ING Bank review from a long-term customer, financial independence enthusiast, and experienced investor. Is this the bank for Financial Independence?

ING was the recommended bank by the Barefoot Investor in his best selling book, but is it still relevant and worth using in the face of the slew of offers from the new ‘Neo banks’, Fintechs and the ‘Big 4’ giants desperate to get your banking business back?

This article is for anyone with Australian residency who is looking to open up a fee-free online bank account that can be used in Australia and around the world.

ING: The Good

- No Fees! No account or ATM withdrawal fees

- Multiple Transaction accounts each with unique VISA cards

- Features instant PayID, OSKO and BPAY

- Supports joint accounts

- Bank @ Post available

ING: The Bad

- Interest Paid on one Savings Maximiser only

- Must deposit $1000 per month and make 5+ card transactions a month for it to be fee free

- No physical branches

- Have to contact customer support to get your sign up bonus

Verdict: ING is a great bank, but read on to see why I also use Up Bank

CaptainFI readers score a free $50 from ING using promo code: FKQ674

CaptainFI is reader supported, which means we may be paid when you visit links to partner or featured sites

ING in Australia

ING (International Netherlands Group) bank itself is actually a Dutch international banking and financial services corporation, started in 1991 through the Merger of previous banking corporations. Its global headquarters is in Amsterdam, but it also has offices all around the world.

If the first thing that comes to mind when you think of ING is the comedian Billy Connolly, then your probably around the same vintage as me. He was featured on a lot of their early advertising, which kind of made ING seem like ‘the Aldi of banks’ – a little different, but good different?

Some of them were just plain cringe-worthy, but most just make me laugh when I go back to watch them these days (especially the ones that featured ‘the internet’ and other ‘cyber’ themes from around the dot com boom).

Of course times have changed, and ING have moved on from Billy Connolly, awkward ‘dot com boom’ era ads and Smooth talking British Orangutans. ING has now settled on the much more attractive redhead Isla Fisher to spearhead the face of their $10 Million dollar PR campaign to re-brand ING as a conventional ‘main’ bank rather than a quirky side offering – and boy has she done wonders for the company!

You might not realise it, but ING Group is actually one of the biggest financial companies in the world with assets over USD $1 trillion (check out ING’s income stats here). It is frequently ranked as one of the top 30 banks world wide, and has and over 40 million customers (with about 2 million of those in Australia alone).

ING Group’s primary business is banking (retail, direct, commercial, investment, wholesale and private), but they also offer asset management and insurance services such as superannuation.

ING began offering banking to Aussies in 1999 with ING Bank Australia Limited, headquartered in Sydney, NSW. ING’s Australian division alone made over AUD $440 million in profit in 2019, by managing (investing) nearly AUD $45 Billion worth of Aussie’s savings, as well as profits from writing AUD $63 Billion worth of loans.

They also signed up nearly half a million Aussies for bank accounts in 2019 (thanks barefoot investor!) So its actually a sizeable player in the Australian banking industry, and has significant capital behind it to ensure customers satisfaction and safety – which is ultimately linked to total shareholder return, right?

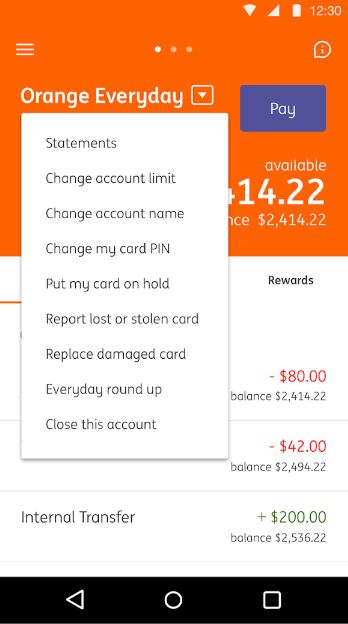

ING online everyday account: Orange Everyday

An Orange everyday is the basic transaction or ‘checking’ account I use with ING. I actually have a few of these, because I like to separate certain pools of money (such as sinking funds for my car expenses) and I like having a couple of visa debit cards as a backup.

Having your salary or regular income deposited into an everyday account and then a record of both your bills going out, and when you transfer funds to your genuine savings into your savings maximizer will improve your borrowing power when it comes time to get a home loan. 12 months or more would be a great start, but of course, seek advice and further details from your broker.

Interest on money in these accounts is basically non-exsistant as they are checking accounts so you typically don’t want to park a lot of money in them – they are transaction accounts so designed for regular money in and money out, and for me the real benefit is that they are pretty much fee-free. Of course, you need to consult the ING Orange everyday Product disclosure statement to be truly sure of their fee structure, because I am sure there are some things that might potentially cause you to cop a fee (overdrawn account maybe?) its just that this has never happened to me.

ING online high interest savings account: Savings maximiser

The Savings maximiser is ING high interest online savings account. Of course, as official RBA interest rates change, so too does the interest yield on pretty much every banks savings account. Not withstanding, ING offer a competitive rates (compared to other banks savings accounts) when you have a linked orange everyday transaction account and meet a few criteria with it;

“Simply deposit your pay of $1,000+ per month and make 5+ card purchases that are settled (not pending) each month to get these benefits the following calendar month.”

ING Bank Australia

In my opinion, it would be great to be able to have multiple savings maximisers linked to the same (or multiple) Orange Everyday account, but alas this is not how it works. So I personally just have one main savings maximiser, and I keep some of my emergency fund here in cash (with the majority of my emergency fund being parked in my mortgage offset account). The other savings maximisers have smaller amounts and are used as a combination of sinking funds.

Check out ING Savings Mazimiser Product Disclosure statement for the full terms and conditions

ING Banks mobile application

ING Banks mobile app is simple, straightforward and everything you need. It displays all of my accounts, transaction history and is very easy to make transfers with. This has been very handy both at home and when overseas, especially making purchases I didn’t quite understand (for example trying to figure out ‘inbuilt gratuities’ – tips, at American bars I just open the app to see just how much they have debited).

Its also handy when I need to make sure I have enough money in my account and quickly load up my card by transferring between accounts.

Face to Face transactions with ING Bank

Most people don’t care, but some *cough* Boomers *cough* don’t like that ING doesn’t have any physical branches in Australia.

One of the ways ING is able to maintain such a low fee service is by maintaining low cost overheads – and one way of doing this is to actually avoid having physical branches all together. As a typical millennial, I salute this move as it means there is a lower chance of me ever having to stand in a cue in a bank and have to deal with another human being (I still occasionally have to do this for business banking with other providers or when I need cash overseas and I dislike it!).

During COVID-19, ING actually had something like 80% of their employees working from home – and why not, since they all technically work ‘remotely’ from the customer anyway?

There are of course some things I need to do ‘in person’ banking for – for example stashing cash I have earned from my side hustles or selling things, or cashing sweet sweet affiliate marketing checks from my eCommerce businesses (although this hasn’t happened much unfortunately!). Luckily, ING have a deal with Australia Post – you can simply go into any post office branch to deposit checks or cash in person.

Features I like about ING Bank

- PayID – I don’t have to give out a BSB, account number and name anymore – I just set my PayID which keeps my details protected (super handy for selling things)

- ING supports OSKO instant payments – this really helps when buying or selling things second hand

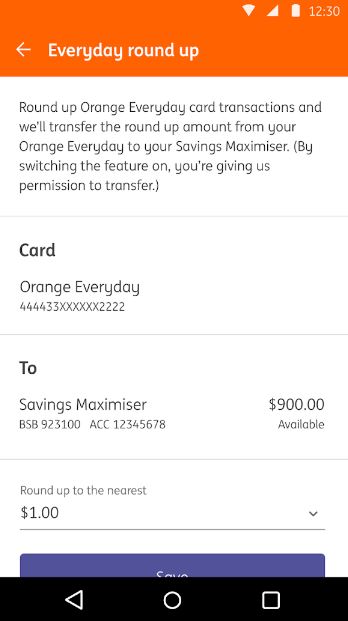

- ‘Round up’ – I can round up purchases to the nearest $1 or $5, and send the difference to my brokerage account which encourages me to invest more.

- No Fees – I don’t ever pay any account keeping, transaction, international purchase or ATM fees – EVER! ING actually even refunds me ATM and international transaction fees when I am charged by other companies or banks.

- Good interest rate – I get a competitive interest rate on the emergency fund in my savings mazimiser (Side note – it might not be the absolute highest available but I could not be bothered changing banks to earn an extra 2 cents per month in interest though)

Other products from ING Bank

ING do have other products and financial services; of course they offer Credit Cards, but they also offer personal loans and home loans, and sell Insurance and Superannuation products. I don’t have any personal experience with any of these other products, but you can find out more on their website if you are interested.

Security and safety with ING

I was recently a victim of identity theft / fraud whereby some loser opened up a mobile phone in my name using an old address they scammed (presumably from a data spill or stolen old mail) and tried to use it to scam me by switching financial services to it for 2FA.

Thankfully, ING were all over this. I spoke to a security expert on the phone for over two hours where she went over everything needed to fix this situation – including helping me with my other financial accounts (even other banks) and a statement for police.

They asked me not to go into too much detail on here due to social engineering concerns, but rest assured I was very impressed by the level of security and how helpful they were.

Does Captain FI use ING?

Yes, I’ve been a personal customer of ING for over 8 years now, and to be honest, I couldn’t ask for a better bank. I use it conservatively (no credit cards for Captain FI just yet!) with just a couple of Orange Everyday accounts and Savings maximizers for my emergency fund (mojo) and sinking funds. I don’t think I have ever paid a cent in fees or ATM charges – and I get interested paid out to me on the balance of my savings accounts.

I use my main everyday transaction account as a ‘Daily expenses’ checking account for direct debit bills (such as rego), grocery shopping, utilities, rent and fuel. I use my second transaction accounts as my ‘backup card’ just incase anything goes wrong with the first card. I simply transfer across the required amounts from my ‘Splurge’ (treat yo self account) or ‘Smile’ (holiday / toy savings account) when needed.

I have multiple savings maximisers – for example the ‘Mojo’ (part of my emergency fund), and the ‘splurge account’ and ‘smile account’ – for things like takeaway food, drinks, and the times I do choose to shop online.

This is perfect since I am frequently traveling the globe and need an easy way to access my cash without getting stung with hefty international transaction fees. ING has actually saved me thousands in fees since I switched!

ING sign up promo code

For now though, if your dead set on joining ING, they have given me a promo code to share with you which should credit your account with $50 or $100 depending on what bonus they are offering at the time – you just need to create an Orange Everyday and a Savings Maximiser, deposit $1000 and make 5 transactions on your Orange Everyday Visa Card. Money for Jam in my opinion!

ING Promo code: FKQ674

Frequently asked questions about ING Bank

Answers to frequently asked questions about ING

Is ING bank a good bank?

Yes. ING is a good bank to bank with, and consistently ranks highly among customer satisfaction surveys.

Is ING bank safe to bank with?

Yes, ING is incredibly safe to bank with. ING has nearly 60,000 staff members and over 40 million customers over 40 different countries – with assets in excess of USD $1 Trillion. They have mature security protocols and an excellent fraud team.

Who is ING bank owned by

ING bank Australia is owned by the Internationale Nederlanden Groep, a dutch banking company.

Why is ING the best bank?

ING is one of the best banks because of their focus on customer service and low fees. They provide an excellent product at an industry leading price.

Is ING a big bank?

Yes. ING (Internationale Nederlanden Groep) is one of the worlds largest banks. Globally, ING has nearly 60,000 staff members and over 40 million customers over 40 different countries – with assets in excess of USD $1 Trillion.

Is ING an online bank?

Yes, ING is an online bank in Australia. This is how they provide such cost effective services with lower overheads and thus pass on lower fees to customers.

How Strong is ING bank?

ING is considered an extremely strong bank, with excellent security and safety protocols. Globally, ING has nearly 60,000 staff members and over 40 million customers over 40 different countries – with assets in excess of USD $1 Trillion.

What does ING bank stand for?

ING bank stands for Internationale Nederlanden Groep which is the name of the Dutch company that owns ING Bank Australia. Internationale Nederlanden Groep is one of the worlds largest savings bank.

How do I deposit cash ING Australia?

The easiest way to deposit cash into your ING Australia account is using Bank at post – at Australia post, tellers will scan your card and take your cash, depositing it into your account.

How long does a transfer from ING take?

OSKO and PayID and BPAY transfers are instant, and standard Bank transfers take between 1-2 days.

Can I pay with my phone ING?

Yes, with ING Australia you can configure Google pay and Apple pay as a fast, secure and convenient way to pay using your phone.

Do ING Charge international transaction fees

No, ING do not charge international transaction fees. Foreign exchange currency conversion is processed by Visa.

Conclusion

ING Bank are typically a free and convenient bank which have helped me in my journey to Financial Independence. They are especially useful for me because of how much I travel internationally because they do not charge international transaction fees or ATM fees. I switched to ING over 8 years ago when I realized I was paying over $400 per year in account keeping and transaction fees with my previous bank. Not only have they saved me over $3,000 in fees since, they also have provided me with competitive interest rates and a very easy-to-use online platform.

Online banking with ING is easy using the ING app where I can manage my own money using two transaction accounts (orange everyday account with debit card) and 3 savings accounts (savings maximiser account) as part of my barefoot investor buckets cashflow management strategy. In my opinion, it is definitely a close contender for the best bank for financial independence.

A better bank than ING?

So what about the competition for good old ING? Well I was recently made aware of what is probably their most potent competitor: Up Bank.

UP Bank is an innovative Australian digital bank that offers entirely digital, cloud based personal banking through the Up mobile application. Because of this, and their strong focus on technology and rapid development, they are often categorized as a ‘neobank”. With over 200,000 customers, Up bank is targeted at a millennial audience and has had two years of proven functionality with outstanding reviews, winning Up several industry rewards such as ‘Digital disruptor of the year’ and ‘Best digital bank’.

I have recently opened an account with Up Bank, and you can check out my Up Bank review here. They seem to have basically combined ING and expense tracking software like PocketSmith or WeMoney. As far as I can see, Up are a massive disruptor in the banking sector and have been poaching ING customers left, right and center. Check out my review and see for yourself!

Further reading – other Bank reviews

Check out my list of bank reviews here to see how the competition stacks up, and to find the right bank for your journey to Financial Independence

- Commonwealth bank

- NAB Bank

- ANZ Bank review

- Westpac Bank review

- ME Bank review

- ING review

- UBank review

- HSBC Bank review

- Up Bank review

- 86400 Bank review

- Finspo review

- Spriggy review

Financial Disclaimer

Financial Disclaimer: CaptainFI is NOT a financial advisor and does not hold an AFSL. This is not financial Advice!

I am not a financial adviser and I do not hold an Australian Financial Services Licence (AFSL). In this article, I am giving you factual, balanced information without judgment or bias, to the best of my ability. I am not giving you any general or personal financial advice about what you should do with your investments. Just because I do something with my money (or use a particular service or platform) doesn’t mean it is automatically appropriate for your personal circumstances. I do not recommend nor endorse any financial or investment product, and my usage or opinion of any product should not be interpreted as an endorsement, advertisement, or intent to influence.

I can only provide factual information based on my journey to Financial Independence, and that is provided for general informational and entertainment purposes only. I make no guarantee about the performance of any product, and although I strive to keep the information accurate and updated as it changes, I make no guarantee about the correctness of reviews or information posted.

Remember – you always need to do your own independent research and due diligence before making any transaction. This includes reading and analysing Product Disclosure Statements, Terms and Conditions, Service Arrangement and Fee Structures. It is always smart to compare products and discuss them, but ultimately you need to take responsibility for your use of any particular product and make sure it suits your personal circumstances. If you need help and would like to obtain personal financial advice about which investment options or platforms may be right for you, please talk to a licensed financial adviser or AFSL holder – you can take the first steps to find a financial advisor by reading this interview, or by visiting the ASIC financial adviser register and searching in your area. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Some of my Favorite ING Advertisements

They always say to leave on a joke – Checking out old TV advertisements can be a laugh and a bit of a blast from the past. Check out three generations of marketing from ING below.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

You make lots of fair points. We’ve had some great experiences with ING too. Also, thanks for sharing the ads. I had almost completely forgotten about the monkey!

It was too funny to not include at the end haha!

I’m abit confused over the 5 transactions on the visa card. Is this a credit card? I barely use my credit card and wouldn’t use 5 transctions per month. This is what stopping me from changing banks. Yet in your post, you say you don’t have a credit card. Can you clear this for me please?

Hey Valerie, Yes I do not have a credit card, and this is a debit card. I’m sure you could get a credit card if you wanted from ING, but I have never had a credit card and just avoided that kind of debt. If you can use them carefully and pay it off before the end of the month then you can get sign up bonuses and sometimes up to 2% cash back. Say if you had $2000 of monthly expenses then by investing that money and paying the credit card off at the end of the month on average you’d be making yourself about $15 in investment compound interest, maybe between $20-40 in cash back, plus whatever sign up bonus you could get (usually around $100-200 value each year so call it $10 per month). So in that way, using a credit card might potentially make a savvy card churner something like $50 a month – which isn’t really too bad but I just haven’t been bothered doing this because of the effort and also the risk since one months missed payment might nearly eliminate all of this gain.

with regards to the 5 transactions, many banks use this as a criteria to get bonus interest, because they sell your purchasing data and want to make sure that you are using the card so they can track what you buy and monitor your spending so that it can get fed into the banks financial information systems. This is how they offset the ‘cost’ of providing you such a horrendously low interest rate… oh the irony…

Hi there. Just for interest, UBank has a high interest savings rate of 1.6% (ING has just dropped theirs to 1.5% as of a day or 2 ago) but much more importantly, with UBank, you can have multiple Savings accounts (USave), with one linked to a transaction account (USpend), and the bonus interest rate is applied to ALL your savings accounts, providing you meet the criteria…$200 minimum deposited each month, no more than $250,000 balance across all accounts. This to me is a real advantage over ING , who I am also with, by the way. Being a Barefoot follower, my everyday accounts are with ING and my Mojo is with UBank, but I also like to separate my money into different pots to save, and UBank is the way I will go to do this in future.

Thanks for the great post,

Sharon

Hey Sharon, UBank are also great and I do have an account with them where I was storing my property deposit funds, although I haven’t been using it much since I ploughed it all into the development. I actually love their sweep functionality which can keep a threshold amount in a checking account, and then you can have the majority in the savings. I am actually in the process of doing up a bit of a review on UBank at the moment. Boy does their customer service and network suck though, I have been locked out of funds before when the whole system has gone down.

Interesting. I’m with ING and get charged an annual fee of $299. I’m a bit ticked off with that.

Thats a bit odd – are you not meeting the $1000 per month and 5 transaction rule? or potentially you have a credit card with them that you don’t know about?

I’m not a customer of ING bank, but here’s a negative experience. I transferred money in AUD from my personal account to a family member’s account at ING, which was returned as ‘unable to accept’. The bank and mine are not willing or permitted to give the reason, and therefore I can’t attempt to fix the problem. Owing to the differences in exchange rate, when the money was re-credited to my account, there was a £50 shortfall. Neither bank is prepared, to date, to accept responsibility for this loss to me. have written to ING customer services to request that since this loss is a consequence of their action, the reasons for which remain secret, they should take responsibility for the consequences. No reply as yet.

I am considering applying to the FSO in Australia for assistance. It is not a large sum, but as a pensioner it matters to me. My view is that the operators of the financial system should accept responsibility for disadvantaging the users of the system.

My term deposit just matured, and they are now offering me FAR less than before (0.22%) – in fact quite a lot lower than some of the other commercial banks in Australia, with whom I also have accounts. Other banks offer ‘loyalty bonuses’ and the like as well. Just saying.. they WERE good, once upon a time 🙂

I say, move your money to where the best interest rate is so long as its got the 250K government guarantee. Or consider alternate investments

ING’s website is not working correctly with Safari or Firefox at the moment and it is preventing people creating an account at the bank. Apparently this has been a problem for sometime. I was told that IT is working on it but that there is no timeframe for resolution and that I should check back next month.

Not a great way to win over potential new customers.

Hey Keith yea that sucks. Is it working yet? I have experienced issues with all of the banks I have been with, not just ING. They take their security pretty seriously when it comes to websites and server maintenance

No mate, still not working. I used another browser in the end. Given the ubiquity of iOS users, it’s pretty short sighted of them.

yeah thats disappointing. I guess goes to show the lack of agility in huge organisations