Complete review of Vanguard Diversified High Growth Index ETF (ASX:VDHG) from a long term index fund investor who has reached Financial Independence.

Vanguard Diversified High Growth Index ETF (ASX:VDHG) review

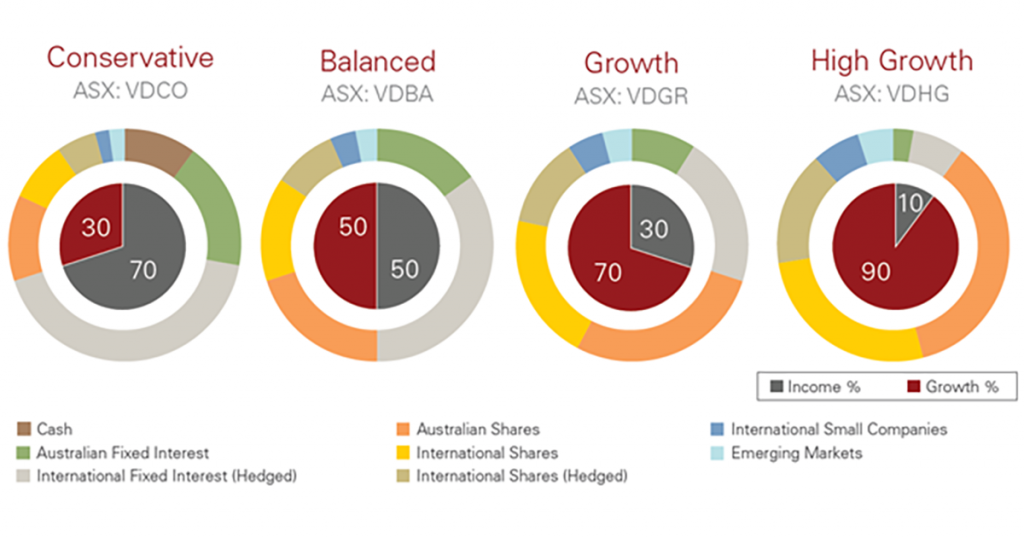

Vanguards diversified high growth index fund (ASX:VDHG) is one of four of Vanguard’s newest diversified ETF offerings offering broad asset allocation with different ‘risk tolerance themes’ within one convenient ETF ‘wrapper’ – VDHG is for high growth, and is predominantly invested in shares (90% shares or growth, and 10% income or defensive).

“Vanguards Diversified High Growth Index Fund is suitable for buy and hold investors seeking long term capital growth, and with a higher tolerance for the risks associated with share market volatility.”

Vanguard Australia

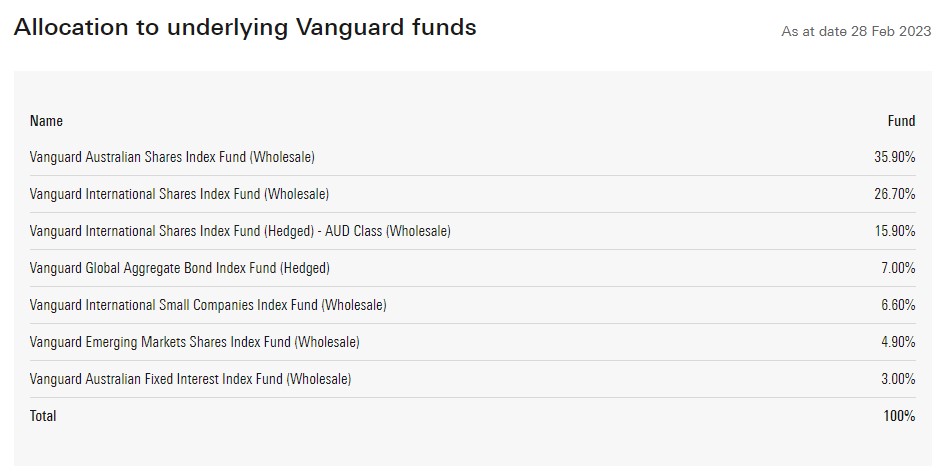

VDHG is a combination of several other Vanguard funds spread across a range of asset classes such as Australian shares, International shares (Hedged and un-hedged), International Small companies shares, Emerging markets, Bonds (fixed interest) ETFs and cash. Vanguard report that the total fund size of the equivalent wholesale fund is over $1.92 Billion.

The Good

- Very simple – you just need one ETF!

- Global diversification

- Less brokerage costs than a multi-ETF portfolio

- Vanguard automatically rebalances for you

- Vanguard Fund manager sets asset allocation

The Bad

- Higher MER than A200/VTS/VEU split

- Contains 10% defensive assets (cash/bonds)

- Vanguard Fund manager sets asset allocation

- When buying VDHG, you buy underlying holdings that might have gone up in price by a lot

- When selling VDHG, you sell underlying holdings that might have gone down in price by a lot

Verdict: VDHG is an all-in-one Globally diversified ETF that holds 90% growth assets and 10% defensive assets.

It is a simple and easy option for investors, but there is less control over asset allocation and rebalancing and slightly higher management fees than you get if you built your own ‘DIY’ equivalent.

Its closest equivalent ETF is Betashares DHHF which is an all-in-one fund with 100% growth assets

CaptainFI is not a Financial Advisor and the information below is not financial advice. This website is reader-supported, which means we may be paid when you visit links to partner or featured sites, or by advertising on the site. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Vanguard Diversified High Growth Index fund (ASX:VDHG)

VDHG provides low-cost access to a range of sector funds, offering broad diversification across multiple asset classes. The High Growth ETF invests mainly in growth assets, and is designed for investors with a high tolerance for risk who are seeking long-term capital growth. The ETF targets a 10% allocation to income asset classes and a 90% allocation to growth asset classes.

Vanguard Australia

The launch of the four Diversified Vanguard ETFs grows Vanguard Australia’s ETF offerings to a total of 22 funds, with total ETF funds under management of $9.4 billion.

Vanguard Diversified High Growth Index fund (ASX:VDHG) holdings

VDHG consists of 7 separate wholesale Vanguard index funds, built in a ratio that is suitable to most investors who want a predominantly growth asset – VDHG has a breakdown of 90% Growth, and 10% Defensive assets.

These Vanguard index funds can be bought separately, and whilst not identical, these are the most similar index ETFs which you could use to ‘Roll your own’ version of VDHG if you wanted to control the breakdown a little more (or get rid of those bonds and fixed interest funds!).

- Vanguard Australian Shares – ASX:VAS – Management fee: .10%

- Vanguard international shares – ASX:VGS – Management fee: .18%

- Vanguard international shares (Hedged) – ASX:VGAD – Management fee: .21%

- Vanguard international small companies – ASX:VISM – Management fee: .32%

- Vanguard Emerging Markets – ASX:VGE – Management fee: .48%

- Vanguard Global aggregate Bond – ASX:VBND – Management fee: .20%

- Vanguard Australian Fixed Interest Fund – ASX:VAF – Management fee: .15%

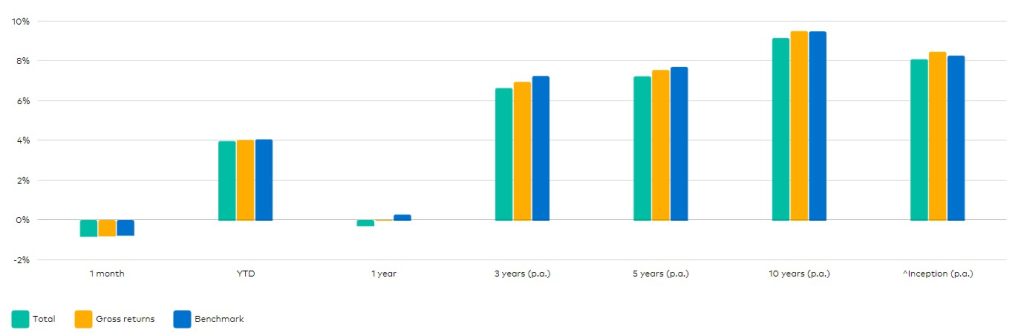

Performance of Vanguard Diversified High Growth Index fund (ASX:VDHG)

“Vanguard Diversified High Growth Index ETF seeks to track the weighted average return of the various indices of the underlying funds in which it invests, in proportion to the Strategic Asset Allocation, before taking into account fees, expenses and tax.”

Vanguard Australia

VDHG is a fairly new fund, launched in November 2017 giving it only a few years of history to look at. However, some of its constituent ETFs have been around much longer – so delving into those would give you a bit of an idea about how things might play out moving forward. Of course, you then enter the tricky domain of asset allocation and how the fund breakdown and re-balancing over time influences total return of the portfolio.

VDHG Capital price growth

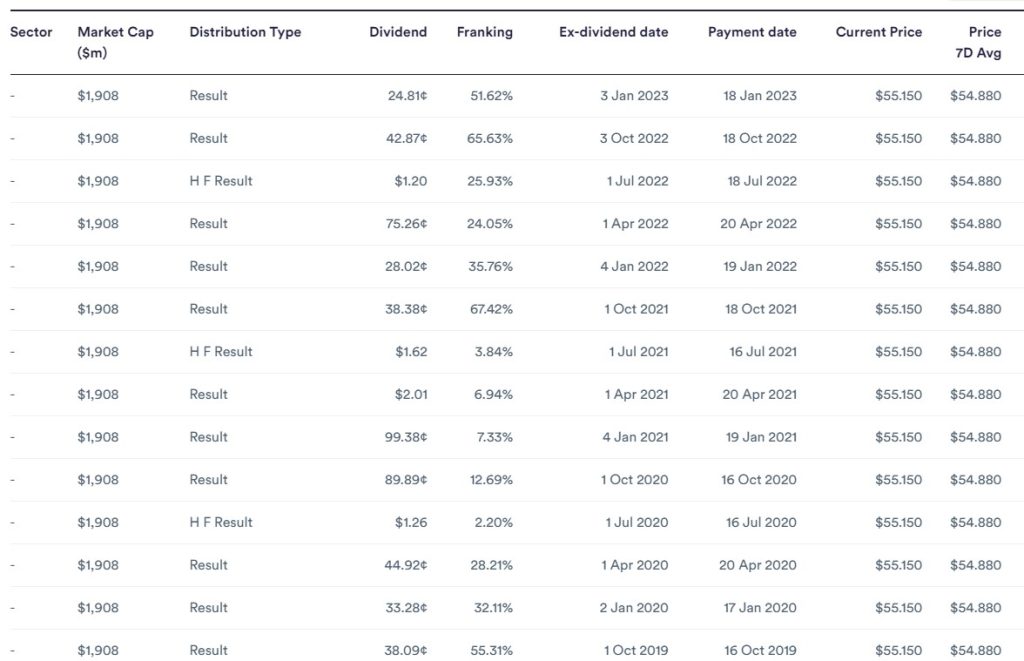

VDHG Dividends

VDHG is predominantly a growth fund, and contains many international shares. International shares typically lean towards retaining dividends and reinvesting in the company to grow, and correspondingly growing the company share price. VDHG does contain around 36% Australian shares though (as well as bonds and fixed interest) which typically produces franked dividends. As a result, VDHG does pay out a dividend that is partially franked (on average around 1/3 franking).

Over the past year, it has roughly provided a dividend of $2.94 with 19% franking. At the current share price of $53.20 this represents a dividend yield of 5.5% or a grossed up yield of 5.9%, which is pretty attractive just based on dividend yield alone.

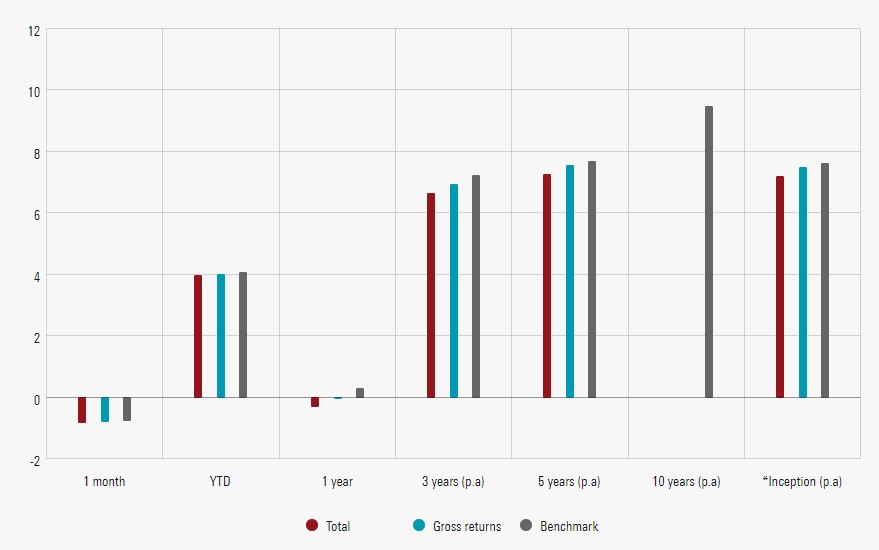

VDHG total Returns

VDHG total returns have been pretty much bang on the benchmark, hovering around 7% since its inception. However, it is worth noting that it is a pretty new fund, so it doesn’t have accurate data for the 10 year performance figures. For these figures we have to dig a little deeper and maybe do a bit of substitution…

Just because the listed ETF fund option is new though, doesn’t mean this is a new concept. Vanguard has had the following index fund products available for a long time as investment fund options for customers (listed with their respective constitution dates), so you can look into them to get an idea of what the performance of the VDHG might be like.

- Vanguard Balanced Index Fund – 30 July 2002 – This aligns to ASX:VDCO

- Vanguard Conservative Index Fund – 30 July 2002 – This aligns to ASX:VDBA

- Vanguard Growth Index Fund – 30 July 2002 – This aligns to ASX:VDGR

- Vanguard High Growth Index Fund 30 July 2002 – This aligns to ASX:VDHG

The most similar fund to VDHG is the Vanguard High Growth Index wholesale fund, which actually has a slightly higher management fee of .29% MER when administered by Vanguard. Below are the Vanguard High Growth Index wholesale fund performance, taken from Vanguard’s website.

Now maybe it is a stretch to compare VDHG to the wholesale fund, but as far as I can tell, they pretty much contain the same things and are being run by the same company (so likely to have the same fund managers?). Either way, don’t take this as gospel because there are so many variables and well, past performance is no indicator of future performance.

Management and fees of Vanguard Diversified High Growth Index fund (ASX:VDHG)

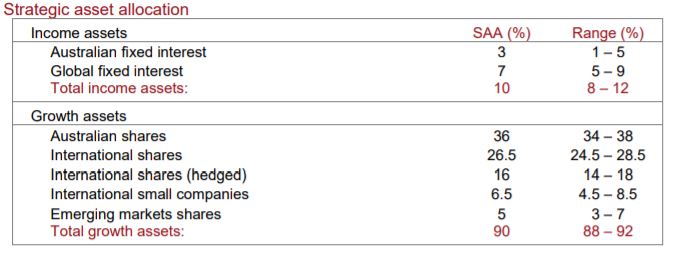

The fund management team at Vanguard are able to change the portfolio somewhat in line with the Strategic Asset Allocation goals as shown below.

But the real benefit lies here in the automation of rebalancing that occurs to keep the fund in line with this strategic Asset allocation

A major advantage for investors using these ETFs is that they can rely on Vanguard’s investment experts to continuously assess their portfolio’s exposure and periodically rebalance it back to its intended level of risk.

Vanguard Australia

This means you do not have to do this yourself – saving you time, and depending on how frequently you would have chosen to re-balance, you could save a lot on brokerage too.

This saving is offset because the Management Expense Ratio (MER) for VDHG is 0.27% p.a, which is obviously a fair bit higher than your basic stock market index funds like A200, VTS and VEU. It is worth noting that VDHG is a slightly more complex product and does give you exposure to things like small companies and emerging markets which these conventional index funds don’t contain, which is always going to drive up the management fees of any portfolio.

At .27% p.a., a $10,000 investment will cost you $27 per year – or a portfolio of $100,000 would be $270 per year. This isn’t sent to you as a bill but is automatically deducted from your returns. All things considered, this isn’t too bad, especially for the convenience / automation / time-saving.

Should I own Vanguard Diversified High Growth Index fund (ASX:VDHG)?

I like Vanguard. I have plenty of money invested with them in their low-cost ETF structures. So why do I like Vanguard so much? Simple -because it is the ‘credit union’ of investments – no one is profiting off of your investments except yourself. Profits are fed back to benefit members by reducing fees.

What sets Vanguard apart, and allows Vanguard to put investors first around the world – is the ownership structure of The Vanguard Group, Inc. Rather than being publicly traded or owned by a small group of individuals, the Vanguard Group is owned by Vanguard’s US domiciled funds and ETFs. Those funds, in turn, are owned by their investors.

Vanguard Australia

This mutual structure aligns our interests with those of our investors and drives the culture, philosophy and policies throughout the Vanguard organisation worldwide. As a result, Australian investors benefit from Vanguard’s stability and experience, low costs and client focus.

So, Vanguard and their ETFs are generally good, but what about the VDHG fund specifically? Well there are a few awesome benefits

- Broad diversification

- Relatively Low cost

- Low Maintenance

- Very Simple – don’t need to know about ‘investing’

- Reduces risk of ‘tinkering’ and self sabotage

- Automated re-balancing

However, you need to consider the following

- Fees of VDHG vs Constructing your own portfolio

- Bonds in VDHG vs 100% stocks

- Small Caps and Emerging market funds in VDHG vs conventional market cap weighted index funds

- Tax efficiency of VDHG

Fees of VDHG

The first is fees. I currently invest predominantly in the A200, VTS and VEU Exchange traded funds, which have a MER of .07%, .03% and .08% respectively. Whilst these funds aren’t exactly the same product, and management fees aren’t everything, the .27% fee of VDHG is a steep increase – nearly four times the price. On a portfolio of $250,000, the difference in fees is about $500 per year. Not anything too crazy, but still a significant factor.

However we should still remember that VDHG contains emerging markets and small caps, and if we wanted to add these ETF funds separately they would drive up our total portfolio costs.

- Vanguard international small companies – ASX:VISM – Management fee: .32%

- Vanguard Emerging Markets – ASX:VGE – Management fee: .48%

When we consider constructing a portfolio with all of VDHG’s constituent funds in the same proportion, According to PassiveInvestingAustralia5, it ends up costing you about a .19% MER. Of course, when ‘rolling our own’ portfolio you need to consider the brokerage fees too. At about $10 a trade, re-balancing yearly on each seven funds would be about $70. Therefore, on a portfolio of $250,000, you might save yourself around $130 per year in fees – obviously the bigger your portfolio, the bigger your savings.

Bonds in VDHG

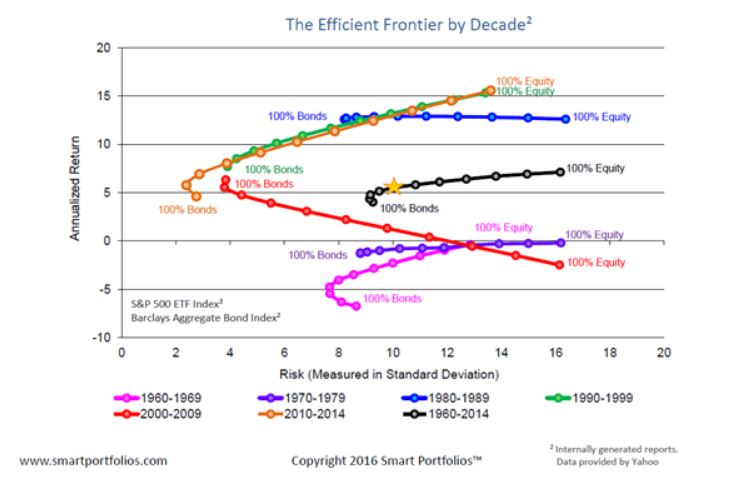

The second is the inclusion of defensive assets – cash and bond funds – to lower volatility. I have stood in ‘camp 100% stocks’ quite firmly for most of my FI journey, however I acknowledge that the inclusion of bonds in a portfolio aren’t quite as bad as I first thought. PassiveInvestingAustralia wrote a great article titled ‘Does the 10% bonds in VDHG make it a No go?6‘ which explains a bit more of the influence of bonds in a portfolio, as well as including this awesome graphic from SmartPortfolios.com

You might have thought – well bonds and fixed interest are defensive assets which under-perform growth assets in the long term, so why would I bother holding bonds when I have the stomach to ride out the volatility? This is what I thought for a long time – that bonds would proportionately lower the total return of a portfolio. However, due to the effect of periodic re-balancing of a portfolio, By having a target balance and then selling bonds to buy stocks or vice versa due to changes in the market to get back to your ideal splits, you actually end up buying low and selling high. The effect of this is not linear, but rather to drag the Risk (volatility) vs Return curve ‘up and to the left’. This means that yes, bonds do still lower the total return of the portfolio somewhat, but greatly improve the risk adjusted return and smooth the ride.

“Here is a link to Vanguard portfolio allocation models7 showing data from 1926 – 2017 and you can see that a 100% stock portfolio returned 10.3% compared to a 80/20 portfolio that returned 9.6%, a reduced average return of 7% for a portfolio with 20% of the assets in bonds. For 10% in bonds we can expect around a 3.5% lower return relative to 100% stock portfolio. Not nothing, but not far from nothing, and it does provide a benefit of diversification between asset classes and improved risk-adjusted returns.“

Passive Investing Australia6

It is such a personal decision though – for me personally, I feel I have enough discipline to maintain a ‘100% stocks approach’ and so personally want to avoid holding too much cash, fixed interest or bonds. Furthermore, I am also young, have a very long investing time-frame, and have a good entrepreneurial spirit so making money is not something I find difficult. This means that I am much happier to accept more investing risks in my personal circumstances. For more reading on a FI journey with 100% equities check out GoCurryCracker.8

Small caps and emerging markets in VDHG

VDHG contains more exposure to smaller companies, through the small caps and emerging markets funds, which does increase your exposure and give you more diversification

“Each Vanguard Diversified Index ETF provides investors with extensive global exposure to around 6500 individual companies and more than 5000 fixed income securities.”

Vanguard

However, I am personally not quite sold on this factor yet. I can appreciate that your conventional market cap weighted index funds are basically Blue Chip Behemoths – but that is also kind of the point. By investing in these traditional index funds we are getting some of the world’s biggest, established and most successful companies and profit machines. When a small-cap stock finally gets big enough, it will automatically be included in the standard index! We aren’t trying to beat, time or pick the market – we just want to be the market.

History has shown us that whilst some smaller companies might have some meteoric rises, there are also some big crashes too – making it a little more risky. But, conventional logic would say that high risk = high reward…. According to Investopedia, some Key takeaways on small caps (and somewhat relevent to emerging markets also) are;

“Individual small-cap stocks offer higher growth potential, and small-cap value index funds outperform the S&P 500 in the long run.

Small caps also experience higher volatility, and individual small companies are more likely to go bankrupt than large firms.

The opportunities of small caps are best suited to investors who are willing to accept more risk in exchange for higher potential gains.”

Investopedia9

I am not fully sold on the risk / return of small cap index funds just yet, but it is something I will be paying some more attention to in the future to see whether it might be worth adding a small cap index fund to the FI portfolio. I’m not too fussed on the volatility, and will be reading to see whether this does actually pay off in terms of tangible long term rewards that exceed conventional market cap index funds.

Tax efficiency

Having all of your portfolio in the one fund can make your tax a bit easier, since Vanguard realistically manage it all for you. You will receive some franking credits to help offset the tax on any dividends, and then you will pay capital gains tax when you sell off any shares of the fund and realise your gain. However, there are some interesting tax implications raised by PassiveInvestingAustralia which can actually lower the overall return of the VDHG fund compared to if you constructed your own portfolio…

“Another tax inefficiency with the diversified funds (both the ETFs and the managed fund equivalents) is that the underlying funds held within are the managed funds and not the ETFs, and since ETFs are more tax efficient, holding the underlying ETFs yourself would be more tax efficient than holding the all-in-one funds.

The reason why ETFs are more efficient is that in managed funds, other investors selling their units triggers capital gains for all investors of the fund. So even if you don’t sell any units, you still have to realise gains. This doesn’t occur with ETFs due to their tax structure and instead you defer these capital gains until you sell your ETF shares.”

Passive Investing Australia5

Conclusion

Vanguard’s diversified high growth index fund ETF (ASX:VDHG) offers high growth by being predominantly invested in shares – 90% shares or growth assets, and 10% income or defensive assets. It is a combination of Australian shares, International shares (Hedged and un-hedged), International Small companies shares, Emerging markets, Bonds (fixed interest) ETFs and cash. The market capital (size) of the VDHG ETF itself is over $498.6 million, and Vanguard report that the total fund size of their equivalent wholesale fund is over $9.2 Billion.

I personally am not an investor in VDHG, and instead I do the ‘Roll your own’ strategy where I am combining A200, VTS and VEU Exchange traded funds to form my own FI Portfolio in line with my investing strategy. I am exploring the concept of small cap index funds and whether I need to add a small cap fund to my portfolio to give it similar exposure to VDHG.

Make sure you check out the relevant Product Disclosure Statement for Vanguards Diversified High Growth Index Fund10 and carefully consider if it’s suitable for you before deciding to buy it or not. If you get stuck, maybe it’s worth having a chat to a licenced financial professional.

Frequently asked questions about Vanguard VDHG

Answers to frequently asked questions about VDHG

What is VDHG made up of?

VDHG is made up of a mix of Australian and international shares, global aggregate bonds and the Vanguard fixed interest fund. This is approximately 36% Australian shares, 26.7% international shares, 16% in international hedged shares, 6.6% in international small cap shares, 5% in emerging markets shares, 7% in global aggrege bonds and 3% in the Vanguard fixed interest fund.

- Vanguard Australian Shares – ASX:VAS – Management fee: .10%

- Vanguard international shares – ASX:VGS – Management fee: .18%

- Vanguard international shares (Hedged) – ASX:VGAD – Management fee: .21%

- Vanguard international small companies – ASX:VISM – Management fee: .32%

- Vanguard Emerging Markets – ASX:VGE – Management fee: .48%

- Vanguard Global aggregate Bond – ASX:VBND – Management fee: .20%

- Vanguard Australian Fixed Interest Fund – ASX:VAF – Management fee: .15%

Is VDHG an ETF?

Yes, VDHG is an ETF (Exchange Traded Fund). It is actually an ETF that combines 7 other Vanguard ETFs under one fund for convenience.

Is VDHG Franked?

Yes, VDHG is partially franked. VDHG holds approximately one third Australian shares as ASX:VAS, which passes on franking credits from Australian shareholders. Any Franking credits received from the underlying holdings in VDHG passed out as dividend franking credits are passed on to the VDHG shareholders.

Is VDHG an index fund?

Yes. VDHG is a diversified index ETF which itself holds seven index fund ETFs across the asset classes of Australian and international shares, bond and fixed interests.

Does VDHG pay dividends?

Yes, VDHG pays dividends which are partially franked.

Is VDHG a good investment?

VDHG is a good investment for someone who is time poor with a long investment timeframe. I personally think the A200 / VTS / VEU split gives more control over your portfolio and is cheaper in terms of brokerage and management fees, but if you don’t care then VDHG is a fantastic one size fits all investment offering broad diversification for a passive investment strategy.

How to invest in VDHG

To invest in VDHG you can search ASX:VDHG from an Australian share trading platform (broker). As it is an ETF, this has a market maker and always trades approximately fair value, so the best option is to place ‘Market Price’ buy orders rather than ‘Limit Price’ orders.

What is the most aggressive Vanguard fund?

The high growth index ETF VDHG is the most aggressive of the Vanguard diversified index ETFs.

Further reading

Financial Disclaimer

Financial Disclaimer: CaptainFI is NOT a financial advisor and does not hold an AFSL. This is not financial Advice!

I am not a financial adviser and I do not hold an Australian Financial Services Licence (AFSL). In this article, I am giving you factual, balanced information without judgment or bias, to the best of my ability. I am not giving you any general or personal financial advice about what you should do with your investments. Just because I do something with my money (or use a particular service or platform) doesn’t mean it is automatically appropriate for your personal circumstances. I do not recommend nor endorse any financial or investment product, and my usage or opinion of any product should not be interpreted as an endorsement, advertisement, or intent to influence.

I can only provide factual information based on my journey to Financial Independence, and that is provided for general informational and entertainment purposes only. I make no guarantee about the performance of any product, and although I strive to keep the information accurate and updated as it changes, I make no guarantee about the correctness of reviews or information posted.

Remember – you always need to do your own independent research and due diligence before making any transaction. This includes reading and analysing Product Disclosure Statements, Terms and Conditions, Service Arrangement and Fee Structures. It is always smart to compare products and discuss them, but ultimately you need to take responsibility for your use of any particular product and make sure it suits your personal circumstances. If you need help and would like to obtain personal financial advice about which investment options or platforms may be right for you, please talk to a licensed financial adviser or AFSL holder – you can take the first steps to find a professional financial adviser by reading this interview, or by visiting the ASIC financial adviser register12 and searching in your area.

For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Wow that dividend yield is super attractive. How comes it’s so high ? Bearing in mind the bonds and hedged etc ?

Yeah it took me by suprise too mate. I’m not too sure why its so high – I assumed this would be a lower dividend paying fund because exactly as you say with the bonds, cash, hedging and international shares. If you look historically the dividends haven’t been as high, and look closer to averaging about 30c per quarter or 2-3% dividend yield. So I wouldn’t get too sexed up about the rolling 1 year dividend history.

I was recommend this by a financial advisor when I explained I was looking for long term, high risk. I feel maybe I should change if I am looking for wealth accumulation?

Sorry Sash I don’t quite follow you there, are you saying long term high risk is different to wealth accumulation?

Thanks Captain . You have inspired me to remember the

” Kiss Principle ” .

Regards , Ramon .