% | Base income (retainer) and leave loading, dividend and websites provided income, as well as raiding my P2P lending capital. Significant bill for property due to design not meeting standards which effectively lowers my equity position, as well as fence being stolen. | LINK |

| Nov 20 | $1,143,433 | +$80,394 | 82% | Big gains came from share market growth (influencing both the Financial Independence share portfolio and Invested superannuation), Business gains (due to increased earnings) and a $30K boost to my annuity thanks to me logging in and checking the fine-print on the accumulation stats. I only invested around $7K. Insane that in one month, I accumulated nearly more net worth than I did in four years from 2009-2012 | LINK |

| Dec 20 | $1,152,920 | + $9,487.32 | 84% | Share market slight drop, Earnings from Business, Contract work, Selling possessions. No share market investments this month (oops! I forgot and money was tight). Invested a lot into the website business this month (way more than planned) and it is still running at a decent loss (plans to turn it cash flow positive in 3 months). | LINK |

| Jan 21 | $1,165,678 | +$12,757 | 79% | Great returns from the share market. Earnings from Business, Dividends, Flying wage, flipping items on consignment. Regular share contribution, investing in micro investing platforms, P2P lending, Investment property and big reinvestment into the business (still running at a loss) | LINK |

| Feb 21 | $1,135,272 | -$30,406 | 76% | Significant write down on property development due to council DA rejection and redesign requiring more money and creating less equity. Offset by small increase to Business value and investments. Simplified my investments and switched over to Pearler. | LINK |

| Mar 21 | $1,155,594 | +$20,322 | 71% | Continued investment into the portfolio as well as growth of investments and business. Gave my notice at work and looking for part time job at home for ‘Barista FI’ | LINK |

| Apr 21 | $1,242,220 | +$86,727 | 74% | Property development back on track | LINK |

| May 21 | $1,379,469 | +$137,248 | 72% | Massive gains in the website portfolio due to revaluation based on recent business income, big growth of superannuation due to annuity increasing (salary increment) and shares generally went up. Crypto went down by about 40% or so. | LINK |

| June 21 | $1,469,989 | +$89,757 | 41% | Quit flying role and moved to Adelaide. Great month for investments, websites producing serious income so accordingly they are valued higher. Spent a lot on furnishing the new apartment and on enjoying some more luxuries. Seeing a therapist to help deal with anxiety from leaving work. | LINK |

| July 21 | $1,543,959 | +$74,732 | ??? | Set myself up in Adelaide. Did basically nothing for the whole month except spent time with family, relax, sleep and go to doctors appointments. Massive boost to website portfolio AdSense and affiliate incomes, as well as general share market performance. | LINK |

| Aug 21 | $1,624,116 | +$70,156 | ??? | Relaxed again, focused on mental and physical health, and spending time with family and my partner. Big increases to spending (too afraid to calculate a ‘savings rate’) but also big increases to NW through website portfolio income growth. Finally got the slab poured on the investment property (foundation). | LINK |

| Sep 21 | 1,640,663.85 | +$16,547 | ??? | Stocks, super etc went down, but business income from websites increased, plus business valuation increased. Property build. got to frame stage, and I also got a dog! Expenses for vet surgery well worth it. Moved into a nicer apartment | LINK |

| Oct 21 | $1,705,907 | +$65,243 | 30% | Big boost from website valuation due to securing new affiliate contracts for recurring income, shares went up nicely. No massive changes to this month. Calculated a savings rate and found myself pretty low due to spending a lot on my garden and going out quite a lot – I don’t think I will calculate this savings rate figure any more. | LINK |

| Nov 21 | $1,739,144.23 | +$33,236 | N.A. | Great month. Relaxing (somewhat). Spent a lot of money doing ‘fun’ things like winery tours, a fine dining experience and self education. Shares moved sideways (well slightly down) but everything else went up. Building got to enclosed stage (roof, walls, windows and doors) but have had some issues with build quality and weather / covid delays. Put a $1000 deposit on the puppy. | LINK |

| Dec 21 | $1,764,516 | +25,372 | N.A. | Spent nearly the whole month with family, did some work on the website portfolio. Traffic recovered from google algorithm changes. Invested $10K into Stockspot and Sixpark, $1K into ACDC, $100 into Comsec pocket and $100 into Bamboo, $260 into BTC, $4K into ETFs through pearler. Paid the $3000 balance for the puppy. |

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

You’ve certainly had a year to remember – and to move on from!

I’m in the process of moving my blog hosting to the company you recommended – it’s stressful when they keep asking me to supply things that I don’t know about! Finally I handed my laptop to my son and asked him to deal with it – hopefully the migration will happen in the next few days and all will be well again!

I have 2 Cavaliers – your Cocker Spaniel will be the heartbeat of the family. 🙂

I was wondering about VEU and VTS too. I’ll be interested to read your conclusions.

Happy new year!!!

She’s a week in and already everyone is just so in love with her! I have a hunch that VGS might just be the more sensible way to go given its aus domiciled and the MER is less than the ‘effective MER’ of VEU and VTS, so I think I may just start going for that in the future, but wont be in a rush to sell VTS or VEU because of the capital gains tax, I’d rather defer that infinitely haha

Congratulations on the continued upward trajectory. Can you please explain the inflation effect on returns in more detail? Or link me to something you recommend reading? I hadn’t factored this into my own investment return calculations.

well as the government prints more money and banks create more credit, there is more currency. This devalues the value of a dollar, and things then go up in price. RBA usually aims to keep it around 1-3% or something. But with all the quantitative easing money printing and low interest rates creating credit, we are seeing higher inflation across the world than usual. Your investments must obviously create a return above inflation for them to go up in value not down, so you have to subtract inflation from your return to consider its real purchasing power, and the shitty thing is you then get taxed on the higher number, not the *real* purchasing power of that return.

Thanks for the extra info. So, on investment companies websites (e.g. Vanguard) when they show the rate of return, it doesn’t factor in inflation, fees, taxes?

exactly mate, some may do, but most show returns without factoring in inflation, taxes and fees. Some will include a separate return accounting for franking credits, but usually the PR people just spin it the best way possible to try and inflow more funds to their pool