BKI is an Australian Listed Investment Company who’s strategy is to invest in a diversified portfolio of around 50 Australian shares, trusts and interest bearing securities. Read the full review

BKI investment company limited was listed on the ASX in 2003 to take over the Brickworks Investment Company portfolio, a LIC that had been listed since the 1980s. Whilst the smaller of the large Aussie LICs, BKI still manages a sizeable portfolio of over (AUD) one billion dollars, which it has grown from the (AUD) $173 Million it started managing in 2003.

BKI objectives and strategy are to invest in a diversified portfolio of around 50 Australian stocks, trusts and interest bearing securities. BKI’s main aim is to generate an increasing income stream for shareholders using fully franked dividends, and their secondary aim is to deliver long term capital growth to shareholders, through long term holdings in a portfolio of diversified assets.

“Today, some 30 years since the inception of the core portfolio, BKI’s investment strategy is focused on research driven, active equities management, investing for the long term, in profitable companies, with a history of paying attractive dividend yields.”

BKI investment company limited

CaptainFI is not a Financial Advisor and the information below is not financial advice. This website is reader-supported, which means we may be paid when you visit links to partner or featured sites, or by advertising on the site. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

The Details

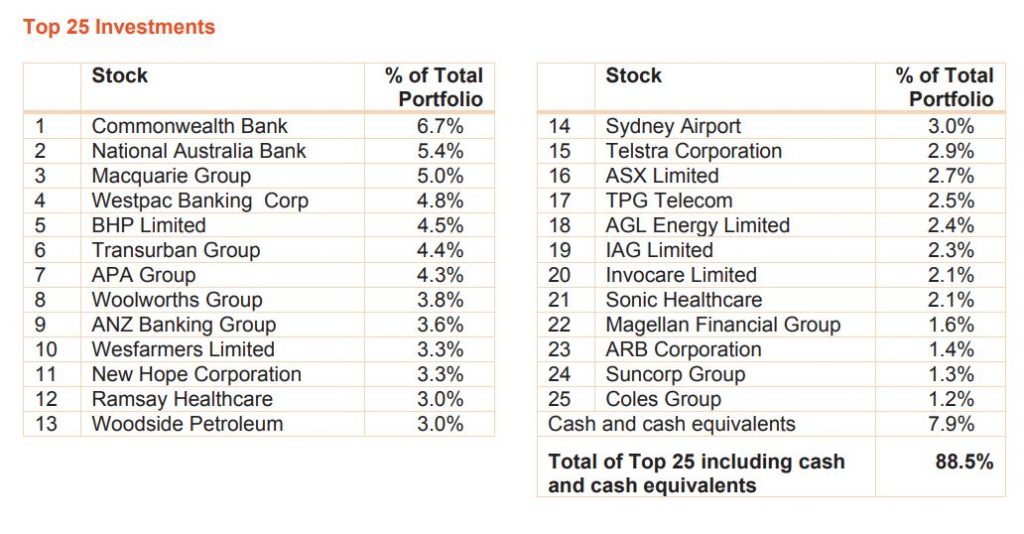

Although mainly holding Australian stocks, in their June 2019 quarterly report BKI estimate that over 51% of their holdings are exposed to global stock market factors. This is in response to criticisms of ‘home bias’ and only buying Australian companies. Amongst these globally influenced holdings are BHP group limited (BHP), Woodside Petroleum (WPL) and Ramsay healthcare (RHC) which all get the majority of their income from international revenue.

In 2016, BKI outsourced its management responsibilities to Contact Asset Management. BKI has an annual Management Expense Ratio of .10%, which still makes it one of the cheapest Aussie LICs to own, despite being over twice the management fee of Vanguards US total market ETF, VTS at .04% MER.

I like that the directors and portfolio managers of BKI are all large shareholders, and that the focus is on dividend payments. Its chairman Robert Millner, Director and portfolio manager Tom Millner, and Director and portfolio manager Will Culbert have strong family ties and history in managing BKI prior to creating Contact Asset Management (jointly owned by Tom Millner – 40%, Will Culbert – 40%, and Washington H Soul Patterson – 20%).

Share turnover is low, as they don’t often sell shares, but often add to existing holdings. This focus keeps costs and tax burdens low, allowing them to focus on dividend growth for investors.

“The Group aims to generate an increasing income stream for distribution to shareholders in the form of fully franked dividends to the extent of available imputation tax credits, through long-term investment in a portfolio of assets that are also able to deliver long term capital growth to shareholders.”

BKI investment company limited

Performance

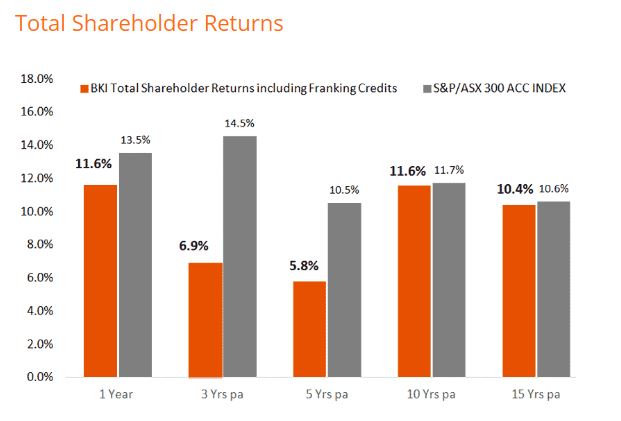

In the year ending June 2019, the total shareholder return (including franking credits) was 11.6% which under performed the S&P/ASX 300 Index by 1.9%. Over the past 15 years, BKI has returned shareholders a total return (including franking) of 10.4% per year.

BKI is currently offering a franked dividend yield of 6.1%, grossed up to 8.8%. This is a very attractive dividend yield, but based on total shareholder return it can see that BKI has under performed some of the other Aussie LICs in terms of capital growth on the portfolio.

Whilst it can be seen that BKI has under performed the index in recent years, BKI has a long term focus on income producing investments and its directing staff are not too concerned about short term noise – they are also holding a fairly large cash holding of 8% (over $100 Million in cash) and are ready and looking to purchase good quality companies, but this is a drag on their total returns.

“The Group will pay the maximum amount of realised profits after tax to its shareholders in the form of fully franked dividends to the extent permitted by the Corporations Act, the Income Tax Assessment Act and prudent business practices from profits obtained through interest, dividends and other income it receives from its investments. Pay Out Ratio Target: 90% – 95% of the Net Operating Result

BKI investment company limited

At the moment there is generally a bit of a lack of earnings growth in the market, and the P/E multiple of the market is increasing as interest rates continue to be lowered – making it more difficult for LICs to snap up a bargain. Over the past year BKI have reinvested in more mining/resource, financial, energy and healthcare stocks, tipping that the mining sector particularly is one of the more attractive sectors given current market conditions.

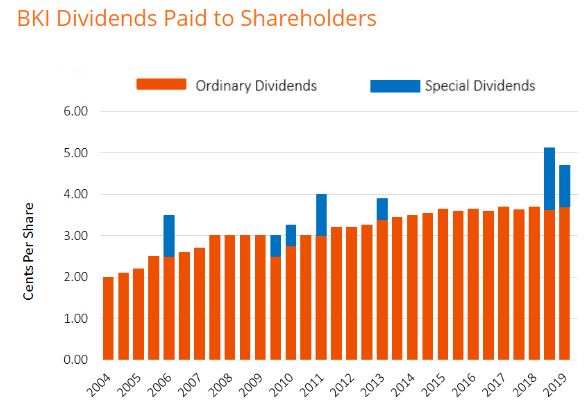

BKI have been able to consistently increase their dividend yield. One way of calculating this is to look at the year on year dividend growth. Using a simple spreadsheet it is seen the yearly dividend growth rate starts at 7.5%, then 16.28%, then 6% and so on, with negative growth occurring in 2012 and 2014, and a record 34% growth in 2019 after three years of dividend stagnation. On average, this works out to be a 6.6% dividend growth over 15 years. A more safe bet at calculating dividend growth is as follows;

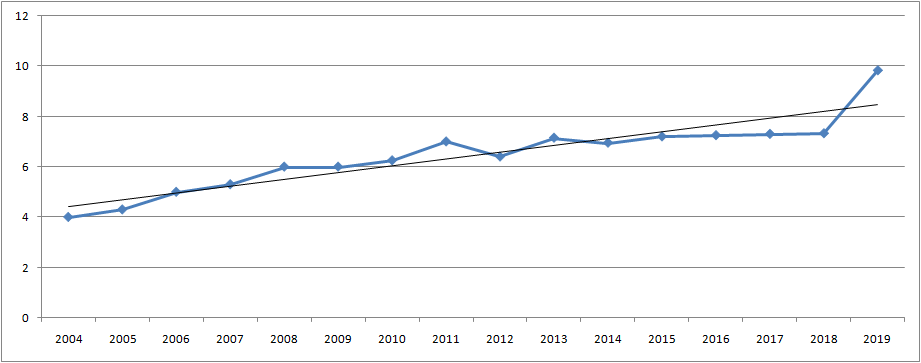

The linear trend above has a an R² value of 0.847 which shows a fairly good fit for our purposes of approximation (the closer to 1 the better the fit). This line has a slope of .271, meaning that on average, starting at around 4c per share in 2004, BKI dividend yield has increased by .271 cents per year. With an average dividend of 6.45 cents over the last 15 years, this means dividend growth has been 4.2% of the average dividend yield over this period – compared to 2.4% average rate of inflation according to the Reserve Bank of Australia.

BKI Investment Company review, CommSec Executive series with Will Culbert

Conclusion

BKI investment company limited is a Listed Investment Company (LIC) that was listed on the ASX in 2003 to take over the Brickworks Investment Company portfolio, a LIC that had been listed since the 1980s. Whilst the smaller of the large Aussie LICs, BKI still manages a sizeable portfolio of over (AUD) one billion dollars, which it has grown from the (AUD) $173 Million it started managing in 2003.

BKI investment companies’ objectives and strategy are to invest in a diversified portfolio of around 50 Australian stocks, trusts and interest-bearing securities with an aim to generate an increasing income stream for shareholders using fully franked dividends, with a secondary aim to deliver long term capital growth to shareholders.

I have previously owned BKI, but I don’t currently own it. As always, just because I do or don’t own stock doesn’t automatically make it a good idea for you to do the same. You should do your own independent research into BKI and carefully consider your personal circumstances before making any investment choices.

Financial Disclaimer

Financial Disclaimer: CaptainFI is NOT a financial advisor and does not hold an AFSL. This is not financial Advice!

I am not a financial adviser and I do not hold an Australian Financial Services Licence (AFSL). In this article, I am giving you factual, balanced information without judgment or bias, to the best of my ability. I am not giving you any general or personal financial advice about what you should do with your investments. Just because I do something with my money (or use a particular service or platform) doesn’t mean it is automatically appropriate for your personal circumstances. I do not recommend nor endorse any financial or investment product, and my usage or opinion of any product should not be interpreted as an endorsement, advertisement, or intent to influence.

I can only provide factual information based on my journey to Financial Independence, and that is provided for general informational and entertainment purposes only. I make no guarantee about the performance of any product, and although I strive to keep the information accurate and updated as it changes, I make no guarantee about the correctness of reviews or information posted.

Remember – you always need to do your own independent research and due diligence before making any transaction. This includes reading and analysing Product Disclosure Statements, Terms and Conditions, Service Arrangement and Fee Structures. It is always smart to compare products and discuss them, but ultimately you need to take responsibility for your use of any particular product and make sure it suits your personal circumstances. If you need help and would like to obtain personal financial advice about which investment options or platforms may be right for you, please talk to a licensed financial adviser or AFSL holder – you can take the first steps to find a financial advisor by reading this interview, or by visiting the ASIC financial adviser register and searching in your area. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

BKI have never owned CSL.

A ridiculously poor error of judgment.

Hi Carlos, yeah CSL has done quite well hasn’t it. Why do you think they didn’t include it in their portfolio? Do you buy LICs or just ETFs? I can see that if you went with a purely ETF portfolio you wouldn’t miss out on stuff like this

They have fallen for the age old trap of avoiding stocks which APPEAR to have low dividend yields.

But in fact CSL have grown their dividends consistently every year at an outstanding rate and I have read that shareholders who bought 20 years ago have received more in dividends than Telstra shareholders have !

Ramsay is a similar case.

Therein lies the best rule of long term investment : buy companies with growing future profits as these will also grow their dividends. Not companies that have high dividends yield now as often the dividends will remain the same or perhaps will be cut ( as per Telstra and recently the banks ).

In reply to your second question, I buy everything at various times, LICs, ETFs, ETMFs, direct shares and unlisted managed funds . But the old school LICs have been underperforming the XAO over the past 1, 3, 5 and 10 year periods which shows they are not good enough for a whole portfolio as promoted by some people. I only buy them at good discount ( 5%+ ) to NTA and cannot believe how they sometimes trade at a premium……ridiculous.

Currently I hold ARG, MLT, PIC, WLE, WMI, OPH, MIR, WGB, MGG, MFF, VG1, MXT.

I know the newer LICs charge higher fees but I prefer the more active approach rather than index hugging.

ETMFs are a great innovation as you always buy and sell around NAV. Bring on more of them.

Wow, Carlos sounds like you have a pretty good grasp of this and a lot of experience investing in these financial products. Thanks for sharing. I am also long on Argo and Milton, although recently I have been debating going into a more ‘all ETF’ portfolio. For some reason I am tempted by the ability to buy a LIC below its NAV, I agree 5% is a great number, but I have been guilty of buying on as low as a 3% discount because I felt I was getting a bargain. I think I will be revising my investing strategy soon too but possibly just looking at a pure VEU, VTS and VAS split. I’m pretty faithful in Vanguard as a company