Hello everyone and welcome to 2020! I am back at work and flying having completed many of my annual refresher and check sims (simulator sessions) and ready for another big year of earning and investing towards reaching Financial Independence!

January

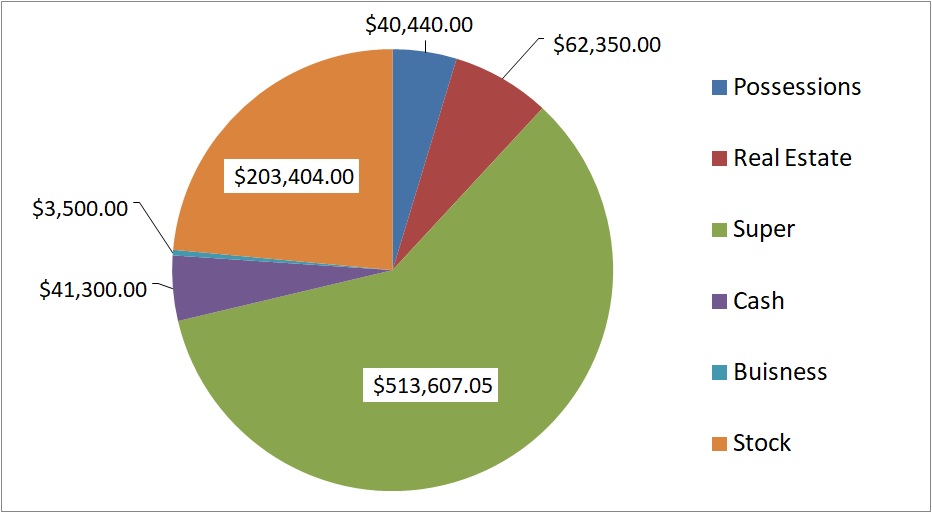

Well January brings some huge and unexpected gains to the net worth due to a Superannuation settlement / revaluation. The net worth is boosted by almost $240,000 this month. This, combined with the investment decisions in shares and property has also moved my asset allocations into a much nicer proportion (for example, cash now being under 5% of my portfolio finally). The vast majority of my net worth (about 60%) is invested in the tax sheltered environment of Superannuation thanks to over 11 years of concessional contributions to my cap. With my later retirement (age 65+) taken care of, all I really have to worry about is my early retirement number now.

Saving rate

Cash flow for January was interesting. It was a fairly expensive month for me, since I got whacked with a few unexpected expenses (including one traffic fine due to my own stupidity). This unfortunately kept the savings rate pretty low at a measly 55%, even despite Vanguard paying me some substantial dividends.

Income

Two standard paychecks from my flying wage plus $1,224.70 and $199.82 in dividends from Vanguard. A sizeable settlement to the retirement superannuation account (which is not considered in the savings rate).

Spending

January incurred some unexpected spending. I got whacked with a pretty shocking traffic fine (in the thousands of dollars range) which I am annoyed at myself for getting however it was out of my control so there was nothing I could do except just pay the darn fine.

I got the great news of being asked to be a Groomsmen for one of my best mates (it seems more and more of your friends get married the deeper you progress into your twenties!) It will be a great night, but I have spent just over $600 on getting fitted for formal wear – which was an unexpected cost and is a pretty huge dent in the budget I am not going to lie. Especially given I normally spend less than $100 a month on discretionary spending / luxury expenses – But it will be worth it to be there supporting my mate!

I also purchased tickets to fly interstate to another, different wedding later on in the year, which was another $580 that came out of the account.

And sadly, due to a HR stuff-up I was overpaid approximately a thousand dollars last year. The first I found out about this was when one of my paychecks was smaller than usual – the company had deducted this off my first January pay stub.

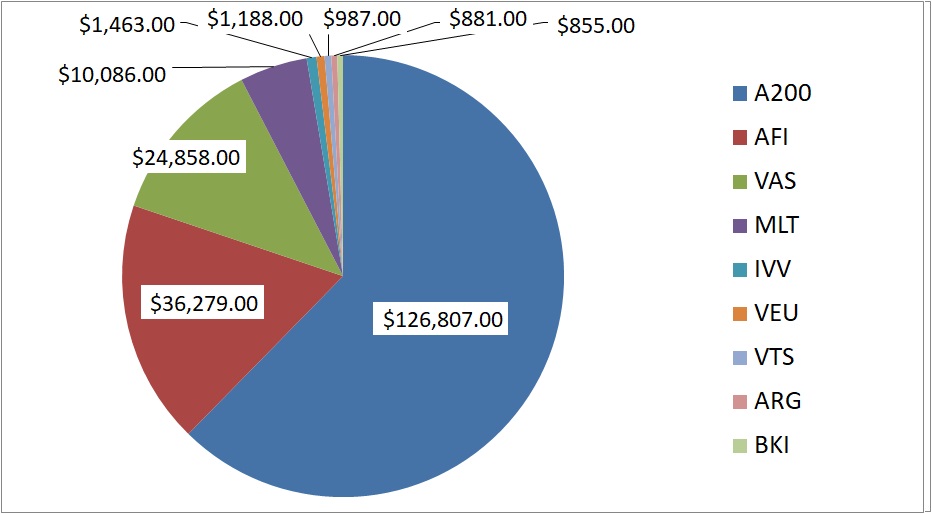

Get FIRE Portfolio

The Get FIRE portfolio is still heavily weighted to Australian stocks due to the delicious franking credits. I have found that some Australian LICs have been trading at a discount which is why I have been loading up on them for the past few months. I will likely be looking to shift my purchase horizon internationally over 2020, and looking to boost my holdings of VTS and VEU. I am not 100% sure but I am currently thinking I may sell the holdings of ARG, BKI and IVV and put the proceeds towards these international purchases. This is because they feel like ‘unnecessary’ double ups (kind of like how I have A200 and VAS at the same time).

Investing decisions

Unfortunately there wasn’t a great amount of money left over from my monthly cash flow to chuck into investments this month. This left me with only enough to purchase $2811 worth of Milton stock. I chose to invest in Milton Investment Corporation due to it being 3.5% under its Net Tradable Assets (NTA) at the time of purchase.

Property

This month a whopping $52,000 went across the lawyers and trusts to fund IP1. This month finds us pouring over the build contracts and removing all the ridiculous clauses which get snuck in by the builders – such as a 20% interest rate for late payments and them deleting landscaping requirements. Although this is a pain and it feels like progress is slow, contracting this out to a project manager and specialists is the smart choice as I am a novice real estate investor. Fixing these clauses and expectations now will lead to a much smoother build and save money in the long term.

Retirement

Click here to see what my Transition to retirement financial planning process looks like

Net worth

Net Worth table

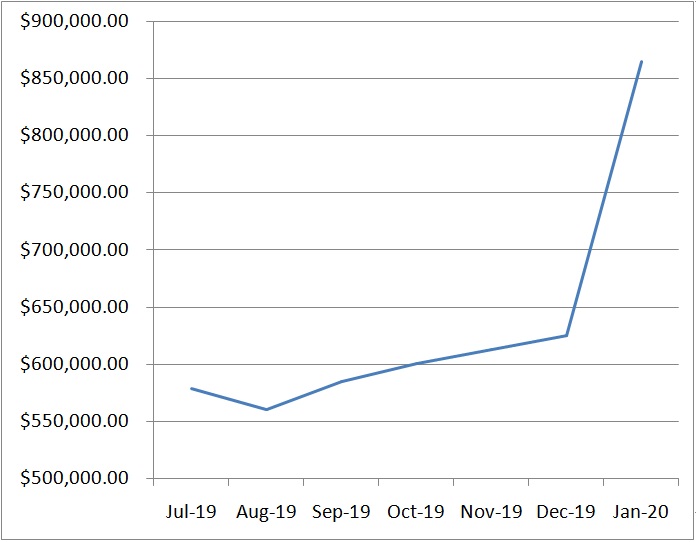

| Date | Net worth | Difference | Saving Rate | Notes | |

| Jul 19 | $578,900.00 | 84% | Finally began tracking this like a proper adult. | ||

| Aug 19 | $560,100.00 | -$18,800.00 | 78% | Share market slight correction, Ok savings. | |

| Sep 19 | $584,744.88 | $24,644.88 | 72% | Share market rebound, savings rate not so good. | LINK |

| Oct 19 | $600,386.00 | $15,641.12 | 84% | Good saving this month. Normal salary, plus allowances, dividends from index funds, tax refund, eBay selling and was working abroad in asia where things are cheap. | LINK |

| Nov 19 | $612,917.21 | $12,531.21 | 76% | Falling short of my savings goal of 80%. Mostly domestic legs this month with higher costs. Also invested in hydroponics. | LINK |

| Dec 19 | $625,350.00 | $12,432.79 | 76% | Good savings of cash (for development) and investment, however higher spending due to Christmas period (Travel and Gifting). | LINK |

| Jan 20 | $865,212.00 | $239,862.00 | 55% | Super settlement was a HUGE boost to NW. $9K growth from stock market. Expensive month lots with lots of unexpected bills – weddings, travel, Booking flights, fines etc. |

Get Financial Independence!

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Hello Captain FI,

Great website and podcast. Well done mate! Stumble across your site via Aussie firebug Facebook group and I am hocked. Thanks for sharing your knowledge. Quick question? Are you nearly fire? I heard you mention on your podcast that would estimate you would need $500k-$1m outside super. Looking at your network, it looks like your kind of their..: what’s the plan now? Do you plan to continue to build your nest egg or ease of a bit. Also do you track your passive income? (Dividends, rental income..etc?)

G’day Aly – Thanks for the question. At the moment a huge chunk of my NW is in superannuation, which means I cant access it for some time. I plan to draw down on my investments outside super when I FIRE until I can get the super nest egg eventually. Rather than think in terms of NW and how much I have invested, I like to think in terms of cashflow or passive income. In terms of a leanFIRE for just me, I’m looking at about $1700 a month or somewhere around $300-350K worth of ETFs/equity which I would draw down at around 7% over 25-30 years (of course supplementing with part time work and passion projects). Although when thinking of kids, that leanFIRE target goal becomes a fair bit higher at nearly $3000 per month or around $550-600K at that same 7% draw down rate. I know it sounds like I am randomly throwing different numbers out there, but its a bit of a tricky subject. Once you hit FIRE, quitting your job is also a massive step and not as easy as it sounds. Personally my first goal is to achieve that 600K mark or $2900 per month in passive income from the ETFs and rental portfolios (and yep I am quite close to my ‘single leanFIRE’ number at the moment), and I think I will potentially spend a little bit more time flying full time to bolster that nest egg and provide a little bit more fat or ‘factor of safety’ before I fully FIRE. Yes I have been tracking Passive income – that’s one of my unhealthy obsessions haha! Passive income sources includes dividends (future rental yield but I have none atm), income from the web portfolio sites and a few other small bits and pieces here and there, which fluctuates but comes to around $2000 per month at the moment.

Hey Aly,

Yeah my figure bounces around a little bit depending on which strategy you want to talk about. Conventional FIRE without using a tax leveraged investment account (401k, IRA, superannuation) tends to focus on the 4% rule. My leanFIRE number is about $1600-1700 per month which works out around the half a mil mark. That figure doesn’t factor kids, and so a more realistic number for fatFIRE would seem to add on another $300k to that figure 😳 all is not lost though, as I wrote about in some of my net worth updates and my retirement planning article – due to Superannuation. The company I work for allows me to invest in an annuity for when I retire. I’ve been contributing wayyy more than I have to into that account ever since I started earning, so my ‘super’ balance makes up a huge chunk of my net worth. The trick here is my conventional taxed investment account doesn’t need to follow the 4% rule and last forever, it just needs to last me until I can access my superannuation annuity 👌 I’ve played with the numbers, and a 7% to 8% draw down is feasible over my time frame. For leanFIRE, that means around a $300k outside super and my current super balance should cut it (supplemented with the old age pension). I’m not fully confident relying on the pension, so to boost my income from the annuity I’ll keep contributing more while I keep on the path to FIRE, and to be honest even when I fire I’ll still plan to make contributions as it’s so tax effective. I also want a family and lots of kids so I eventually need fatFIRE! 😂 that increased draw down rate means a $500k conventional taxed portfolio would suffice. I write about this in more detail in my monthly portfolio updates but yeah I’m probably 18 months to two years away from achieving that. Realistically though, side hustles will continue to supplement income as I love projects which should help the bottom line and reduce risk. Sorry for all the bouncing around with numbers getting thrown out there, but as you can appreciate there are many factors at play!

Damn, nice work!

I don’t have much to add, I came across your website via Aussie Firebug. I’m always looking for other finance blogs to checkout because I enjoy reading about people’s monthly progression towards FIRE and the different ways their achieving it.

I definitely get the addiction with tracking passive income, it’s my favorite metric for measuring my progress towards financial independence and comparing it with my annual living expenses. I’ve mostly been in camp LIC for Australian exposure with AFI, MLT and BKI, and for international VGS. (75/25 split)

However I’ve been building up my allocation to VAS since July last year, which might seem a bit like doubling up but I’ve slowly been coming around to owning the whole index as part of the portfolio. It also spreads out the distributions a bit more throughout the year.

Anyhow, I’ll have to checkout some of the podcasts on here after work.

Cheers.

Great work Scott, I find myself bouncing between Camp LIC and Camp ETF quite a bit haha – I think they are both pretty good! Can’t beat that juicy fully franked dividend, but part of me somehow thinks its just easier (and somewhat safer with diversification) to passively own an ETF. I don’t have a good answer, but perhaps my desire for the franked dividend means my portfolio splits (VAS/VTS/VEU) will be a little higher weighted toward Aussie stocks as I hold some of the aussie LICs too. I don’t think you can really go too wrong on this regard – although I am a terrible person to be talking about portfolio splits as I seem to just randomly buy whatever is on special at the time 😅

G’day Capn,

Just wondering if you could touch on the large boost in Super? By ‘revaluation’ I’m assuming you’re running a SMSF holding property which has been revalued?

Thanks for all of the info!

Hey Jacob, this was due to a few reasons. Firstly the DB was increased as my backpay increased my salary, and then my financial advisor recommended valuing it as would a like-for-like annuity policy. Currently it is valued at 25x yearly earnings (indexed to inflation).