Barefoot Investor Super – Everything you need to know about the barefoot investors’ Superannuation fund recommendations

What are the Barefoot Investor Super recommendations? The Barefoot Investor Scott Pape highlights the powerful long-term financial benefit of making two incredibly simple changes to your Superannuation. Firstly, The Barefoot Investor agrees with American finance celebrity Dave Ramsay and states you should be making additional pre tax super contributions – recommending you boost your contributions to 15% of your wage*. Secondly, The Barefoot Investor states you should be investing it into a broad market diversified index fund with ultra-low costs (Like HostPlus’ Index Balanced option).

*NB the current concessional cap is $27,500, roughly correlating to 15% of a $180K salary. Any contributions above the cap are taxed at marginal rates.

Making smart changes to your superannuation early in your career can be the difference between adding hundreds of thousands of dollars to your Superannuation retirement fund, or needing to rely on the aged pension. There are risks either way, but one scary possibility is that the pension could potentially be phased out for the majority of us in the workforce anyway as the Australian government deals with an aging population and an impending train wreck of aged care spending over the next decade. Paying attention to your super is important for everyone who wants financial freedom.

This article will explore The Barefoot Investors’ superannuation recommendations, what is his ‘Don Bradman retirement Strategy’ and how much superannuation you need, why Barefoot recommends Hostplus, whether there is any potential conflict of interest here, and what are other low-cost options.

The Good

- Low fees maximize your total return

- Most of these funds have millions of members

- Well known PDS

- ‘Good enough’ solution

- Index investment options for building wealth passively

The Bad

- Most are pooled trust fund style – tax inefficient due to provisioning

- One size fits all may not be the optimum choice for you

- Some TPI and income protection career exclusions (Eg PILOTS!)

- Low fee investments does not always align with low fee insurance – some compromise in price is necessary

Verdict: The Barefoot investor has some great advice regarding superannuation in Australia, but you should only use it as a starting guide and not follow it blindly. Superannuation and associated insurances are a serious topic, and it’s worth getting professional advice.

CaptainFI is not a Financial Advisor and the information below is not financial advice. This website is reader-supported, which means we may be paid when you visit links to partner or featured sites, or by advertising on the site. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Barefoot Investor Super Disclaimer

The Barefoot Investor is often called the finance bible and has provided some great advice and general information when it comes to his barefoot investor super recommendations for your retirement savings, but it’s worth noting that it is just factual information about products and none of it should be considered financial advice – either personal or even general advice, because it doesn’t factor in your personal situation. Super is a pretty important topic, and something you should pay attention to. For most Australians, it can be our largest asset and a safety net for retirement, and it also forms part of any ‘FIRE’ retirement plan. Accordingly, it’s worth paying attention and potentially obtaining professional advice from a licensed advisor.

The Barefoot Investor

Scott Pape, Author of the Barefoot investor and the Barefoot for Families writes no frills, no nonsense advice on your finances and how to raise kids. The Barefoot Investor claims impartiality, and simply ‘calls it how he see’s it’! If you want to see whether or not the barefoot investor works, read my article about how he changed my life.

When it comes to your Superannuation, Scott Pape promotes the powerful long term financial benefits of making additional super contributions by boosting your contributions to 15% of your wage, and investing it in a low ongoing fees, broad market index fund. You can salary sacrifice these additional contributions, or claim them back at tax time. The Barefoot says if your paying more than .85% in fees – your being taken advantage of and need to switch as you can make a huge boost to your retirement savings (tens of thousands or more!) by switching.

The Barefoot Investor previously worked for Hostplus in the ‘Ka-ching Ka-ching’ educational scheme ran by Hosplus as part of their marketing division. These days though, The Barefoot Investor publicly states that he has no affiliates or relationships with any companies, he has shut down his stock tipping website ‘The Barefoot blueprint’ and he now runs a not-for-profit financial counselling service.

Despite his previous connections, The Barefoot Investor has publicly expressed his fondness for Hostplus’s Indexed Balanced Fund as Australia’s leading superannuation fund and states that this is the Super fund he has his superannuation in. Although, for legal purposes he also says he doesn’t recommend or endorse it – just that it is the best – he doesn’t want to get sued or get in trouble with ASIC I suppose!

The Barefoot Investor does point out though that it isn’t the only cheap super fund offering index fund investing options, and so in this article we will explore his other suggestions, what the funds hold and what they are currently charging.

Choosing an Australian superannuation fund

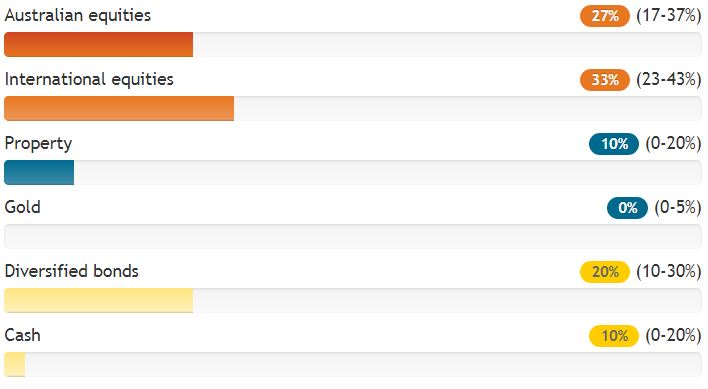

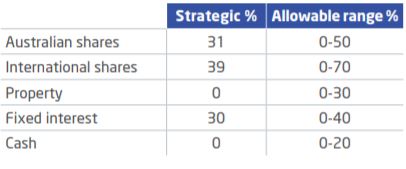

Choosing a super fund is a pretty important step for all Australians. Disregard all the glossy brochure bullshit, what you really want to know is do they offer an index fund option, what does the fund hold (breakdown of Australian shares, International shares, Bonds or fixed interest and cash) and what are the management fees.

Super funds annoy me, because they often don’t give you a straight answer. They crap on about Indirect cost fees, Management fees and accounting fees. Super funds – if you are reading this – WE DON’T CARE! We just want to know a bottom line, no nonsense answer about what the fees are in simple-to-understand terms.

And the fees can be ridiculous! I have seen super funds charging in excess of 2% fees which to be honest, should be a criminal offense!

“Fees can have a substantial impact on members — for example, an increase in fees of just 0.5% can cost a typical full-time worker about 12% of their balance (or $100,000) by the time they reach retirement”

Super Guide

Why then, would you pay in excess of 2% on your super when you could be paying as little as .06% ? This can be the difference of hundreds of thousands of dollars – potentially nearly half a million dollar – to your retirement!

On average, 40% of Australian’s investment returns are gobbled up by fees, which means instead of you enjoying the benefit of your hard earned dollars, they are siphoned away into the pockets of HUGE financial corporations and paid out as million dollar bonuses to executives. This was one of the reasons for the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry

Want to make more money for retirement?

Before we go any further, if you are interested in knowing how to make more money in order to invest for your retirement, check out my detailed article how to make money online.

Best Australian Superannuation Funds

There are a number of great Australian Superannuation funds to choose from, and here are 5 of the best funds currently available in 2020 with a bit of a brief run down on each.

Remember though, its SUPER important that you do your own research and look into each of these funds to find out whether it might be right for your personal circumstances. My advice is to start with their website, track down their Product Disclosure Statement and then give their sales department a call and get them to talk you through each of the options – make sure to stress you want to know exactly what is in the fund, what indexes it tracks and the exact fee structure and breakdown.

The general trend within super funds is to move towards index strategies, and the management costs are decreasing with a general trend towards negligable or zero management costs – which is a no brainer since indexes don’t really need managing! Super funds are still charging administration fees and creaming profits on their insurance policies though, so that should still keep them in business!

The following superannuation fund information was correct as of 2021, but may have changed, so be sure to consult the latest PDS and terms and conditions for the latest fees and performance figures.

Hostplus Index Balanced

Just like how The Barefoot Investor says he uses the Dutch multinational ING Bank, Pape also uses Hostplus for his super, investing through their Index Balanced fund. I also use Hostplus and think they seem pretty good.

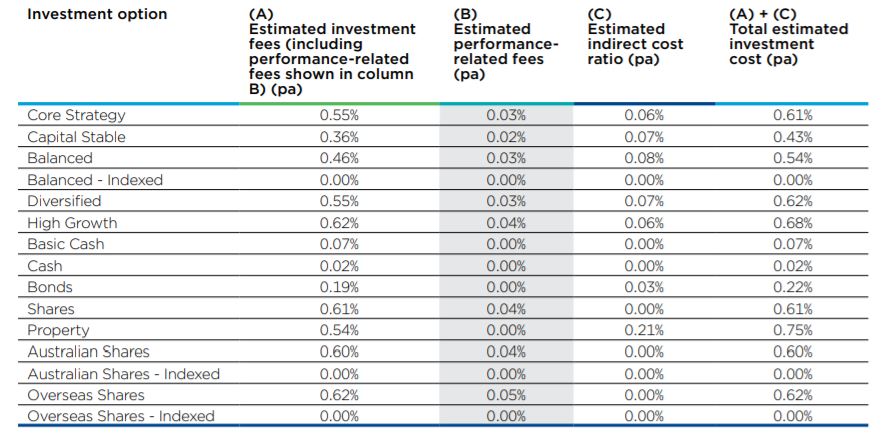

Fees: To invest in the Hostplus Balanced index fund costs .06% p.a., plus $78 per year ($1.50 per week)

Whilst The Barefoot has always been on Hostplus’ side and did previously work for them, recently he did take aim at their Balanced fund – which is COMPLETELY different from their index balanced fund. The Balanced fund contains a lot of unlisted assets (think: tollways, bridges, airports and properties) which the Barefoot Investor says are very difficult to value, and it has MUCH higher fees. It is also very easy to confuse the indexed balanced and the balanced option, so a lot of people who think they are in the low fee index option actually aren’t! He had criticized Hostplus for lack of transparency on this.

“And why shouldn’t he feel free to criticise the super fund? Everyone knows past employment is no guarantee of future endorsement.”

Michael Rodden, Australian financial Review

Make sure to check out their Product Disclosure Statement and go to Chapter 6 – Fees and Costs to check out all the Fees and Services associated with Hostplus, and give their customer support line a call to grill one of their operators. Furthermore, if you like tinkering then Hostplus also offer ChoicePlus, which is a way to directly invest in ETFs through Hostplus, giving you more control similar to a Self Managed Super Fund but without all of the headaches, administrative burden and costs.

REST Super Balanced Index

Fees: To invest in the REST Super Balanced fund costs 0.00% p.a, plus $78 a year ($1.50 per week)

REST has removed the management fees for their index investment options – Balanced Index, Australian Shares Index and Global Shares index, leaving only the $1.50 per week administration fee.

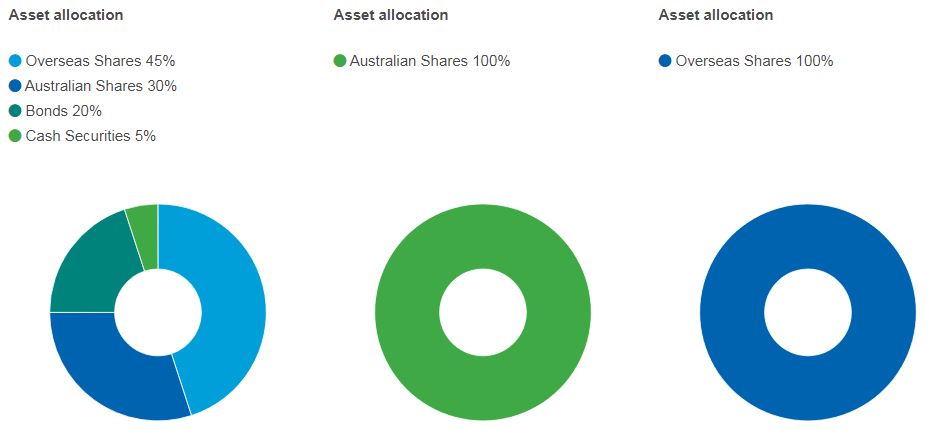

REST Super Balanced – Indexed contains a default mix of 45% global shares (ex tobacco), 30% Australian Shares, 20% Bonds (fixed interest) and 5% cash.

Check out Rests Product Disclosure statement for the total breakdown.

Australian Super Indexed Diversified

Fees: To invest in the AustralianSuper Index Diversified fund costs 0.18% p.a., plus $117 a year ($2.25 per week admin fee).

Be sure to critically analyse AustralianSuper’s fees and costs on their Product Disclosure Statement.

Vision Super Sustainable Balanced

Fees: To invest in the Vision Super Sustainable Balanced fund costs 0.15% p.a., plus an admin fee of $78 per year, plus a reserving margin of 0 to 0.02% p.a.

Check out Vision Supers Product Disclosure Statement for a full breakdown of Fees and Costs.

SunSuper Balanced Index

NOTE – SunSuper and QSuper have marged to become Australian Retirement Trust – ART Super

Fees: To invest in the SunSuper Balanced Index fund costs 0.26% p.a., plus $78 a year, capped at $800,000 balance.

Check out SunSupers Product Disclosure Statement for a full breakdown of Fees and Costs.

The Barefoot Investor Don Bradman Retirement Strategy

So How much superannuation do you need? Well, the answer might be a lot less than you think.

“The aim of the Donald Bradman Retirement Strategy is simple: to ensure you’ll never run out of money.”

Scott Pape, The Barefoot Investor

The Barefoot Investor Don Bradman Superannuation retirement strategy is a technique for Australians to retire comfortably without needing to have over $1 Million in their superannuation funds like conventional financial planners espouse. According to the Association of Superannuation Funds of Australia (ASFA), retirees typically spend $59000 a year for couples, or $43000 a year for singles.

‘You need $1 million in retirement,’ say most financial planners. ‘$2 million might not even be enough,’ wrote a financial planner in the newspaper recently. If you’re in your 50s these retirement figures will likely scare the bejeezus out of you. After all, the average Aussie couple retires with $200,000 in super. Let me be clear: you do not need a million dollars in super to retire. A million dollars is way above what you actually need.

Scott Pape, The Barefoot Investor

So, without a conventional balance exceeding $1 Million to fund your retirement, to make up the gap for what retirees typically spend, the scott paper explains in The Barefoot Investor Don Bradman retirement strategy how to supplement this using a paid off house, some superannuation income, the aged pension and casual work. The strategy is as follows;

- You need a fully paid off house (Primary Place of Residence) to live in

- You need at least $170,000 in your superannuation for Singles, or $250,000 for couples

- Claim the full Aged Pension through Centrelink. Currently the maximum rate of Age Pension is $34252.40 per year for couples and $22721.40 for singles.

- Work one day per week – earning up to $6,500 per year for singles or $13,000 per year for couples before it impacts the aged pension amount.

Currently, if you exceed the superannuation balance the ATO will deem you to have an income, and if this and your income exceed the income tests then your aged pension payments will be reduced accordingly. If your work is really lucrative, and you earn more than around $29K per year (singles) or $58K per year (couples), then you won’t get the pension and you will even have to start paying tax.

So what is an example of how this might look like when all is said and done?

“You’ve paid off your home.

You’re getting the Age Pension of $34252.40 (per couple) a year, indexed for life.

You’ve got $250000 in super which will pay you a tax-free income of $12500 a year.

You and your partner each work just one day a week to bring in a combined $13,000 a year, completely tax free.

Total: $59 752. That’s almost $1000 more than you need for your comfortable retirement! Ker-ching!”

Scott Pape, The Barefoot Investor

Insurance Through Superannuation

Now this is one of the quirks of Australian finances. Most superannuation companies give you the option to purchase insurance through superannuation – this usually includes income protection (if you need to take time off work due to a recoverable injury for example), Total and Permanent Disability (TPD or TPI) if you have a serious and permanent accident or illness, and life insurance which covers a payout to your dependents in the instance of your death. Because it is done through your superannuation you save on some tax (super is only taxed at 15% vice your marginal rate).

For example if you have significant debt, a mortgage or various other liabilities, then having these insurances can be important to a lot of people for peace of mind – knowing that if something does go ‘wrong’, that the insurance will cover it and their dependents or children won’t get lumped with this responsibility.

Firstly, Insurance is a tricky industry and you should be aware of potential conflicts of interest. Secondly, it doesn’t automatically cover everything you might think (or might reasonably be led to think) it does – so you really need to understand your policies Product Disclosure Statement. Thirdly, many superannuation insurance providers have exemptions – for example HostPlus wont provide insurance to LPG tanker drivers (I guess because they consider them at higher risk of being blown up?) as well as a whole Host of other occupations – (check HostPlus’ insurance career exclusion list here).

My dearest mother for example – paying thousands of dollars per year on comprehensive insurance for a $3000 vehicle, paying thousands of dollars per year on home insurance for a grossly inflated level of contents cover (who needs $200K of content insurance alone – sorry but no reasonable persons clothes and old daggy furniture is worth that much!), and of course my pet peeve… Pet insurance that never ever paid out and left her with a $12,000 Vet bill! I took much glee in sitting down with her and working out how we could remove these useless insurances and unnecessary line expenses from her budget, and working with her to get a much more appropriate level of cover for her retirement.

This being said, some insurances are very important for financial freedom. If, like the majority of us, you derive your income from working, and not being able to work would be financially devastating to you and your family – then you probably need some level of income protection insurance. I firmly believe you should only insure against things that would financially devastate you (like driving your car into a Ferrari, your house burning down or permanent impairment) and for everything else you should maintain a solid emergency fund, low cost of living and create additional streams of passive income. These things help deal with life’s ‘little annoyances’. A big enough emergency fund can help turn a stressful emergency into a frustrating annoyance – you effectively ‘self-insure’ and get to keep your premiums, and never pay an excess!

You need to work with your super provider to know exactly what level of income protection, TPD and life insurances you need for your personal circumstances, as well as what these policies cover, time frames and anything that might void them (such as exclusions). Remember that having multiple superannuation accounts with multiple policies may actually be a voiding condition – in this circumstance if there is an event requiring insurance, they will often ’round table’ it, each super fund arguing over who is liable and paying out the lowest level of cover, regardless of the other policies. Sometimes they use this as a loop hole to pay out nothing and leave you to rely on public healthcare and social security.

Workers Compensation insurance

You should bear in mind that there are government agencies which regulate mandatory workplace insurance which is separate to your superannuation insurances, which must be provided to employers by their employers.

“Workers compensation is a form of insurance payment to employees if they are injured at work or become sick due to their work.”

Australian Fair Work Ombudsman

Workers Compensation Insurance is administered in Australia by the following agencies;

- Australian Capital Territory: WorkSafe ACT

- New South Wales: State Insurance Regulatory Authority (NSW)

- Northern Territory: NT WorkSafe

- Norfolk Island: Norfolk Island Workers Compensation Agency

- Queensland: WorkCover Queensland

- South Australia: ReturnToWork SA

- Tasmania: WorkCover Tasmania

- Victoria: WorkSafe Victoria

- Western Australia: WorkCover WA

If there is an injury, illness or serious accident at work, your superannuation fund, relevant workers compensation agency, employer and your employers workplace insurance provider will usually start a legal shit fight and the loser has to cover your costs. This can be a very drawn out process requiring extensive interviews, assessments, medical examinations and even lengthy legal court cases which can be extremely stressful. Take it from experience, my family has been through three of these cases (Car accident, Workplace bullying and harassment, and Cancer treatments). My Mum’s emergency fund and income protection insurance was invaluable to help get her through these tough times.

Disability Support Pension vs TPD cover

Finally, yes there is the Disability Support Pension (DSP) which is the Australian social security backup to TPD insurance. Should you find yourself totally and permanently disabled and do not have TPD insurance, you might be able to rely on the Australian government DSP Centrelink payment so that you have enough money to eat and don’t die. But take it from someone who has a family member on long term DSP due to a crippling chronic illness – the DSP is not dignified lifestyle and it is barely enough to live on without being extremely frugal. You should definitely get TPD cover to protect your future in the event of a total and permanent disability or injury.

Where do I invest my superannuation?

Personally, the majority of my superannuation is invested in a pension (annuity) scheme through my company – I can’t actually change this for now, as this is what I agreed to in my contract. Even if I could though, I wouldn’t – this pension scheme is great. I worked out it is better ROI and lower risk than many of the other direct invested schemes I was offered, and when I resigned contracts I was asked several times to switch into a shittier fund (which I did not). The annuity is basically an insurance product (sometimes called a defined benefit), and when I reach the preservation age for the fund I will start getting paid out the annuity for the rest of my life. It has more than adequate insurance (income protection, TPD and life insurance) attached to it, although the fees are way too high for my liking (I’m afraid to even mention them for fear of being stoned to death by the FIRE community) but the pension payoff at the end more than makes up for these fees.

However, I have also previously contributed extra payments (concessional contributions) towards my superannuation because it was tax effective for me at the time (and because to be honest, I didn’t know any better). Now this is building in a separate, directly invested fund. I don’t make extra super contributions anymore because I am focused on FIRE and building up my taxable investment accounts to fund early retirement. So I was looking for somewhere good to park this and let it grow for the next 30+ years.

Because of all the hype around HostPlus I looked into it. I opened a HostPlus account, and initially looked into their ChoicePlus options (As the Barefoot Investor puts it – SMSF Lite) so I could replicate my FIRE portfolio. However, when I explored it in more detail, it looked like too much of a pain in the arse: it wouldn’t let you invest more than 80% of your fund in one option, it had high brokerage fees, the cash account COSTS YOU MONEY (Negative interest rate!!), and you would need a significant investment in it to break even when compared to the basic index options due to the higher ChoicePlus fees.

So, instead of ChoicePlus I am in the process of rolling my direct invested superannuation portion into a mix of 50% of the IFM Australian shares* fund (index Australian shares MER = .03%) and 50% of the International Index fund (MER = .12%). I am using this split because I don’t like how much cash the Indexed Balanced fund currently holds – I think there is still too much tinkering going on and wanted more exposure to stocks rather than fixed interest.

*Dont Confuse the IFM Australian shares (index fund) with the IFM Australian Infrastructure fund (unlisted property fund). Also, do not confuse these fund names because HostPlus also rather shockingly offer the managed fund versions of these with VERY similar names and it is very easy to accidentally select the actively managed version with hideously more expensive fees rather than the index version.

I have recently helped both of my parents (who are separated just to add duplicity!) navigate through sorting out their Superannuation and social security (aged pension) applications. After meeting with a financial advisor for peace of mind (FYI they were pretty useless) and then a few super fund providers in person to grill them about fees and charges, we ended up doing what I am doing with my personal super.

We switched theirs over to Hostplus into the indexed Australian shares (IFM Australian shares) and indexed international funds, as well as taking out a big chunk to pay off the mortgage for their peace of mind. Dealing with the team at Hostplus was fairly pain-free, I called them about four times just to clarify everything and then used their website to set up an account and request a roll-over which took about 10 minutes to complete, and then about two weeks for the funds to settle. I also didnt reveal who I was or that I was secretly judging them for my blog haha!

So Finally, what about insurance? As I mentioned earlier, insurance through your super can be a very contentious issue. If you fuck it up, you are at risk of not being covered at all, having too much expensive cover you don’t need, or not having enough cover. This is why if you are not 100% confident in what you are doing and your ability to digest a Product Disclosure Statement or confront salespeople on the phone or in person, you should look to consult a professional financial advisor. A professional financial advisor can give you specific personal advice tailored to your unique circumstances, which is incredibly valuable – my advice would be look for a reputable, fee for service (hourly rate or agreed project cost) financial planner that does not stick you with ongoing contracts or percentage based fee structures. Of course, make sure to remind them that legally they need to disclose any affiliate relationships or kickbacks from any products they recommend.

With that out of the way, I have chosen not to take out any insurance through my HostPlus account – I simply ticked the ‘No insurance’ box when I was setting up my account online – this is because I have insurance through my companies super policy and I did not want to muddy the waters by getting secondary unnecessary policies. Secondly, my parents also chose to do the same – they are both retired, have paid off their homes, have no debt, and have ‘passive’ income streams from their superannuation, social security (and weirdly enough – also by selling solar power back to the grid from their panels).

Australian Superannuation funds

Check out reviews of the following super funds;

- HostPlus super

- UniSuper Review

- REST Super review

- ART Super review – Australian Retirement Trust

- Australian Super Review

- MLC Superannuation Review

- ANZ Smart Choice Super

Conclusion

The Barefoot Investor agrees with finance celebrity Dave Ramsay and states you should be making additional contributions to your super – recommending you boost your contributions up to at least 15% of your wage (noting the current concessional cap is $25,000 per year and above that you will not receive the discounted tax rate and have to pay your full marginal rate tax on contributions). Secondly, The Barefoot Investor states you should be investing it into a broad market diversified index fund with ultra-low costs, and if you are paying over .8% in fees, you should be looking for better deals.

So where should you invest your superannuation? This is an incredibly personal and serious decision and not something you should make on a whim.

Low fee options recommended by the Barefoot Investor currently include Hostplus’ Index Balanced option, as well as Rest, VisionSuper, AustralianSuper and SunSuper, whom all offer low fee index fund investment choices.

Make sure you understand exactly what you are buying into and the underlying assets, the fees and costs you are paying and their impact on your returns. You also need to have a good understanding of your level of need and policies on income protection, trauma, TPD and life insurances policies (level of protection and costs) associated with your super – many policies have exclusions and it sometimes becomes a trade-off between insurance cover and investment returns which can be very frustrating for the typical pooled-fund industry super funds.

Making smart changes to your superannuation early in your career can be the difference between adding hundreds of thousands of dollars to your Superannuation retirement fund, or needing to rely aged pension (which will likely be phased out for the majority of us in the workforce anyway). It also means should some unexpected accident occur, that you can be covered more appropriately.

If it’s still feeling a bit mystified for you – I highly highly recommend you track down a good, independent, fee-for-service (hourly rate) financial advisor for professional advice.I had an awesome chat to Vince Scully about Superannuation on the Financial Independence Podcast. Vince is a licenced financial advisor, and we spoke for hours all about Superannuation where he clarified a lot of confusions, have a listen to the episodes if you want to learn more;

Podcast | Superannuation with Life Sherpa part 1 of 2

Podcast | Superannuation with Life Sherpa part 2 of 2

Further Reading on the Barefoot Investor

Related articles share, book review, buckets and bank accounts;

- What Index funds does the barefoot investor buy?

- Does the Barefoot Investor work?

- What is the barefoot investor blueprint

- What are the barefoot buckets

- What are the bank accounts the barefoot investor recommends

- How to Make Money Online

Frequently asked questions about the Barefoot Investor Super funds

Answers to frequently asked questions about the Barefoot Investor and Superannuation funds.

What super fund does the Barefoot Investor recommend?

The Barefoot Investor doesn’t recommend any fund due to legal concerns, but he publicly states that he uses the Hostplus Indexed Balanced fund for himself and his family.

How much super do I need Barefoot Investor?

According to the Barefoot Investor, Singles need at least $170,000 and couples need $250,000 in their super for a comfortble retirement when used in conjunction with a paid off home, the aged pension, and casual work of one day per week.

Which Super Fund has lowest fees?

According to the Barefoot Investor, RestSuper currently has the lowest fees with a their Balanced Index fund not charging a management fee at all, and only costing $78 per year in administrative fees.

What is the best super fund in Australia 2020?

The Barefoot Investor suggests Hostplus, Rest, VisionSuper, AustralianSuper and SunSuper as the best super funds in Australia in 2020.

Cheapest super fund in Australia

Rest is currently one of the cheapest super funds in Australia.

When can I retire in Australia

You can retire as soon as your passive investments cover your cost of living. If you do not invest outside of your super, you will have to wait until preservation age to access your superannuation entitlements (unless you are granted early release due to injury or other extenuating circumstances). Your preservation age depends on your birth year, however for most Australians it is 65 years old.

Barefoot investor superannuation contributions

The Barefoot investor recommends you contribute 15% of your wage into your superannuation accounts. This is 5.5% above the legal minimum requirement of 9.5%.

How much superannuation does the barefoot investor recommend?

For Financial freedom, The Barefoot investor recommends at least $170,000 in your superannuation for singles, and $250,000 for couples. This is part of his ‘Don Bradman Retirement Strategy’;

- You live in your own home, and its paid off.

- You need at least $170,000 in your superannuation for Singles, or $250,000 for couples

- Claim the full Aged Pension through Centrelink. Currently the maximum rate of Age Pension is $34252.40 per year for couples and $22721.40 for singles.

- Work one day per week – earning up to $6,500 per year for singles or $13,000 per year for couples before it impacts the aged pension amount.

Financial Disclaimer

Financial Disclaimer: CaptainFI is NOT a financial advisor and does not hold an AFSL. This is not financial Advice!

I am not a financial adviser and I do not hold an Australian Financial Services Licence (AFSL). In this article, I am giving you factual, balanced information without judgment or bias, to the best of my ability. I am not giving you any general or personal financial advice about what you should do with your investments. Just because I do something with my money (or use a particular service or platform) doesn’t mean it is automatically appropriate for your personal circumstances. I do not recommend nor endorse any financial or investment product, and my usage or opinion of any product should not be interpreted as an endorsement, advertisement, or intent to influence.

I can only provide factual information based on my journey to Financial Independence, and that is provided for general informational and entertainment purposes only. I make no guarantee about the performance of any product, and although I strive to keep the information accurate and updated as it changes, I make no guarantee about the correctness of reviews or information posted.

Remember – you always need to do your own independent research and due diligence before making any transaction. This includes reading and analysing Product Disclosure Statements, Terms and Conditions, Service Arrangement and Fee Structures. It is always smart to compare products and discuss them, but ultimately you need to take responsibility for your use of any particular product and make sure it suits your personal circumstances. If you need help and would like to obtain personal financial advice about which investment options or platforms may be right for you, please talk to a licensed financial adviser or AFSL holder – you can take the first steps to find a financial advisor by reading this interview, or by visiting the ASIC financial adviser register and searching in your area.

For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

The Barefoot Investor suggests bumping super contributions to 15%. If I was earning over $166k, is this no longer effective? Or put another way once you are contributing $25k to super per year is there a better use of any excess money such as straight ETF so you can access the money earlier if needed?

Hey Sean. Yeah $25K is the max concessional contribution you can make, and there are also some rules around using up previous years contributions if you haven’t maxed them out already. Best bet is to talk to an accountant. Personally, I have made lots of contributions to super in the past, however these days I prefer to invest my money outside of super which maximises my options and gives me the flexibility to ‘Retire Early’, or more to the point to be ‘Financially Independent’. Still, super is a great idea and if you are on a high income or in the first few years of your career it is probably a good idea to tuck some away into it and then it can compound in a tax effective environment. Check out my NW posts to see how I am investing my money. Cheers

Great summary. From 1st July 2021 confessional.contribution cap has gone up.to $27500 per annum

Hi CaptainFI,

Thanks for a great article! I was just wondering how you were able to allocate your super into the 50/50 split without using the ChoicePlus option? I have been looking at the HostPlus website but can’t seem to find where this would be an option?

Thanks!

can you please give the most updated super info—June 2024. Is Barefoot now using Vanguard Super and which one exactly?

G’day Agnes, I will look into this soon 🙂 cheers

In 2024, is barefoot still using Hostplus or Vanguard Super?