CaptainFI April Update

Gee, its May already hey. The nights are getting a bit fresh here in Sydney as we see the annual northward march of the Australian high pressure belt. This normally blocks those snaggle-toothed cold fronts from down south (Antarctica?) from reaching us. Generally the weather has been great but the occasional cold front has reached us braining chilly and showery weather – and some challenging flying conditions.

I have spent a good portion of time at home, making hay while the sun shines studying work related topics as well as writing a few quality articles of the blog. Check out my reviews on Does barefoot work, SelfWealth and ShareSight for some good gouge!

I started a new ‘folder’ of articles called ‘Book Reviews‘ as I transition my longer book reviews from the Captains Library into their own dedicated articles. There is a couple in there already, and I will slowly work my way through the almost 100 book recommendations in the library over time.

Speaking of which, the fancy widget on my website development tool tells me that the blog has now reached 68 published articles, but with a sneaky 5 scheduled for posting and almost 36 drafts in various forms of readiness, this number should rapidly run north of 100 within the years end!

There has been some changes to both the FIRE portfolio and my life in general as I try to simplify my life and follow the lessons taught in The Ancient Art of Stoic Joy. I am becoming more and more satisfied with less and this is helping to reassure me that Financial Independence is so close I can taste it! I can feel a sense of chronic stress slowly melting away.

Saving rate

Cash flow for April was A+. I earned good money and spent bugger all of it since most of my time has been spent at home studying on work for an upcoming yearly assessment (which I find very nerve wracking!). I focused on chowing through what I had in the fridge, freezer and cupboards and trading stuff with neighbours rather than buying more groceries 🤣 The net result is a 85% savings rate, well and truly smashing my goal of 80%!

Income

Two standard paychecks from my flying wage however due to reduced flying on a few day only domestic routes only I received no allowances. I am very thankful for my salary and the opportunity to still be working.

I redoubled my efforts on eBay/Gumtree/FBMP and ramped up my decluttering sales this month. This provided almost $1000 of income. I also just gave away and donated a heap of good stuff which I just to be honest couldn’t be bothered trying to sell myself.

The FIRE portfolio paid in a reduced first quarter dividend.

Website Portfolio income is still zero as I have turned adds off to improve user experience. Due to affiliate links going in the background I saved $28.50 in brokerage thanks to a SelfWealth referral from one of the readers.

Spending

Spending is well and truly reigned in for April. I have discovered a number of wonderful resources in my community which have helped cut spending. First of all (despite COVID-19 and whilst maintaining social distancing) I have massively ramped up my community involvement.

I have continued giving away and trading foods like home grown produce, home-brew cider and beers, seedlings, established herb plants, kombucha tea, kombucha Scoby’s, sourdough bread loaves and sourdough starter cultures. Most if not all of this stuff costs me next to nothing apart from a small amount of time and ingredients. In return, I have received a number of awesome home made foods, baked goods and snacks which have cut down my own grocery spending.

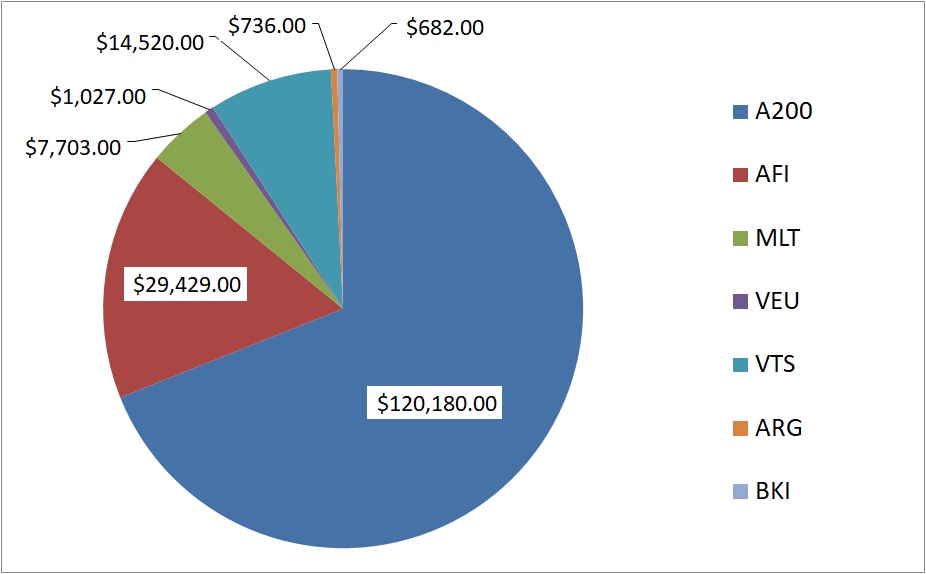

Get FIRE Portfolio

The FIRE portfolo is up 6% or about $11,000 in capital value in April as the stocks rebound in price post Corona virus COVID-19 hysteria. Thankfully we are also seeing flour, toilet-paper and pasta return to our supermarket shelves, too (carbohydrate and crap lovers rejoice!). Touch wood though, because the market will probably remain volatile for a while now (making these NW snapshots probably somewhat misleading).

A reduced first quarter dividend has been paid by most of my holdings, which unfortunately I think was something like 50% of what it should have been due to the requirement for banks and other companies to reduce dividends in order to withhold capital to weather the economic downturn and rely less on government assistance. I figure this is fair enough, and provided dividends go back to normal over the remainder of the year I’ll be happy enough.

Investing decisions

This month I unfortunately needed to throw my cash fire-hose into the property development of IP1 (rental unit build). I am absolutely frustrated that I have not been able to stick to my investing strategy of buying index funds every fortnight but unfortunately without extra cash to finance the IP1 build, it will just cost me more money in the long run.

I noticed that IVV and VAS were both experiencing higher percentage gains than VTS and A200 – so I decided to roll them over into A200. I had some free trades from SelfWealth so I didn’t have to pay brokerage.

Whilst I freely admit this sounds quite like portfolio fiddling and trying to time the market, I had been wanting to simplify my FIRE portfolio for some time

Property

All of my disposable cash was directed towards IP1 build in April, tucking away nearly $10K into the various development fund accounts. Due to COVID-19 we are experiencing difficulty with financing as banks are increasingly playing bullshit games with us as they try to consolidate their loan sheets in ‘uncertain’ times.

The Project manager is still happy, expecting to pay out another lump sum shortly and get rid of this annoying cash surplus that has been plaguing my balance books with terrible returns and slowly eroding away thanks to the wealth destroying effect of inflation. Whilst only 5% of the portfolio, it still needs to go. I don’t need a cash cushion at the moment as I have a secure job contract and my emergency fund is sufficient.

Retirement

Click here to see what my Transition to retirement financial planning process looks like

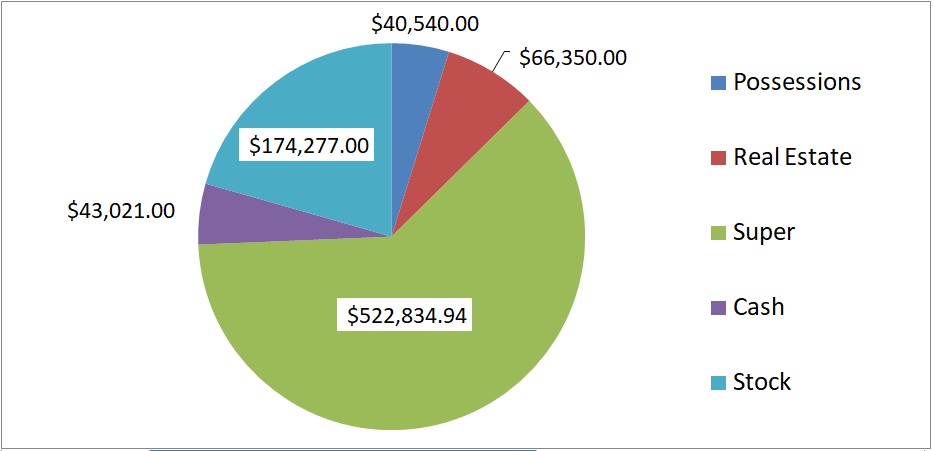

Net worth

I was pretty stoked to keep reducing my physical possessions (Car, motorbike, trailer, tools etc) this month, with them now making up only 4.8% of my net worth. Whilst this might sound a little cheeky and some rationalise you shouldn’t include these, because I am liquidating a good chunk of them I think its worth to leave it in for now. Once it gets below 2% of the total portfolio I will probably just drop the sector all together!

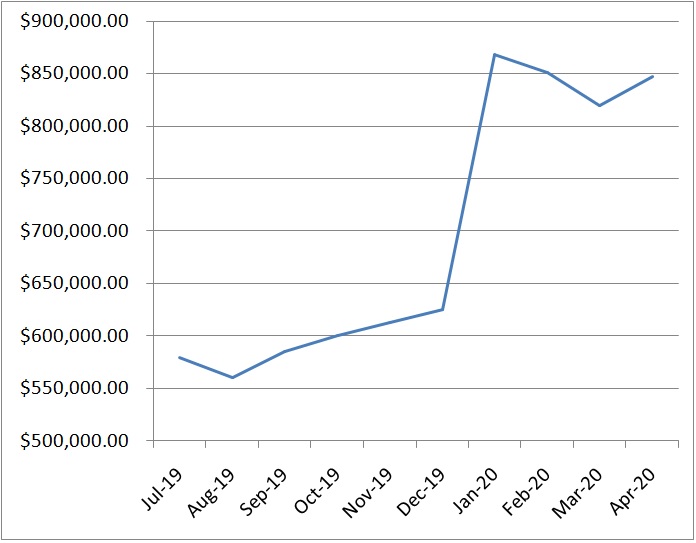

Net Worth table

| Date | Net worth | Difference | Saving Rate | Notes | |

| Jul 19 | $578,900.00 | | 84% | Finally began tracking this like a proper adult. | |

| Aug 19 | $560,100.00 | -$18,800.00 (-3.2%) | 78% | Share market slight correction, Ok savings. | |

| Sep 19 | $584,744.88 | $24,644.88 | 72% | Share market rebound, savings rate not so good. | LINK |

| Oct 19 | $600,386.00 | $15,641.12 | 84% | Good saving this month. Normal salary, plus allowances, dividends from index funds, tax refund, eBay selling and was working abroad in asia where things are cheap. | LINK |

| Nov 19 | $612,917.21 | $12,531.21 | 76% | Falling short of my savings goal of 80%. Mostly domestic legs this month with higher costs. Also invested in hydroponics. | LINK |

| Dec 19 | $625,350.00 | $12,432.79 | 76% | Good savings of cash (for development) and investment, however higher spending due to Christmas period (Travel and Gifting). | LINK |

| Jan 20 | $865,212.00 | $239,862.00 | 55% | Super settlement was a HUGE boost to NW. $9K growth from stock market. Expensive month lots with lots of unexpected bills – weddings, travel, Booking flights, fines etc. | LINK |

| Feb 20 | $851,802.0 | -$16,592 (-1.9%) | 52% | Large increase in spending on myself this month, still managed to tuck away $5K to put into shares and property. Corona Virus market scare resulted in a correction and gave NW a small negative trend. Time in the market not Timing the market! | LINK |

| Mar 20 | $819, 354.6 | -$31,806.95 (-3.7%) | 80% | Another small step backwards in the NW due to the ‘market crash’ in full swing. FIRE Portfolio of ETF/LICs down about 15% this month, however due to high savings rate and structure of my superannuation annuity (guarantee – thank you unions!) the NW is only down 3.7%. Savings rate good at 80%, higher than usual income (with some slightly higher spending, too). Picking up shares on discount – this is the best outcome for someone in the accumulation phase with good income! | LINK |

| Apr 20 | $847,023 | +$27,668 | 85% | $11,000 in rebound of stock market capital prices alone (up 6%), plus first quarter dividends paid (heavily reduced due to banks withholding dividends). Great savings rate due to COVID-19 lock-down = no spend. Increased entrepreneurial efforts and selling down of physical possessions provided side hustle income. Two standard paychecks from flying activity; domestic day trips only so no allowances. All cash unfortunately had to go into the property development due to contract timing, I am chomping at the bit to buy some more index funds before they go back up in price too much – hence why I am selling most of my toys! |

Get Financial Independence!

What did you think of the update? Let me know in the comments below!

Monthly question from the Captain

I have a question I want to ask everyone regarding portfolio construction. Do you invest in both ETFs or LICs? Or just one? I would love to hear your opinion on whether you go for LICs for dividend smoothing tax efficiency, or whether you go for the raw power and simplicity of ETFs. Which one do you think is better for Financial Independence? I value simplicity, and so have been thinking of adopting a purely ETF based approach with the A200/VTS/VEU split, but can still see the value of buying the LICs at a discount!

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

How did you get so much super!? I saw on Instagram feed you are only 28

G’day OzFIRE. Sorry this comment must have snuck under the radar. Thanks for the compliment and the question mate! So I will start by saying that I have a pretty decent super package for work, and actually this kind of makes up for my actual pay not being as high as some of my peers in the industry; overall I think its pretty even. This was a deliberate decision I made then applying for the job. I have also worked many different jobs and roles since I was 15 (supermarket stacking initially), and have always tried to contribute more or ‘max out’ my super. Last year I also won a legal battle with HR regarding underpayment of wage and super, and received a small lump sum and massive super contribution – this boosted the value of my super significantly. My Super consists of a lump sum benefit and an annuity (or income guarantee). Whilst I will get the lump sum and can do with it what I wish (most people seem to pay off their house, buy a new car, go on holiday and give some to their kids), the annuity component is designed to support me for the rest of my life. I did the maths behind going 100% into a lump sum style super scheme, but I figured I will live past 75 and so the annuity would be a better option in the long run. PS I am also now 29! Cheers

Thanks Captain Fi – I just discovered your podcast and blog and enjoy the way your present. I also used your referral code for Selfwealth 🙂

G’day there Cokox, thanks for the feedback! SelfWealth has been great for me so far, so welcome to the cult!