CaptainFIs financial and personal update for Q4 2025

Q4 2025 Net Wealth: $2,433,746

Change from last quarter: +$35,259 – property valuations drove NW higher despite cash savings reducing.

Savings rate: N/A – (negative / deficit)

Total spend for 2025: $119K, $34K above baseline budget due to buying new car, tractor, property projects and travel.

Captain FI is not a financial advisor, does not hold an AFSL and this article is not financial advice. This website is reader-supported, which means we may be paid when you visit links to partner or featured sites, or by advertising on the site. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer

Executive Summary (AI summary – Chat GPT)

2025 was a major year of transition for Captain FI, defined primarily by becoming a father and reshaping life around family, health, and long-term sustainability. Parenthood has been deeply rewarding, albeit demanding, prompting a deliberate slowdown in work, a period on Paid Parental Leave, and a stronger focus on systems that support a balanced life on the hobby farm. While sleep deprivation, Centrelink challenges, and higher living costs added pressure, the year ultimately reinforced core values around time freedom, intentional living, and building a “rich life” beyond pure financial metrics.

From a financial perspective, spending decreased from 2024, but was still higher than baseline projections due to family life, property projects, travel, and lifestyle choices associated with acreage living, with total 2025 spending landing at $119k resulting in spendings outpacing earnings. Despite this, finances remained controlled and intentional. A renewed focus on automation and simplicity provided clarity across multiple accounts, repayments, and expenses, reducing mental load and supporting better decision-making. This visibility helped maintain predictable cashflow, make additional debt repayments, and stay aligned with the broader goal of reducing debt and increasing resilience rather than maximising short-term returns.

Strategically, Captain FI continues to prioritise simplicity, low stress, and flexibility over complexity. This includes favouring mortgage repayment over debt recycling for now, selectively rebuilding share investments, holding a leveraged investment property for long-term growth, and maintaining a lean online business to support semi-passive income. Alongside speaking engagements, podcast appearances, and a New Year partnership with WeMoney, the overarching theme for the year was clear: boring, repeatable systems work best. Clarity leads to confidence, simplicity leads to consistency, and strong foundations—financial, physical, and personal—create the conditions for long-term independence and a fulfilling family life.

Captain FI’s personal update

I cant believe its the end of the year already – wow, 2025 was a big year of firsts for us. Obviously the big change for 2025 is I am now a father, and I think it is just the best thing I have ever done. I have the most beautiful, bubbly, energetic, cuddly, adorable little toddler zooming around the house, and it has just made our lives so much richer. Yes the sleep has been sacrificed, but we are hoping (praying?!) that it will come back soon…

We are really growing into the big house now, with two dogs and the toddler zooming about, you wouldn’t believe it but there is a part of us that are actually wishing for some extra rooms! We do have a project on the go to build a very large shed with a mezzanine office / man cave, and a laundry and bathroom downstairs – but that is still probably a few more years away at least.

I have just finished up being on Paid Parental Leave which has been great to step away from running the business and hand the reins over to my wife for a little while, although the $4000 a month didn’t go super far with the expenses of running a hobby farm, 5 mouths to feed, a mortgage and a negatively geared investment property.

There was a bit of an administrative nightmare because centrelink wouldn’t allow my wife to take the PPL entitlement due to her not meeting residency requirements – even though she had her Australian Citizenship already approved (but just not physically presented with the certificate yet). In the end we basically did a swap and she took over running the company whilst I took on full time Daddy duties.

I found the centrelink system in general was a huge pain in the arse, it felt like they were fighting us at every step to try and discourage us from accessing our entitlement, but we stuck to our guns and despite several rejections we finally got it approved.

In terms of Personal relationships, we spent a lot of time with our mates, we made some new friends, my wife is going out a bit more with her mums group, and I had been doing more fishing, some camping trips and hiking. Caught a few big fish, including a 1.03m Barramundi, and my mate caught a 1m cobia out on the reef which we turned into Sashimi and beer battered fish and chips. I still have really no clue what I am doing when we get out on the water, but I am having a lot of fun learning, and have all the gear now at least.

We did find we got a little bit stretched thin helping out a lot of people with their projects and maybe even just socialising a bit too much, making the journey into Brisbane city a lot, and neglecting our own self care and house / farm work. Ultimately we did have to pull back a bit to focus just on our own little family and core circle of close friends, as well as trying to run the day-to-day on the hobby farm and slowly make progress on our projects.

We started prioritising our health better now that we are out of the newborn trenches – we put the finishing touches on the home gym now by adding cardio machines, and working on some pretty physically demanding projects around the property. I am taking it slow, so I try to do just do an hour in the early morning and another hour in the late afternoon to avoid the heat and peak of the UV. Thankfully it’s been working and I haven’t been sunburnt in a while. The irony is I haven’t even really been using the home gym at all because Im always so shagged from farm jobs!

We are getting into a great rythm with the family, and all seem to be in bed by about 7pm!

I am starting to get back in control of my weight, as I got a bit too heavy at the start of the year almost hitting 100kg. I am back down to 83kg, and feeling much more limber. I was really struggling with motivation, poor sleep and diet, low energy, and an increase in chronic back and joint pain. A health check with my GP showed some risk marker levels in the blood test, so we came up with a plan to shed some weight.

Whilst not for everybody, I decided to try the GLP-1 (glucagon-like peptide-1) injections – commonly known as ‘Ozempic’. I’m not about to dive into how it all works – you can ask ChatGPT to spit you out all the details if you like (if you trust what it says), but basically it just suppresses your appetite and stops you absorbing sugar. It does have some risks and negative side effects though so its not a magic bullet.

It has really helped suppress my appetite so the whole ‘ADHD food noise’ thing has been quietened down, and I don’t seem to be snacking much anymore. My weakness was if we had snack foods in the house or even lots of fruits, I would just gobble them up. So thankfully that’s not happening as much. Whilst I was on the GLP, I felt even more tired than usual most likely due to the fact that I was not eating as much calories as my body was used to getting, hence the weight loss I suppose.

Its not all beer and skittles though, because I’m eating less and focusing on a low carb (keto) diet, my ability to do anaerobic activity has been massively reduced and a couple of times its resulted in me dry retching or spewing my guts up after trying to do yard work in the heat. So I have had to learn to pace myself, take it slower and work in the aerobic / cardio ‘fat burning’ heart rate zone in the early morning and late arvo so I don’t keel over.

Given I am now approaching my target weight zone, of around 80kg, I’ll be weaning off it in the new year, adding a small amount of complex carbs back into the diet and getting back into weight training in the gym to rebuild up a bit of the strength I have lost.

Another good thing we did for our health recently was finish off the home office with a large ‘triple station’ corner sit / stand desk. The funny thing was we sold our old desk on facebook marketplace for the same price as what we paid for the new one – its triple the size and has three motors and electronics for pre-set heights.

It’s works well with our current work cycle system, because my apple watch will buzz me to tell me to stand so I just hit the preset button and stand up, which helps close my activity rings. When I’m tired, I convert it back to sitting. Because of the additional standing, I have got a new set of Hoka trainers and Oofus slides to help reduce foot pain. Good shoes are well worth the investment, and I should really be getting new ones every year at bare minimum anyway – they are just expensive. The new shoes and slides I think have also helped reduce back pain, and I do have to go see the podiatrist for some new orthotics soon too.

We expanded our apiary this year too, adding native beehive’s which have been a lot of fun. We have been learning to care for them, including doing our first batch of splits (turning one hive into two) and now in total we have 14 hives on the property. Whilst the natives don’t produce anywhere near the scale of honey that the european honeybees do (native beehive circa 1kg per year whereas our honey bees closer to 120kg per year), they are much safer around the family as they don’t have stingers. So we have really packed them throughout our house gardens, dragon fruit zone and veggie patches – I am hoping to see an increase in pollination and therefore stronger fruiting.

We have not (touch wood!) lost a single chook this past year, so I am pretty proud of the work that went into building our predator proof chicken house and run, and the girls enjoy foraging out in the orchard all day where they can feast on dropped fruit and pest bugs, and then hide under the fruit trees and bushes from potential predators if needed. They get our kitchen scraps and food waste, as well as mixed grain feeders and shell grit which keeps them very happy and healthy. The worm farm gets anything the chooks can’t have or wont eat, so everything gets used and there is very little waste here.

Had some classic car shenanigans with ScoobyDoo – to be expected with a 20 year old car I suppose. The radiator tank cracked just as my wife was pulling into the driveway – as far as failures go, that’s probably the best case scenario.

Ended up being a really simple fix – new radiator (bought for $100 on marketplace), a thermostat and some coolant from super cheap auto and we were back in business!

In addition to the yearly oil change, we also modernised the old girl and put in a 10 inch touchscreen with apple carplay and a reversing camera. It is a game changer and I can’t believe I drove her for 13 years without it! I feel like it is almost a necessary safety item to have the reversing camera now that there is dogs and young children on the property. Total cost around $1000 for the repairs, annual maintenance and upgrades, and she’s good for another year.

We decided to keep driving her for another ~5 years so we can prioritise paying down debt. When we did the math regarding upgrading to a newer Pajero / Prado, if we keep her for another 5 years the projected savings in depreciation, additional maintenance, increased fuel consumption, higher insurance premiums and opportunity cost (of mortgage interest saved) would completely pay for the new car anyway. So the sensible option is to simply keep her and throw that money onto the mortgage.

Also, the whole point of getting a larger 4WD is to tow a larger boat (safer and more capable for offshore fishing trips), and we can’t really get the bigger boat until we build our Big Fricken Shed to put it in anyway. Plus there is no way im spending $30K+ on a 4WD to then leave it parked outside in the weather. So for now, Scooby-doo languishes on the driveway, exposed to the harsh QLD elements while our current boat takes pride of place inside the garage.

It’s really only me that drives anyway, or our guests if they need a set of wheels. The family have the nicer, newer, safer car in the garage which stays cool, and I don’t mind getting into a hot car – it just reminds me of the good ole’ days flying in the tropics anyway!

We are in the midst of sleep training our toddler and weaning off night feeds, which has been one of the hardest things I have ever had to do. Hearing the cry and having to wait the 5 minutes before calming them, it feels like an eternity and I feel like a real bastard. But, this is on the advice of the paeds and nearly every book and thing I have read online about sleep training. Bub is still in our room in a cot literally right next to our bed, but I guess would rather prefer to be in the big bed with us!

My wife really wanted to do this six months ago, but at the time I wasn’t ready (literally emotionally I couldn’t deal with it) but we are now on the same page. It is slowly working, and bub is already sleeping better. This is really the start of equipping our child with the skill to self-regulate, which is a pretty critical life skill. But yes, it is a bumpy road and lots of ups and downs with all the cycles of development. It feels like just as we achieve something, a new development stage starts and then we get the regressions.

Parenting is hard, but SUPER rewarding. I love that as our child is growing bigger, stronger and more confident, they are becoming more adventurous to explore the property and try some of the home grown produce like the bananas, berries and figs.

It makes it feel like all the hard work and sacrifice was worth it, as this is my dream come true – I can focus the majority of my time, effort and resources into being the best dad I can be. I am breaking generational cycles and building wonderful relationships.

I have to resist buying toys as I am an absolute pest for buying “educational”, “climbing”, “musical” or basically any wooden toy on Facebook Marketplace or at the op shops – my wife often sighs as I grin ear to ear unloading the latest boot load of ‘things for baby’.

FI Freedom Retreat Bali

I was invited to be a guest speaker at the 2025 FI Freedom Retreat in Bali, hosted by Amy Minkley, which was awesome! I was pretty blown away by the level of experience amongst the attendees – we had a range of people from just starting out making their first investments, right through to those who had been retired for decades and those pursuing Fat-FIRE.

I learned a lot myself and it was a good ego check as initially I thought I would just be going to speak, run workshops and to work through constructive critiques of the case studies, but I ended up learning heaps, taking away a lot of lessons myself and making some beautiful friendships.

It was awesome and well worth going – that is not to say the trip was not without its challenges. Taking my wife and six month old and trying to balance ‘work / life’ was difficult on little sleep. Many of our extended family had also come to Bali from the Philippines with the intent to catch up and spend time together as a family ‘after hours’. So it was a very busy week, trying to balance the workload of the retreat, hanging out with other attendees and wanting to add value where I could, but then also see my family and give my wife a break from having the (then teething) baby all day.

I gave a talk on my journey to FIRE – basically what I did and how I deviated from the usual path, what led me to actually pull the trigger, and then why I eventually chose to ‘un-FIRE’ and get a hobby farm (pivoting back to coast-FI).

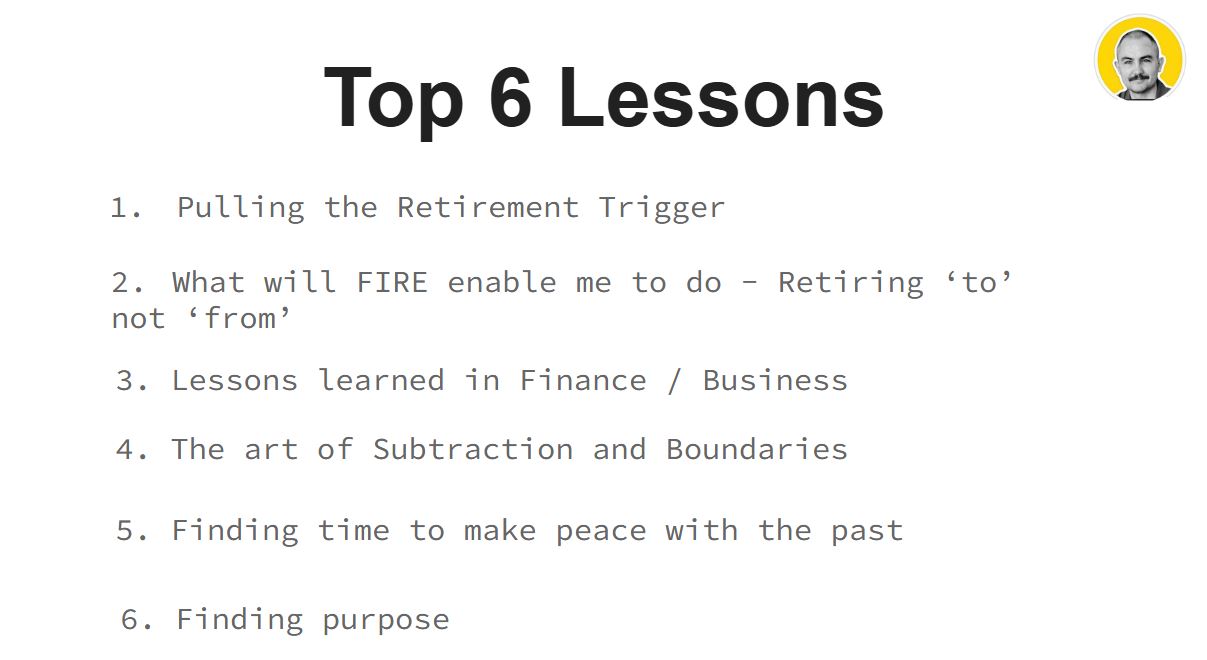

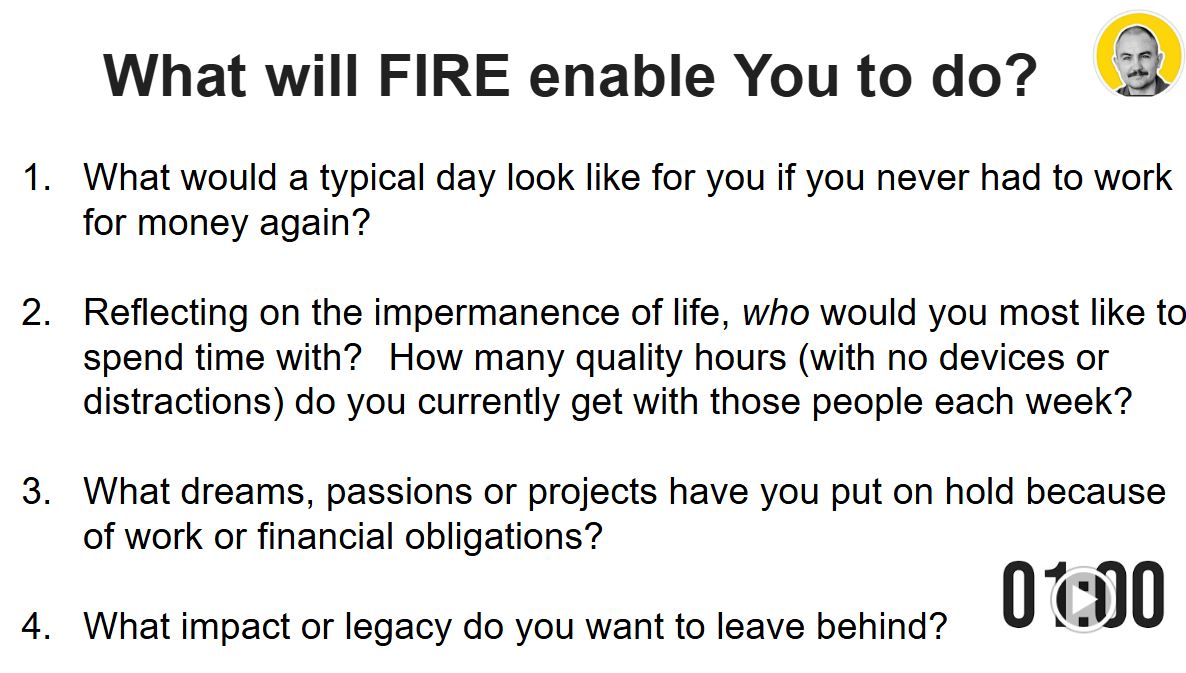

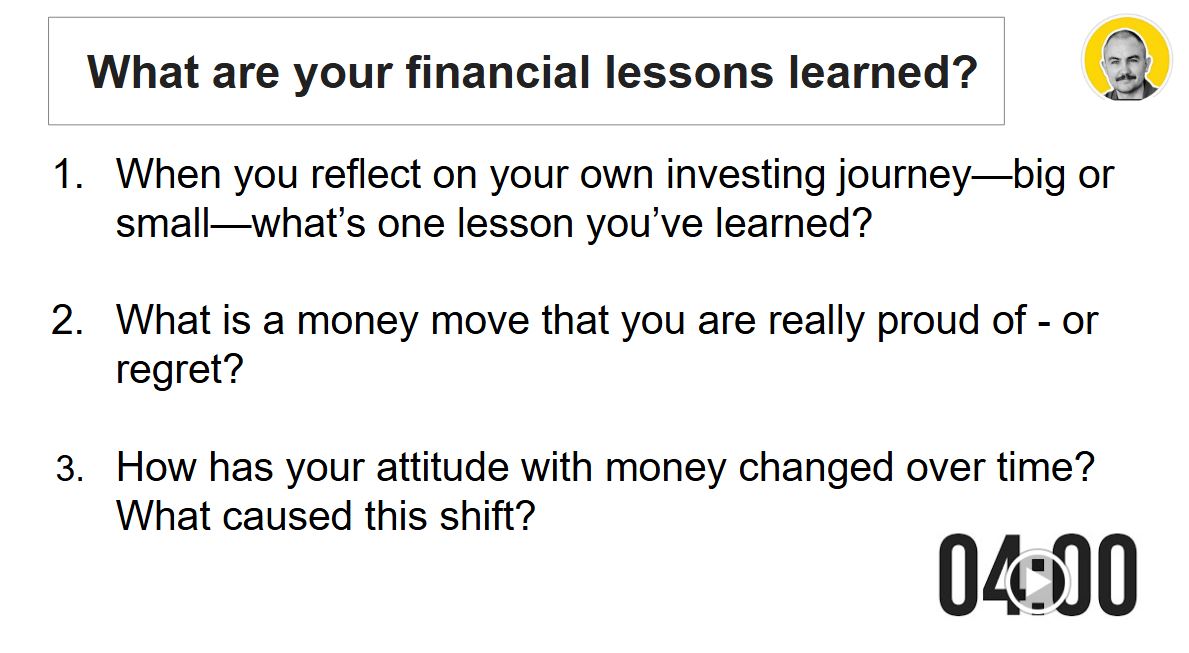

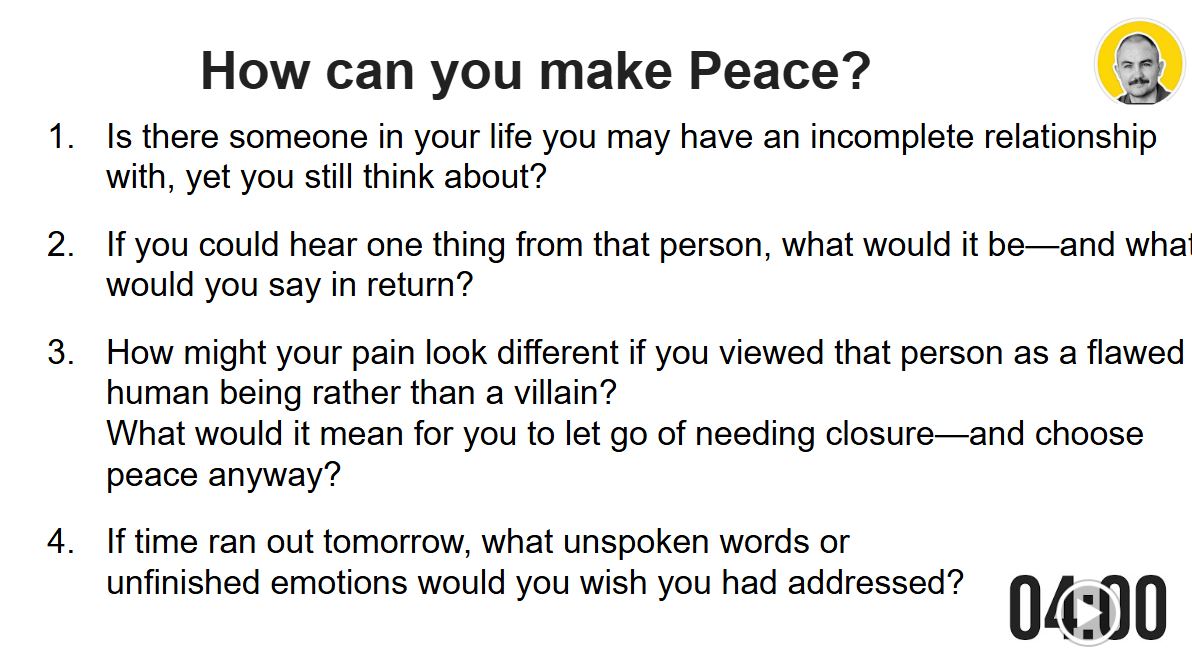

In general people are always interested to see an example or case study of someone doing FIRE, but I think the more powerful (and useful) part of my presentation for everyone was my top 6 lessons learned – basically what did and what didn’t work, with some thought provoking discussion points for group discussions. I figured I will put some screenshots of the slides here so that you can run through the reflections yourself (minus my personal examples – SORRY they are super private).

Pulling the Retirement Trigger

Retiring to something, and not from something

Lessons learned in finance and business (i.e. the boring numbers stuff)

The art of subtraction and boundaries

finding time to make peace with the past

Finding purpose – something not everyone agreed on actually being something we need to do. At the end of the day, it is OK to just enjoy life, food, art etc. You don’t need to be constantly ‘adding value’ or whatever. It was all about taking the pressure off and letting life flow naturally.

All in all, it was a great experience. I met a lot of awesome people, like Jackie Cumings-Koski (from the Catching up to FI podcast) and we even co-hosted a live podcast in front of the whole retreat which included interviewing a bunch of attendees and hearing some pretty inspirational stories. I made a lot of new friends (too many to mention) from all over the world and it was really nice to even be able to host a couple when they came to visit Australia and show them around our beautiful area in South East Queensland.

Of course, the first order of business was to get them a feed of our world famous QLD mud crab!

This year I did a small social media advertising campaign for WeMoney. WeMoney is a money tool that I have been using for years – Back in 2021 I interviewed their founder Dan Jovevski (Founder & CEO at WeMoney) for the CaptainFI Financial Independence Podcast.

The New Year campaign was a great opportunity for me to work with a trusted fintech to spread awareness about an awesome money tool that I have used for the past 5 years, and being able to earn some extra money to support my family while I was at it. The crux of the campaign is below, and you’ll be able to check it out if you follow me (or WeMoney) on social media.

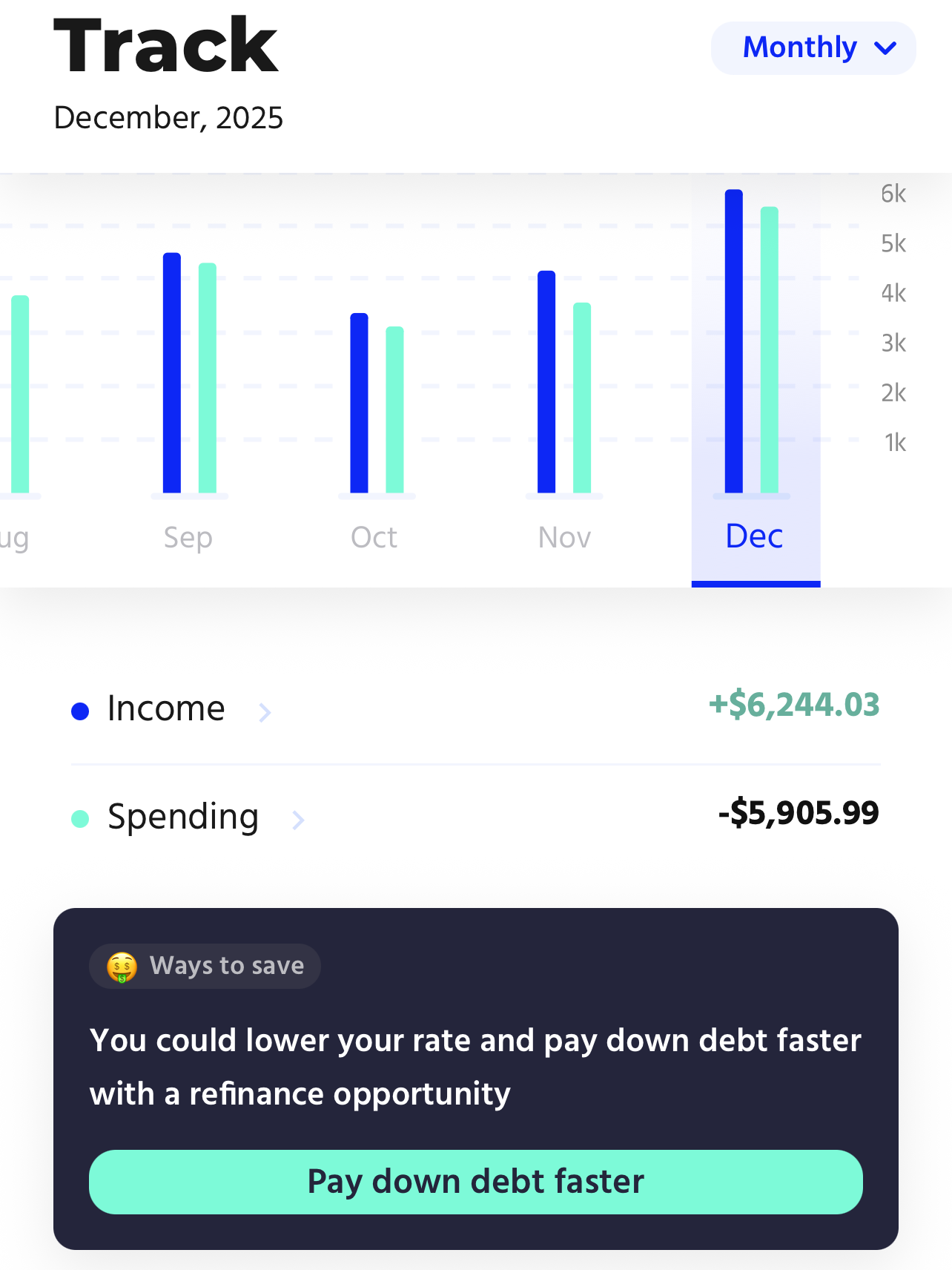

With the turn of the year, I spent a bit more time than usual reviewing where our money was actually going — partly because New Year always feels like a natural reset, partly because I knew my Quarterly net wealth review was coming up, and partly because I was running a social media advertising campaign that forced me to look at my numbers more closely.

Heading into a new year, a lot of Aussies want clarity, confidence and control over their finances. That’s exactly the mindset I brought into both the campaign and my own spending review.

Using WeMoney, I could see multiple accounts and transactions all in one place, auto-categorised, without spreadsheets or excessive manual tracking. That visibility made it easy to keep an eye on our discretionary spending, while still staying focused on our bigger goals of becoming debt free and paying off the mortgage on the farm.

What really stood out was how clearly WeMoney highlights where money is actually going. Multiple repayments, subscriptions, and day-to-day spending can quietly create overwhelm — especially around the New Year when everyone is reassessing habits and setting goals. Seeing everything together reinforces why simplicity matters.

One dashboard, one clear picture, less mental load.

From a campaign perspective, this clarity helped me speak authentically about the real value of tracking spending. When you understand your outflows, budgeting becomes less about restriction and more about structure and awareness of personal values and choices. That’s the foundation for confidence — and it’s also the first step toward tackling bigger wins like debt reduction and improved cashflow.

Captain FI, WeMoney New Year Partnership 2026From a Net Wealth point of view, our spending stayed intentional this quarter which allowed us to make additional debt repayments.

From a systems point of view, WeMoney proved itself as a practical tool for both everyday money management and highlighted a clear New Year reset message:

Clarity leads to confidence, simplicity leads to consistency, and better structure leads to better outcomes

Captain FI podcasts

I have done a couple of podcast interviews this past quarter, and also did a podcast take-over with Jackie Cummins Koski for a live podcast I co-hosted at the FI Freedom Retreat Bali

- Making Cents Podcast with Frances Cook – What its really like to quit work ‘Forever’ with CaptainFI

It’s a fantasy many of us share: what if you could retire early, walk away from your job forever, and live life on your own terms by the age of 30? Would it be all freedom and fun… or would the reality look very different?In this episode of Making Cents, I talk to Captain Fi, one of Australia’s most well-known FIRE (Financial Independence, Retire Early) bloggers. He shares what it really takes to achieve financial independence at such a young age, and whether he would actually recommend it to others.

I co-host a LIVE episode of the Catching up to FI podcast with Jackie Cumings Koski, recorded during the third annual FI Freedom Retreat in Bali hosted by Amy Minkley. This is an awesome episode with lots of powerful stories and life lessons across a wide variety of FI experience – from relatively new starters, to experienced retirees!

Check out the previous episodes of the Financial Independence Podcast on Spotify or now they have been uploaded to the CaptainFI YouTube channel!

Captain FI blog articles

I have been slowing down with the blogging while we adjust to life as parents – in case you may have missed it, my last net wealth update is below

Captain FI 2025 spending figures

As I have talked about in my last few updates, my spending has increased a lot since we bought acreage and started our family. For contex over the past few years, my total spending figures (cost of living) were roughly;

- 2020 – $30k – Renting subsidised Sydney apartment (single), working full time with lots of away trips

- 2021 – $43k – Renting subsidised Sydney apartment (single), then moved to Adelaide

- 2022 – $32k – Renting apartment 6 months, then moved back in with my Mum as her carer

- 2023 – $69k – Renting a small house with my girlfriend (our combined total household spending figure inc holidays)

- 2024 – $144k – Moved onto acreage with my wife (large expenses furnishing house, farm projects etc)

- 2025 – $119K – Projects around the property (fencing + landscaping), wifes new car, 2 x overseas trips, 2 x domestic trips

With the turn of the year, I spent a bit more time than usual reviewing where our money was actually going — partly because New Year always feels like a natural reset, partly because I knew my Quarterly net wealth review was coming up, and partly because I was running a social media advertising campaign that forced me to look at my numbers more closely.

To be honest, I am pretty miffed at how expensive some things are getting with inflation. Come Christmas shopping time, I have somehow managed to somehow spend $2,000 on groceries and totally blew the budget…. to be fair, one of those trips was to Costco and we got some stuff for the house, and we have been entertaining a lot too.

I must say, its kind of our own doing as we haven’t really been checking prices and we are in a sort of permanent state of semi sleep-deprivation at the moment, so we have decided to just grab whatever looks easy and healthy. It is sort of like that old project managers conundrum – cheap, fast, or healthy (good?) – you can only pick two!

I also had to spend a bit more than planned this month on our retaining wall project to shore up the drainage in preparation for our big summer storms, which was about $1500 spent on two truck loads of drainage gravel, pipework and a truck load of clean fill.

I do want to point out though, this unplanned spending was mostly discretionary spending, and despite inflation we still have a pretty low cost of living for what we get to enjoy. So I want to clarify I am not using ‘Inflation’ and ‘cost of living crisis’ as buzz words to not accept responsibility for our spending. We chose to spend, deliberately, and enjoyed it, and a lot of that spending went into upgrading the property which makes it worth more and ideally some of these projects (like expanding the apiary) improves our cashflow. But yes, things ARE most definitely getting more expensive, so we think it is important to make informed spending choices and continue invest to grow our disposable income.

Anyway, closing off for the year the tally for 2025 was $119k, which included a heap of projects around the property such as fencing, retaining walls, my wifes new car, our trip to Indonesia, a thermomix, some minor renovations to the house, and a whopping $15k spent on next years holidays to Tasmania and Japan!

Our baseline cost of living estimate is around $70k per year (mortgage, groceries, rates, insurance, transport, health etc), and we seem to average around $15k a year on holidays and recreation. This figure always changes around because it isn’t a budget and doesn’t dictate our spending – it’s just what we seem to spend around, and works for us. In addition to that I have been spending money on farm projects and upgrades, which I am considering ‘one off expenses’ (that should end up making us money in the long run) and I dont factor those projects into the projected cost of living.

Going forward I’m estimating around a $85k annual spending figure, which is good because it means we only really need to generate around $8k a month income to cash-flow our baseline living costs after tax. This means any surplus we can put back into the business, shares or property upgrades (such as expanding the apiary, stock, fences, shedding and equipment).

My spending reality check – WeMoney

As I mentioned I had a bit of a spending blow out, and being aware of this is half the battle – I used WeMoney as my spending “reality check”.

WeMoney is a money tool that I have been using for years – Back in 2021 I interviewed their founder Dan Jovevski (Founder & CEO at WeMoney) for the CaptainFI Financial Independence Podcast.

WeMoney is Australia’s #1 financial wellbeing app, trusted by 1.35M+ people.

Dan Jovevksi , WeMoney CEO and Founder

After being convinced to have a go, I connected up my accounts and did up a full WeMoney Review for the blog, and I have had it ticking away in the background ever since – 5 years and counting. I regularly post in the WeMoney app community feature, talking about my financial tips and tricks and giving updates on my financial journey.

What I like most about WeMoney is the simplicity. All accounts in one place, spending auto-categorised, Budget automated, and no need to manually update my old excel spreadsheets just to get a clear picture. When you’ve got multiple expenses and repayments ticking along in the background, it’s easy for things to feel messier than they really are. Seeing everything laid out in one dashboard removes a lot of that mental noise – One dashboard, one clear picture, less mental load.

That’s especially useful at the start of a new year, when the goal isn’t perfection — it’s awareness. Once you can actually see where the money is going, better decisions tend to follow naturally. Heading into a new year, it is important for us to have clarity, confidence and control over our finances – this sets the preconditions for wealth building and progress on Financial Independence.

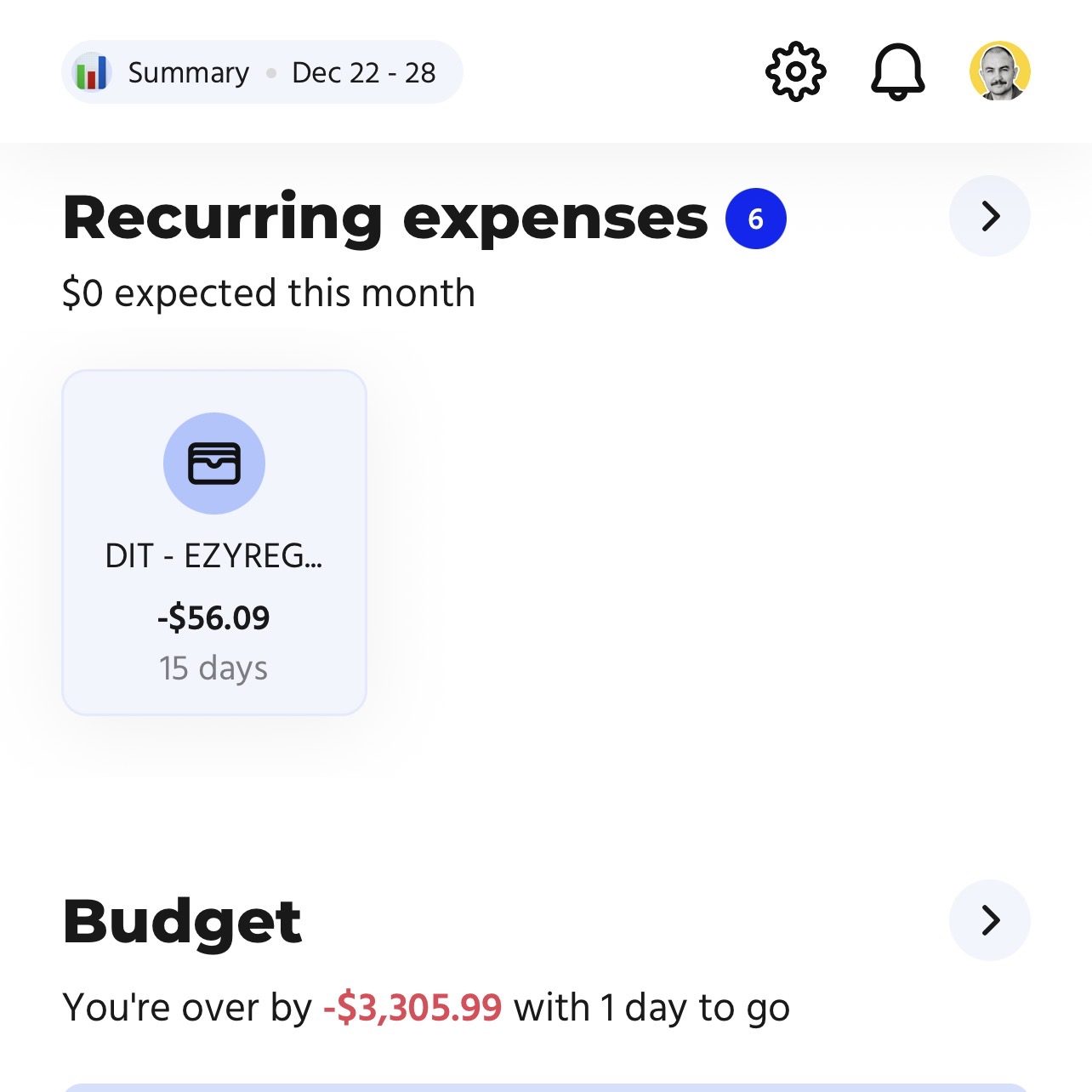

I primarily use WeMoney as a spending and Budget tracker, but over the last few years they have really improved their app, making the user interface cleaner and easier to use, adding and improving features like the Net Worth (although I still prefer the term NET WEALTH, if you are reading Dan!) tracker which automates the process by linking directly to my Pearler investing account, Bank accounts and Mortgage Accounts. I do still manually add valuations for some assets such as the properties, car and boat (or are those last two liabilities? haha).

It would be good if there was a tool in Australia to automatically value properties and then that could be linked into WeMoney, too!

Anyway, as you can see below I was slightly in the red for December, over budget by $3,306, hence I am ready for it to be Jan already so that little reminder will go away 🤣

From my net wealth perspective, nothing revolutionary really happened on the spending front this quarter — and that’s a good thing. Referring to my spending tracker shows costs stayed mostly controlled (apart from our December grocery blow out…), cashflow remained predictable, and my system did its job quietly in the background.

Tools like WeMoney don’t magically fix your finances – as demonstrated by my overspending, but they do make it much easier to stay organised and consistent, which is where most of the real progress comes from. As always, boring, repeatable and low-stress wins the race.

We do still have a few expenses that seem to fly under the WeMoney radar, because my wife doesnt use it for her accounts, and sometimes we deal in cash with Facebook Marketplace buying and selling, and small cashie jobs on the farm, but I do keep a tally of it all in my diary. So we just have the conversation to sync ourselves and then I do still do a bit of a manual comparison and reconciliation for these reviews.

Captain FI’s Investments

I don’t calculate a Net Wealth or Savings Rate Figure each month anymore, but I do try to keep a rough track of everything for these quarterly updates

My investments are split across the following areas;

The ‘FIRE’ Portfolio of Index ETFs(SOLD December 2023 to fund dream home).- Global shares – Betashares diversified high growth ETF (ASX:DHHF)

- Acreage – hobby farm in Queensland.

- Investment Property in New South Wales – Residential duplex

- My company – which runs a portfolio of content marketing websites

- Angel Investment in the investing platform Pearler

- Cash (Emergency Fund in the mortgage offset account)

NB – December 2023 I sold the ‘FIRE’ Portfolio (mix of Index ETFs) to fund my dream acreage purchase. In July 2025 I have started rebuying shares using the Betashares DHHF Diversified high growth ETF as the I believe the convenience of having an ‘all-in-one’ fund that is Australian domiciled for a incredibly small management fee of 0.19% is worth it for us.

My wife tracks her own investments separately and her investments include;

- Overseas property

- Global Shares – Betashares diversified high growth ETF (ASX:DHHF)

- Global shares index fund via her superannuation

- Cash (emergency fund)

- Shares of several family businesses including a hospital, aged care facility and school.

The ‘FIRE’ Portfolio (Exchange Traded Index Funds) – SOLD

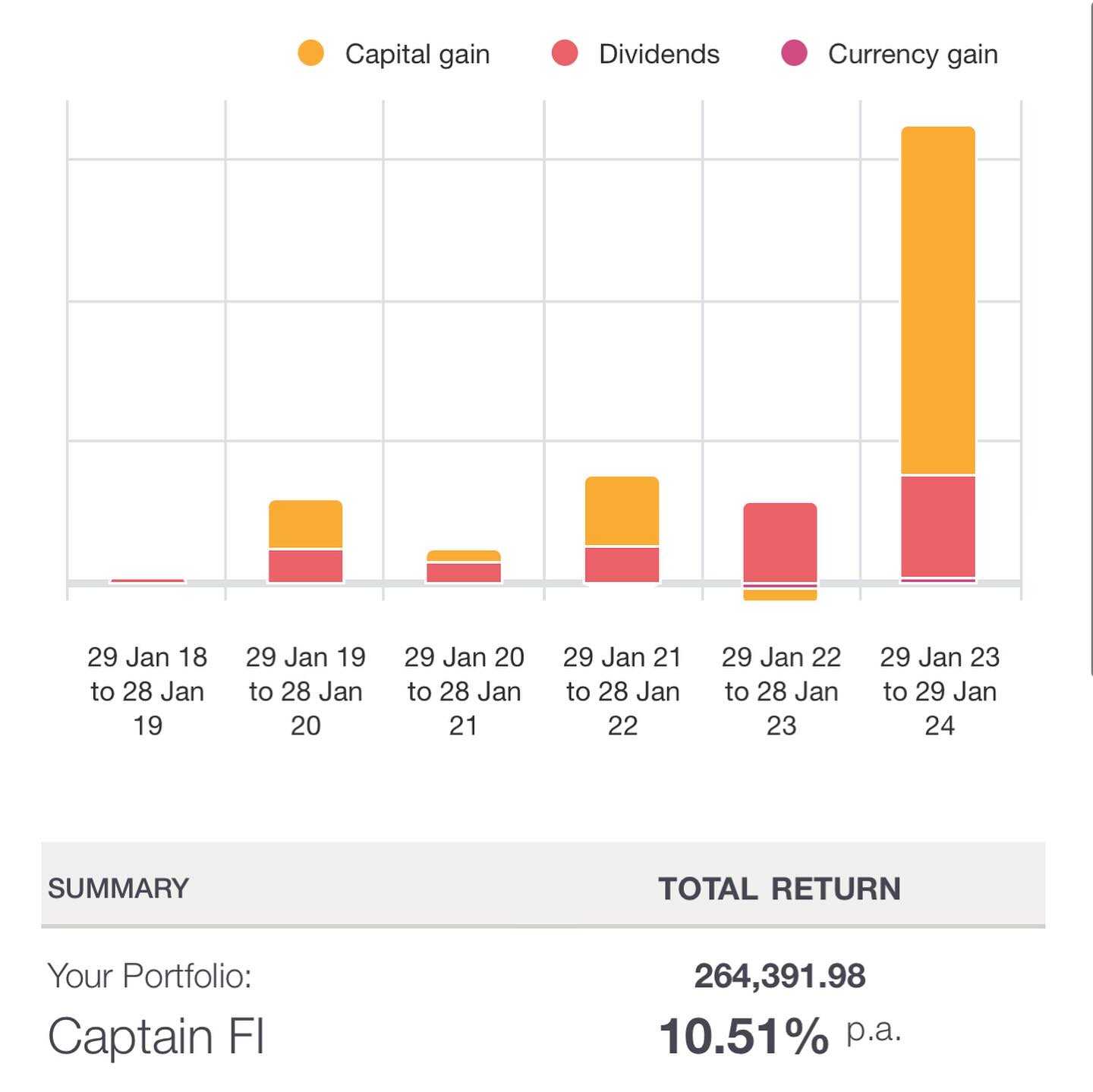

The ‘Financial Independence Retire Early’ or FIRE Portfolio was a simple, passive share portfolio started in January 2018 with the aim of growing wealth through both capital gains and tax efficient franked dividend income.

It was split between three parcels of incredibly low-fee, index-tracking Exchanged Traded Index Funds (ETFs) to achieve global share market diversification – A200 (15%), VTS (60%) and VEU (25%), and I tracked the share portfolio using Sharesight, which means my portfolio accounting and tax reports were all completely automated.

After six years of passive index fund investing where I bought shares every payday with the intent to live off dividends once I retired, I finally sold the entire portfolio in December 2023 so I could buy my forever home – a large luxury home on acreage in the SE QLD hinterland where I can hobby farm and raise my family in peace and quiet.

Cashing in the chips I sold approximately $1.7M of shares with a total annualised return of 10.51% – which was an incredible feeling. Whilst it was difficult to let go of that passive income stream and the market has continued to grow since I sold, I had achieved what I set out to do which was to become financially independent, retire early from the rat race, and buy my dream acreage to raise a family.

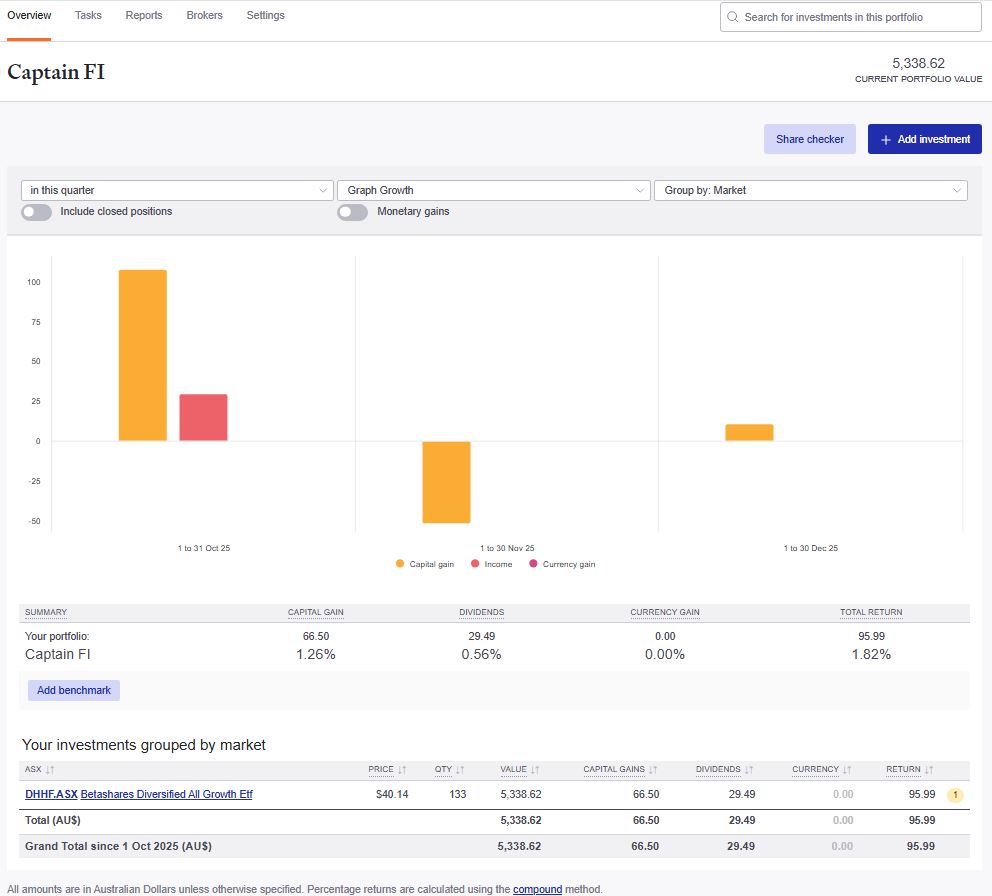

Back in July 2025 I started rebuying shares with a $5,000 purchase of DHHF. Whilst the priority at the moment is paying down the mortgage (to reduce our cost of living), I still wanted to get the snowball started – we may even be debt recycling from the mortgage to build up the share portfolio (and passive income) again quicker.

For now its just doing its thing, we may add to it but usually when we choose to invest we would do it in my wifes name anyway because of tax reasons.

Whilst the shares haven’t done much this quarter, if you look at my wifes portfolio below, you can see over the past year they have performed basically exactly in line with expectations giving her a 10.37% annualised return which she is really happy with. She basically has the same thing in her super too (using indexed global shares).

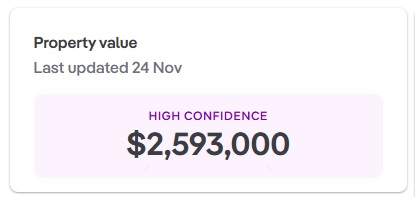

Captain FI’s Primary Place of Residence

The acreage (hobby farm) is a lifestyle choice which provides a safe place to raise my family with plenty of space, fresh air and privacy, whilst also providing an opportunity to produce an income from an appreciating asset using leverage.

To keep things simple, I just check the property value using online valuation. The current PropTrack automated online valuation estimate is $2593K, which is up $112K from the last time I checked it for the Q3 2025 net wealth update.

I owe $498K on the mortgage, with $10K in the mortgage offset account. The net mortgage position is $488K, of which I pay a ~$3600 monthly repayment.

I had previously been paying weekly and making extra repayments to get ahead on the mortgage a bit so I could refinance to a better rate, and since have now switched to monthly repayments to improve cash flow (so I can work less). Going forward the plan is to continue making the minimum repayments to rebuild the emergency fund up in the offset, and then once that is built up again to make a decision regarding debt recycling vs refinance vs property upgrades.

Debt recycling plans

I had plans to redraw equity from the mortgage to debt recycle into the Betashares DHHF ETF in order to build up the share portfolio and passive income faster. With the intent that this passive income stream could then not only cover the mortgage repayments (which would become tax deductible) but also eventually our cost of living.

You can play around online with calculators to see what effect debt recycling might have on paying off your mortgage or building a share portfolio quicker, but you just have to be comfortable exposing yourself to market risk and the fact that you are essentially using equity in your family home as collateral.

When I ran the numbers, it showed if I maxed it out and then continued to debt recycle dividends and tax savings each year, I could pay my mortgage off in 11 years. However I would have to max out my redraw which would mean increasing the repayments, and therefore I would need to make more income as the dividends alone wouldn’t cover the loan costs, essentially meaning I would be negative gearing into shares using the home loan and again be shackled to a desk and forced to bombard you with constant advertising and sponsored articles 😉

When I compared debt recycling to just not withdrawing from the loan, the ASIC moneysmart calculator showed that by just doing nothing and staying ahead on the mortgage would actually reduce the original mortgage term down to 12 years – only one year longer than the debt recycling option, with none of the market risk.

When I spoke to our financial advisor, they recommended that we just pay down our home loan over debt recycling. They offered a few reasons;

- Paying down the mortgage locks in an ‘”Equivalent grossed up (taxable) return of around 8% with zero risk”, when compared to the share markets ~10% long term average and high short term volatility.

- As we get further ahead on the mortgage, we can ask the bank to absorb the redraw and recalculate a lower minimum monthly mortgage payment which improves our cash-flow and takes the pressure off to earn more. Very handy with a young family!

- The dividend income from the debt recycled shares would not cover the cost of the loan – even when factoring the tax deduction for the loan interest, and the franking credits from the dividends. This makes it a ‘negatively geared’ strategy which would reduce our cash flow and create pressure to earn more. Not good for someone trying to retire!

- Debt recycling is more attractive for high income earners who are claiming the tax deduction for loan interest at higher tax brackets – 45c, vs us in the lowest brackets.

- Debt recycling would increase our ‘adjusted annual taxable income’ and total assessable asset pool – both of these impact our eligibility for certain family benefits such as the child care subsidy, Family Tax Benefit, and reduces how much benefit we can receive. Adjustable Taxable Income is basically your total income with no deductions allowed – Check out the ATO website for the technical definition of Adjusted Taxable Income. As we have a young family with plans for more kids, we would like to make use of any entitlements we have – which means preferencing reducing our debt over increasing income and assets.

Currently we have decided not to invest / debt recycle, and are just planning to pay down the mortgage for now. We will look into it again next year.

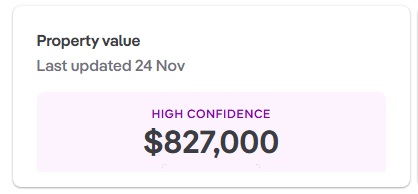

Captain FI’s Investment property

The goal of the Investment Property is to build wealth through capital growth, whilst also providing a growing source of income from the rent. I chose to use an investment property as it is independent from my other assets, I can use leverage, and I am bullish on property prices due to our current political and immigration policies and supply constraints.

The current PropTrack automated online valuation estimate is $827K, which is up $20k from the last quarters estimate, and up $60k for the year.

The property has a $528K mortgage, for an equity position of $299K and approx 66% LVR. I no longer use the offset account for the IP. Instead, I put all cashflow into my PPR offset and draw expenses for both properties from that (I then just record IP expenses to tally for tax time).

I pay a $3200 monthly repayment for the loan and collect $750 weekly in rent. Other costs (Building and landlord insurance—$1500, Council rates—$2000, water and sewage—$500, property management fee—5.5% ($2000), termite and fire alarm inspections -$300) add up to around a $5800 shortfall per year. In other words, this property costs me about $113 per week to hold, plus any maintenance issues that crop up along the way.

This means it is negatively geared (which is annoying for someone who is trying to be retired) but the interest and other costs are tax deductible, and that combined with the depreciation schedule does give me a couple of grand back at the end of the year – for a total ‘net’ loss of around $4000 per year – making the ‘actual’ holding cost closer to $75 a week.

Whilst it has cost me around $20K to hold since building it, the property valuation has gone up over four times that in that same period. Whilst no one has a crystal ball, the property market is tipped to grow between 3% to 6% per annum – which given the 66%LVR means the projected ‘cash on equity’ return would be three times that or around 9 to 18% – which means that holding leveraged property should still be better than shares (~10%) or paying off my home loan (~8%).

Over time, rents increase and this means it will also become more positively geared and provide us with a source of income – the current estimate is that the crossover point should be in 2027 after a couple more annual 5% rent increases. Currently it is rented out below market value to a single mum – a strategy to encourage a long term tenancy to reduce maintenance costs and vacancies.

If I sold the property now, with a 3% realtor commission, a few grand for staging and a conveyancing, and the current valuation I should end up with about $800k. After paying out the remaining loan I would be left with about $270K. With a cost base of around $500K to build and approx $20K claimed so far in deductions, I would have about $320K in taxable capital gains, which with the long term CGT discount would result in around $55K of actual capital gains tax payable. After paying the tax bill, I would be left with around $215k.

I don’t think $215k after tax is really attractive enough at the moment to sell the property, as we are managing alright and its only currently ‘costing us’ $4K a year in cashflow, and it will become cash-flow positive within a few years. Currently I think its worth holding onto it for the potential growth in property price. Having said that, if I used it to pay down the home loan, it would save us almost $1300 a month in mortgage repayments which is certainly attractive in terms of the time freedom that buys.

Projecting forward, If I could sell it in a couple years for $1M, there would be about $460K remaining on the investment loan. With $30K in selling fees I would be left with $510K. With $60K of deductions claimed, the cost base would be around $470K for a $530K capital gain, which with the CGT deduction would probably result in around $110K worth of capital gains tax payable – leaving me with about $400K – this will be more than our remaining home loan mortgage would be, so it would definitely be very tempting to sell it and become totally debt free, and then stash any surplus into index funds or maybe even superannuation to reduce our tax bill.

I have previously written a full separate article on the IP build if you want to know more about the process – CaptainFI’s residential property development investment.

Captain FI’s Online Business (website portfolio)

I have a small website portfolio of content and affiliate marketing sites. These make money semi-passively from display Advertising through managed ad networks such as Adsense and Mediavine, and affiliate programs such as Amazon Associates and other direct affiliate deals. The overheads are pretty low – just some software subscriptions, and I’m back to doing everything myself again to save on outsourcing costs – previously I used a bunch of virtual assistants and writers, but I’m avoiding this cost at the moment to maximise how much I can pay myself.

On one hand I want to be transparent with my investing and money, but when it comes to the websites I have to maintain privacy about SEO, traffic, contracts and cashflow as it is my business and I don’t really want to invite competitors to the space. So that’s why I don’t really publish my business income or valuations anymore. I’m thankful I have an awesome accountant who helps me through the specifics of business ownership including the nightmare that is BAS lodgements!

A while ago I decided to shift my strategy and just work on a couple of bigger sites rather than trying to spread myself too thin on a massive portfolio. Right now my personal focus is on making as much money with as little effort as possible, so I can spend my time on the farm with my family.

I’ve written a pretty detailed article here about how to make money online, and I recently published a few more articles about how to start making money online for beginners, as well as an ultimate list of blog income reports for anyone wanting a peek into the industry.

I still have a couple for sale if anyone is interested in giving this side hustle a go – price depending on how established and how much time, money and effort I have put into them. They range in age and have various backlink profiles, number of published articles, and traffic. You can check out this article on website operation if you are keen as I’ve listed all the details in there. Feel free to send me an email through the contact form or get in touch on social media if you are interested in getting started.

I originally learned these skills through the eBusiness institute over the past 5 years – I have done a pretty comprehensive review of the eBusiness institute as well as interviewed Matt and Liz Raad about this on the podcast a couple of times where we go over a huge list of frequently asked questions about online business if you want to learn more about this. They also provide some free introductory training for CaptainFI readers.

Check out these podcast episodes for more information

- Podcast | Q and A Session with Matt Raad – Part THREE

- Podcast | Q and A Session with Matt Raad – Part TWO

- Podcast | Q and A Session with Matt Raad – Part ONE

- Captain Fi Podcast | Online Business with Matt Raad

- Podcast | Digital Marketing with Richard

- Podcast | Entrepreneurship with Liz Raad

- Podcast | Digital entrepreneurs Matt and Liz Raad

I have also recently finished the Authority Hackers TASS (The Authority Site System) Course as well as the Making Sense of Affiliate Marketing course which has been a cool way to consolidate the skills I have learnt from the eBusiness Institute, and I have published a few comparison review articles such as Authority Hacker vs Making Sense of Affiliate Marketing and eBusiness Institute vs Authority Hacker which might help you choose between training providers.

Angel Investing

I made an ‘Angel Investment’ of $10,000 into the Fintech platform Pearler in 2021. Pearler was founded in 2018 and launched in 2020. Since then, Pearler has carved out a niche market in the financial independence community as one of the best investing platforms available. Since I made the investment the company has grown heaps, but there isn’t really a secondary market for these shares until Pearler either lists on the ASX or has a corporate buy out – so I can’t really get an updated official valuation.

Cash – Mojo Emergency fund

The cash emergency fund has taken a hit. I currently only have $7,000 cash in my emergency fund – down $30k from last quarter. This is WAY lower than I want, because I have been spending a lot lately and haven’t been earning as much as I have been on Paid Parental Leave.

I will be aiming to build this back up to around six months expenses or around $30k in the offset account.

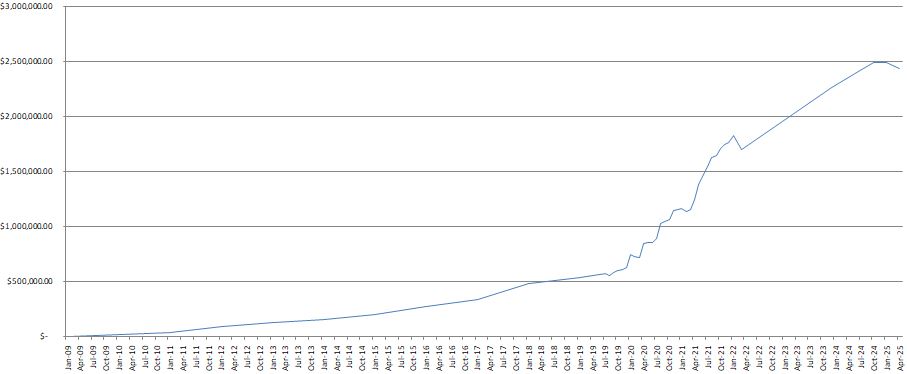

Captain FI’s Net Wealth progression

During my journey to FI I roughly documented my net wealth progression via monthly updates and a graph which was rather crudely constructed in Excel. It demonstrates the ‘somewhat exponential’ journey over my 14 year ‘working’ career. You can access the archives for my Net Worth updates here to see how it’s gone over time. Check out the graph and all the updates below to see how it has gone since the beginning.

When I FI/RE’d, I stopped putting out regular net worth updates and stopped calculating my net worth, and tried to just put out quarterly ‘updates’ but I was pretty slack. I am trying to keep up with quarterly tempo, and recently calculated my net worth after selling shares to buy my dream farm (hence the lack of data points on the graph below lately).

| Date | Net worth | Difference | Saving Rate | Notes | |

| Jan 09 | $5,000.00 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK | |

| Jan 10 | $24,000 | +$19,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 11 | $40,000 | +$16,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 12 | $92,000 | +$50,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 13 | $130,000.00 | +$38,000 | ? | Estimate NWbased on historical Super, Bank statements and assets at the time | LINK |

| Jan 14 | $161,000.00 | +$31,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 15 | $200,000.00 | +$39,000 | ? | Estimate NWbased on historical Super, Bank statements and assets at the time | LINK |

| Jan 16 | $281,000.00 | +$81,000 | ? | Estimate NWbased on historical Super, Bank statements and assets at the time | LINK |

| Jan 17 | $340,000.00 | +$59,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 18 | $482,000.00 | +$142,000 | ? | Estimate NWbased on historical Super, Bank statements and assets at the time | LINK |

| Jan 19 | $542,000.00 | +$60,000 | ? | Estimate NWbased on historical Super, Bank statements and assets at the time | LINK |

| Jul 19 | $578,900.00 | +$36,900 | 84% | Finally began tracking NW this like a proper adult. | |

| Aug 19 | $560,100.00 | -$18,800.00 (-3.2%) | 78% | Share market slight correction, Ok savings. | |

| Sep 19 | $584,744.88 | $24,644.88 | 72% | Share market rebound, savings rate not so good. | LINK |

| Oct 19 | $600,386.00 | $15,641.12 | 84% | Good saving this month. Normal salary, plus allowances, dividends from index funds, tax refund, eBay selling and was working abroad in asia where things are cheap. | LINK |

| Nov 19 | $612,917.21 | $12,531.21 | 76% | Falling short of my savings goal of 80%. Mostly domestic legs this month with higher costs. Also invested in hydroponics. | LINK |

| Dec 19 | $625,350.00 | $12,432.79 | 76% | Good savings of cash (for development) and investment, however higher spending due to Christmas period (Travel and Gifting). | LINK |

| Jan 20 | $865,212.00 | $239,862.00 | 55% | Super settlement was a HUGE boost to NW. $9K growth from stock market. Expensive month lots with lots of unexpected bills – weddings, travel, Booking flights, fines etc. | LINK |

| Feb 20 | $851,802.0 | -$16,592 (-1.9%) | 52% | Large increase in spending on myself this month, still managed to tuck away $5K to put into shares and property. Corona Virus market scare resulted in a correction and gave NW a small negative trend. Time in the market not Timing the market! Became Single again. | LINK |

| Mar 20 | $819, 354.6 | -$31,806.95 (-3.7%) | 80% | Another small step backwards in the NW due to the ‘corona crash’ in full swing. FIRE Portfolio of ETF/LICs down about 15% this month, however due to high savings rate and structure of my superannuation annuity the NW is only down 3.7%. Savings rate good at 80%, higher than usual income (with some slightly higher spending, too). Picking up shares on discount – this is the best outcome for someone in the accumulation phase with good income! | LINK |

| Apr 20 | $847,023 | +$27,668 | 85% | $11,000 in rebound of stock market capital prices alone (up 6%), plus first quarter dividends paid (heavily reduced due to banks withholding dividends). Great savings rate due to COVID-19 lock-down = no spend. Increased entrepreneurial efforts and selling down of physical possessions provided side hustle income. Two standard paychecks from flying activity; domestic day trips only so no allowances. All cash unfortunately had to go into the property development due to contract timing, I am chomping at the bit to buy some more index funds before they go back up in price too much – hence why I am selling most of my toys! | LINK |

| May 20 | $857,859 | +$10,836 | 92% | Some Great sales as I let go of my Super Sport Motorcycle, Some gym gear, expensive flying equipment and a few other various bits and bobs and invested this money. Flying still reduced, but increasing from April. The share market grew as I continued to make my fortnightly investments. I also wrote down the ‘value’ of some of my possessions (liabilities) such as my car, tools and furniture by around $10K to align them to market price (“tell him hes dreaming…!”). | LINK |

| June 20 | $858,650 | +$791 | 90% | Small Net Worth gain as I continue to declutter and simplify my life, despite being off work due to a family emergency. Share market not doing much. | LINK |

| July 20 | $888,218 | +$29,568 | 68% | Majority gain due to share market going back up, low spending due to being on the family farm and at home because of lock down. | LINK |

| Aug 20 | $1,029,293 | +$141,075 | 74% | Became a millionaire. Achieved this massive milestone I set out for myself in Dec 2019. Included unrealised gains in my property development as well as website business. Good savings rate due to not much spending, invested in Aus and total world shares. Investing in my web business. Starting to shift focus away from $$$ and more into looking after my mental health. | LINK |

| Sep 20 | S1,045,486 | +$16,193 | 60% | Officially took time off work for the rest of the year to be close and look after family during major operations. Continued to sell down physical possessions and work on digital business while at home. NW gain mainly due to valuation of websites. | LINK |

| Oct 20 | $1,064,399 | +$18,913 | 80% | Base income (retainer) and leave loading, dividend and websites provided income, as well as raiding my P2P lending capital. Significant bill for property due to design not meeting standards which effectively lowers my equity position, as well as fence being stolen. | LINK |

| Nov 20 | $1,143,433 | +$80,394 | 82% | Big gains came from share market growth (influencing both the Financial Independence share portfolio and Invested superannuation), Business gains (due to increased earnings) and a $30K boost to my annuity thanks to me logging in and checking the fine-print on the accumulation stats. I only invested around $7K. Insane that in one month, I accumulated nearly more net worth than I did in four years from 2009-2012 | LINK |

| Dec 20 | $1,152,920 | + $9,487.32 | 84% | Share market slight drop, Earnings from Business, Contract work, Selling possessions. No share market investments this month (oops! I forgot and money was tight). Invested a lot into the website business this month (way more than planned) and it is still running at a decent loss (plans to turn it cash flow positive in 3 months). | LINK |

| Jan 21 | $1,165,678 | +$12,757 | 79% | Great returns from the share market. Earnings from Business, Dividends, Flying wage, flipping items on consignment. Regular share contribution, investing in micro investing platforms, P2P lending, Investment property and big reinvestment into the business (still running at a loss) | LINK |

| Feb 21 | $1,135,272 | -$30,406 | 76% | Significant write down on property development due to council DA rejection and redesign requiring more money and creating less equity. Offset by small increase to Business value and investments. Simplified my investments and switched over to Pearler. | LINK |

| Mar 21 | $1,155,594 | +$20,322 | 71% | Continued investment into the portfolio as well as growth of investments and business. Gave my notice at work and looking for part time job at home for ‘Barista FI’ | LINK |

| Apr 21 | $1,242,220 | +$86,727 | 74% | Property development back on track | LINK |

| May 21 | $1,379,469 | +$137,248 | 72% | Massive gains in the website portfolio due to revaluation based on recent business income, big growth of superannuation due to annuity increasing (salary increment) and shares generally went up. Crypto went down by about 40% or so. | LINK |

| June 21 | $1,469,989 | +$89,757 | 41% | Quit flying role and moved to Adelaide. Great month for investments, websites producing serious income so accordingly they are valued higher. Spent a lot on furnishing the new apartment and on enjoying some more luxuries. Seeing a therapist to help deal with anxiety from leaving work. | LINK |

| July 21 | $1,543,959 | +$74,732 | N.A. | Set myself up in Adelaide. Did basically nothing for the whole month except spent time with family, relax, sleep and go to doctors appointments. Massive boost to website portfolio AdSense and affiliate incomes, as well as general share market performance. | LINK |

| Aug 21 | $1,624,116 | +$70,156 | N.A. | Relaxed again, focused on mental and physical health, and spending time with family and my partner. Big increases to spending (too afraid to calculate a ‘savings rate’) but also big increases to NW through website portfolio income growth. Finally got the slab poured on the investment property (foundation). | LINK |

| Sep 21 | 1,640,663.85 | +$16,547 | N.A. | Stocks, super etc went down, but business income from websites increased, plus business valuation increased. Property build. got to frame stage, and I also got a dog! Expenses for vet surgery well worth it. Moved into a nicer apartment | LINK |

| Oct 21 | $1,705,907 | +$65,243 | 30% | Big boost from website valuation due to securing new affiliate contracts for recurring income, shares went up nicely. No massive changes to this month. Calculated a savings rate and found myself pretty low due to spending a lot on my garden and going out quite a lot – I don’t think I will calculate this savings rate figure any more. | LINK |

| Nov 21 | $1,739,144.23 | +$33,236 | – | Great month. Relaxing (somewhat). Spent a lot of money doing ‘fun’ things like winery tours, a fine dining experience and self education. Shares moved sideways (well slightly down) but everything else went up. Building got to enclosed stage (roof, walls, windows and doors) but have had some issues with build quality and weather / covid delays. Put a $1000 deposit on the puppy. Stopped tracking Savings Rate. | LINK |

| Dec 21 | $1,764,516 | +25,372 | – | Spent nearly the whole month with family, did some work on the website portfolio. Traffic recovered from google algorithm changes. Invested $10K into Stockspot and Sixpark, $1K into ACDC, $100 into Comsec pocket and $100 into Bamboo, $260 into BTC, $4K into ETFs through pearler. Paid the $3000 balance for the puppy. | LINK |

| Jan 22 | $1,826,633 | +$62,117 | – | Stock market slightly down, Massive boost to website traffic (overall its more than doubled). Invested $10K VTS, 2K VEU through pearler, Paid for Angels cancer surgery, bought more BTC and ETH, bought a parcel of ETHI on commsec pocket. | LINK |

| Feb 22 | $1,757,210.57 | -$69,422.93 | – | Stock market down, Website business revenues down and additional spending on content and staff for business, Additional property development bills, some unexpected expenses, Wrote down the value of some of my personal property (and gave stuff away). | LINK |

| Mar 22 | $1,701,410 | – $55,799 | – | My last ‘regular’ monthly Net wealth update as I give notice at work and finish up my non-flying job. | LINK |

| Q3, 2022 | Over $2M | N.A | – | Six months of Early Retirement in Rest mode! I stopped tracking my net wealth post-FI, my dog passed away, I gave away most of my physical stuff and moved to become my mums live-in carer, met a lovely girl, bought a puppy. Had some incredible months with semi-passive website income but overall neglected the business and regular (stable) revenues decreased. | LINK |

| Q1, 2023 | Over $2M | N.A | – | One year of Early Retirement! A lot of (sad) changes, the passing of my mother and family feuding resulting in temporary homelessness, selling my ‘nursery’ of plants, and traveling overseas for a few months. Finding a new home to settle, couple of domestic trips flying to Tasmania and Queensland a couple of times, and plenty of camping and road trips within SA. Did not work much on the business at all and lost a few more contracts and had to cut staff. | LINK |

| Q2, 2023 | Over $2M | N.A | – | Getting back on top of things with podcasting and blogging more regularly. Focusing on building our ‘rich life’ and deliberately increasing spending in areas such as food, travel and convenience. Did a few interviews and went on a few podcasts. | LINK: CaptainFI Q2, 2023 Net Wealth Update |

| Q3, 2023 | Over $2M | N.A | – | Big focus on health and fitness, fixing diet and losing excess weight. Continue to sell a few websites from portfolio and focus on largest ones. Attended some FIRE events and lots of road trips | LINK: Captain FI’s Q3, 2023 Net Wealth Update |

| December 2023 | $2.26M | N.A | +$260K (21 months since last calculated) | Interim calculation due to share sales prior to purchasing property – no update published | No update published |

| Q2, 2024 | $2,417,426 | 12% – Calculated to see where we sat | +$157,426 (6 months since last calculated) | Mid year 2024 Net Wealth update. Sold shares, crypto and 5 websites, Purchased the farm in Queensland, received $250K inheritance, significant cost in setting up the property. | LINK: Captain FI’s Q2, 2024 Net wealth update |

| Q3, 2024 | $2,485,000.00 | N.A | +$67,574.00 (3 months since last calculated) | Q3 2024 update. Lots of spending on wedding and bought a boat, preparing to debt recycle. Properties saw great paper gains. | LINK: Captain FI’s Q3, 2024 Net wealth update |

| Q1, 2025 | $2,482,000.00 | N.A | -$3,000 | Q1, 2025 update. Write down of business valuation due to reducing income. PPR valuation estimate down, IP up. Slowly paying off debt. Farm life is great! | LINK: Captain FI’s Q1 2025 Net wealth update |

| Q2, 2025 | $ 2,431,487.00 | N.A. | -$ 50,513.00 | Q2, 2025 update. Property prices up, continued to pay down debt, some big spending: household help, fencing, retaining walls and chicken enclosure projects, bought second car, paid for international trip and 3 x domestic trips. | LINK: Captain FI’s Q2 2025 Net wealth update |

| Q3, 2025 | $ 2,398,487.00 | N.A | -$ 33,000.00 | NW down again! third quarter in row… My father passed away. I have been spending time with family on the farm and raising our baby, our mother in law has been staying with us for six months. I have hardly done any (paid) work at all, mostly household / dad / hobby farm stuff. Got our flock of chickens and getting lots of “free” eggs… Made first shares investment for years (DHHF all in one fund). Property prices steady – switched back to monthly repayments to improve cash flow, bought some more upgrades for the farm. Paid the rates, rego (cars, trailers, boat), insurance, tax bills, and some BIG electricity bills ($$$!). Considering selling the investment property to pay down home loan and simplify finances. Probably should work more… | LINK: Captain FI’s Q3 2025 Net wealth update |

| Q4, 2025 | $2,433,746 | N.A | $35,259 | Property price valuations increased, driving NW higher. Fair bit of spending including pre paying $15K for two holidays in the new year, total spend for 2025 coming in at $119K, $44K above total yearly budget due to buying new car, tractor, farm projects and travel. |

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.