CaptainFIs financial and personal update for the third quarter of 2024

Captain FI is not a financial advisor, does not hold an AFSL and this article is not financial advice. This website is reader-supported, which means we may be paid when you visit links to partner or featured sites, or by advertising on the site. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer

Captain FI’s personal update

Probably the biggest news is that Miss FI and I got married (so thats now Mrs. FI!), and that we are expecting our first baby in the new year!

The wedding

We had a beautiful ceremony in the back paddock, under the shade of our oldest macadamia tree, surrounded by lots of close friends and family who travelled from all over Australia and overseas to share the day with us. We were pleasantly surprised by how well everything went and that we had the perfect spring weather here in South East Queensland, with thunderstorms that held off until later that evening.

It was a morning ceremony, followed by a pretty relaxed barbecue style reception with games, swimming, singing and dancing and a bonfire.

We hired chairs, lawn games and wedding decorations, and then bought a lot of umbrellas for the ceremony for guests (QLD sun can be harsh!), four large park benches, catering chaffing dishes for the food and then hit up the op shops for few other bits and pieces like cups, glasses, crockery, cutlery, vases and centre pieces. We also borrowed some large marquees, sound system and camping fridges from friends just to get a bit more shade and to have cold drinks outside for the reception BBQ.

We also hired a barista, bartender and a babysitter for the day to help for the day, which kept everything running smoothly (especially the baby sitter for everyone’s kids!). One of my groomsmen brought some of the homebrew Vodka that he makes, and the bar tenders whipped it up into espresso martinis for everyone which was pretty cool.

From our perspective as the people getting married, the day just seemed to fly past. It started with us groomsmen getting ready at 9am in the movie room listening to beats from our old uni days and cracking open a rather special single malt to steady the nerves, but then before I knew it it was 11pm (well past my bed time!) and I was sitting around a bonfire in the rain, and it was time to go in for a shower and head to bed.

There was lots of work in preparation for the wedding, which included;

- Finishing off furnishing the home and all of the guest rooms to accommodate all of our guests (so.much.linen!!!!)

- Major gardening and landscaping works including bringing in over 70 tonnes (yes, tonnes) of mulch and wood chip to finish garden beds and edging

- 4 x large Lawn renovations (not in any rush to do that again – seriously just have a look on youtube search ‘lawn renovation’ and you will see how much time, effort and money is involved!) – followed by mowing, mowing and more mowing

- A lot of planting – flowers, flowers and more flowers!

- Shopping and meal preparation for guests and for the day of the wedding

- What felt like seven hundred airport runs 🤣

- Harvesting honey for the wedding gifts, and making the beeswax wraps to go with them.

It was very busy in the week leading up to, and then winding down from the wedding. Because people had travelled from so far and we had the space, we invited our interstate and overseas guests to stay with us – I think we had 21 guests the night before, and then 23 on the night of the wedding, which was AWESOME. We were blown away by how thoughtful everyone was and how much everyone pitched in to help get everything set up and ready, and then with the help to pack up.

The day before the wedding I began smoking up 15kg of beef brisket in my trusty little smoker, which was ready to serve for lunch after 24 hours of slow cooking – it was definitely a crowd pleaser, but I think my mother in law (who is a retired chef) took the crowd favourite with her Italian Saltimbocca, as well as a host of other Phillipino classics.

Overall, we are super glad we had our wedding at home. Firstly because we love the space, and it made it so much more personal and special. Now we have incredible memories of getting married under the old macadamia tree, and sharing our first dance on our terraced lawn (which I painstakingly renovated).

We also got to host everyone which meant we got to spend a lot more time together with everyone in the week leading up to and following the wedding, which was bloody great – especially for those mates who I haven’t seen for ages. I mean, compare that to previous weddings I have attended where everyone has stayed at hotels, and then only gets to see the bride and groom at the ceremony and during speeches at the reception, and then maybe only gets to briefly chat or maybe share a drink or two with them later in the night… I thought this way was heaps better.

On the downside, yes a few things got broken around the house and on the farm (ehhem some of the gates were locked for a reason!), nearly running out of water was stressful, and it was probably a lot more work than outsourcing at a venue, but that trade off was definitely worth it in my mind for the time we got to spend with our loved ones.

When we initially googled how much do weddings cost, as you could imagine the answer is pretty variable. A figure that gets thrown around here in Australia a lot is around $30,000 to $40,000. When we were doing some initial research in our planning phase we got some quotes for venues, and just the venue fees alone were coming back at around $10,000 to $15,000. When you factor in the additional minimum spends on catering (around $100 to $150 per head), drinks packages ($50+ per head) and then all the little things that add up like decorations, flowers, outfits, transport, DJ then you can see it easily gets into this range.

All up, I think we spent around $18,000 on the wedding and we had about 60 guests on the day. This was roughly

- $3,000 on food / groceries (which also included about 150 meals for house guests before and after the wedding)

- $1,500 on drinks and alcohol – a lot of which was left over! (I guess we are hosting Christmas lunch)

- $3,500 on photographers for photos / videos / drone

- $2000 on staff – Bartender, Barista, Babysitter (for creche), and our celebrant (who is our neighbour!)

- $2000 on furniture (which we wanted/needed for the house anyway!) – extra fridge and coffee machine, bunk beds, wooden park benches etc

- $4400 on landscaping and lawn renovation supplies

- $300 on on our outfits for the day

- $250 for lawn game hire

- $1,100 for cleaners who did a deep clean of the house both before and after the wedding.

- $500 on misc stuff / errands on the day

When you consider that a lot of our costs was landscaping to improve the gardens for the wedding, plus a bunch of furniture (like a second fridge, beds, linen etc) which we get to keep, plus all the leftover food and alcohol, it probably only *really* cost us closer to 10 grand for the actual wedding itself which was mostly things like staff, cleaners and photographers.

The Baby

We are super excited to be parents in the new year and have been doing a lot of reading and preparation. Our youtube video recommendations are basically all parenting videos now! We have decided to go through the public system, and we plan on hiring a Doula to help Mrs FI and I through the challenging period of birth and the first few weeks after. My mother in law will also most likely come and move in with us for a while to help out, which is a real blessing.

Due to fertility issues, this is something we had kept pretty quiet, but that we announced at our Wedding to our close friends and family.

Its pretty fucking awesome to not have to worry about money and working and applying for leave and stressing about centrelink and maternity/paternity leave etc – I am feeling super grateful for our position and all the good decisions and privileges that has led into this lifestyle. I really think this has let us relax a lot which has massively helped with my feelings of anxiety and certainly with Mrs FI also, which is good news for any pregnancy.

I’m pretty stoaked with my research into family planning and the cost of kids, because its lined up pretty well so far (accounting for a bit of inflation I guess haha!)

Thankfully everything is going beautifully, as well as could be. We have had a couple of ultrasounds now and all the tests and scans show our baby is healthy and developing well. Mrs FI has had a challenging first trimester with nausea and extreme lethargy and nausea, but it settled down and she really enjoyinged the second trimester (especially eating ALL the foods haha), and is getting really big now as we get closer to the due date. She is now in the nesting phase and its been really cute to see her stockpiling and organising all our supplies and gifts.

Since we moved up the coast we have made some awesome new mates here, and what a coincidence but two of these couples are also expecting and there is only a few weeks gap between each our due dates! We have also made some more new friends that are new parents, and to be honest most of our friends here (including two of my best mates) have young kids too, so its great to have a tight community of close friends with young families that we can all support each other. We have already been practicing with having hordes of kids over here whenever friends come over for barbecues or pool parties – and aside from the chaos and (at times overstimulation) it is generally pretty fun. Kids are awesome.

We haven’t purchased that much baby gear aside from our Snoo bassinet, the owlet sock, baby cam, bottle steriliser and a few items from the op shop. Our generous friends and family have showered us with baby gifts, and there are only one or two things we still want to get. Fortunately, we can easily exchange the duplicate gifts we received at Baby Bunting for those remaining items without spending any extra money. All up its been about $2,000 spend, but I think we were gifted or inherited at least a thousand dollars worth of stuff (baby clothes, equipment etc).

We have a couple months left of the calm before the storm – so we are trying to just ready everything, smash out some house projects while we have time and keep up on the research / prep as well as attend the parenting classes.

The Bucks

Before I got hitched, my mates organised an impromptu bucks night which I flew out for. It was great to catch up with some of the lads who I hadn’t seen for ages – some from our Uni days, or who live interstate, and a mate who flew over from the USA. We did whiskey tastings, had some nice beers, went to some nice restaurants had a go hurling some axes down range. Mostly it was a lot of shit talking and catching up nostalgia, which was great. Really what I needed.

It really got me thinking, it was too long since seeing a lot of these guys, so we want to try and organise a yearly reunion / trip where we can all catch up. Just in case I can’t travel much after the baby is here, I bought some of the nice whiskeys we tried and have them tucked away on a shelf for future ‘At home whiskey tastings’.

The Boat…

Since I am retired and living in paradise, I figured it was high time I bought a boat! I actually kinda made the final D when I was recently away on my Bucks weekend trip with the boys – there was a fair bit of heckling involved as well as some pretty top notch whiskies which could have have influenced my decision making.

So when I got back, I got a Skippers ticket (that has been on the ‘to-do’ list for decades!), bought a small boat and have taken up the hobby of spending money on petrol, fishing tackle and equipment – I think you actually have to catch fish before you can say you have “taken up fishing” – Despite my best efforts (and 4 trips…) haven’t managed to land a fish thats legal size just yet, which is a bit sad – but you know what they say – “A bad days fishing sure as hell beats a good day at work!”

Its actually a bloody awesome little craft and we’ve had it ripping along at 45km/h on the river two up with full tanks and equipment, thanks to the decent sized engine on the back. Having the power means this thing gets up on the plane and fangs along, so transit times to ‘the secret spots’ is much shorter (if you know any secret spots between the Gold Coast and Harvey bay, let me know haha!).

So far the ‘Hobby’ has cost me around $14,000 for the course, licence, boat, trailer, rego, some basic maintenance, and equipment (safety gear i.e. flares, a couple of rods, tackle, crab pots etc).

I am looking forward to learning to fish a little better and be able to bring home a catch for the family, but also to spend some quality time with mates on the water.

The seller was a bit of a pro fisho, and had really decked it out well. I decided to add a shade canopy to it (because I friggen hate sunburn) and a few other small bits and bobs.

Initially I wanted to spend only a few thousand on a boat, but I quickly realised I would just be buying someone else’s problem at around that price. It is a lot more relaxing than flying a plane and a hell of a lot cheaper, so in the end I think its worth paying a little more for reliability, capability and peace of mind.

In the future (5-10 years) when I’m a bit more of a salty sea dog (and have a few more pennies in the bank) I might look at upgrading to something like a 6m alu half-cab with 100hp for going offshore. But I definitely want to at least catch a few fish in the river / estuaries off this tinny first!

The property

The garden is looking great, loads of spring blossoms and the veggie beds are growing very well. We have been picking and eating the fast cropping things that are already ready – Beans, Peas, Blueberries, Mulberries, Tomatoes, Radish, Salad greens, pepino melons and a few other bits and bobs. It is very fun to wander around eating things on the property.

The warmer weather means that everthing is growing well, including the grass. I have upgraded to a larger ride on mower and it seems to be up to the task.

It is really hard to explain this coincidence, but the day before our wedding, we had two very significant flowers bloom.

The first is our Purple Agapanthus plants. Personally, I never really cared for Agapanthus – however my Dear mum loved these and always planted them in her gardens. She especially liked the purple ones. So to come out for my morning walk and see them blooming, with a butterfly feeding on one was very special. Butterflies were always very special to my Mum, and she always joked and she said she would come back as a Butterfly (because… no one suspects the butterfly!). So everytime I see one, it reminds me of her and I feel close to her. I actually did not plant this agapanthus, it came with the property, so it was a nice surprise to find.

The second was our large Jasmine bush, which I didn’t even know was there (as it was originally hidden behind a viney weed which I had to rip out). Well it burst into a gorgeous display of flowers and filled the entire backyard and paddock with the intoxicating, intense, sweet aroma of Jasmine flowers. About a year ago, I lost a close friend and ex partner, who was named after this flower. And she was very much a ‘larger than life’ type personality that was just insanely beautiful, always the centre of attention, and always smelled amazing. So for it to bloom the day before the wedding was pretty powerful for me. I also didn’t plant this, it came with the property, which was again a pleasant, but emotional surprise.

Maybe I am seeing patterns that don’t exist, and of course flowers bloom in spring, but anyway, it felt like in spirit that these two very significant people from my life were able to attend the wedding and were making their presence felt.

On the day, I also wore a pink rose, which I had planted several months ago hoping for a blossom to wear on the day, as this was another favourite flower of my Mum.

Health

I feel like my health has massively improved since we settled in our acreage. My mindset is better, and I am looking forward to getting out in the garden and orchards and each day and working the bees. Physically, I am feeling good, but I am often overdoing it as I think my ambition exceeds my ability, and as a result I seem to end up on the couch recovering with lots of ‘quiet days’. In time I am sure I will get the balance right.

Actually as I type this, I am wearing finger braces because I’ve given myself trigger finger in both hands from gardening too much (trigger finger sucks, you cant uncurl your hands properly after making a fist!). Luckily my wife is very handy for diagnosis and rehab directions. I did go to the GP, but they weren’t super helpful and just told me to talk to my physio about it and take NSAIDs for the pain (which I do take as needed).

I did spend pretty much a whole day working on the websites, and after having a pretty decent break from the computer this was a bit of a shock to the system and I ended up straining my neck which has taken about a week to recover from, including a couple trips to the physio and one to a local massage place. I guess getting older just need to be mindful about consistency – I have decided to limit myself to no more than 2 hours a day on the computer and am prioritising getting myself an ergonomic sit / stand desk again, and a large triple monitor set up.

I have set up our home gym but if I am honest, I barely use it at all since I am always tired from mowing, weeding, pruning, mulching, planting, watering etc 😅 I mean I knew I was up for some maintenance but perhaps I underestimated the load!

Now that the weather is warming up a bit and the pool is warmer, we have taken to morning swims, which has been great for my rehab and for my wife being pregnant to get some gentle exercise. It is very relaxing and I will have to remember to wear swimmers in the pool once we start renting out accommodation 😅

The boat is part of the mental health plan, too, with the aim to spend more time with friends and on recreation rather than on ‘jobs’. In some ways its a bit of my inner child coming out too, as I really always wanted to go fishing with my old man but he never bothered to take me. So this is kind of healing old wounds. I want to be eventually be able to take my kids out and spend some quality time with them on the water. So its something I actually look forward to going out and doing, even though it is pretty exhausting and I don’t seem to catch any fish 🤣

I have also tried my hand at a bit of “carpentry” and made four nice little wooden benches and coffee tables for the house, which did make me feel rather accomplished as I never really excelled at woodwork or shop class at school. My grandad was an academic researcher and a very skilled woodworker as his hobby – so making these reminded me of time in his workshop building things as a kid. I purchased the Camphor laurel slabs from a local sawmill and then planed off most of the bark from the edges, sanded the edges and face, screwed on the legs which I bought already made and then varnished them. Came out alright I reckon!

Captain FI podcasts

I am feeling a bit slack as I have not recorded any new podcast updates this quarter, but I will as soon as I get my studio set up!

I plan to record a ‘life update’ podcast and I am very overdue to jump on as a guest on a few other podcasts I have been invited on too – PS other hosts if you are reading this thank you for being so patient whilst we get established in our new home!

You can still check out the previous episodes of the Financial Independence Podcast on Spotify or now they have been uploaded to the CaptainFI YouTube channel!

New Captain FI blog articles

As I mentioned, I have been slowing down with blogging while we get settled into the new place and adjust to our new life – but I did publish these articles

- Wednesday, September 11 | Beem App Review; How does this bill splitting app work?

- Wednesday, August 7 | Affiliate Marketing Courses: Making Sense of Affiliate Marketing vs eBusiness Institute

- Monday, July 1 | Superannuation in Australia

- Thursday, May 9 | Barefoot Investor Health Insurance

- Wednesday, April 10 | Best Money and Budgeting Apps in 2024

Captain FI’s Spending

In my last update (Q2 2024 net wealth update) I mentioned that last years (2023) expenditure was approximately $46,000 – which was pretty reasonable for my second year of early retirement – renting a modest 2 bedroom home in Adelaide with my girlfriend, with an international trip to SE Asia and a couple of domestic holidays throughout the year. We didn’t really need to make any major life upgrades or spending, and we lived very comfortably not tracking our grocery bills, and ate out multiple times a week.

My wife (then girlfriend) was working and contributed a 1/3rd share to the bills. So all in all, my $46,000 (from my bank accounts) was pretty darn good value for what I got lifestyle wise. If you combined both of our spending, then it would be an approximately $69,000 total household spend – for two adults that is pretty bloody insane value for the lifestyle we had.

As a bit of a side track – if you do the maths on this figure, that means we would have had to earn $38,500 each pretax to fund this lifestyle. This could come either from a ~$2M index fund portfolio (in a tax structure that can distribute), a $1M portfolio each, or by each of us working around 30 hours a week at a minimum wage job (8am to 2:30pm with half an hours lunch break, or a full 8 hr day for 4 days a week). Either way, we had an awesome lifestyle (some might even say excessive with a lot of overseas and domestic travel, and eating out twice a week) and it is very much achievable for a two person household with no kids. Especially if you earn above minimum wage. I think people just like complaining about how expensive things are (myself included…).

Due to the stress of moving and setting up the house, my wife’s rough first trimester during pregnancy, and then the wedding, we decided it was best for her not to worry about looking for full-time work just yet, or start the new NDIS contracting business until our baby is a bit older. For the same reasons, we had also been spending a bit more on convenience and on stuff to set the house up to make our lives a bit easier, but we plan to try and not be too outrageous with any big purchases for the rest of the year 😅 Although there has been some massive lifestyle inflation going on.

For now, she is lining up some casual half-day shifts a few times a week to keep her registration compliance stuff up to date (this brings her about $1000 a week which she splits into her super, index funds and spending money as she see’s fit) and her household role / contribution is in the form of growing our baby and then coparenting. She is unsure if she will go back to work after the bub as we will be trying for #2 pretty much straight away (due to fertility issues)

Anyway, back to this years spending – I calculated that in the first half of 2024 I had almost managed to exceed our prior years total combined spending figure, with a ball-shatteringly expensive start to the year – just over $65,000. To be clear, this is my responsibility as it’s my role to fund our joint spending account. My wife does have her own accounts / sources of income (as do I) but thats for her investing or private spending money.

To be fair, we do have a lot more expenses now that on acreage, and the eye-watering mortgage is one of the main culprits (almost 3 times our previous rent). Expensive things I had splurged on in the first half of the year included;

- Over 300 fruit trees

- Four established beehives and associated equipment

- Home CCTV system

- A large, beautiful, hardwood dining table with live edges

- 85 Inch Sony Bravia flat screen and paid for wall mounting

- Bose home movie sound system

- High speed internet, router and Wifi extenders for the property

- Ride on mower for the house lawns and paddocks

- Tools and machinery

With a further three months gone by, there has been a few more purchases….

- Over

300400 fruit trees - Beehives – investment in updating/refurbishing older equipment, replenishing consumable stock and upgrading to a larger, electric centrifuge honey extractor

Ride on mower for the house lawns and paddocksA Larger, faster, more capable ride on mower for the lawns, orchard and paddocks- A Scotty Bonnar 45 cylinder mower for the terraced lawns (yep – I’m going for that ‘golf course green’ look at the moment)

- *More* Tools and equipment

- Additional furniture and appliances for the house – a second fridge, coffee machine and TV, couches, setting up guest bedrooms etc

- Ziggler and brown gas barbecue, table and chairs, outdoor lounges and umbrellas for the pool area

- Wedding costs (including some landscaping)

- The Fishing boat, trailer, rods, tackle and assorted accouterments

- A second hand Snoo baby bassinet (Cheers to the Aussie Firebug for the recommendation, mate!), Owlet baby monitor (new), baby cameras, bottle steriliser, and various other baby paraphernalia to the tune of around $2,000 – strangely enough, this was the cost I had ‘guesstimated’ in 2022 in my research article into family planning and the cost of kids – obviously high inflation between then and now has pushed prices of new stuff up, but the second hand market is still very reasonably priced. To be fair we were also gifted about a thousand dollars worth of baby stuff too (clothes, swaddles, nappies etc).

Thankfully I have been able to ‘recoup’ some of our previous spending to put towards new purchases by selling some of the things we have upgraded – such as the old ride-on mower, as well as by selling a few things we have produced – honey, a couple of beehives, and some rare and large plants from the property. When I do this, I mentally put the money aside and consider it ‘guilt-free’ money for buying something else I need later,.

For example, we sold our ride-on mower for $2000, and then I bought a bigger one for $2500, so I only feel like I have spent $500, not $2500.

We also usually only buy things second-hand and wait until we can find something in good condition at a good price, so we don’t buy things from shops much anymore.

Anyway, its a bit shocking when I tally up all my bank statements and diary entries, as this brings my 2024 running spend up to approximately $118,000, with a projected spend for the rest of the year of $136,000, making it a pretty spendy year indeed (almost three times my 2023 spend figure!).

It is also worth mentioning that my wife has also spent some of her money this year too – she has contributed approximately $10,000 which she had in her savings towards things like the wedding, house-hold stuff and general cost of living expenses like groceries or eating out.

When we combine our spending, its a projected $146,000 for 2024 – just a tad over double our combined household spending for 2023. Which checks out, because we have just moved and have had a massive lifestyle upgrade.

If I just pay the bare minimum to the mortgage and household expenses (insurance, rates, electricity, internet, fuel, maintenance, groceries etc) it works out to be around $95,000 per year cost of living – plus whatever we end up needing to spend on fertility for subsequent pregnancies, and childcare costs if we decide to do a couple days a week.

2025 and beyond are also shaping up to potentially be somewhat expensive as we have a few major projects planned over the next few years…

- Raising the children – Fertility, Childcare, enrichment etc

- Buying a second car – we almost bought a cheaper 2010 model, but we think we may actually splurge on a 2020 for better features!

- Extra water tanks and tank pads put in

- Bushfire safety sprinkler system for the house

- New water bore to be drilled (plus pump and plumbing…)

- Sprinkler irrigation system for orchard and paddock

- Sheep fencing around orchard

- Hail / fruit fly netting for orchard

- Retaining wall, slab and shed for boat and trailer

Captain FI’s Investments

I don’t calculate a Net Wealth or Savings Rate Figure each month anymore, but I do try to keep a rough track of everything for these quarterly updates

My investments (outside super) are split across the following areas;

The ‘FIRE’ Portfolio of Index ETFs- My primary place of residence – hobby farm / acreage in Queensland.

- Aussie Investment Property – Residential duplex in New South Wales

- My company – which runs a portfolio of content marketing websites

- Cash (mortgage offset accounts)

- A small Angel Investment in the investing platform Pearler

NB – A while ago I ended up divesting in various things such as RoboAdvisors, Micro investing funds, Managed funds, Metals/resources, and a few other speculative investments or experiments I had invested in, in order to simplify my finances. I had racked up a complex mix of investments as I wanted to try out and review various investing services but this became unmanageable in the end and I needed to simplify my life.

In December 2023 I also sold off the ‘FIRE’ Portfolio (mix of Index ETFs) to fund my dream acreage purchase, but I will be rebuilding this to build passive income through debt recycling over the next 10 years to reduce our families reliance on my business and my wife’s income.

The ‘FIRE’ Portfolio (Exchange Traded Index Funds)

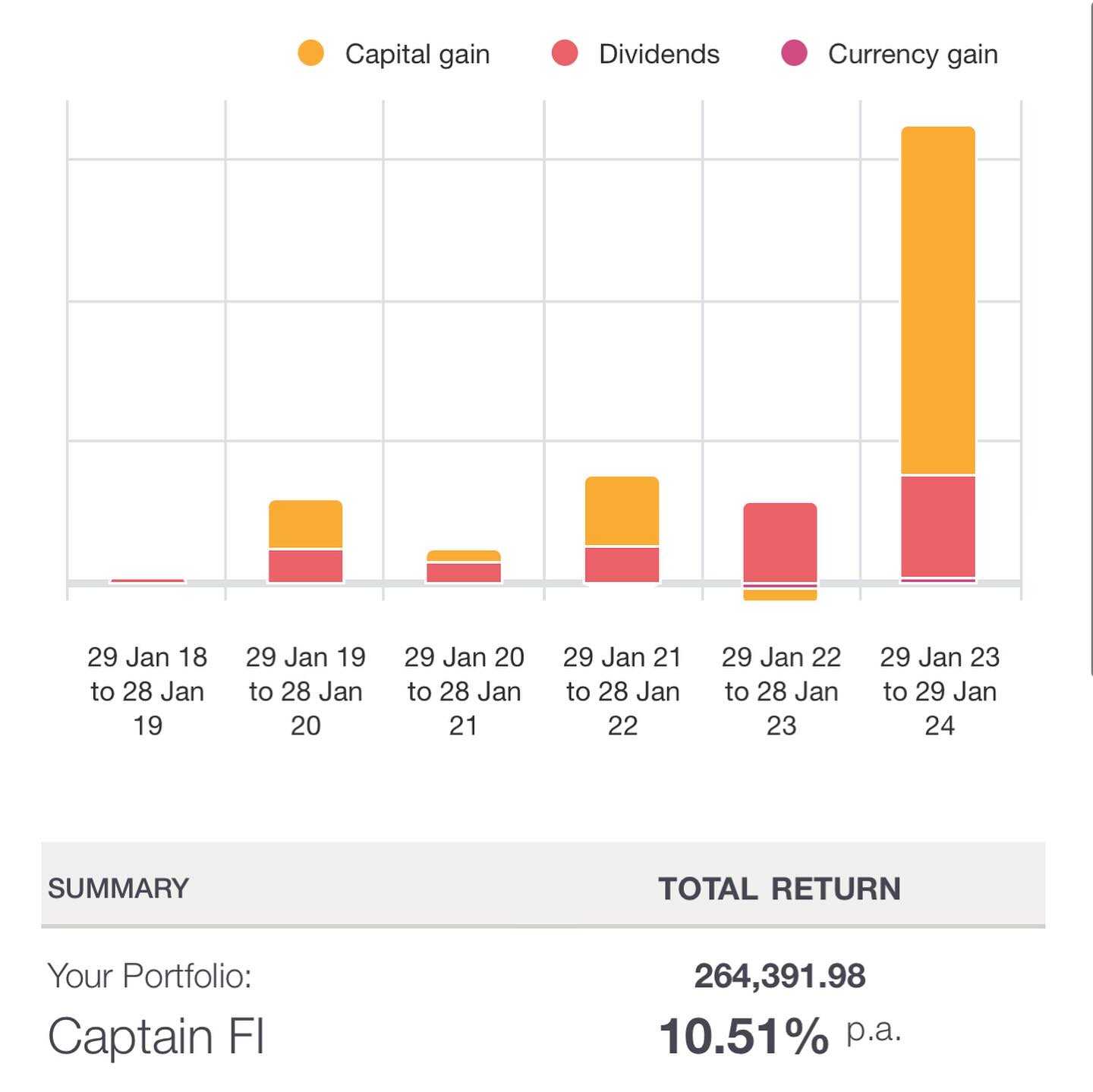

As you may have known, my ‘Financial Independence Retire Early’ ETF Portfolio was a simple, passive share portfolio split between three parcels of low-fee, index-tracking Exchanged Traded Index Funds (ETFs) to achieve global diversification.

I began switching to this passive index approach to investing in 2018, firstly by adding new contributions, and then over time by divesting in other assets (individual shares, managed funds, LICs etc) and rolling the investments over to it.

- I tracked my share portfolio using Sharesight, which means my portfolio accounting and tax reports are completely automated.

This was sold in December 2023 to fund the acquisition of a hobby farm, after six years of passive index fund investing. Going forward I will be first building up cash again for an emergency fund in the mortgage offset, and then when we are ready to invest I will be redrawing from the mortgage to invest (debt recycling) using something like the Betashares DHHF ETF which is an ‘all-in-one’ ETF in order to keep things simple.

Cashing in the chips with a total return of 10.51% was a good feeling. I know the market has continued to grow in the six months since we have sold, but you know what, I achieved what I set out to do which was to become financially independent and retire early from the rat race / grind, and buy my dream acreage to start hobby farming and raise a family. I will get some skin back in the game with the share market soon!

Captain FI’s PPR (acreage)

To keep things simple, I just value it as a residence only and use an online valuation tool. The current PropTrack automated online valuation estimate is $2.436M, which is up $61,000 from the last time I checked it for the Q2 2024 net wealth update, but still $64,000 less than I paid for the property.

As I said last time we probably did overpay for the property a bit, but the Aus property ponzi scheme does seem to only go up, so it shouldn’t really matter, right? LOL.

I still owe $775K on the PPR mortgage, for a net equity position of $1.661M, with $285K in the offset for a net mortgage of $490k (6.39%) of which I pay $1250 weekly repayments.

Opting to pay $1250 weekly, instead of $5000 monthly repayments shortens our mortgage by SIX years – from 29 years remaining to only 23 years. This is because I am making one whole extra monthly repayment per year ($65,000 vice $60,000 per year). Additionally, by paying weekly rather than monthly I am also paying less accumulated interest as I am paying chunks of the loan off sooner rather than waiting till the end of the month to pay off those chunks – so there is less interest due.

Debt recycling plans

I plan to use the money I currently have in my offset account to pay down the loan, and then immediately re-draw it as a new loan soley to be used for investing (this process is called debt recycling). I will be leaving a healthy emergency fund in the offset account though, for peace of mind (which I will grow to 12 months)

Despite my love for the VTS/A200/VEU split, I think I will probably just use something like the Betashares DHHF or the Vanguard VDHG ETFs as the investment vehicle for simplicity sake.

Assuming I kept the mortgage for the full remaining 23 year term, if the investments grew at the average long term rate of 10%, inflation remains within the target range of 2-3%, and assuming I make ZERO further debt recycling contributions, they would be valued at $2.17M, which would be approximately the equiavalent worth (buying power) of $1.228M in todays (2024) dollars, adjusted for inflation (assuming a 2.5% inflation rate).

Which I think is pretty awesome share portfolio to have alongside a paid off home – that portfolio alone could reasonably kick off just shy of $50K a year income (in 2024 dollars purchasing power) which is probably enough for us to live off with a paid off home, and especially when you add in my superannuation annuity income, any income from websites, or from my wife or her investments, and that our children would be adults that should either have moved out or be working part time whilst studying at uni and paying board.

In practice, there would be a cross-over point where the remaining mortgage balance (both tax and non-tax deductible portions which are being paid down) would be the same as the dollar value of the growing share portfolio, and one could potentially just sell the shares (keeping in mind any tax due on CGT) if they ever needed to wipe out the remaining property debt. Good for the sleep at night factor!

I had a bit of a play around on https://debtrecyclingcalculator.com and assuming I debt recycled the tax savings (around $3500 a year?) once a year, and comparing that to my mortgage amortisation documents (where I see how the loan gets paid down over time) then it seemed like that crossover equal point for me was actually around the 11.5 year mark – which is pretty bloody exciting – and that doesn’t even include any additional debt recycling contributions I could potentially make along the way too which would speed it up further. Debt recycling is not as attractive for me now that I am not a high income earner as it used to be, and now interest rates are higher, but it still looks worth it.

Having said that, even just keeping that cash in the mortgage offset account massively speeds up the mortgage being paid off because it offsets a big chunk of interest – and due to the compounding interest effect, having that money in the offset early on helps a lot. Using the ASIC moneysmart calculator shows that just keeping the money I was going to debt recycle in the offset account actually reduces the mortgage life down to 12.5 years – a 10.5 year reduction, and only one year longer than the debt recycling option, but with none of the market risk. Its actually a pretty hard decision to make, which is probably why I have been dragging my feet on executing…

Considering I also keep my 12 month emergency fund in the mortgage offset, in both cases (debt recycling or just pure offset) this actually speeds up the mortgage paydown by a further 2 years. So it is definitely achievable to pay this PPR mortgage off well within 10 years at the current repayment rates, as long as I don’t blow out on the spending on all the exciting projects I was talking about earlier and chew up my offset funds.

Having said that, with the debt recycling I probably wouldnt be blowing up my share portfolio a second time just to pay off the mortage at that 11.5 year mark – its more about growing an additional income stream for retirement and lowering our overall financial risk.

Our current lifestyle is a pretty sustainable financially, even with Mrs FI not working, so once she decides to get back into it and starts up her contracting business, and we start to rent out some accomodation we should be pretty sweet in terms of diversified income streams and being able to make additional deby recycling investments as well as add to the mortgage offset and smash it down quicker.

Captain FI’s Investment property

The current PropTrack automated online valuation estimate is $731K, which is up $31,000 from the last quarters estimate. The property has has a $530K mortgage (6.39%) attached, for an equity position of $201K.

I have a small offset of a few thousand (to help manage cashflow and property management expenses) and pay $850 weekly repayments for the loan, and collect $700 weekly in rent. Other costs (insurance, rates, water, sewage, property management) adds up to about another $50 a week, so at the moment it costs me about $200 a week or $10,400 a year to hold.

This means it is negatively geared (which is annoying for someone who is trying to be retired) but the interest (and other costs) are tax deductible, and that combined with the depreciation schedule does give us some tax time relief. Although I am not a high income earner anymore, so it clearly isnt the prime reason I have kept the property.

More issues with tenancy – unforunately had the tenants break lease and had to get new tenants. Wasn’t the end of the world as it meant I could align to the market rent (it was leased below market rent before). Annoying as had to pay advertising and letting fee again early.

The goal of the Investment Property is to build our wealth (diversified outside super and shares) through the capital growth of the property so that we have financial options without having to sell (or try and remortgage using equity in) our home if we are not quite ready to move out and downsize yet.

As inflation causes rents to rise, we slowly pay down the loan, and when (or if) interest rates decide to cool, it should over time become positively geared and provide us a source of income. The current estimate is that the cross over point should be around 3 years away at around Christmas 2027.

I currently have 22 years left on the loan (Principle + Interest) before it is paid off, however I don’t mind having the mortgage on the IP as we have a good chunk of equity, and if everything goes to shit – well I can just sell it. Whereas we definitely do NOT want to be selling the home that we currently live in, so the PPR mortgage is a small source of anxiety for me. That is why we like the IP mortgage but dont like the PPR mortgage. Also the IP mortgage is tax deductible and the PPR mortgage is not

With our current situation, its not really possible to refinance – but if I could, I would like to somehow access the equity to buy shares or other investments. Actually, I would have loved it if we could have done an interest only loan so we don’t have to keep locking up our cash away as equity in the property by repaying the loan principle portion every week – this would massively improve the cashflow and essentially we could be using some of the rent to pay the loan interest, and then we could use the rest of the rent as an income stream to invest more.

We would still be gaining equity with the capital growth of the property anyway as the housing market continues to grow over time – the theory being that when you just continually ‘roll-over’ the interest only loan every five years and then when you eventually sell the property, you settle the loan. But alas, banks are not offering interest only loans any more!

For this reason, I don’t put much money in the IP mortgage offset – a few thousand dollars only for cashflow management purposes. I think I will also switch the repayments from weekly back to monthly repayments which should free up about another $3400 a year in cash flow and make it positively geared quicker. I will just run this by my accountant first.

I have previously written a full separate article on the IP build if you want to know more about the process – CaptainFI’s residential property development investment.

Captain FI’s Online Business (website portfolio)

I have a small website portfolio of content and affiliate marketing sites. These make money semi-passively from display Advertising through managed ad networks such as Adsense and Mediavine, and affiliate programs such as Amazon Associates and other direct affiliate deals.

The overheads are pretty low – just some software subscriptions, my Virtual Assistants, and the cost of producing content – either writing it myself or subcontracting it out and paying specialist writers and editors

I’ve written a pretty detailed article here about how to make money online, and I recently published a few more articles about how to start making money online for beginners, as well as an ultimate list of blog income reports

I have been pretty slack with the business because I’ve got a big chunk of savings so I don’t really have the fire lit under my ass anymore. I think some of the sites I am just sick of working in that niche and its just not as interesting to me anymore, but I still enjoy CaptainFI, the flying site and the gardening site.

I have actually since sold a number of my smaller sites, and am just focusing on the larger ones which are more of passion projects for me. This is probably for the best as I’m just going to end up neglecting them anyway – someone else can take them over and grow them with the enthusiasm and time/effort investment needed.

I have a couple more for sale around the $5,000 to $10,000 mark, depending on how established and how much time, money and effort I have put into them. They range from 3 to 6 years old, with various backlink profiles, number of published articles, and traffic. You can check out this article on website operation if you are keen as I’ve listed all the details in there. Feel free to send me an email through the contact form or get in touch on social media if you are interested in buying one.

I originally learned these skills through the eBusiness institute over the past 4 years – I have done a pretty comprehensive review of the eBusiness institute as well as interviewed Matt and Liz Raad about this on the podcast again recently where we go over a huge list of frequently asked questions about online business if you want to learn more about this. They also provide some free introductory training for CaptainFI readers.

Check out these podcast episodes for more information

- Podcast | Q and A Session with Matt Raad – Part THREE

- Podcast | Q and A Session with Matt Raad – Part TWO

- Podcast | Q and A Session with Matt Raad – Part ONE

- Captain Fi Podcast | Online Business with Matt Raad

- Podcast | Digital Marketing with Richard

- Podcast | Entrepreneurship with Liz Raad

- Podcast | Digital entrepreneurs Matt and Liz Raad

I have also recently finished the Authority Hackers TASS (The Authority Site System) Course as well as the Making Sense of Affiliate Marketing course which has been a cool way to consolidate the skills I have learnt from the eBusiness Institute, and I have published a few comparison review articles such as Authority Hacker vs Making Sense of Affiliate Marketing and eBusiness Institute vs Authority Hacker which might help you choose between training providers.

Angel Investing

I have a small ‘Angel Investment’ in the Financial Independence brokerage platform Pearler. This was the maximum allowable private investment of $10,000 (AUD) made in July 2021, with the total number of ‘private equity’ shares based on their June company valuation.

I am not tracking the exact company valuations for Pearler, but I know the company has had its valuation more than triple and has raised over $10m through VC funding rounds, with more to be raised in later rounds, so I assume the shares are worth a bit more. How much exactly, though? I am not sure, but trying to find out.

Cash – Mojo and emergency fund

Cash reserves are high at the moment – $285,000 in cash waiting to be debt recycled through the PPOR home loan. As I said, with the interest rates being so high at the moment, its actually not a bad idea to just keep the cash parked there – ultimately I do want to deby recycle, so I will eventually get around to it soon.

After Debt recycling, I will look to keep 12 months worth of expenses in the offset account, which is probably about $75,000 (including my mortgage repayments)

Captain FI’s Net Wealth progression

During my journey to FI I roughly documented my net wealth progression via monthly updates and a graph which was rather crudely constructed in Excel. It demonstrates the ‘somewhat exponential’ journey over my 14 year ‘working’ career. You can access the archives for my Net Worth updates here to see how it’s gone over time. Check out the graph and all the updates below to see how it has gone since the beginning.

When I FI/RE’d, I stopped putting out regular net worth updates and stopped calculating my net worth, and tried to just put out quarterly ‘updates’ but I was pretty slack. I am trying to keep up with quarterly tempo, and recently calculated my net worth after selling shares to buy my dream farm (hence the lack of data points on the graph below lately).

| Date | Net worth | Difference | Saving Rate | Notes | |

| Jan 09 | $5,000.00 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK | |

| Jan 10 | $24,000 | +$19,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 11 | $40,000 | +$16,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 12 | $92,000 | +$50,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 13 | $130,000.00 | +$38,000 | ? | Estimate NWbased on historical Super, Bank statements and assets at the time | LINK |

| Jan 14 | $161,000.00 | +$31,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 15 | $200,000.00 | +$39,000 | ? | Estimate NWbased on historical Super, Bank statements and assets at the time | LINK |

| Jan 16 | $281,000.00 | +$81,000 | ? | Estimate NWbased on historical Super, Bank statements and assets at the time | LINK |

| Jan 17 | $340,000.00 | +$59,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 18 | $482,000.00 | +$142,000 | ? | Estimate NWbased on historical Super, Bank statements and assets at the time | LINK |

| Jan 19 | $542,000.00 | +$60,000 | ? | Estimate NWbased on historical Super, Bank statements and assets at the time | LINK |

| Jul 19 | $578,900.00 | +$36,900 | 84% | Finally began tracking NW this like a proper adult. | |

| Aug 19 | $560,100.00 | -$18,800.00 (-3.2%) | 78% | Share market slight correction, Ok savings. | |

| Sep 19 | $584,744.88 | $24,644.88 | 72% | Share market rebound, savings rate not so good. | LINK |

| Oct 19 | $600,386.00 | $15,641.12 | 84% | Good saving this month. Normal salary, plus allowances, dividends from index funds, tax refund, eBay selling and was working abroad in asia where things are cheap. | LINK |

| Nov 19 | $612,917.21 | $12,531.21 | 76% | Falling short of my savings goal of 80%. Mostly domestic legs this month with higher costs. Also invested in hydroponics. | LINK |

| Dec 19 | $625,350.00 | $12,432.79 | 76% | Good savings of cash (for development) and investment, however higher spending due to Christmas period (Travel and Gifting). | LINK |

| Jan 20 | $865,212.00 | $239,862.00 | 55% | Super settlement was a HUGE boost to NW. $9K growth from stock market. Expensive month lots with lots of unexpected bills – weddings, travel, Booking flights, fines etc. | LINK |

| Feb 20 | $851,802.0 | -$16,592 (-1.9%) | 52% | Large increase in spending on myself this month, still managed to tuck away $5K to put into shares and property. Corona Virus market scare resulted in a correction and gave NW a small negative trend. Time in the market not Timing the market! Became Single again. | LINK |

| Mar 20 | $819, 354.6 | -$31,806.95 (-3.7%) | 80% | Another small step backwards in the NW due to the ‘corona crash’ in full swing. FIRE Portfolio of ETF/LICs down about 15% this month, however due to high savings rate and structure of my superannuation annuity the NW is only down 3.7%. Savings rate good at 80%, higher than usual income (with some slightly higher spending, too). Picking up shares on discount – this is the best outcome for someone in the accumulation phase with good income! | LINK |

| Apr 20 | $847,023 | +$27,668 | 85% | $11,000 in rebound of stock market capital prices alone (up 6%), plus first quarter dividends paid (heavily reduced due to banks withholding dividends). Great savings rate due to COVID-19 lock-down = no spend. Increased entrepreneurial efforts and selling down of physical possessions provided side hustle income. Two standard paychecks from flying activity; domestic day trips only so no allowances. All cash unfortunately had to go into the property development due to contract timing, I am chomping at the bit to buy some more index funds before they go back up in price too much – hence why I am selling most of my toys! | LINK |

| May 20 | $857,859 | +$10,836 | 92% | Some Great sales as I let go of my Super Sport Motorcycle, Some gym gear, expensive flying equipment and a few other various bits and bobs and invested this money. Flying still reduced, but increasing from April. The share market grew as I continued to make my fortnightly investments. I also wrote down the ‘value’ of some of my possessions (liabilities) such as my car, tools and furniture by around $10K to align them to market price (“tell him hes dreaming…!”). | LINK |

| June 20 | $858,650 | +$791 | 90% | Small Net Worth gain as I continue to declutter and simplify my life, despite being off work due to a family emergency. Share market not doing much. | LINK |

| July 20 | $888,218 | +$29,568 | 68% | Majority gain due to share market going back up, low spending due to being on the family farm and at home because of lock down. | LINK |

| Aug 20 | $1,029,293 | +$141,075 | 74% | Became a millionaire. Achieved this massive milestone I set out for myself in Dec 2019. Included unrealised gains in my property development as well as website business. Good savings rate due to not much spending, invested in Aus and total world shares. Investing in my web business. Starting to shift focus away from $$$ and more into looking after my mental health. | LINK |

| Sep 20 | S1,045,486 | +$16,193 | 60% | Officially took time off work for the rest of the year to be close and look after family during major operations. Continued to sell down physical possessions and work on digital business while at home. NW gain mainly due to valuation of websites. | LINK |

| Oct 20 | $1,064,399 | +$18,913 | 80% | Base income (retainer) and leave loading, dividend and websites provided income, as well as raiding my P2P lending capital. Significant bill for property due to design not meeting standards which effectively lowers my equity position, as well as fence being stolen. | LINK |

| Nov 20 | $1,143,433 | +$80,394 | 82% | Big gains came from share market growth (influencing both the Financial Independence share portfolio and Invested superannuation), Business gains (due to increased earnings) and a $30K boost to my annuity thanks to me logging in and checking the fine-print on the accumulation stats. I only invested around $7K. Insane that in one month, I accumulated nearly more net worth than I did in four years from 2009-2012 | LINK |

| Dec 20 | $1,152,920 | + $9,487.32 | 84% | Share market slight drop, Earnings from Business, Contract work, Selling possessions. No share market investments this month (oops! I forgot and money was tight). Invested a lot into the website business this month (way more than planned) and it is still running at a decent loss (plans to turn it cash flow positive in 3 months). | LINK |

| Jan 21 | $1,165,678 | +$12,757 | 79% | Great returns from the share market. Earnings from Business, Dividends, Flying wage, flipping items on consignment. Regular share contribution, investing in micro investing platforms, P2P lending, Investment property and big reinvestment into the business (still running at a loss) | LINK |

| Feb 21 | $1,135,272 | -$30,406 | 76% | Significant write down on property development due to council DA rejection and redesign requiring more money and creating less equity. Offset by small increase to Business value and investments. Simplified my investments and switched over to Pearler. | LINK |

| Mar 21 | $1,155,594 | +$20,322 | 71% | Continued investment into the portfolio as well as growth of investments and business. Gave my notice at work and looking for part time job at home for ‘Barista FI’ | LINK |

| Apr 21 | $1,242,220 | +$86,727 | 74% | Property development back on track | LINK |

| May 21 | $1,379,469 | +$137,248 | 72% | Massive gains in the website portfolio due to revaluation based on recent business income, big growth of superannuation due to annuity increasing (salary increment) and shares generally went up. Crypto went down by about 40% or so. | LINK |

| June 21 | $1,469,989 | +$89,757 | 41% | Quit flying role and moved to Adelaide. Great month for investments, websites producing serious income so accordingly they are valued higher. Spent a lot on furnishing the new apartment and on enjoying some more luxuries. Seeing a therapist to help deal with anxiety from leaving work. | LINK |

| July 21 | $1,543,959 | +$74,732 | N.A. | Set myself up in Adelaide. Did basically nothing for the whole month except spent time with family, relax, sleep and go to doctors appointments. Massive boost to website portfolio AdSense and affiliate incomes, as well as general share market performance. | LINK |

| Aug 21 | $1,624,116 | +$70,156 | N.A. | Relaxed again, focused on mental and physical health, and spending time with family and my partner. Big increases to spending (too afraid to calculate a ‘savings rate’) but also big increases to NW through website portfolio income growth. Finally got the slab poured on the investment property (foundation). | LINK |

| Sep 21 | 1,640,663.85 | +$16,547 | N.A. | Stocks, super etc went down, but business income from websites increased, plus business valuation increased. Property build. got to frame stage, and I also got a dog! Expenses for vet surgery well worth it. Moved into a nicer apartment | LINK |

| Oct 21 | $1,705,907 | +$65,243 | 30% | Big boost from website valuation due to securing new affiliate contracts for recurring income, shares went up nicely. No massive changes to this month. Calculated a savings rate and found myself pretty low due to spending a lot on my garden and going out quite a lot – I don’t think I will calculate this savings rate figure any more. | LINK |

| Nov 21 | $1,739,144.23 | +$33,236 | – | Great month. Relaxing (somewhat). Spent a lot of money doing ‘fun’ things like winery tours, a fine dining experience and self education. Shares moved sideways (well slightly down) but everything else went up. Building got to enclosed stage (roof, walls, windows and doors) but have had some issues with build quality and weather / covid delays. Put a $1000 deposit on the puppy. Stopped tracking Savings Rate. | LINK |

| Dec 21 | $1,764,516 | +25,372 | – | Spent nearly the whole month with family, did some work on the website portfolio. Traffic recovered from google algorithm changes. Invested $10K into Stockspot and Sixpark, $1K into ACDC, $100 into Comsec pocket and $100 into Bamboo, $260 into BTC, $4K into ETFs through pearler. Paid the $3000 balance for the puppy. | LINK |

| Jan 22 | $1,826,633 | +$62,117 | – | Stock market slightly down, Massive boost to website traffic (overall its more than doubled). Invested $10K VTS, 2K VEU through pearler, Paid for Angels cancer surgery, bought more BTC and ETH, bought a parcel of ETHI on commsec pocket. | LINK |

| Feb 22 | $1,757,210.57 | -$69,422.93 | – | Stock market down, Website business revenues down and additional spending on content and staff for business, Additional property development bills, some unexpected expenses, Wrote down the value of some of my personal property (and gave stuff away). | LINK |

| Mar 22 | $1,701,410 | – $55,799 | – | My last ‘regular’ monthly Net wealth update as I give notice at work and finish up my non-flying job. | LINK |

| Q3, 2022 | Over $2M | N.A | – | Six months of Early Retirement in Rest mode! I stopped tracking my net wealth post-FI, my dog passed away, I gave away most of my physical stuff and moved to become my mums live-in carer, met a lovely girl, bought a puppy. Had some incredible months with semi-passive website income but overall neglected the business and regular (stable) revenues decreased. | LINK |

| Q1, 2023 | Over $2M | N.A | – | One year of Early Retirement! A lot of (sad) changes, the passing of my mother and family feuding resulting in temporary homelessness, selling my ‘nursery’ of plants, and traveling overseas for a few months. Finding a new home to settle, couple of domestic trips flying to Tasmania and Queensland a couple of times, and plenty of camping and road trips within SA. Did not work much on the business at all and lost a few more contracts and had to cut staff. | LINK |

| Q2, 2023 | Over $2M | N.A | – | Getting back on top of things with podcasting and blogging more regularly. Focusing on building our ‘rich life’ and deliberately increasing spending in areas such as food, travel and convenience. Did a few interviews and went on a few podcasts. | LINK: CaptainFI Q2, 2023 Net Wealth Update |

| Q3, 2023 | Over $2M | N.A | – | Big focus on health and fitness, fixing diet and losing excess weight. Continue to sell a few websites from portfolio and focus on largest ones. Attended some FIRE events and lots of road trips | LINK: Captain FI’s Q3, 2023 Net Wealth Update |

| December 2023 | $2.26M | N.A | +$260K (21 months since last calculated) | Interim calculation due to share sales prior to purchasing property – no update published | No update published |

| Q2, 2024 | $2,417,426 | 12% – Calculated to see where we sat | +$157,426 (6 months since last calculated) | Mid year 2024 Net Wealth update. Sold shares, crypto and 5 websites, Purchased the farm in Queensland, received $250K inheritance, significant cost in setting up the property. | LINK: Captain FI’s Q2, 2024 Net wealth update |

| Q3, 2024 | $2,485,000.00 | N.A | +$67,574.00 (3 months since last calculated) | Q3 2024 update. Lots of spending on wedding and bought a boat, preparing to debt recycle. Properties saw great paper gains. |

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Wow, lots happening for you! Congratulations on the wedding and Bebe! So I’m not active on social media so I probably missed the announcement but did you love to QLD? I thought you were in Adelaide and bought a farm there?

Thanks Claire! Don’t worry, I haven’t been as active either. It seems there is always a lot to do now after getting acreage haha. We used to live in Adelaide, but for a fresh start we decided to move somewhere greener 🙂

What are your thoughts on the SWR here? I have read somewhere that it is more like 2.5% for multiple reasons, can’t really find much good country specific information

Safe withdrawal rate? It depends on your risk tolerance. Personally I am pretty happy with 4% and how that has played out over recent history. However its probably worth noting I YOLO sold my share portfolio and bought a farm, so my SWR is probably how many beans I can pick from my veggie patch at this point 🤣