October was a big month for me. I finished a long training package at work and spent quite a bit of time overseas – visiting new countries throughout Asia and the Pacific region. I have to say I really enjoy getting immersed in the local culture, and I am not a fan of simply staying in the resort or hotels – although this is sometimes your only option on a maximum crew duty day when all you want to do is eat a meal and go to sleep!

From a finance perspective, being away a lot is great as you earn extra money and realistically your not going to spend all the allowances, especially when your exploring and eating like a local. Being away a lot also means you save money on transportation to and from the airport (I used way less fuel this month) and you spend less money on going out, on groceries and general house-hold upkeep. Being in a one bedroom apartment in Sydney, its fairly low maintenance anyway and I just turn the power off as I leave and lock it up.

I have started to expand my balcony garden, now that my bamboo has really taken off and is providing a good amount of dappled sunlight shade which will protect the seedlings from the harsh sun. I have planted Beans, Corn, Snow Peas, Sweet Peas, Lettuce mix, carrots, parsley, cherry tomatoes, regular tomatoes and basil which should give me a heap of fresh healthy produce for my whole food plant based diet. I don’t know if its the right season or not, but i’ll give it a crack anyway.

I have a heap of pots lined up on my balcony by the edge. I really wanted to do this and try and spend as little money as possible – so I have ‘borrowed/begged/stolen’ almost all of the items required (except for having to buy 20 large pots from a gardening store for $2 each). I filled up the pots with dirt from a nearby creek (being passionate about FI/RE I seriously just refused to buy the dirt – even if it is dirt cheap!). After a week I have seen the peas and beans germinate, as well as some of the lettuce. After the Veggies take off I want to start with some fruit trees – my family has always had orchards and I am a total fruit bat. Even in Sydney a mate of mine has a fantastic collection of fruit trees in pots in the backyard which are very impressive and are yielding awesome fruit so I know its achievable. I think I will start with a lemon tree in a large pot.

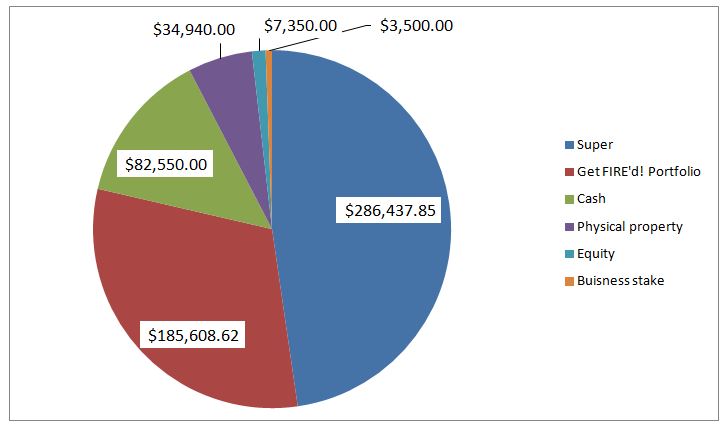

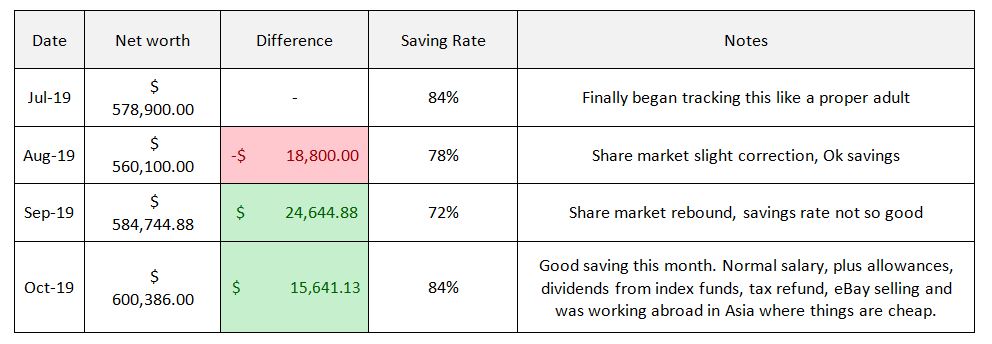

The Networth has been steadily growing and finally cracked $600K (including superannuation). I have reached my first milestone of Lean FI which entails a gradual draw down of my investment portfolio at approximately 7% for approximately 25 years before I can access my Superannuation and Pension. I think that 7% is still a fairly high draw down rate (so the level of risk is higher than I would like) – I’ve joked that this milestone should be called Risky FI. Each day I continue working, saving and investing in the portfolio, the draw down rate decreases and I feel a little more comfortable with the situation.

Net Worth

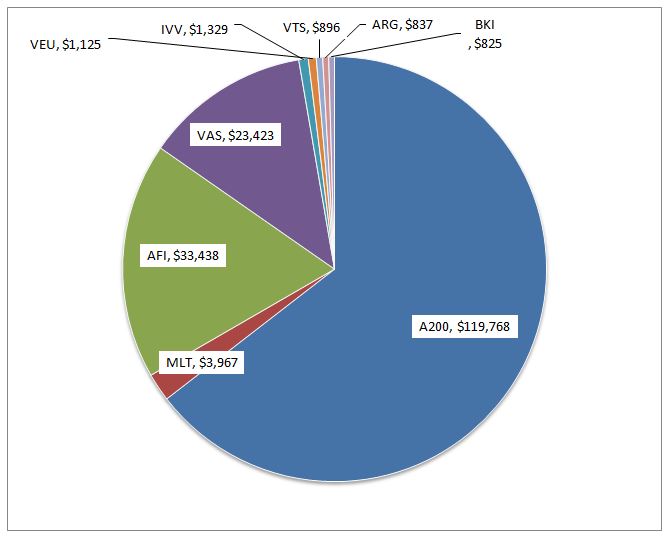

Get FI Portfolio

The Get FI Portfolio is now sitting at approximately $185,600. I broke my cardinal rule and sold some MLT stock to fund a property deal, but it is for the greater good, and I plan to continue adding to the Get FI Portfolio once I have finished directing my torrent of cash savings into the property development. I am also quite heavy on investing in stock market index fund ETFs and plan to continue to add to the LIC pile so long as they keep trading at a discount.

Investment Decisions

I sold some of my Milton stock which kinda sucked, I felt like I was killing the golden goose. I needed the money for the property deal and the price had just risen and all of the other ETF/LICs in my portfolio had dropped, so I sold my entire holding. However later in the month with surplus cash I reinvested approximately $4000 into a parcel of MLT which was a bit of a consolation prize for the month – yes I realise the irony of buying and selling but whats done is done.

I also invested a further $3500 into a property management business start-up, and hope to see some good returns on investment by the end of the year. It has been a bit of a learning curve but gathering all the required items to start and then outsource the management of a short-term rental property has been kind of fun!

Property

Settlement is completed on the land purchase, and negotiations with the builders through Northblock have started. Hopefully we turn soil by the end of the year – with an estimated 18 month build time to generate approximately $150K of equity (profit) through the deal. Not a bad ROI for a $100K investment (deposit on the land and construction loans, fees and bank interest payments for the project build time).

Time will tell, however, if this is as profitable in reality as it was seen to be on paper. I expect delays, extra costs and lower than expected valuations, but I am confident it WILL make a profit. I have been wanting to diversify out of just 100% stock on the path to FI – given that I currently have a large super balance (essentially a 401K or Roth / IRA tax sheltered stock portfolio) as well as a respectable Get FI ! Portfolio of stock market ETF and LIC index funds outside of super.

Doing your own property development (buy land, build, subdivide) means you can either flip for some cash to then inject into your stock portfolio (probably the best option – good returns and almost zero holding costs – no hands in the cookie jar), OR you can hold it and then have ‘bought it at wholesale price’ to keep as a rental. There are many hands trying to get ‘in your cookie jar’ (land tax, rates, utilities bills, mortgage interest, council fees, stamp duty, emergency services levies, management fees, landscaping/gardening, maintenance etc etc etc) so you just need to be careful and diligent about cash flow – but rentals if bought at the correct price, in the correct area, and managed well can be an attractive cash flow positive option to complement a good stock portfolio.

Just don’t be foolish and mortgage yourself up to your eyeballs negatively gearing and hoping that inner city property prices will continue to skyrocket so you might be able to cash out in a few years. To me an investment needs to put money in my pocket, and food on my plate (not the other way around!)

Superannuation

No real news to add here. Approximately $1000 in contributions to my superannuation as well as growth within the fund. Its tricky to get up to date statements so I will just report my contributions per month and then at the end of the financial year when I receive an annual statement I will be able to compare my estimates to the actual value.

Income stream

Income for October was a combination of my regular flying salary, international trip allowances, dividends from the Get FI ! Portfolio, as well as eBay selling and receiving last years tax return. This all ended up being a bit higher than normal (as well as considering that October contained three paydays this year). I can’t disclose my actual salary or position due to non-disclosure agreements however for the more savvy readers you can probably get the hints and work backwards based on super contributions etc ??

Budget and expense tracking

Tracking the budget got a bit of a shake up this month. I started treating gross allowances as income rather than whatever I had been able to save after spending; I thought I was ‘cheating’ a bit with regards to my savings rate and so this should keep it a bit more transparent (and help motivate me to spend less when I am away overseas on tasks). Unfortunately this makes my savings rate go DOWN but I am still determined to meet my goal of a minimum 80% savings rate.

I am confident that as my income grows both from my flying career, the GetFIRE’d! Portfolio, Side Hustles and businesses that I will not fall fowl of lifestyle inflation and see a positive trend of an increasing savings rate.

Even accounting for the new way of calculating savings rate (Savings+Investments+Super)/(Gross income into the account) I managed to meet an impressive 84.2% saving rate for October 2019.

Retirement Income streams

The following income stream calculations are an approximate of how much passive income I am expecting to receive as a base retirement income if I retired right now. Obviously I am still going to work on some projects and on my businesses in my retirement (such as web development, property development, property management and online arbitrage) so its unrealistic that this will be all I have to live on.

The passive retirement stream is based upon a combination of dividends from the Get FI ! Portfolio, and rental returns from cash flow positive property with an interest only loan (cash out refinance to buy more stock market index ETFs whenever the property goes up in value and can be revalued). It does not currently include yield from the business or any other active investments, and is purely a passive income stream

Stage one – before preservation age

- 4% sustainable draw for ever = $11,020 per year ($918/month), or;

- 7% draw down over 25 years = $19,285 ($1607/month)

Stage two – Superannuation

- Super pension benefit / retirement annuity = $7,983 ($665/month), and;

- Social Security Aged pension = $18,122 ($1510/month)

Net worth table

Conclusion

I hope you got something out of this update and it helps you towards FI and developing your very own Get FI portfolio! Let me know in the comments below if there is anything you need clarifying or want me to include for Novembers update. Cheers

Get FI !

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.