Ubank review from a long term customer, experienced investor and property owner. This UBank review is based on my personal experience as a UBank customer for over five years.

UBank review

UBank is an online bank that provides transaction and savings accounts as well as loans, term deposits and superannuation. They are backed by NAB (so could be thought of as ‘NAB lite’), and with over 600,000 customers and AUD $16 Billion under management, they have been a popular choice for Aussies looking for a no frills bank since they started in 2008.

2022 Update – uBank and 86400 combined

On 19 May 2021, the neo bank 86 400 was taken over by NAB, meaning that 86 400 is operating under NABs Authorised Deposit taking Institution licence. After NAB took over 86400, it removed the Neobank branding, and absorbed 86400 into uBank . Basically, uBank and 86400 have been merged into the same thing!

The Good

- No overseas ATM Fees

- No international transaction fees

- No ongoing fees

- No minimum balance

- Competitive interest on savings

- No interest penalty for withdrawing savings

- Offer great home loan packages

- Fantastic App with great features

The Bad

- Must satisfy age requirement conditions

- Must link to transaction account

- No branch access

- Must deposit into savings to get bonus interest

- Limited Customer support

- Difficult to get approved for home loans

- Rating of 1.5 out of 5 on Product Review

UBank do not charge ongoing fees, they have a great App with cool features and provide competitive interest rates, however they do not have physical branch access, and their customer support can be frustrating at times. All things considered, I think it is a good no frills banking product and I used them to stash my Emergency Fund for more than 5 years.

CaptainFI is not a Financial Advisor and the information below is factual review information, not financial advice. This website is reader-supported, which means we may be paid by advertising on the site, or when you visit links to partner or featured sites. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Introduction to UBank

Ubank is the budget or ‘no frills’ arm of NAB – you can think of it as ‘NAB Lite’, which is kind of analogous to what Jetstar is to Qantas. UBank has over 600,000 Australian customers and Manages over AUD $16 Billion in deposits making it a pretty big bank.

There is a number of benefits to using Ubank including zero sign up costs or ongoing monthly fees, a competitive rate of return, and in general customer support is great once you are connected with one. Overall, I think UBank is a great place to stash away your Emergency Fund or Mojo Account.

Interestingly, in January 2021, NAB announced its acquisition of 86400 Bank which merged into UBank.

UBank online transaction account – Spend Account

Spend is Ubank’s basic transactional bank account. When I signed up I received a standard VISA debit card, and this transaction account can be linked to all your smart devices such as Apple Pay etc. At the time of writing the Ubank Spend account is fee free with;

- Zero account keeping fees

- Zero overdrawn fees

- Zero ATM withdrawal fees

- Zero foreign transaction fees.

As always though, keep up to date with the latest Product Disclosure Statement before signing up.

I haven’t had any major issues with my Spend account, except when overseas trying to make transactions over the daily transaction limit (which was difficult due to 2FA not working at the time).

UBank online savings account – Save

The UBank Save account has no withdrawal restrictions and there is no monthly spending conditions to meet either. All you have to do is deposit at least $200 per month into your accounts, so it’s fairly easy to earn the bonus interest (as a little hack, you can just set up an automated transfer into and then out of your Save account each month so you technically don’t even need to be saving $200 per month).

Whilst it isn’t exactly a fantastic rate across the board for any savings rates with current interest rates, the Save with bonus interest applied is competitive with other banks and ultimately, better than nothing. The interest is capped at $250,000 (which is coincidentally the Australian government guarantee limit), but if you have this much in Cash you’re doing Financial Independence wrong.

You can set up a shared Spend or Save account with your partner of choice and get colour-coded cards – aqua for your individual Spend account, and Purple for your shared account, making it easy to know which account you are spending from.

You can keep track of your spending with your partner, get the colour coded cards, set savings goals together, and make the most of the App features together. You can also transfer into your shared account using Osko and PayID. You can also start spending straight away using your shared account, with Apple Pay or Google Pay, so you’re not waiting for the plastic card to arrive.

Customer Support and Dealing with UBank

Ubank is the budget arm of NAB – so you can think of it as ‘NAB Lite’. Think of it as being to NAB what Jetstar is to Qantas, and what Tiger airways was to Virgin. So, with this in mind – customer support is always going to be a point of friction.

I found both the web and mobile app interface to be a bit clumsy in the past, but the App and the web interface have since been updated with new features and are a huge improvement compared to a couple of years ago.

I actually found myself over in Dubai for a longer period than expected some time ago, and trying to shift money around from my Ubank account was such a pain due to the 2FA codes – which I could only receive at the time through my Australian phone number via SMS. Just when I thought I had to give up, customer support totally pulled through and was able to transfer funds for me via phone, giving me access to the cash I desperately needed. To be honest, if they hadn’t pulled through with that – I would have totally ditched them when I got back to Australia. Instead, I am still a happy Ubank customer.

Just manage your expectations and expect not to really get instant answers to emails.

You can read this article in the SMH HERE about how the bank merger caused problems for customers.

UBank App

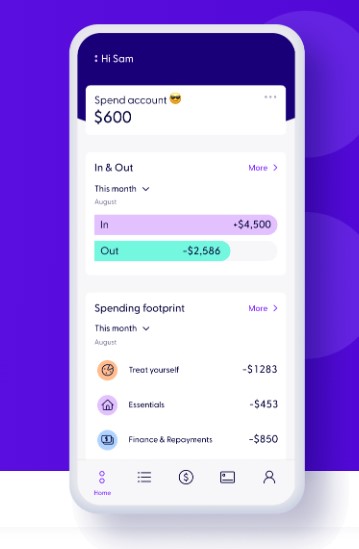

So, how does the UBank app compare to other banking apps? Ubank are determined to make their app the best banking app around and have included heaps of features, such as the following:

- The Smart Search feature is a search bar within the app where you can search for particular transactions by name such as ‘rent’ or ‘Menulog’ for example within your connected accounts

- Connect accounts from other financial institutions and see all your money and balances in one place

- The Coming Up feature keeps track of upcoming subscriptions, bills and regular payments – predicting them and showing you what’s coming up

- The Spending footprint sorts your spending into categories for you so you can see what you spent on shopping, entertainment, eating out etc

- In & Out feature shows you how much money is coming in and going out with an easy to read graph, so you can keep on top of your spending

- Within any of your Save accounts, you can create savings targets, using emojis if you really want, and the app will help you create a plan and track your progress

- You can lock your Visa debit card instantly through the App if the card is ever lost or stolen

- Access your actual card details within the app at any time, even if your physical card is not on you

- Notifications can be turned on for various app activity

Home loans from UBank

UBank offer home loans with very competitive interest rates. So competitive in fact that I am constantly harassing my mortgage broker about why my investment property loan interest rate isn’t that good! The only problem with UBank loans is that it is actually pretty difficult to apply for them without proper guidance, they don’t tend to work with brokers (so your broker won’t suggest using them) and a lot of people won’t meet their strict lending eligibility criteria.

After listening to people gripe about UBank applications, the key is to submit all of your paperwork at the same time (making sure it is up to date). Documents over 6 weeks old are sure to get your application rejected, and they won’t progress your application until they have every last form they request.

They offer really good rates by only taking on extremely low risk clients, which means UBank loans are best suited to those with a sizeable deposit, or already have significant equity in their property (20% or more) if refinancing to a better rate with UBank.

UBank review, can it compete with digital banks?

I have found in the past that UBank’s web and mobile banking seemed to be down a lot, but they have improved their App and their online features so in the past year or so, I haven’t experienced any issues.

Interestingly, Ubank, or more to the point NAB, decided they couldn’t compete with 86400 Bank, so instead bought them out for AUD $220 Million. There are more and more digital banks coming onto the scene, but Ubank have improved their web interface, they have a new App with some great features, and they have updated their accounts too, so they are definitely still a great online bank to use for your spending and saving.

Conclusion

UBank accounts include transaction accounts and savings accounts and they also offer loans, term deposits and superannuation. They are backed by NAB and with over 600,000 customers and AUD $16 Billion under management, they have been a popular choice for Aussies looking for a no frills bank since they started up in 2008.

They do not charge ongoing fees and provide competitive interest rates which is a massive plus, however they do not have physical branch access, and their customer support can be frustrating at times. All things considered, I think it is a good no frills banking product and have used them for the past 5 years.

I think it is important to stash your Emergency Fund or Mojo Account in a different bank than you use for everyday transactions – just making it that one bit more out of reach, but obviously easy to get to in an actual emergency.

Have you opened up a new uBank account recently? Or are you considering switching banks? Let me know your thoughts and your why!

Want to know where Captain FI banks?

Check out my Personal Resources Page and my Net Worth Updates.

Financial Disclaimer

Financial Disclaimer: CaptainFI is NOT a financial advisor and does not hold an AFSL. This is not financial Advice!

I am not a financial adviser and I do not hold an Australian Financial Services Licence (AFSL). In this article, I am giving you factual, balanced information without judgment or bias, to the best of my ability. I am not giving you any general or personal financial advice about what you should do with your investments. Just because I do something with my money (or use a particular service or platform) doesn’t mean it is automatically appropriate for your personal circumstances. I do not recommend nor endorse any financial or investment product, and my usage or opinion of any product should not be interpreted as an endorsement, advertisement, or intent to influence.

I can only provide factual information based on my journey to Financial Independence, and that is provided for general informational and entertainment purposes only. I make no guarantee about the performance of any product, and although I strive to keep the information accurate and updated as it changes, I make no guarantee about the correctness of reviews or information posted.

Remember – you always need to do your own independent research and due diligence before making any transaction. This includes reading and analysing Product Disclosure Statements, Terms and Conditions, Service Arrangement and Fee Structures. It is always smart to compare products and discuss them, but ultimately you need to take responsibility for your use of any particular product and make sure it suits your personal circumstances. If you need help and would like to obtain personal financial advice about which investment options or platforms may be right for you, please talk to a licensed financial adviser or AFSL holder – you can take the first steps to find a financial advisor by reading this interview, or by visiting the ASIC financial adviser register and searching in your area. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Hopefully the UBANk app does get a facelift after the marriage with 86400, its a bloody shoddy piece of tech at the moment

Good one!

If they are backed by NAB assuming they invest in fossil fuels?

Yes I think most of the big banks do

I switched my home loan to UBank when I owed just under 100K. It was a pain to switch over but it was worth it. The mortgage simply melted away…

I, too, found problems with the online website being down. My son suggested switching to Safari when I wanted to use it. Since then, no probs.

Yeah the rates under 2% these days are amazing, good opportunity to knock down any debt if that is your plan. Great suggestion re: browsers. Safari and Chrome are both my top picks too.