Show notes

- Pat the Shufflers LIC discount estimator

- The trinity study

- Captain FI’s Financial Independence Investment Strategy original article

Captain FI’s Investments

ETFs

- Betashares Australian top 200 index fund (ASX:A200) MER = .07%

- Vanguard Australian shares top 300 (ASX:VAS) MER = .10%

- Vanguard Total US Market (ASX:VTS) MER =.04%

- Blackrock iShares S&P 500 ETF Total US market (ASX:IVV) MER = .04%

- Vanguard Total world ex US (VAS:VEU) MER = .09%

LICs

- Australian Foundation Investment Company (ASX:AFI) MER = .14%

- Milton investment corporation (ASX:MLT) MER = .12%

- Argo Investments (ASX:ARG) MER = .16%

- Brickworks investments (ASX:BKI) MER = .17%

Readings

- The Intelligent investor: Benjamin Graham

- Rich Dad Poor Dad: Robert Kiyosaki

- The Barefoot Investor: Scott Pape

- Total Money Makeover: Dave Ramsay

- Predictably irrational: Dan Ariely

- Uncommon Sense: Michael Kemp

- Creating real wealth: Michael Kemp

Awesome FI Bloggers

- The Aussie Firebug

- The Mad FIentist

- Mr Money Mustache

Transcript

Ladies and Gentlemen, this is your Captain speaking welcome aboard Captain FI the financial independence podcast Podcast where I open the cockpit to some of the best and brightest in personal finance as well as those who breached or are on their way to financial independence before we get started today remember anything on the show is provided for general information only and should not be taken as constituting a professional advice you should always do your own research when making any financial decision

G’day everyone Captain FI here checking in with episode number two – my financial independence investment strategy. After releasing episode number one I had a lot of questions from the listeners asking to speak a little bit more about my personal circumstance and journey towards fire and specifically my investment strategy

so first of all as we spoke about on the last episode its super important that your pursuit of financial independence that you set yourself some goals and educate yourself, then decide on an investment strategy. That’s really gonna help you stay accountable; remember smart investors educate themselves, regularly read and set about to investing regularly.

For me personally I’m the kind of person I really need to understand why I (why I’m doing something and how it works) Maybe because my background is, well I trained professionally as an Aerospace engineer and I actually really love that industry and I hope the one day continue to work in the Aerospace or the space sector part time. For a lot of engineers they have to understand why – why am I doing something, why does this machine operate the way it does, why does the system operate the way it does and once they understand it’s like a lightbulb moment the penny drops. Then they’re happy to to work on that system or or keep improving that system. For me it’s the same with flying I really have to understand how an aircraft works and how its systems works before I can fly it, and thankfully having a bit of a technical background in Aerospace engineering that really helped me.

When it comes to investing I really need to know the ‘why of FI’ – Why am I doing it? My goal to reaching financial independence for some time has really been with the idea of starting a family I want to get to a point where I’ve got enough passive income coming in where in it I can afford to buy my own block of land in the country and I can raise my kids. So you do some reading about how it all works and a great start is the Trinity study which is a paper showing the maths behind retirement draw down rates. This study led to a pretty widely accepted rule of thumb within the fire community of 4% withdrawal rate being a safe draw-down rate.

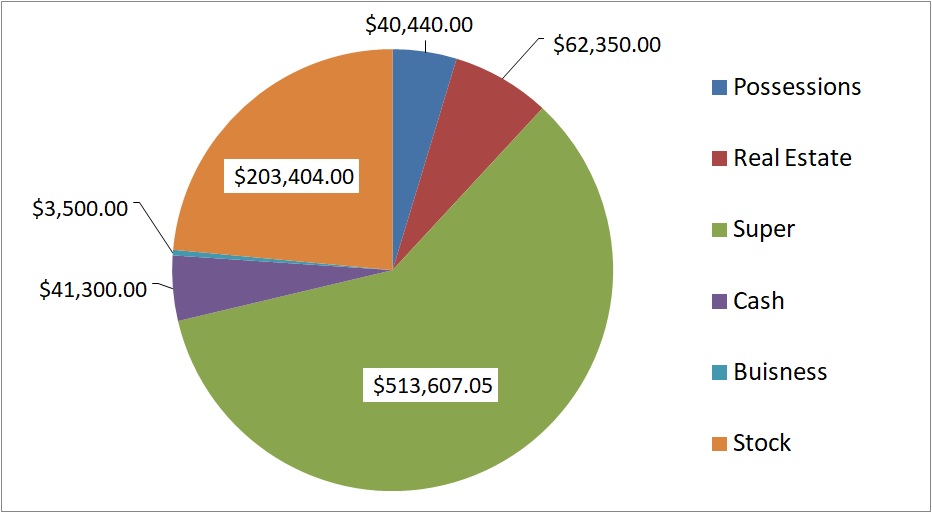

so based on my projected spending in retirement and the four percent rule, I would really need to buy and hold a portfolio of around $600,000 of ETFs just for myself – that’s based off a spending of around $24,000 per year and not an increasing up to the $1,000,000 mark of ETFs with family. You can imagine raising some kids I feel will be more expensive and so I’m budging a projected spend increase of up to $40,000 per year

There’s a rough number start with – ok why I want to be financially independent I don’t want to be locked down to a roster a flying roster where I don’t know what I’m doing in advance, and I’m away from my family quite frequently. I want to get financial independence and I want to be able to have more control over where my time goes. Based on the 4% rule looking at somewhere between $600,000 to $1 million dollars worth of investments.

The second thing when I’m sitting my goal here is I got a realise it as an Australian we have a fairly unique tax retirement structure are called superannuation or super. This means that Australians pretty much have a two-tier retirement system now that’s the same for many nations – the USA has their 401k, 403b and there is actually so many different tax retirement accounts and structures – health savings accounts, IRAs, Roth IRAs. The Canadian and UK governments have similar offerings too.They are all essentially a way where you can tuck money away now and receive a bit of a tax savings on your salary as well as tax savings on the growth of the assets within the the retirement accounts.

Coming back to some my situation I’m actually got a really good superannuation package with my employer the company puts in above industry award contributions which is fanbloodytastic I’ve also been salary sacrificing lots of why concession cap which is at the moment my accountant recommended $15,000, but I was recently speaking to someone who mentioned it that that that number might actually be a little higher at $25,000 per year so I need to do a little bit of research and and get back to you on that.

When I salary sacrifice instead of paying my marginal tax rate I actually only pay 15% on the super contributions and for people who aren’t familiar with the Australian marginal tax system, our system you pay progressively more tax as you increase in income. So it starts off the other tax-free threshold I should know this I think it’s somewhere around $20,000 or maybe just under that $18,200. It progressively increases I think the average rate is about 30-37 cents in the dollar foremost income goes up to about 47% once you’re on a quite a high high income (>$180K). It’s a progression Tiered or marginal System.

If you’re not sure how that works there’s some really awesome explanations on the ATO website; Basically it means that up to that first $18,200 you’re not going to pay any tax at all, and then up to the next bracket of $37,000 you pay 19c in the dollar and thenif you earn more you start paying 32.5c in the dollar. You only the pay the higher tax rate on the amount that you’re above the increment so it’s not like you magically start earning above in a certain amount of money and you will suddenly get a huge tax bill – despite a lot of people at my work that think some out it works that way. Its a really fair system

Straight away I knew hey super is going to be a massive tool for me to achieve FI and I’m going to need to use it to my advantage. What does that mean for my FIRE number – well it means that my get FIRE portfolio or my taxable investments are only really gonna need to keep me going until I reach preservation age when I can receive my super. So for now I’ll keep stashing as much as the government let me into Super because hey why not and I will continue to then put any surplus into my taxable investments. This gives me the peace of mind that might FIRE portfolio is only going to have to last me 25 to 30 years.

Even though when we did our first pass the using the 4% rule and we works out in are going to need $600,000 up to a million dollars, I can actually afford to draw-down that portfolio bit quicker so won’t need as much. I did a heap of research and played with some calculators online – by the way there’s a heap awesome tools online just get into Google look at compound depreciation or cost base calculator you can actually work out quite easily how long your portfolio can last with average market returns and your drawdown.

I came up with 7% as a starting point ‘quick draw’ number – I talk to some people about this and their horrified ‘you know 7% your crazy that is not going to last you‘ and they even talk about using it 3% drawdown to be even more conservative than the traditional 4% rule. To that my response is well hey I’m not expecting this money to last my whole life, maybe 25 to 30 years absolute tops.

Working backwards with good old spreadsheets with my projected spending it means I really only need about $320,000 of each year by myself and about $520,000 ETF portfolio once I have a family with that increased spending. Thirty Years though is a pretty long time and there’s no guarantee that the portfolio will actually last that whole time – there might even be some legislative changes to superannuation works potentially they will raise that preservation age and put that rung just at further out of reach. No one’s going to know I mean 30 years there’s a lot of potential for changing governments to come in, and we all know they do enjoy tweaking and playing with our superannuation funds. Even an interesting change of terminology where the government used to refer to super as ‘your super’ and ‘your fund’ and I have noticed that the last couple of governments it’s increasingly being referred to as ‘our superannuation’ which is an interesting from a psychology point of view it’s starting to frame super as no longer purely yours it’s now a national tool.

I don’t want to get into politics – I don’t know anything about politics, I’m sure nobody really wants to hear about it anyway! I think the relevance is that you need to protect yourself or have some kind of insurance against that happening. For me personally when I look at my goal of FI I’m pretty flexible. I know that I enjoy and could take up flying instructing or other part-time gigs and I’ve got a couple of business running in the side and whilst they’re not super profitable and whilst flying instructor isnt a Super profitable gig it’s still an option to earn a little bit of money on the side and suppliment the portfolio.

The average amount I was getting instructing is about $100 an hour so you if I really only needed an extra $200-300 a week I could achieve that maybe it one day or maybe into split over 2 days at the airport. Hopefully maybe I’ll be teaching navigation and doing a very long 5 hour flight to maximize wages for that day.

I do have options to go back to part-time work and I know I’m able to tighten the old purse strings and reduce my spending, so really I’m not that worried about catastrophic market crash – something like that is not going to wipe me out in early retirement

With my goal set the next step for me was educating myself again that was that step 1 to reaching financial independence which we talked about last time. I set out to read everything I could. One of the first books on the topic was Scott Pape’s barefoot investor which has actually been around for a very long time and is remarkably similar to another book that I read Dave Ramsey total money makeover. These are really fantastic books full of really practical common-sense tips that you can use. This helps you slash your spending and allows you to keep that money starting investing and generally just get a much better deal. Scott Pape provides you scripts to negotiate a better mortgage rate and get a better rate on your Internet and phone service. So again great books – I would definitely recommend them as a starting point

I’ve always been naturally pretty good with money – coming from an engineering background maths and physics anything to do with numbers and equations was easy – I get off over that stuff. I know some peoples eyes will glaze over but I quite like that, you know that’s why I love flying it’s a very ‘on the numbers game’. If you set the correct attitude and the correct power settings the Jets gonna perform just how you want it too. It’s really fun tweaking and trying to get the best fuel efficiency out of the aircraft and finding the best level to be flying it.

Similarly with finances I was always pretty good at making money stretch further so reading reading those two books was almost a little bit of self validation really, I was glad to see that there was a community of people out there with similar minds. Although I read these books and I thought look OK this is a great solution for most people, for 80 to 90% of people that just want to work a job pay, down the mortgage, get a good deal on their services, go to work do that 9-5 grind and I guess retire eventually with a paid off house and super.

That didn’t really sit right with me because I thought why would I slave away sort of my whole life making money for someone else, struggling to pay a mortgage – look at a market like Sydney where you median house price is well over 7 figures now. I look at some of the houses for sale around my area and some of them are even multiple millions of dollars for what’s essentially just a four-bedroom house with two bathrooms and and two garages on like a 400-500 square metre block it just doesn’t seem to be good value. Growing up in the country and regional suburbs my idea of what property was worth really took a massive hammering when I came to Sydney. I was like they what how much for a house; and the next question was and how many years do I need to work to pay that off?!

I accept that property is expensive in Sydney and wages are may be higher in Sydney on average, but the cost to wage ratio is incredible in Sydney. It is over 10-15x whereas you look at somewhere like where I grew up for example the multiple is 5-6x, so housing affordability varies quite dramatically I think across Australia.

Those those strategies presented in The Barefoot Investor and the Dave Ramsey’s money makeover are great. They are fantastic books – those guys are really clever and really good authors as well. I really enjoyed their writing Style. At that stage though I hadn’t quite discovered FIRE yet so I set out to keep reading and keep digesting everything I could. I found a copy of Robert Kiyosaki’s ‘Rich Dad Poor Dad’ at my local library. Again I was a bit Savvy before before reading these these books and true to my frugal ways I loaned the book out of the library got it for 2 weeks and I read it overnight.

Rich Dad Poor Dad by Robert Kiyosaki is a fantastic book. What I think it really helps with your mindset. You’re not going to read the book and magically become rich overnight, or even get a strategy to start growing wealth at all. What it really helped outline for me was the difference between an asset and a liability – and we spoke last episode about that to some great length about why you need to gather assets and cut away your liabilities. So that book was great and that really charged me up – It was kicking my desire for FI/RE into afterburner mode. I knew that I had to have some kind of business and I needed to keep getting assets and with my abundance mindset I was going to succeed.

I thought I was good with money but I had really just been stashing it term deposits and managed funds and then spending pretty much all of it. The money came from jobs, scholarships as an engineer and subsequent jobs that I had. I was tutoring whilst I was that University, gardening, anything that I could do for a bit of extra money – I mean at one stage I was picking up cigarette butts and cleaning graffiti because I was spending so much money pursuing my dream of becoming a pilot.

All up it was $300,000 which is quite really high from an aviation perspective – I think most people would be able to get away with spending probably half of that. The reason it was so expensive for me was partly my fault – I did a lot of extra courses and consolidation and I hesitated on pulling the trigger – I was scared to leave my secure desk job in pursuit of a flying job which generally pays a lot less and is a lot riskier with no job security, that kind of stuff. In Aviation if you hesitate or you delay, your retraining can actually be quite expensive. After a while your skills begin to fade you sort of get rusty so you do need a continue to fly and to keep yourself sharp – and of course if you’re not being employed as a pilot you’re going to have to pay for that

So part of that craftiness with money came out of necessity – I was spending at one point over $1,000 per hour to train on a particular type of aircraft. It wasn’t cheap so I tried to get money anywhere I could. Thankfully it paid off and eventually I scored a great flying Job.

In my continued reading I found a reference to a book by Benjamin Graham. I found this online when I was learning about Warren Buffett and I found out that he actually written a forward to chapters in Benjamin Graham’s book The Intelligent Investor. Now for someone who’s in the FI community obviously those two names are legendary – they are the Michael Jacksons, the Einsteins of investing. They are two of the most successful investors I think the world has ever seen. Benjamin Graham was Warren Buffett’s mentor and Buffett learn a lot from from Graham. I read thier book which isn’t the easiest read it’s it’s quite long. It talks about value investing and and how to work out whether something is a good deal and also about working out what kind of investor you are. I describes the difference between an active and a defensive investor – I’ve never really heard of the term ‘defensive investor’ before; an active investor would tend to work quite hard on his or her investments wheras the passive or defensive investor really just didn’t really want to spend their time doing any of that.

I learned some interesting delineations and some new concepts in that book – again, fantastic book. I also read Buffets letters to his shareholders and notes which are freely available on his website through Berkshire Hathaway. Its a pretty rudimentary site which I guess is probably testament to buffets value based investing approach (no frills sort of thing).

After this I sort of myself a bit of a bit of a value investor and started to look at evaluating individual companies and stocks and you know what these dividends are, and look at the earnings per share and the P/E ratios… I had a lot of fun over it basically a year or two but the problem was it was taking up quite a lot of time. I read an article someone forwarded to me about index investing – of course everyone is trying to beat the index through active investment – myself included. Anyway after some 2 years trying to beat the market with what I believed in his superior investing ability which you like let’s be honest I was rubbish. There was nothing special about me other than maybe that I liked spreadsheets and numbers.

After I crunched all the numbers I worked out that for all my wins and losses, I Actually under performed the index. Brokerage, bad picks and the opportunity cost of sitting on money in my brokerage account clearly explained this under performance of the market. I would have just been much better off to buy some kind of index tracking fund.

I knew that was what I needed to do – I needed an index fund so I got to work investigating indexed funds and learning all I could about indexed funds and I discovered funnily enough FI/RE. The FIRE financial independence retire early community is amazing there are there a lot of really talented people are providing a lot of fantastic information and guidance online

One of the first FIRE blogs that I actually discovered was the Aussie firebug. The Aussie firebug is an Australian millennial as he says ‘trying to escape the 9-5 grind’ and he’s got some really quality articles on his site which really led me down the rabbit hole. I started listening to his podcast and I noticed that one of his first guests was a Canadian blogger The Mad Fientist – so I went and read all of The Mad Fientist blogs and listened to his podcasts. I found his interview with Mr Money moustache – which sounds like a ridiculous name but this guy is actually super famous in the FI community. This guy is kinda like the Jesus, or the The Beatles of personal Finance.

Mr Money moustache was actually blogging anonymously and he wrote hundreds of articles, I think there’s probably even thousands of articles that he has either written or co-written or featured in. They are awesome and feature everything from cutting down your bills to investing, to dealing with the social aspects of FIRE. Really great stuff. I pretty much ‘cover to covered’ the Mad Fientist, Mr Money moustache and the Aussie firebug’s websites. They really helped me totally immerse myself in this myself in the subject of financial independence. The better understanding of FI helped me to come up my own FI investing strategy. As Warren Buffett says – a smart investor is someone who is always listening and reading and learning more

I got to work learning different strategies; I read about lump sum investing, dollar cost averaging, buying the dip, flipping – which is you know is the buy buy low sell High make money thing (maybe make money for your broker) and the buy and hold strategy. I knew there was all these different ways, but I didn’t necessarily like them or like some parts of them all. I had to somehow had to pick and mix the best parts to come up with my investing strategy

Dollar cost averaging or systematic implementation / investing provides some kind of benefit against emotion a you put a whole bunch of money in the market and and it goes down and then you feel bad – so this psychology human psychology aspects of investing is kind of what I think makes the market a little bit irrational in the short term but I do believe in it in a in efficient market and that eventually price and value will be the same thing. Because of people’s emotional approach to investing we know we see this crazy volatility in the in the stock market. Dollar cost averaging can be a way that someone with a low risk appetite might choose to invest their money into the into the stock market. It’s a really interesting subject if you want to learn a little bit more there’s a book by Dan Ariely called predictably irrational and I think he has some stuff on YouTube as well awesome reads.

Another really good book I read was by Michael Kemp called uncommon sense and that talked a little bit about investing in the stock market and why people act the way they do. You know why common sense is not all that common amongst investors haha. I think Michael Kemp actually works pretty closely with The Barefoot Investor so that’s how I got onto him as an author. He’s actually got another really awesome book called creating real wealth.

I think there worth a read especially if you can pick them up at your local library. I’ve also seen a lot of bloggers and podcasts recommending audible and offering you know their free trials so you could investigate that as another way to do this learning self-directed learning for free. and it’s not going to cost you I mean technically if you pay taxes are you probably have paid for it because you’ve paid the rates that goes towards the maintaining the library. It’s your community resource so get involved. While you’re at it literally just go up and down the same aisle and see if you can pull out a bunch of other great reads – if you find any that you love please drop a comment and get in touch cos you know sometimes I have these really long cruise segments and there’s not a lot to do – so if you can put me onto a fantastic book that would be awesome!

I guess the opposite to dollar cost averaging is lump sum investing. People think this is kind of like getting all your chips at the casino and sliding them forward and saying ‘All in’ with a sort of steeley eyes look at the dealer. It sound scary but its not actually anything like that – like I said I love numbers so I dug deeper into the idea of doing it – I asked myself if I should try and balance out the volatility with Dollar cost averaging or should I go all in early.

I read some great papers through Vanguard research (which is a bunch of Finance professionals / statisticians) as well as a few other finance firms like Morningstar quantitative and I actually found out that if you look over the long term, lump sum investing produces greater returns. Over time the market goes up – that’s why the media is always hyping and telling you that it has reached unprecedented new highs. It goes up more than it goes down. Look that’s just the way the world’s fiscal policy works with inflation the way it is. Returns on the stock market are always going to be higher and higher and that is not a bad thing – it’s not good thing – it’s literally just how the economy works.

So these research papers explained when you consider that the market goes up more than it goes down you actually get better returns from putting it all in early as opposed to waiting and missing out on the returns. I didn’t know whether to believe this or not and I thought well let’s give it a crack and see how it goes. I had some some money which I had in a managed fund that I was getting told was doing really well, but I was getting charged really high management fees. I was told I was getting 8-12% growth but actually when I looked at the money that I put in, how long it was in there, and how much I got out and threw it into an excel spreadsheet and annualised the return, really I as only getting just over 4%, and then I had to pay full taxes on that with no franking credits. Those little fees really add up. So I took the money out of there and lump sum invested it into direct shares. Although I now use an index approach, I personally believe that lump sum investing is a better approach to dollar cost averaging.

This is because your money is working for you right away as opposed to say sitting in say deposit with today’s interest rates that that’s barely breaking even you know you might actually you actually probably going backwards in terms of purchasing power when you consider the really low rates of return on the savings account you know might be 1 to 2%. When you look at the target rate of inflation of 2 and 3% it doesn’t add up. For Australians you can have a look on the Reserve Bank of Australia website look at the inflation calculator tool and you can actually see for yourself when you put your details in – ‘oh jeez that money is actually your eroding in value by more than the interest that I’m actually earning’. Of course you’ve got to pay tax income tax on that interest despite the fact that your overall wealth has gone down, which just accelerates that erosion faster. So those bank interest payments are a bloody joke – especially when you consider what the bank is doing with that money. Well the bank is either fractional reserve loaning against it creating credit traps, or they are just investing it themselves – I figured I might as well just bloody do the same thing too.

I’ve had some good and bad timing in the market with volatility around my buys. Nothing I do could give me the upper hand which just highlighted how futile any attempts to time the market really are. When I was buying and selling individual stocks I ended up just basically breaking even with the index or a slight underperform of the index. It made me realise that I should just buy and hold a index fund strategy like an ETF or an LIC and just hold it for the long-term, and you know cash flow the dividends or potentially even sell are small portion as I needed money.

I got to think you’re ok lump sum investing is for me, but what about buying the dip you – could I just take this Benjamin Graham Warren / Buffett style value investing philosophy and apply that to my personal investing strategy? I quickly learnt that you can’t predict the market, volatility is a fact of life. Just like in the book predictably irrational, people make emotional choices and there are so many different triggers and levers and actions and cogs turning in the stock market and you know the national and global economies that you can’t predict price movements.

An earnings profit schedule might be a percent lower than what it was forecast the previous quarter and the stock could plummet 10% or something. The opposite is well is true Tesla recently announced a favourable earnings change and it went up 10%. You really you can’t predict the market.

What that are value investor looks at is what is a good deal or essentially what can I buy discount. Buying the dip is a form of value investing and it’s basically just that – you’re buying what’s good value at the time. Warren Buffett is sometimes referred to this as buying a stock that it’s on the nose with investors, or that’s something that’s not currently popular so Mr market is selling at a discount. Usually though the other line Holdings and companies can be pretty good, and it’s for some reason just not the flavour of the month and that’s the key – as long as the underlying business or company is good. That’s what stock is – you’re buying a piece of a profitable productive company which is taking part in the economy and making peoples lives better.

So for me value investing means buying a stock below it’s net asset value or net tradable assets. I found it incredibly difficult to keep track of with individual equities but I found I could do it with listed investment companies. Old school low fee LICs can actually be like a form of index fund very similar to an ETF. The listed investment company rather than being automated and open-ended like an ETF (which always bite definition trades at its Net Aset Value), is a closed ended fund and can trade at a premium or a discount to its net asset value or NTA. The first LIC I bought was ASIC and last episode we had a laugh about how silly I was when I thought it was actually a concrete or foundation. Well no it’s a listed investment company so it takes your money and it goes and invests in a bunch of other profitable businesses. Depending on the current climate investors may agree or might disagree with the boards investing decisions and as a result the LIC can trade at a premium or discount to its net holdings.

A fantastic tool that I discovered through the Aussie firebug was Pat the shufflers LIC discount estimater. Pat the shuffler is a finance blogger that was interviewed by the aussie Firebug. Pat’s actually lives in the same city as me and was an engineer too – his website the lifelongshuffle is a fantastic website by the way you guys should all go and check it out. Pats LIC discount estimator takes in all the current information from the live market as well as the latest company release and interpolates using the index performance to predict whether a LIC is trading above or below its NTA.

Of course value investors would never look at buying if a LIC was trading at a premium so we are only interested in if it’s at discount. I’ve used that site a number of times to work out which is trading at the highest discount – any time it’s below about a 3% discount is when I get interested in buying (or else I just buy an ETF).

Again, short term trading v long term trading – we talked that it’s about time in the market not timing the market and the dangers of a short Trading against being long on a stock. I personally think that being long on an index stock or being in it for the long haul is the way to go. Maybe that’s just my personal investing preference where I don’t really want to put all my time and effort into actively trading – but I also knew that even when I tried it out I didn’t have fantastic success. So buy and hold for the long-term is really what I’m All About.

Personally I think short term trading is a bit of a mug’s game – all you are really doing is making you making your broker richer, complicating your tax returns and statistically you just likely to get it taken advantage of by a professional trading firm waiting to pounce on any mistake by an individual investors. If you are interested in that last one then check out the book ‘Flash boys’ by Michael Lewis. It actually talks about trade latency and how some investment firms by – for want of a better word – their position in the internet or their node in the network they are actually able to trade faster than you general mum and dad investors and they’re actually able to take advantage of that split. So yeah trading stocks not interested. Again we have said million times Warren Buffett’s famous quote – ‘its not about timing the market but about time in the market’. It’s proven again by the fact that the majority of millionaires made in the stock market are those who have a really simple buy-and-hold mentality and who reinvested dividends.

For me the best way to remove individual company risk over the long-term is diversifying through a good quality ultra low fee ETF index fund.

So by combining lump sum investing, Dollar cost averaging, value investing and buy and hold I came up with my personal investing strategy which works for me. I think it’s based on mathematical evidence and human psychology which works really well for me because you know I’m not very smart, I’m a little bit impulsive and I am also lazy. So I need this super simple, super easy and quick strategy. All I do I make a regular investment decision every fortnight on which indexed funds I’m going to purchase and hold, ideally forever, and that’s it. It takes literally 5 minutes every fortnight

Whenever I get a windfall like an extra payout from work, or I sell a course or book or you know I received a dividend then basically I’m just adding that into my brokerage account and that’s just going to add to my next fortnightly investment decision. In that way whenever I get any capital I’m investing it straight away and I’m putting it to work just like I learnt with the Vanguard and Morningstar papers that showed investing the lump sum straight away he’s going to give me better returns over dollar cost averaging. So statistically the sooner I invest my money the quicker is working for me and those dollars are all my employees. Rather than buying a sort of set amount of shares in the chosen index fund every fortnight I just allocate a certain amount of money so we are trying invest as much money as possible so I’m 80% savings rate which you know I don’t achieve every month but but that’s my target.

I went to lot of different schools I was a bit of a naughty boy got asked to leave quite a few schools. One thing that stuck with me from one was a teacher said aim for the moon even if you fall you’re still amongst stars. I thought it was a beautiful saying with reference to goal setting, and now that I have a masters degree in Space engineering I know that the Stars are a lot further away than the moon its still a good saying! You should set high standard for your goals, so for me with the 80% saving rate I know I might not get there all the time but hey on average I do and that gives me so much more cash to put into investments.

A lot of my colleagues are wasting their income on flashy cars, expensive meals and general lifestyle inflation. Sydney is horrendous – you can waste a lot of money in this city, and you can waste it trying to impress other people and by not thinking long-term or being mindful about your spending and your activities. So by being mindful I’m getting that saving rate up to that 80% which means I can regularly invest a good amount of money. At the moment my goal is to purchase about $3,000 worth of index funds every fortnight. The majority of that comes from my job flying full-time but I fill the gap where when I fall short from my side hustles and other income sources.

The simplest one there is reinvesting dividends from my portfolio – I personally choose to have my dividends paid out to me into my brokerage account and then I can choose where I want to reinvest them. That helps me a bit with portfolio management and asset allocation, but mostly it gives me a bit of a feeling of control over the situation. Realistically I probably should just use the DRP dividend reinvestment plan. They honestly makes a lot of sense since you save on brokerage and they usually allow give you the stock at a discount to what it actually trading at…so yep probably should be doing that but again humans are predictably irrational and I love tinkering – thats pretty much my job right. I know I should touch the portfolio less and just let it be.

Other sources of income for me are selling things, income from my website portfolio, designing and selling websites, property development which I am just getting into. I also had this random phase where I started designing and selling stickers and t shirts and I put them up for sale on a bunch of websites it made a bit of cash and was a bit of fun but really wasn’t a lot as you know by now I kinda suck at graphic design. I haven’t actively pursued it for a while but it does still occasionally drop money straight into my brokerage account which I put towards the next investment decision.

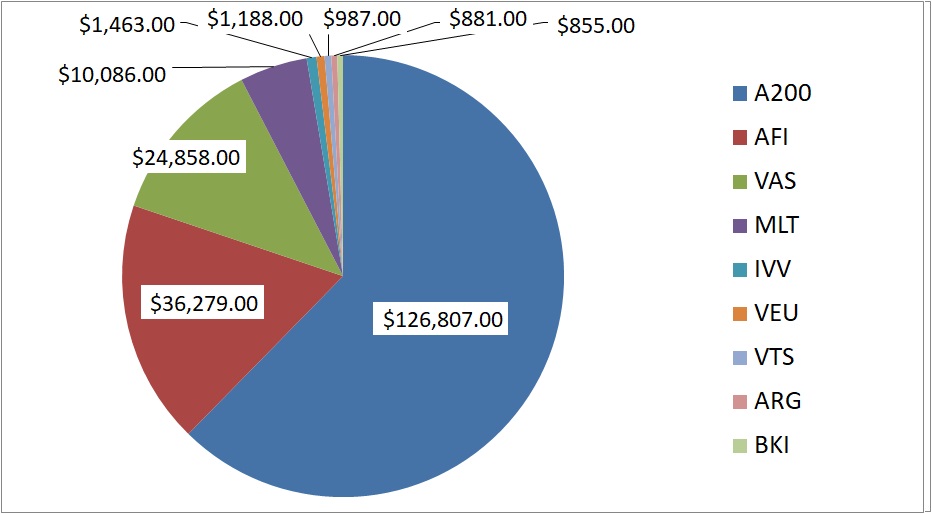

In terms of investments themselves, I’m splitting across 9 different index funds which probably is a little excessive. I basically doubled up every one (asset class) to try and spread my organisational risk – so for example investing in Australian shares through both the ETF Vanguard VAS and also through the Betashares A200 index fund. There’s some slight differences between those two funds – Betashares is slightly cheaper but it’s a newer fund and tracks are slightly index. I actually have articles on all of the different investment vehicles on my website. Just head to www.captainFI.com and go to the investing tab and yeah they’re all in there for you to have a read.

So I split across nine funds, five of which are ultra low fee diversified stock market ETFs and four of which low-cost diversified Australian LICs. The reason I invest to heavily in Aussie shares is because of the franking credits. These are basically a tax credit that comes with distributions from these companies (which have already been taxed). Pat the shuffler has a great article on how franking credits work. At the moment with my salary the franking credits are a really tax effective strategy for me, and I am gaining an extra percent or more return using them over say investing purely in US stocks. I also like LICs because I can buy them under value from time to time. When I reach FI/RE I will likely transition purely to an ETF based strategy – I know there might be some issues with capital gains tax on the LICs though. Its hard to figure out a perfect strategy but honestly its better to just start now and get some skin in the game rather than procrastinating and getting smashed by inflation.

A lot of my ETFs, infact most of my ETFs are managed through Vanguard and are purchased through the Australian Stock exchange. Vanguard is an awesome company, I talk about it a lot on the blog. John (Jack) Bogle started Vanguard and came up with the idea of ETF index funds, he split from his employer who disagreed with him to go and start Vanguard. Revolutionary, Vanguard now manage funds in the Trillions, Im sure the VAS fund probably has more money than the federal government

ETF wise, I have the BetaShares A200 Australian index, the Vanguard Australian Fund VAS, The Vanguard total US market VTS and the Vanguard Total world ex US – VEU, and for extra diversification in the US front I also hold the BlackRock iShares S&P 500 index fund IVV which is basically the same thing as VTS. For the LICs, I four that I own are AFIC, Milton, Argo investments, Brickworks Investments.

These all have a varying management fee. The cheapest are the Vanguard and Blackrock US S&P index funds, which are about .03 and .04% Management fee. That’s incredibly cheap, its basically 4 bucks for every 10 grand you have invested every year. Its pretty low, you’d never find anything that cheap elsewhere. For example I was paying 3% on my managed funds – I didn’t know I was paying that I was just getting charged that. What does that make Vanguard like 100 times cheaper? I read that something like the average person has 40% of their investment return gobbled up by fees which is incredible. Having low fees is super important. You cant time the market or control it, but what you can control are your fees. My LICs are a bit more expensive than the ETFs, which the highest is .17% or $17 bucks per year per $10 grand.

You might wonder why I would then own a LIC with such a high management fee of .17% compared to the vanguard US .04%. That’s a valid question, and I guess people are irrational. I like to invest in LICs as some kind of active thing. Whether that’s a waste of time I am yet to figure out. So far I just keep adding LICs to my portfolio whenever they are trading at a discount. I use Pat the shufflers LIC discount estimator and seriously great work Pat if your listening, mate you save me a lot of time going through NTAs and monthly announcements.

So if your paying a higher expense ratio but you manage to snag a discount of a couple of percent value you might even find the difference in management fees and discount balance out over the long term, and then the ETF will over take the LIC in value. For example if you pick up Brickworks LIC at 2% undervalue, when compared to paying the lower management expense of Vanguard that works out to be about 15 years worth of management fee’s before vanguard becomes better value. If you plan to sell it before the 15 years then hey maybe the LIC was the better choice. This all really depends on different funds, where the spread between management fees is lower it takes a much longer time for the ETF to be the clear winner; for example comparing Milton and Betashares A200 – a 2% discount on Milton would take over 40 years of holding before Betashares cheaper management fee makes it better (assuming the funds perform the same)

There’s a pretty raging debatein the FIRE community about what’s better ETF or LICs – which one should I invest in? Honestly if you choose to invest in either you or you gonna fall pretty close to the mark. My opinion is that actually getting started and investing sooner is going to have a much bigger influence on your financial well-being between than figuring out what is a better investment structure to buy.

We touched on it earlier and I am probably grossly over simplifying it (if theirs any finance professionals feel free to pull me up!) but another factor really is that an ETFs have a fairly simple open ended trust structure. This means they have to distribute any earnings from underlying holdings to their shareholders, wheras the LIC with the closed end company structure can potentially retain those and trickle feed them out shareholders over time.

This means the LICs could be more tax effective if you are chasing more uniform and reliable income – rather than paying out big lumpy dividends they can hold that cash and smooth out distributions giving you stable dividends for the other times when business isn’t booming. The ETF structure has to distribute everything to you at once which might push you up into a higher tax bracket and result in more tax payable.

Some people don’t really like that sort of babysitting type approach the LICs have and would prefer to have their money given to them straight up, pay your share of tax and then get the get those dollar employee’s working for you straight away.

The other difference is that ETFs automatically rebalance depending on the index they are tracking. In Australia you due to the market capital of the big companies that means they are fairly heavy on the financial sector – the big 4 Banks as well as mining stocks. LICs on the other hand employ fund managers to pick stock so they can choose a different weighting. That makes LICs actually a form of active investment which for me raises alarm bells. Thankfully, the older LICs are low fee and stick mainly to a conservative index. I’m not a fan of managed funds because of the irony that most actively managed funds under perform the index and make you pay a premium to do so – I think its funny you’re basically paying someone to stuff up your investments for you when it’s actually just better to have an ETF.

so it sounds like I’m bashin LICs here but you know I’m not I do buy both, I buy the old school conservative low fee LICs which have a pretty good track records. Their portfolios mostly mimic the index but they do deviate away from some of the larger speculative stocks in preference to more high dividend yielding sectors and companies with a stable and known increasign rate of dividend.

Buying a LIC at a discount is great, but the other benefit is they tend to focus on producing an increasing dividend yield every year. The LICs I own have a strong history of increasing dividends to their shareholders. This is really important when your building a FI/RE portfolio as your essentially looking to replace your income as an employee. Getting tax effective dividends which increase over time is a huge benefit and a great way to replace your employee income. You can sell portions of stock but dividend streams and dividend investing one of the simplest ways to do this. We will talk more about dividend investing next time when we compare the Thornhill dividend investing approach with the capital growth or Boglehead approach. But in the crux the Thornhill or dividend investing approach is very tax efficient in Australia due to franking credit refunds. Whilst Im investing in global ETFs, Im also holding Aussie LICs just for that increased tax effectiveness.

So wrapping up, lets talk about some of the benefits of my investing strategy. The first thing I think is emotion. I’m technically over time Dollar cost averaging into the market but because this is money I invest as soon as I get it, this is also ironically a form of Lump Sum investing. By doing this I am removing any emotion and doubt about the market I don’t have to think or stress about if the market has gone up or down. Its really simple I just stick to my strategy every fortnight and I don’t have to really think about it.

The second benefit is cost base, so whilst I’m lump sum investing every fortnight in the long-term this means I actually buy shares cheaper and how this works is if the market rises and the price of shares increase, my $3,000 fortnightly investment decision by it’s me less shares that fortnight. On the flip side if the market drops and the market goes down then my $3,000 buys me more. So overall when I consider what I have paid I have bought more for less than I have bought less for a higher price – so better value for money.

The third benefit is Diversification – by splitting my investments across 9 ETF and LICs I have global diversification and to loose all of my money I would need every company in the world to pretty much collapse.

The fourth benefit is franking credits. This is due to a having a large amount of money invested in Australian shares. It might seem like a classic case of home bias but the franking credits are too juicy to pass up. They account for over an extra whole percent of return which is a huge amount for anyone chasing FIRE.

Benefit number 5 is I never need to know when to sell – so I just buy and hold. My smartly diversified Holdings of thousands of different companies are all getting re-evaluated in rebalanced in the ETF and LICs are sorting them all out for me. I never ever need to worry about getting the best price for a sale or working out what my CGT implications are. I just sit back by the pool and sip cocktails from a coconut while the dividends continue to pour in and increase over time. Well maybe not the coconut thing but you get the idea. It cuts out a huge waste of brokerage on sales

benefit 6 years value. By purchasing the LIC at a discount I know it’s instantly a good deal for me and generally it’s going to go up in value with volatility and overtime – so I’m confident that if I do need to sell that stock in the future I can get more than I paid for it, but again I don’t plan to sell it and I only buy it for the increasing divident stream over time

Benefit 7 is management fees and which is super important. By buying ultra low fee index fund ETFs and low cost LICs I pay bugger all in management fees. I’m saving hundreds of times the management fees most people spend on actively managed funds. On a portfolio of $1M, the average cost for ETFs would be $1000 a year -you’d spend more if you went out for dinner once a month!

I guess the last my last benefits is Free portfolio tracking and management using sharesight! I’m pretty embarrassed to say originally I was using Microsoft Excel initially – I had a fairly complicated spreadsheet which I just could not manage in the end. I tried using the registries as well but you know they the registries often want to charge you for your end of year end of financial year tax documents. I stumbled across share sight through the Aussie Firebug and its super easy to use and completely free if you have under 10 holdings.

So that’s my strategy guys, I’m sticking with it and on my way to creating a $1M net worth by the end of 2020. Let me know what you think and hit me up with your personal strategies. remember I’m just a bloke trying to reach Financial Independence, and not a financial professional so take everything you’ve read with a grain of salt.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Thanks Heaps, i also wanted to be financially free I don’t know how, but this podcast is certainly showing some light at the end of tunnel.

Hi Gurdeep! You and me both! Great idea to start learning and getting into the nuts and bolts of how it all works. In terms of my own journey, I’ve found really cutting down my expenses and maximising how much I can save of my pay to invest has been a great start. Then I’ve just been putting it into low cost index funds and LICs, little by little building the portfolio and the passive income it generates. If all goes to plan in a little under two years I should reach FI, but I’ve also been working on it since 2016, so don’t lose hope if your still early on in your journey!

Sounds like a great option! This is a real motivation for me! I am always interested to know the experience of others. Thanks for sharing!