REST Super is Australia’s third-biggest superannuation fund by membership. REST Super was started for the benefit of retail workers, but is open for employees in other industries to join. Read on for my full REST Super review.

REST Super is an Australian superannuation fund started in 1988 that was set up for the benefit of workers in the retail sector. REST stands for the Retail Employees Superannuation Trust (REST) Super fund. REST Super is an industry super fund that benefits its members. The fund is also open to those outside the retail industry.

REST Super provides different investment options for workers in Australia. REST Super is Australia’s third biggest super fund by membership and offers advice and products in insurance and superannuation. Read on for more details about REST

The Good

- REST is Australian owned

- Established fund

- Third largest fund based on membership

- Low fees

- Recognised as a leader in incorporating environmental, social and governance principles into their investment options

- Variety of investment options on offer to match your risk tolerance

- Member benefits program

- Easy to monitor your super with an online portal and phone apps

- Website has tips, tools, resources and advice

- REST is an industry fund and their profits benefit members

The Bad

- Rating of 2.4/5 on Productreview.com.au, with 653 reviews

- Negative customer feedback regarding poor communication and difficulties with paperwork

- Customers providing feedback on difficulties with insurance payouts

- Customer reports on difficulty in accessing super in times of hardship

- Low customer ratings for transparency and customer service

Verdict: REST has low fees, is Australian owned and benefits members but there are a fair few negative reviews, and there are probably better super funds out there.

CaptainFI is not a Financial Advisor and the information below is factual review information, not financial advice. This website is reader-supported, which means we may be paid by advertising on the site, or when you visit links to partner or featured sites. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Introduction

REST Super is an Australian superannuation fund started in 1988 that was set up for the benefit of workers in the retail sector. REST stands for the Retail Employees Superannuation Trust (REST) Super fund. REST Super is an industry super fund that benefits its members. The fund is also open to those outside the retail industry.

REST Super provides different investment options for workers in Australia. REST Super is Australia’s third biggest super fund by membership and offers advice and products in insurance and superannuation.

It’s important for workers to partner with the right super fund. High super and insurance fees can erode your retirement savings, so it’s important to consider these and not just a fund’s yearly performance on returns. Getting the balance right can really help boost your retirement savings. You can listen to more about Superannuation in my podcast with Vince Scully HERE.

Is REST Super an industry super fund?

REST is a public offer industry super fund. This means workers outside the retail industry can invest in REST Super. REST Super is a fund that benefits its members, rather than shareholders. REST super doesn’t pay commissions to financial advisers. REST Super charges its members low fees and has a history of competitive returns, which can mean members save more money for their retirement.

Is REST Super an Australian company?

REST Super is an Australian company. It was started in 1988 as a super fund for those in the retail sector. Since then, it has opened its doors to those outside the retail sector.

Who owns REST Super?

The Retail Employees Superannuation Pty Ltd company runs REST Super2. The board has eight directors and four of those directors are nominated on behalf of associations representing employees and employers.

Is REST Super regulated by the ATO?

REST Super is regulated by the Australian Prudential Regulation Authority (APRA)3, but this is not the Australian Tax Office (ATO). APRA is an independent body that oversees superannuation, banking and insurance.

REST Super’s USI Number, ABN & SPIN. (supernumber.com.au)4

What are the super options5 through Rest Super?

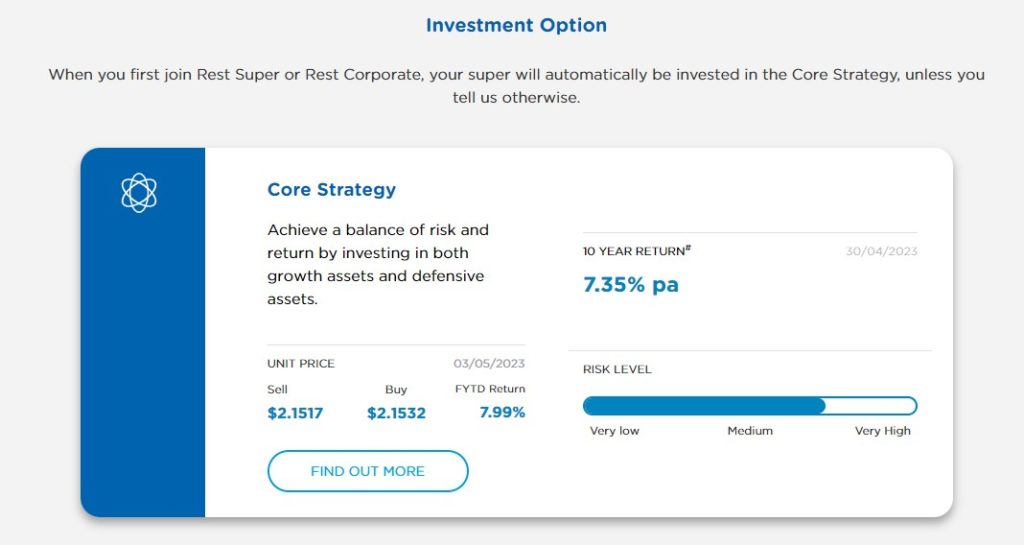

- Core Strategy – this is REST Super’s default MySuper fund. It invests in both growth and defensive assets

- Balanced – an option with approximately 50/50 split of growth and defensive assets

- Balanced Indexed – an indexed-based option with about 75% growth assets

- Capital Stable – a low risk option with 65.5% defensive assets

- Diversified – a similar option to Balanced Indexed, but not an indexed fund

- High Growth – aims for 85% growth assets for higher returns

- Sustainable growth – similar to Balanced Indexed, but not an indexed fund. Assets take into account social and environmental factors.

In 2022, REST Super was awarded6 the (Environment, Social, Governance) ESG Leader rating by Rainmaker Information for implementing ESG principles in investment, with decent investment performance.

REST Super | Performance, features and fees | Finder.com.au7

“For many of us, super is one of the biggest investments we will make. How you choose to invest your super savings could make a difference to how much money you could have in the future. Here at Rest, we have 15 different investment options to choose from. You can choose from Core Strategy, Structured Options, Member Tailored Options. Giving you more control over how your money is invested.”

rest.com.au/member/investments/super-options5

What are REST Super’s fees?

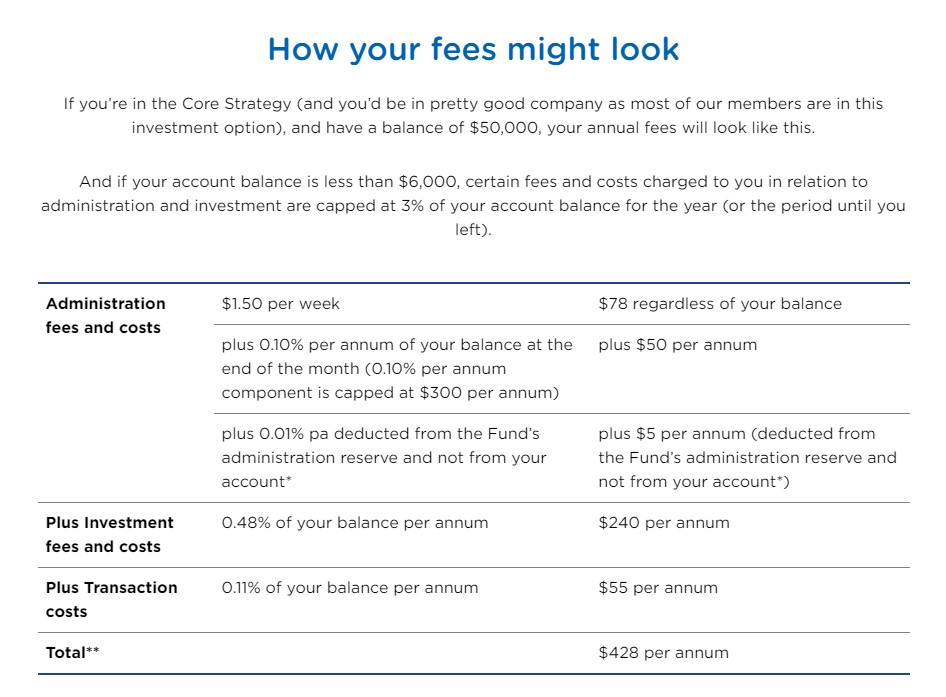

REST Super charges a number of fees8, as do other super funds. If you have less than $6000 in your account, fees are capped a 3%. The following fees are for a balance of $50 000:

· Administration fees – a minimum of $1.50 per week ($78 per year no matter what your balance), an asset-based admin fee of 0.10% of the account balance at about $50, capped at $300 per year. Plus 0.01% taken from the admin reserves of the Fund, not your account, of about $5 per year.

· Investment fees and costs – 0.48% of your balance each year, or $240.

· Transaction costs – 0.11% of about $55.

· Advice fee – for simple personal advice over the phone, advice is at no extra cost. For more complex advice, your adviser will let you know the cost upfront.

·!– /wp:paragraph –>

So, at a minimum for the MySuper Balanced Fund with a balance of $50 000, you would be charged about $428, deducted from your fund. This is made up of $78 admin costs (irrespective of the balance), plus $50 asset-based admin fee (0.01% of $50 000), plus $240 for investment fees and costs and $55 in transaction costs.

In comparing REST Super fees to the Hostplus low fee Indexed Balanced fund mentioned by Barefoot Investor, REST Super is cheaper.

How does REST Super perform?

When it comes to REST Super’s performance9, the following will look at REST Super’s MySuper compliance option, Core Strategy, with a super account balance of $50 000. Core Strategy aims for a return of CPI plus 3%. This investment option is used for this example as it’s easiest to compare with the MySuper offering of other funds.

Like most funds over the past 12 months, REST Super Core Strategy has lost ground with a 3.88% fall. However, their 3 year performance shows a 4.09% increase. Over 10 years there has been a 7.47% increase.

Just remember, past performance is not always a reliable indicator of future performance.

REST Super insurance policies

REST Super has the usual range of insurance policies offered by a super fund. Your premiums come out of your super contributions and it can be tax effective to pay for insurance this way. When choosing a super fund, it’s important to do your homework on the cost of insurance because high fees can really eat into what is left over to invest and may significantly erode your retirement savings.

While you may start off with low premiums, there are a number of things that can cause your insurance premiums to increase over time. This includes the amount of cover you have, your line of work and how old you are. You also have to be eligible for insurance through REST Super. This depends on whether you are an Australian resident, the type of work you do and your age. Your insurance may also be cancelled if you are out of work for a certain length of time, or there is not enough money in your super account to pay the premium.

The following REST Super insurance premiums are for a male aged 30 with Income Protection Insurance for a white collar job with a uni qualification and a gross income of $100 000. The summary also includes $500 000 Total and Permanent Disability (TPD) and $500 000 Death Cover.

REST Super offers the following insurance policies:

· Death cover, which includes Terminal Illness cover: Premium example – about $260 per year for $500 000 cover

· TPD – Premium example – about $150 per year for $500 000 cover

· Income Protection cover – if you temporarily can’t work, you can be paid up to 75% of your income for a set period of time. For example – for a 2 month wait and 2 years of payments – not an option in the REST calculator. 2 months wait for 5 years of payments – about $140 per year.

TAL Calculator – Calculators | Rest Super10

How does REST Super invest my super?

The investment options invest in the following asset types:

· Bonds

· Property

· Australian shares

· Overseas shares

· Cash

The mix of defensive and growth assets depends on which investment option you choose, for example Core Strategy or High Growth.

Advantages of Rest Super

- Australian owned

- Established fund

- Third largest fund based on membership

- Low fees

- Recognised as a leader in incorporating environmental, social and governance principles into their investment options

- Variety of investment options on offer to match your risk tolerance

- Member benefits program

- Easy to monitor your super with an online portal and phone apps

- Website has tips, tools, resources and advice

- REST is an industry fund and their profits benefit members

Disadvantages of Rest Super

- Rating of 2.4/5 on Productreview.com.au11, with 653 reviews

- Negative customer feedback regarding poor communication and difficulties with paperwork

- Customers providing feedback on difficulties with insurance payouts

- Customer reports on difficulty in accessing super in times of hardship

- Low customer ratings for transparency and customer service

FAQs about Rest Super:

Where does REST rank in super funds?

REST Super ranks at 13 out of 161 super funds in Australian in terms of assets with about $67 billion under management. REST Super is the third largest fund in Australia based on membership numbers.

Can anyone use Rest super?

REST Super is a public offer industry fund. It was established for retail workers, but you don’t have to be a retail worker to join.

Is Rest an ethical super fund?

In 2022, REST Super was given the ESG Leader rating by Rainmaker Information. This acknowledged that REST Super applies ESG principles in investment. Also, REST Super’s Sustained Growth option is positioned for ethical investment.

The REST Sustainable Growth option invests in companies like renewable energy, that contribute positively towards society and the environment. It doesn’t invest in companies like those producing fossil fuels, which may be harmful to the environment.

This gives members an option to build their retirement nest egg without compromising the environment. However, many super funds offer this sort of investment option, so ethical super is not the exclusive domain of REST Super.

“REST Super is one of the 13 super funds that has committed to achieving net zero absolute carbon emissions in their investment portfolios by 2050, in alignment with the Paris Agreement.”

superguide.com.au/super-funds-guide/rest-super-retail-employees-superannuation-trust1

Does REST charge an exit fee?

REST Super does not charge an exit fee to move all or part of your super out of the fund. However, keep in mind that tax may be deducted.

Tax and super – Moneysmart.gov.au12

How many members does REST Super have?

There are about 1.9 million members1 with a REST account which makes it Australia’s third largest super fund based on membership.

Conclusion

REST Super is Australia’s third biggest super fund based on its membership numbers and provides super and insurance products to workers in a variety of industries in Australia, not just retail.

REST Super is recognised as a leader when it comes to including environmental, social and governance principles in its investment options, while generating reasonable returns over the past 10 years.

REST Super is a large organisation, and some customer feedback highlights areas for improvement such as communication and ease of insurance payouts. However, REST Super’s past performance, low super fees and low insurance premiums make it worth comparing alongside Australian Super and the Hostplus Index Balanced option recommended by BFI, as a partner for saving for retirement.

You can also take a look at my detailed guide to Superannuation in Australia as well as my other Super reviews:

Check out reviews of the following super funds;

- HostPlus super

- UniSuper Review

- REST Super review

- ART Super review – Australian Retirement Trust

- Australian Super Review

- MLC Superannuation Review

- Barefoot Investor Superannuation funds

- ANZ Smart Choice Super review

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.