Unless you’ve been living under a rock, you’ve probably heard of the Barefoot Investor. But Does the Barefoot Investor work? I review his steps to reach financial independence and explain how this book changed my life forever

Barefoot Investor Review

The Barefoot Investor, written by Scott Pape is a great book. It is packed full of great financial advice that can help you grow your wealth. I stumbled across this book in 2016, and it actually was one of the things that got me very interested in finance and growing my wealth.

You can continue living in the past, beating yourself up about the money mistakes you made when you were younger, telling yourself you’ve left it too late… or you can rise up and make yourself proud.

Scott Pape

In this article I will present my review and ask the question “Does the Barefoot Investor Work”, along with my personal experience of using his steps and my reflection several years later.

The Good

- Easy to read Step by Step guide

- Very cheap for the advice you get

- Proven money management technique

- Scripts you can read out word for word to service providers (banks, telco, insurance brokers etc) to get better deals and discounts

- Hard copy and digital copies available

The Bad

- Conservative views

- Encourages everyone to buy a home (not possible for everyone in Sydney or Melbourne!)

- Does not encourage investing before paying off home

- Limited advice on how to invest in shares

- Hates ALL forms of debt – although tolerates mortgages for PPOR

Verdict: You MUST read The Barefoot Investor.

No products found.

CaptainFI is not a Financial Advisor and the information below is factual review information, and general advice, not financial advice. This website is reader-supported, which means we may be paid by advertising on the site, or when you visit links to partner or featured sites. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Who is the Barefoot Investor written for?

The Barefoot Investor is targeted at your average Aussie who is trying to improve their financial situation and their financial future. This person has little to no knowledge on finance or investing, and potentially has poor self discipline and self control, with unreasonably large spending habits.

It is a beginner’s book, but it is so foundational that I believe it is something everyone should read as there is hard, actionable advice that anybody can take to grow their wealth and their money management habits.

No products found.

The Barefoot Investor

The Barefoot Investor is presented in a very easy to read and straightforward format. After Scott Pape introduces himself and the context of the book, he explains his simple nine step guide to financial success. These start with essentially taking time out with your spouse or significant other to get serious about your money, and progress all the way through to planning for retirement and leaving a legacy after you die.

Barefoot Step 1

Schedule a monthly ‘Barefoot date night’. You can get dressed up and go to a lovely restaurant or somewhere nice to review your finances over a quality meal and glass of wine, helping to reduce the stigma of talking about money and to make it fun and memorable. It’s about positive association!

Barefoot Step 2

Set up your ‘buckets’! This is about automating how your income hits your bank account. This means using pay splits and automatic transfers to ‘put your money on autopilot’ between your needs, wants and investments.

The Barefoot Investor recommends using three ‘buckets’: The Mojo, Blow and Grow accounts.

The Mojo bucket

The first bucket is your Mojo account – your emergency fund1 or safety fund. The Barefoot Investor recommends a MINIMUM of $2000 to be raised into the Mojo. Unless you have $2000 in your emergency fund, you are having an emergency. Repeat with me “YOU ARE HAVING AN EMERGENCY”. Depending on your salary, job stability and cost of living, you might choose to raise or lower this a little, but $2K is a good number for most Aussies to start with. (I use $25K).

Unless you have this safety net, you should not be ordering Ubers or using Uber Eats, using credit cards or spending any money at all! You should in fact be eating potatoes at home with the lights and heating off wrapped in a blanket whilst madly listing all of your possessions on Gumtree, Facebook marketplace and eBay, applying for as much as the overtime you can get and considering working a second job!

Haha ok maybe we don’t have to be that extreme, but you get the idea…

Once you have your initial Mojo safety net, your Mojo bucket is happy ticking over by itself for a while. This account should be separate to your everyday expense bank account, and it should be difficult (but not impossible) to access the funds – i.e. lock the card up in your safe or freeze it in a cup of water. Check out the Barefoot Investors bank account recommendations if you are in Australia, but any no fee bank account service will work. The Mojo will be boosted later, but this is done for now!

The Barefoot investor Blow buckets

The Blow bucket is your working account, or expenses accounts. Money goes in, and Money goes out. It has the subsets of Daily expenses, Splurge, Smile and Fire Extinguisher.

Daily expenses

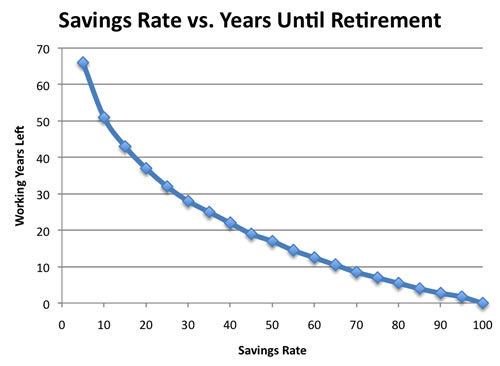

The Daily expenses account is your cost of living such as rent, groceries, petrol, insurance etc. The Barefoot Investor is a total wimp here and suggests this should be a staggering 60%, or more than half of our income!

Whilst 60% sounds like a good start for beginner Barefooters, experienced investors on the path to financial independence such as ‘Mustachians2‘ will know you can live a fantastic quality of life with an extremely low cost of living. You should aim to get this 60% number down as low as possible! The lower your cost of living, the sooner you can retire – Check out the graph below;

After I read the Barefoot Investor I got serious about investing, but even before then, I was managing to live on almost only 20% of my income, whilst travelling the world, riding ridiculous motorbikes, chasing girls (what all guys do in their 20’s, right?). Take a few simple steps to review your expenses and cut down your cost of living.

Splurge

The splurge is your kryptonite account. This is where you can indulge your lack of self control or discipline and use your Splurge account to buy stuff that you don’t need or otherwise waste your money. For example that grande-orange-caramel-double-shot-soy-mocha-frappe-latte-chino that was $12 in a disposable fluorescent plastic/foam cup that goes to landfill because you were too lazy to have one at home or bring your travel mug with one from home.

The Barefoot Investor recommends wasting up to 10% of your take-home after tax income on this account. If you ask me, this is just put in to please the masses as we tend to be brainwashed by media and bombarded with advertisements to ‘Spend, Spend, Spend, Splurge, Splurge, Splurge’. So much so, that people feel they need to waste their money on products and purchases to feel good about themselves, and get their Dopamine rush. So if the Barefoot Investor told you not to be a mindless consumer-spender, surely he would be rejected as being ‘too extreme’?

Well lucky you have CaptainFI here to slap you in the face. Your Splurge account is not necessary. I do not think this works. Since this book is designed for the masses and those with poor self control, perhaps it is meant as a starting point to help those hopelessly addicted to spending to reign it in to a more reasonable level.

Smile

Your smile account is just like the splurge account, only it’s supposedly for more ‘worthy’ purposes like going on Holidays, or splurging on larger consumer items such as gifts for yourself or others.

Again, the Barefoot Investor recommends spending 10% of your take home after tax salary on things that make you Smile. Is this necessary? Again maybe not, but the book is targeted at people with poor self control and poor self discipline who are programmed to spend, spend spend.

I think a ‘Smile’ savings account can be useful for long term goals like holidays, but a fundamental mind-shift away from ‘spending makes me smile’ is really required for long term happiness and financial security. Remember you don’t need to spend your money to make you smile, or spend money on someone else to make them smile!

Fire extinguisher

The Fire extinguisher is a great account. This is one we can all enjoy. The Barefoot Investor recommends we direct 20% of our take home income into our fire extinguisher account. This account is used to ‘put out fires’ such as credit card debt3 and is our way of deliberately increasing our allocations to certain areas.

For example, During Barefoot Step 3 (coming in a moment) we direct the Fire Extinguisher account into destroying any personal debt (bad debt) that you have using the debt domino method.

Given our discussion on the Splurge and Smile accounts (and my personal disdain for wasteful spending), a financially savvy person may choose to direct some of the money from these two wasteful accounts into boosting their very useful Fire extinguisher!

No products found.

Grow

Your Grow bucket is for your long-term wealth. The Barefoot Investor explains that your Grow bucket includes your mandatory superannuation contributions (minimum 10.5%)4, rolled over super funds from previous jobs (it is important to consolidate them into an ultra-low cost super fund) as well as any investment properties you may have. For more information, check out this article on Barefoot Investor Superannuation.

Personally, I believe you should aim to have as much of your income going into this bucket as possible. However the Barefoot Investor5 is pretty wimpy here, and I think Mr Money Mustache2 might agree with me. The Barefoot Investor is very conservative, and doesn’t suggest people allocate any extra income into their grow bucket until they have fully paid off their mortgage, hold three months of living expenses and boosted their super to 15% – but more on this in the subsequent barefoot steps.

Barefoot step 3.

Domino your debts – pay off your debts, smallest to largest, and escape the cult of credit once and for all. There are of course more logical methods to reduce debt, such as the debt avalanche technique which involves paying off the highest interest-rate debts first.

The reason the Barefoot investor recommends to use the Domino your Debt approach is due to the psychological factor of seeing debts closed out and less number of repayments being made (even if it takes a little longer and costs a bit more than a debt avalanche to fully repay everything). This psychological factor works, and so in this aspect, the Barefoot Investor definitely works!

Barefoot step 4.

Buy your home. This means buying a ‘Principle Place of Residence’ to live in, rather than renting.

This is a contentious topic, because us in the Financial Independence community know that home ownership comes with many thousands of dollars per year of hidden costs, and it is often more beneficial to ‘Rent-vest’, that is to say, to rent a house or apartment, and invest the difference. This could be in ultra low-cost index fund ETFs (taking advantage of compound interest) or even property investment in a more profitable location (lower capital values and higher rents, such as regional cities).

Depending on where you live, Rent-vesting can be a much smarter alternative. For example inner Sydney and Melbourne Cities, you would be crazy not to Rent-vest. Even the 1 bdr apartment I rented for $550 per week would cost me nearly $700 in principle plus interest repayments per week alone (depending on interest rates), and another $150 per week in council rates, strata fees, levies and insurance!

I would need a guaranteed 3% capital growth just to make up this difference and not go backwards in my net worth. Even then, all the whilst my money is being turned from cash flow (which I need to live) and getting locked up into capital appreciation of the apartment – which I will have a lot of problems trying to access (high transaction costs to sell), and I might even get TAXED on when I sell (noting there are exemptions for capital gains on your primary place of residence in most cases).

Having said that, The Barefoot Investor is tapping into the ‘Great Australian Dream’ of owning your own home. Owning your home isn’t purely a financial thing, and there are loads of great emotional reasons to want to own your own home. For example security – you can’t be evicted by your landlord if you own it, right..? (if you mismanage your finances and default on those large mortgage repayments, the bank can still foreclose on the loan and kick you out!).

If your goal is to buy your home, I think a great way is to save yourself up a 20% house deposit and avoid the horrendously expensive scam of LMI (you have to purchase the bank’s insurance for them against your loan – it doesn’t protect you at all and it usually costs over $10,000!). Save this using your wonderful Fire Extinguisher account.

To help Ramp up the savings, ditch your Splurge and make the home deposit the goal of your Smile, meaning you now have an arsenal of 40% income at your disposal to save. If you can ditch some of those expensive costs of living and live more mindfully, you could save up that 20% deposit in no time!

Barefoot step 5.

The Barefoot Investor recommends to increase your retirement savings to 15% of your income. This is a fantastic idea, especially for people who have no clue about their finances.

In Australia we have Superannuation, just like the USA’s 401K and Roth IRA, Canada’s RRSP and TFSA, and the UK’s PPP. This helps to provide a boost to your retirement by letting you contribute at a reduced tax rate of 15%, and let it grow in the reduced tax environment of 15%. When you access it in the ‘pension’ or retirement phase, it is usually tax free.

Contact your administrative / human relations team / pay cell and a company like Smart Salary6 to organise boosting your Superannuation to 15% of your salary, because in most instances you can contribute up to the concessional cap of about $27,5007.

This is taken out of your pre-tax income, not your post tax paycheck. since super contributions are only taxed at 15%, For someone on the top marginal tax rate of 45%, your effective tax savings are 30%. Your super balance gets a boost of $27,500K a year, but it’s only costing you just under $17.5K from your paycheck, meaning the government is effectively giving you $10,000 for free!

You can also make non-concessional or post tax contributions, but this is less desirable. From July 1, 2021, the non-concessional contributions cap was actually increased up to $110,000. Visit the ATO HERE10 for more info.

Check out more information on Barefoot Investor Superannuation here.

Barefoot step 6.

Boost your Mojo (emergency fund) to three months living expenses.

I think this step works for those with lumpy incomes, high risk jobs or really those without job security. If you are running your own business, work as a contractor or on a short term or casual basis then it’s an extremely smart move to do this. For those on fixed long term contracts with a reliable paycheck, such as Teachers, Police officers or doctors, then this might be overkill – it all depends on your personal situation.

For example, my living costs at the moment are approximately $30K per year, but if I needed to, I could pare that down to $20K a year living a fairly minimalist (but totally awesome and happy) life. This means I should hold somewhere between $5-8K in cash sitting in a bank account somewhere doing absolutely nothing, silently eroding and rotting away in value (purchasing ablity) due to the wealth destroying ‘rust’ of inflation.

This is where I think the barefoot investor doesn’t work. Rather than hoarding all your cash in a bank account and letting it devalue, I think this should be thrown into a mortgage offset against your PPOR or your investment property if you wisely decided to rent-vest. This reduces interest payable and due to the fact that loans aren’t taxed, it grosses up the return by 30% or more for most people and most loans – much better than the paltry interest you earn on a savings account.

Before I had an investment property, I just used to stick this into index fund ETFs. Sure the stock market fluctuates, but the goal is never to sell and only spend the dividends if you absolutely have to – but in an emergency stocks can be sold and the money goes into your account usually on T+2 or two days after the trade is complete. Index fund ETFs are a very liquid asset.

All things considered, I now keep a balance of approx $25-30k in my ‘Mojo’ and checking account, which is around one year living expenses, kept in my mortgage offset account, reducing the amount of monthly interest payable. This is a good compromise so I always have quick access to cash but I can also outsmart inflation by not having large chunks of cash sitting around ‘rusting’ away and I can make sure that my dollar employees are deployed working as hard as they can for me.

Scott Pape also covers the topic of insurance, such as private health insurance and income protection insurance and advocates strongly for these, depending on your age and your situation.

Barefoot step 7.

Get the banker off your back – Knock down your mortgage by making extra repayments! This is a risk management decision. As discussed with parking your Mojo in a mortgage offset, paying down your mortgage is a great strategy for those with risk aversion or who are very conservative with their money, but still want to get a great return on their surplus cash.

On average, paying down your mortgage returns around 6%, whilst investing in stocks return ~10%. You can read more about it in my article ‘Shares vs Property’, but the crux is that investing in stocks is riskier but will on average give you higher returns.

Work out where your personal risk appetite sits, and act accordingly. Making extra mortgage repayments on your home is a fantastic idea in any case. Building equity in the home helps knock down the balance you’re paying interest on and keeps money in your pocket, not the bank’s.

As the mortgage reduces due to this increased payment, you could even refinance to make a lower weekly payment if you are finding yourself wanting to transition to a lower paying job or wanting to invest more in index fund ETFs instead. Be warned though, this comes with an increased loan period so the total amount of interest payable increases – the banks only ever act in their own interest.

Barefoot step 8.

Nail your retirement number: Financially plan for retirement. At its most simple core, your retirement number is 25 times your annual expenses. SUPER EASY. This means if your annual expenses are $50,000, then you need $1.25M invested in index funds. If your annual expenses are $20K, then you need $500K invested in index funds.

Having a paid off home obviously lowers your cost of living, since you aren’t paying rent anymore. There are still costs of home ownership however, so remember to factor them into your cost of living. Do not include the capital value of your home in your investment number, as it isn’t actually producing you any returns in line with the 4% rule.

We saw in step 5 that Superannuation is a way to boost your retirement savings since in most cases it gets taxed lower than any investments you might have outside of super. I say in MOST cases because check out this Podcast8 by the Aussie Firebug which actually shows a case where it’s cheaper and you pay less tax to retire outside of super for a couple earning below the threshold sharing their income loading together.

When you reach preservation age, you’re likely going to get either a lump sum of money (handy for paying off any remaining mortgage or investing into ETFs) or you can keep your money in super and receive a pension / annuity (fortnightly payment for the rest of your life) or some form of combination of both. Usually it works out better due to tax reasons to keep the money in the superannuation investment vehicle and draw out a pension, on the proviso you plan to live at least another 10 years or so.

This means that you have a two-stage retirement system if you want it. Once you amass 25x your annual expenses in index funds, you can retire and you don’t actually even need super. Your taxable investment portfolio can sustain you forever, and when you get your super it’s like a ‘boost’ to your income.

There comes a point then, where your taxable investments are large enough to last you until you are eligible to access your superannuation, and then the super keeps you going for the rest of your life. This means at some stage prior to conventional retirement, you can actually quit your job if you want to. This is the FIRE hype that you hear so much about on this blog and others such as Mr Money Mustache and The Aussie Firebug.

This begs the question, just how many index funds do I need, and just how much super do I need? It is a very individual answer. Luckily a very clever blogger and software developer the Aussie Firebug developed THIS FREE TOOL9 which you can use.

For me personally, I am using superannuation as part of my transition to retirement financial planning process, and I found this calculator pretty useful!

Furthermore, social security (aged pension) is yet another safety net, capable of paying up to $18,000 ($1500 a month) to supplement any superannuation annuity should it not be enough to comfortably live on, noting that the aged pension is means tested so above a certain income you won’t be eligible for it – which is fair!

Barefoot step 9.

Leave a legacy. Step 9 is about making a permanent positive benefit. How do you want to make a difference in the world?

Personally I am going to establish a set of trust structures. One set for my family, and another set for a charitable cause.

That way, the investments within the trust can generate income, and a portion of that (up to 4% of the portfolio gain) can be distributed to the trustees, whilst still ensuring the capital value of the trust portfolio grows forever, providing an increasing stream of income that can be used to make the world a better place

How it changed my life

Throughout this article, we have talked in great detail about how I implemented the steps but really the book has changed my life. The Barefoot Investors’ 9 steps, alongside his no frills examples and literal scripts you can use to get better deals have improved my finances for life.

Yes, the Barefoot Investor literally gives you word for word transcripts you can cite to your credit card company, bank you have a mortgage with, internet/phone/insurance providers that you can use to lower your payments and get a better deal.

Not only is it about physically enacting these steps and making lasting changes in your lifestyle to improve your finances, but the book is about growing up and being a mature, responsible adult. It helped me to take responsibility for my actions, use common sense, and plan for my life ahead.

I seriously recommend you read this book, and listen to his sage advice – even if I do poke fun at him from time to time for being too softcore.

Where to buy the Barefoot Investor

If you don’t have a copy then don’t rush out to an expensive book store, there are many older copies of this book floating around (albeit a little creased and pages dog eared) on second hand sites like Gumtree, Facebook marketplace and eBay. I actually picked my copy up for 95% off in a Post Office clearance sale. I’m sure Scott Pape would recommend this sage advice – don’t BLOW your hard earned income on brand new things!

Of course, in true barefoot style, you can just borrow it from the library or read a friend’s copy. If you really must have it now, you can buy it on Amazon here.

Addition: If you liked his first book, he has written a second book called Barefoot for Families which is aimed at financial literacy for children and helping families pass on good money habits to the next generation. You can find it on Amazon here.

Frequently Asked Questions about The Barefoot Investor

Answers to some frequently asked questions about the Barefoot investor. Don’t laugh – these are legit questions that get asked ALL the time.

What pillow does the Barefoot Investor recommend?

The Barefoot investor recommends the Dunlopillow latex pillow. No this is not a joke. He buys these as gifts for all his employees, and urges every single person to at least try one. I personally did not find it comfy.

No products found.

Barefoot Investor how much to save?

The Barefoot investor advises you to save 15% of your pretax income in super, and then 10% to your post tax income in your smile account for medium term savings goals. He recommends directing 20% of your after tax salary to your Fire Extinguisher account which is used like a ‘savings booster’ once you have used it to pay off any debts.

What is the Barefoot Investor?

The Barefoot investor is the brand name given to Scott Pape’s financial advice business. It focuses on independent, no bs, honest and down to earth financial management advice for Aussies.

What super does the Barefoot Investor recommend?

The Barefoot investor recommends low fee, broadly diversified index fund super funds. Check out all of the barefoot investor super funds here.

What bank does the Barefoot Investor recommend?

The Barefoot investor recommends a number of fee free, online bank accounts. Check out all of the barefoot investor bank accounts here.

Where does the Barefoot Investor live?

The Barefoot Investor lives on his hobby farm with his wife and kids in Romsey, Victoria.

Conclusion

The Barefoot investor works, really well. If you are new to this, just follow the steps and trust the process. There’s a reason why it states it’s the ‘only money guide’ you’ll ever need. As you get more financially savvy, you can decide which bits to improve and which bits you can abandon all together to get you closer to financial freedom.

Grab yourself a copy from Amazon Here, listen to it through Audible or buy it from Australia’s local bookstore Booktopia

No products found.

Reference List:

- ‘Save for an emergency fund’, MoneySmart.gov. Accessed online at https://moneysmart.gov.au/saving/save-for-an-emergency-fund on Jan 31, 2023.

- https://www.mrmoneymustache.com/

- ‘Credit card debt top issue for Australians calling the National Debt Helpline’, Matilda Marozzi, ABC News. Published: Nov 16, 2022. Accessed online at https://www.abc.net.au/news/2022-11-16/credit-card-debt-top-concern-australians-national-debt-helpline/101645050 on Jan 31, 2023.

- ‘Tax & superannuation’, Fair Work Ombudsman. Accessed online at https://www.fairwork.gov.au/pay-and-wages/tax-and-superannuation on Jan 31, 2023.

- https://barefootinvestor.com/

- https://www.smartsalary.com.au/

- ‘Super contributions’, MoneySmart.gov.au. Accessed online at https://moneysmart.gov.au/grow-your-super/super-contributions on Jan 31, 2023.

- PODCAST – SUPERANNUATION AND FIRE’, Aussie Firebug. Accessed online at https://www.aussiefirebug.com/super-and-fire/ on Jan 31, 2023.

- ‘AUSTRALIAN FINANCIAL INDEPENDENCE CALCULATOR’, Aussie Firebug. Accessed online at https://www.aussiefirebug.com/australian-financial-independence-calculator/ on Jan 31, 2023.

- ‘Non-concessional contributions and contribution caps’, ATO. Accessed online at https://www.ato.gov.au/individuals/super/in-detail/growing-your-super/super-contributions—too-much-can-mean-extra-tax/?page=5 on Jan 31, 2023.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Great review of the book with some other valuable links too. Thank you

G’day Peta, My pleasure. Thanks for reading!

Good review of the book. Like the way you frame the steps here. I read it once and have adopt some of the steps. I plan to read it a second time and a third after that. Wish I had pick up the book and read it earlier