October is over and Christmas fast approaches; a quick examination of Google Search Console shows that Mariah Carey’s ‘All I want for Christmas’ inquiries are starting their yearly spike, signalling that retailers globally are cuing up their Christmas playlists – much to everyone’s disgust. Nothing terribly exciting happened for me this month – I continued to make my regular investments into the share market, received some sweet dividends into my bank accounts, and even started to sort out sponsorship (through advertising) for this blog and some of my other websites. I continued paying into the property development, and had some horrendous bills associated with poor design requiring re-design and higher than agreed upon consruction costs. Overall, I have enjoyed the slower life: reading, writing and recharging my batteries at home with the family.

October update

October for me was a very relaxed month. I spent a lot of time at home reading, writing and babysitting the family younglings – free practice for becoming a Dad, right? It doesn’t even matter if I stuff it up because I just hand them back to their parents at the end! In all seriousness though, I reckon I am pretty bloody good – I am the exciting Uncle that teaches them how to make fireworks, lets them destroy the enamel on their teeth with warheads and sour lollies, and takes them out to cool places.

A fair bit of time was spent with my old man, his health continues to decline as he progresses through his Chemotherapy for leukemia. Unfortunately some complications have been vascular issues (lack of blood flow) which have severely threatened his life twice now, requiring urgent surgeries. He has been in and out of the hospital it seems for months – vascular surgery, heart operations and unfortunately some amputations. It is pretty confronting stuff, and he has now developed diabetes that he refuses to acknowledge which further complicates things (especially when eating sugary junk comfort food). Nearly 70, after a life time of smoking, poor diet and alcohol abuse, there isn’t much I can say or do to change his behavior now. So I just try and sit with him, and give him healthy food to eat. Not much else can be done or said, really.

Mum is still pretty nervous about going in for a major operation soon, too. Thankfully we have sorted out her Superannuation (rolled it over into HostPlus index funds) as well as applied for a lump sum to be paid out which she is using to pay off her mortgage. Having her finances sorted has put her mind at ease, and we are slowly working on getting a few major projects sorted at home – like hooking up the new 20,000L rainwater tank, putting in the new chicken coop boundary fencing, adding more fruit trees to the orchard and upgrading the solar panel system on the roof.

I’m not too sure how much longer the family dogs are going to last either, the old girls tend to just do a lot of sleeping these days. I have been getting arthritis / pain medicine for them just to help them have a better quality of life, but at 16 and 17 years old they have done well to make it this far. They are still occasionally frisky and playful, and always wag their tails furiously and are happy for any attention or treats. Walkies only go down the path and back now though, and outings further afield need to involve the car and some level of carrying them. I know in the near future there will come a decision for the welfare of the dogs which is to let them pass. But even just thinking about it now makes me well up, so lets change the subject.

After what feels like too long, I have also started dating again – I forgot how both exciting and crap dating can be in your late twenties. To speed the process up I enlisted the help of a few dating apps – which have had some wins and some epic fails. Apart from being cat-fished what feels like six hundred thousand times, I have actually met some really nice girls out of it. Because of this, my first dates are usually super super casual – take-away coffee and a walk through the park or something similar. If it goes well, then progress to dinner and drinks, a picnic on the beach or something ridiculous like hiring a plane (and forgetting to tell them its aerobatic and capable of going upside down mwuahahahahah!). I figure you get ‘three for free’ – which means you go on three dates to get to know someone better before you have the conversation about where its going and exclusivity. That kind of feels like the sweet spot for me – what do you think?

After some expert stratagems from my online readers, I have sort of been patiently treading the line when it comes to talking about the future – After a few dates I make it clear that I am looking for the right person to settle down with though. Without being too blunt, I also try to subtly drop hints about investing, running a business, the whole Financial Independence thing and maybe turning in my wings for the shot at starting a family and being a Dad.

So far though, it hasn’t really gone anywhere. A few of the girls I dated didn’t want to have kids (or unfortunately couldn’t), or we just didn’t vibe, both of which is a deal breaker for me. Some close friends suggested I hang out at Church, and go to Hillsong when I get back to Sydney to find a Christian wife… Does that mean I have to give 10% of my dividends to Dave Ramsey the Church?! Religion has never been a deal breaker for me and I accept people come from all walks of life – I wouldn’t call myself religious though – maybe spiritual (without trying to sound like a wanker?).

I have been doing some more interviews lately, doing some profiles such as with Steph and Sarne for their Frugal Beans Blog, as well as a podcast interview with team from WeMoney on the Money Bites Podcast, as well as explaining to them some of the most influential finance books I had read on my journey to FIRE. I have also been doing a heap of recording for the CaptainFI podcast.

Finally, I have had some really great conversations with my friend The Hippie Investor (@the.slow.fast on Instagram) about the concept of FIRE and why certain people might want to latch onto the idea more than others. Our concept was, maybe that people that have had unstable or uncertain lives (particularly childhoods) such as missing out on having certain authority figures in their upbringing, can tend to crave the structure and certainty that FIRE can provide.

The same could also be said for people that have been subject to abuse or other trauma, and this can make the concept of FI/RE become highly romanticized in our minds and cause us to be a bit predisposed to becoming obsessed with it. Like if we finally reach Financial Independence, it will solve all our life problems. I think there are certainly worse things to obsess about, but obsessing about anything isn’t healthy. I have certainly tried to step back a bit and ‘loosen the purse strings’ so to speak to try and enjoy a bit more of the here and now, rather than fantasizing about the future and the mythical day I reach FIRE when my life will suddenly be amazingly happy and fulfilled.

Recently chatting to Dave from StrongMoneyAustralia as we recorded episode 10 of the CaptainFI podcast, it was great to air out all of these concepts. Dave reinforced that FI/RE to him meant he could live every day like it was the weekend, and so it is important to still enjoy your life (especially your weekends) on your journey to FIRE. Dave recommends having a list of hobbies and things you enjoy that you can look forward to doing more of when you do hit FI, and not flogging your guts out just to get there a few months quicker. I think this is great advice, and I have been trying to follow it lately.

End of financial year tax return is still outstanding…

When I am back home in Sydney, I will print the Sharesight tax summary for my investment portfolio and then take it down to my local tax accountant, pay $300 and walk away with an estimated $5,000 tax return. I am not ‘banking’ on getting this return, but when I do get it I will just be using it to buy more index funds. Or maybe a new motorcycle – I have been eyeing off something like a Street Triple!

Saving rate

My Saving rate was 80.1% in October which actually shocked me since my wage income was significantly dropped (finished up all my leave loading and now taking half unpaid leave) and I thought my expenses had gone up significantly. It turns out I actually made enough extra from Dividends, Selling my stuff, income from the website portfolio and raiding my P2P lending stash to boost me up to actual working levels of income!

Income

Income included my base salary and leave loading, Dividends from the FI portfolio (about $1500), Money from selling my possessions, revenue from the website portfolio (mainly affiliate sales and advertising through google Adsense) as well as withdrawing my money from my Peer to Peer lending account.

Spending

Spending was significantly up in October. In addition to paying for an empty apartment in Sydney, I have been contributing towards the family household back home. As I mentioned earlier, I have been getting back into the dating scene and had quite a full ‘Dance card’ so spending has increased for things like coffee dates, drinks, nice dinners, movies and things like fancy picnics and bottles of champagne. I have also been going out with the family more, taking the kids out to the movies and on adventures, as well as family dinners and functions. Whilst I try to prioritise things that involve nature and that are low cost or free (like going to the beach or going on a hike), these things always end up costing a bit of money – and that i fine, its all part of enjoying yourself. Whilst I am not including money I have technically ‘reinvested’ into the website portfolio as spending, this has also been a factor as I begin outsourcing certain tasks and paying for tools to make my life easier.

Investing decisions

This month I allocated $8,649 between the property development, mandatory superannuation contributions, my online businesses and shares.

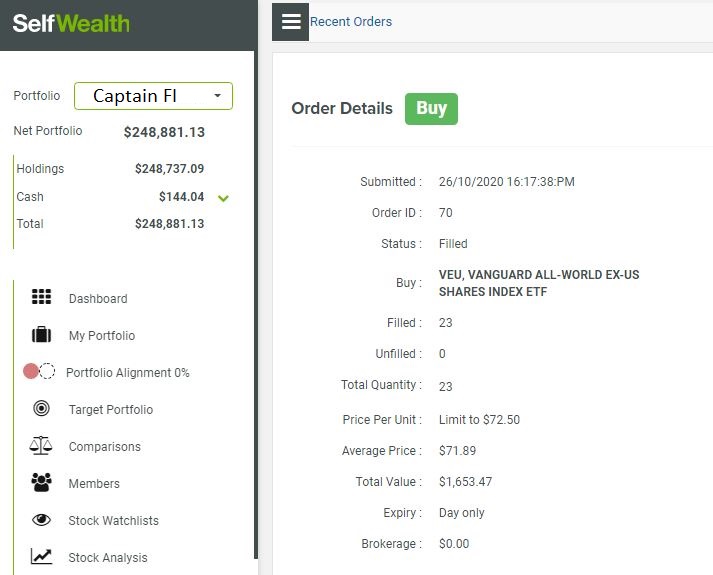

$1,650 went into the share market this month through SelfWealth with a purchase of 23 shares of Vanguard Total US Market index fund (ASX:VEU). This was because it was one of my lowest splits and I also saw it had gone down more than the other shares in my portfolio.

Property

I paid $4,776 into the construction fund, as well as $1000 into the mortgage fund. More on this below…

P2P lending

Due to my financial situation, I unfortunately needed to actually take my money out of Plenti account. I did get $7.86 of ‘interest’ while I had it invested with them, and once I am earning good money again I will look to put a portion of it back into P2P lending.

Business

$500 went into paying for various costs for the buisness.

I recently set up my trade confirmation emails between SelfWealth and Sharesight, which means my portfolio accounting is completely hands free. I simply log in to confirm all the trades and dividends over the year when needed for my tax return, or to produce these monthly updates for you guys. The following section contains Sharesight reports for;

- Monthly

- Financial year to date

- Rolling 12 months

- Since Inception (since I started tracking it with Sharesight).

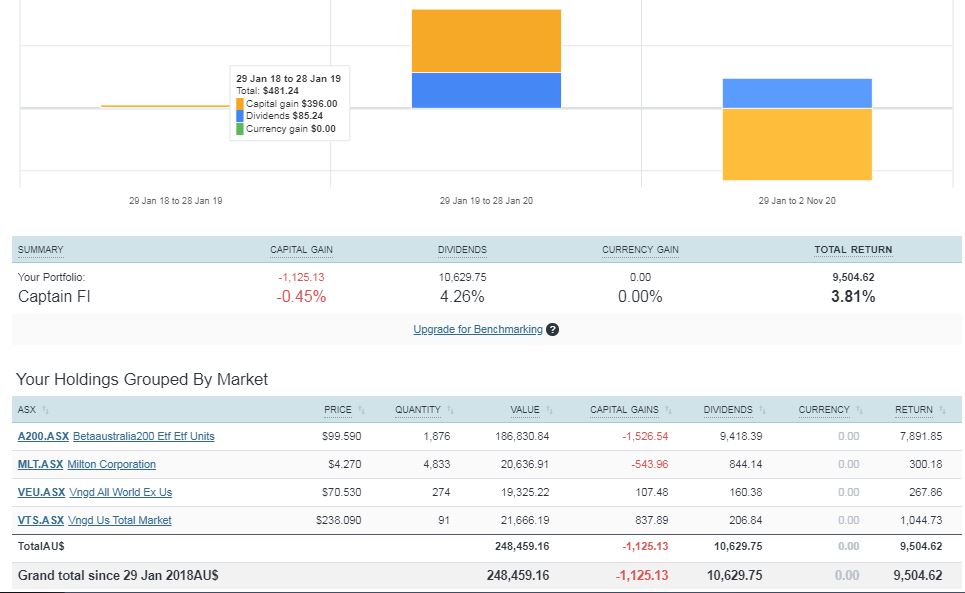

From the Sharesight reporting, the portfolio is overall up by 1.34% in October. For some reason, the dividends I got in October are not showing up in the rolling 30 day window (probably because they were technically distributed earlier in the year but only hit my account in October) but they are showing up in the longer windows which covers their distribution date. I am happy with this, and plan to continue my buy and hold investment strategy.

This financial year to date has shown a small gain as the market continues to recover from the COVID-19 crash, despite its subsequent drop in September.

The rolling 12 month figure shows the impact of the COVID-19 crash early in the year, but also that the power of dividends has helped to offset the capital loss, so actually be in a position slightly above breaking even.

This is the total return since I started using Sharesight to track my portfolio, and switched to a core holding of A200, VTS and VEU complimented by LICs (currently Milton). In the grand scheme of things, this isn’t really a long time at all. What I love about it is the simplicity and automation though. Dividends drop into my accounts randomly, and make for a nice suprise, and then I can choose to either spend them or reinvest them to grow my passive income stream. I knew there would be some kind of market correction, but couldnt say when, where or by how much. So instead of trying to fight it and time the market, stressing over when to jump in and out, I just tanked the hits and continue to invest. In the long term, I think this is the best strategy.

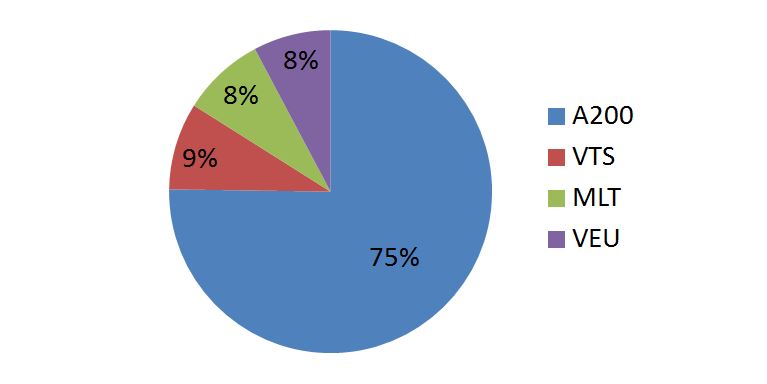

Pie chart

Because sometimes you just need a pie chart to visualize what a portfolio looks like. Clearly I am overweight on Australian equities – taking on higher portfolio risk to chase franking credits. Over time, I will expect to invest more into VTS and VEU to bring

Investment Property

The builders mucked up the environmental requirements on the plan, meaning we needed to redesign the windows and this will cost an additional $8,000! Safe to say I am pretty annoyed.

Furthermore, it has dawned on me that the people that stole the fence are most likely the company we hired it from – Unofficially, I have heard from my builder friends and police friends that this is fairly commonplace in the building industry. Of course, no one would want to admit this publicly though.

We still don’t have DA yet, so fingers crossed. Also waiting on getting a contract from the builder to state there will be no more variations to the design moving forward. I am guessing this will be more of a money pit as we move forward, but it will be worth it in the end. I am still hoping that this will be sorted this year and the slab can be poured in the train wreck that has been 2020.

Until the project is completed obviously there is no tenant and no rent, so I will be paying the mortgage interest only out of pocket. I do this at the moment by just transferring $1000 per month into the mortgage fund which should cover everything as well as build up a small buffer just in case.

P2P lending

Because of my current financial situation I needed to withdraw my Peer to Peer lending that I had with Plenti. This was unfortunate since it was a nice place to park my cash and get a higher return than I would have from my online bank account. Not to worry – when I am making good income I will explore using Plenti for P2P lending again in the future, because they seem like the best provider out there in Australia.

Business portfolio

My business portfolio includes a number of digital properties which make income from;

- Sponsorship.

- Advertising (currently using Google ads).

- Affiliate marketing.

- Digital products.

- E-commerce.

In October, the revenue increased substantially (commensurate with increases in traffic to the sites which was about 30%) – however a lot of this was reinvested back into the business. I am going to use a 3 month profit average because I think this is a smoother and more appropriate number to work with. The revenue month to month can be pretty lumpy and also doesn’t factor in the costs of running the business. In October, this figure was pretty much bang on $1000 – I have tucked some aside to pay for tax, and have taken the rest as a ‘personal distribution’ and invested it.

Conservatively valuing the web portfolio at 30x monthly profit has them sitting at a total value of $30,000. However, interestingly these sites have not been fully monetized to their full potential yet. Based off current content and future projections for growth, I would honestly not sell these sites for anything less than $1,000,000. I am not even joking. That is how profitable this industry and websites can be. I am cautiously optimistic, but I think I can probably replace my full time flying income in somewhere between 6 to 12 months the way this is going. This is such an interesting revelation on the journey to FIRE.

However, it is a lot of work. The CaptainFI blog alone has taken me somewhere around 1500 hours over the past year, and I am starting to spend an equivalent amount of time on the other sites. It is a very large time investment into creating these online buisnesses which one day might become profitable – but then again they might not be.

A different idea is to simply invest money by purchasing an online business or ‘ready made website’ that is already getting lots of traffic and is monetised. I am looking into this currently through Flippa, however I am naturally very sketpical and pessimistic so finding it hard to trust the sellers and take the leap of faith to actually buy one. This is a limiting mindset and something I need to overcome, and hopefully when I find a site I like to buy, I will talk all about the process on here.

I am obviously a little gunshy to be sharing the exact URLs and Niche that my other sites are in, because it is an industry where it is very easy to ‘copycat’ and undermine an online buisness. I will eventually fess up to what they all are, and how profitable each one is – but remember, it is pretty much no money for the first year, and then a very small amount of money as it slowly grows – it is basically the same as dividend investing (but maybe even slower!).

The way they are going and with the income they are producing (including income made by this blog!) I will need to sort out a proper business structure soon and visit the accountant – a headache I have been putting off. Usually if your hobby is earning below $10K a year, the ATO doesn’t really care, but when it starts to exceed this figure you need to get smart, keep records and see an accountant. There will obviously be some costs associated with this, but it is worth it. I never thought that websites could legitimately make so much income, and to be honest it has completely overtaken the idea of dividend investing in my mind!

Retirement

For now though, I have smashed my ‘Single FIRE’ goal of $2,000 per month, and am still working toward my ‘Family FIRE’ goal of $6,000 per month. When looking at the future trust structure, to earn $6,000 per month after tax it will more or less take $6,800 of gross portfolio income. Currently, I am still conservatively at $2,500 out of the $6,800 goal, or just over a third of the way to ‘Family FIRE’!

Of course, with the growth of the web portfolio and the increasing income stream, the 3 monthly profit average will increase and I can see this rocketing my journey to ‘Family FIRE’ in no time at all. This will also let me take profits and reinvest them into the more benign and safer environment of index funds (to grow the passive income) as well as potentially paying for the acreage on which I want to build the home for my future family house and farm.

You can read my dedicated Transition to retirement Financial Planning process article here.

Captain FI Net worth October 2020

The Net Worth pie chart is still dominated by my super. Listed in order of size is;

- Super – Annuity: $498,650 [ valued at 25x annual pension value ]

- Shares (FI portfolio of ETFs + LICs): $248,686

- Equity (Investment property): $195,470

- Super – invested fund: $74,090

- Business (website portfolio): $30,000

- Physical possessions (stuff that I own): $12,850

- Cash / Bond: $4,644

Captain FI Net Worth Progression

Tracking your Net Worth over time is one way to monitor and compare your progression to FIRE. A better way though, is to track your passive income – such as dividend income. Because that is what you are going to be using to live off if you do choose to retire early. Because of how I have my finances structured as an Australian investor with a significant amount invested in Superannuation, my NW number isn’t really all that reflective of my ability to FIRE, but I still think it is an important metric to track since its growth is representative of performance – the rate of change of net worth is more important than Net worth by itself, in my opinion.

CaptainFI Net Worth Progression – Graph

The Net worth progression graph is rather crudely constructed in Excel, but still demonstrates the ‘somewhat exponential’ journey over the past 12 years.

CaptainFI Net worth progression – table

I decided to include a Net worth table which provides a bit more information on my journey for anyone wanting to go back and see how individual years or months went at a quick glance.

| Date | Net worth | Difference | Saving Rate | Notes | |

| Jan 09 | $5,000.00 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK | |

| Jan 10 | $24,000 | +$19,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 11 | $40,000 | +$16,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 12 | $92,000 | +$50,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 13 | $130,000.00 | +$38,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 14 | $161,000.00 | +$31,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 15 | $200,000.00 | +$39,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 16 | $281,000.00 | +$81,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 17 | $340,000.00 | +$59,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 18 | $482,000.00 | +$142,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 19 | $542,000.00 | +$60,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jul 19 | $578,900.00 | +$36,900 | 84% | Finally began tracking NW this like a proper adult. | |

| Aug 19 | $560,100.00 | -$18,800.00 (-3.2%) | 78% | Share market slight correction, Ok savings. | |

| Sep 19 | $584,744.88 | $24,644.88 | 72% | Share market rebound, savings rate not so good. | LINK |

| Oct 19 | $600,386.00 | $15,641.12 | 84% | Good saving this month. Normal salary, plus allowances, dividends from index funds, tax refund, eBay selling and was working abroad in asia where things are cheap. | LINK |

| Nov 19 | $612,917.21 | $12,531.21 | 76% | Falling short of my savings goal of 80%. Mostly domestic legs this month with higher costs. Also invested in hydroponics. | LINK |

| Dec 19 | $625,350.00 | $12,432.79 | 76% | Good savings of cash (for development) and investment, however higher spending due to Christmas period (Travel and Gifting). | LINK |

| Jan 20 | $865,212.00 | $239,862.00 | 55% | Super settlement was a HUGE boost to NW. $9K growth from stock market. Expensive month lots with lots of unexpected bills – weddings, travel, Booking flights, fines etc. | LINK |

| Feb 20 | $851,802.0 | -$16,592 (-1.9%) | 52% | Large increase in spending on myself this month, still managed to tuck away $5K to put into shares and property. Corona Virus market scare resulted in a correction and gave NW a small negative trend. Time in the market not Timing the market! Became Single again. | LINK |

| Mar 20 | $819, 354.6 | -$31,806.95 (-3.7%) | 80% | Another small step backwards in the NW due to the ‘corona crash’ in full swing. FIRE Portfolio of ETF/LICs down about 15% this month, however due to high savings rate and structure of my superannuation annuity the NW is only down 3.7%. Savings rate good at 80%, higher than usual income (with some slightly higher spending, too). Picking up shares on discount – this is the best outcome for someone in the accumulation phase with good income! | LINK |

| Apr 20 | $847,023 | +$27,668 | 85% | $11,000 in rebound of stock market capital prices alone (up 6%), plus first quarter dividends paid (heavily reduced due to banks withholding dividends). Great savings rate due to COVID-19 lock-down = no spend. Increased entrepreneurial efforts and selling down of physical possessions provided side hustle income. Two standard paychecks from flying activity; domestic day trips only so no allowances. All cash unfortunately had to go into the property development due to contract timing, I am chomping at the bit to buy some more index funds before they go back up in price too much – hence why I am selling most of my toys! | LINK |

| May 20 | $857,859 | +$10,836 | 92% | Some Great sales as I let go of my Super Sport Motorcycle, Some gym gear, expensive flying equipment and a few other various bits and bobs and invested this money. Flying still reduced, but increasing from April. The share market grew as I continued to make my fortnightly investments. I also wrote down the ‘value’ of some of my possessions (liabilities) such as my car, tools and furniture by around $10K to align them to market price (“tell him hes dreaming…!”). | LINK |

| June 20 | $858,650 | +$791 | 90% | Small Net Worth gain as I continue to declutter and simplify my life, despite being off work due to a family emergency. Share market not doing much. | LINK |

| July 20 | $888,218 | +$29,568 | 68% | Majority gain due to share market going back up, low spending due to being on the family farm and at home because of lock down. | LINK |

| Aug 20 | $1,029,293 | +$141,075 | 74% | Became a millionaire. Achieved this massive milestone I set out for myself in Dec 2019. Included unrealised gains in my property development as well as website business. Good savings rate due to not much spending, invested in Aus and total world shares. Investing in my web business. Starting to shift focus away from $$$ and more into looking after my mental health. | LINK |

| Sep 20 | S1,045,486 | +$16,193 | 60% | Officially took time off work for the rest of the year to be close and look after family during major operations. Continued to sell down physical possessions and work on digital business while at home. NW gain mainly due to valuation of websites. | LINK |

| Oct 20 | $1,064,399 | +$18,913 | 80% | Base income (retainer) and leave loading, dividend and websites provided income, as well as raiding my P2P lending capital. Significant bill for property due to design not meeting standards which effectively lowers my equity position, as well as fence being stolen. |

Monthly question from the Captain

Do you know the fees you are paying on your Superannuation? Has this influenced your choice of super providers

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.