Ah, the famous Barefoot Investor index funds! We all know index funds are a method of stock market investing, so what share market index funds does the Barefoot Investor buy? Read on to find out exactly what and how to create your own Barefoot Investor index fund portfolio.

Topics: Barefoot Investor index funds – Barefoot Investor shares – Barefoot Investor ETFs

Exchange-Traded share market Index funds, or ETFs for short, provide diversification, are easy to buy and manage, and most have very reasonable (low) management costs (management expense ratios).

They make it easy for investors to choose what markets and assets they want exposure to, making them a useful tool to structure a portfolio according to an individual’s personal circumstances and preferences.

So, what does Scott Pape the Barefoot Investor think of index funds, and what are the barefoot investor index fund portfolios?

The Good

- Outperforms actively managed funds over the long term

- Diversification

- Passive investment – no time required to actively manage

- No experience required

- Fewer trading decisions required

- Lower fees than actively managed funds or all in one funds

- Can tailor each ETF weighting to suit your personal preferences

The Bad

- Need to manually rebalance these portfolios over time

- Higher brokerage costs than an ‘all-in-one’ ETF

- Limited exposure to small-cap companies

- You can still stuff it up if you don’t know what you are doing

- Not appropriate to everyone’s circumstances

- Share market volatility means they can go down in value

Verdict: The Barefoot Investor Index Fund portfolio can be easily set up through Pearler using A200, VTS and VEU

CaptainFI is not a Financial Advisor and the information below is not financial advice. This website is reader-supported, which means we may be paid when you visit links to partner or featured sites, or by advertising on the site. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Introduction to the Barefoot Investor index funds

This article will explore what the Barefoot Investor thinks of index funds, and explores some of the index fund portfolios he has created and invested in, such as the Breakfree Portfolio, and the Idiot Grandson Portfolio, including his recommended Barefoot Investor ETFs. The article then explores the practical side of things – how I take Barefoot Investor index funds recommendations and actually construct and manage a portfolio. I cover:

- How I have constructed my portfolio using the A200, VTS and VEU index funds

- How I use Pearler to buy the Barefoot Investor index funds, and how I rebalance the portfolio using the Autoinvest feature

- How I track and manage my portfolio using Sharesight.

However, you shouldn’t just blindly follow what the Barefoot Investor says or copy what I do with my money, and you need to do your own thorough independent research (including reading things like the PDS), and consider holistically your financial needs such as risk tolerance, investment time frame/horizon, emergency funds, insurance requirements etc. If it’s starting to sound complicated and overwhelming – think about going to see a licensed financial advisor.

Who is the Barefoot Investor?

Well, unless you’ve been living under a rock, you’ll know that the Barefoot Investor is Australian Scott Pape. Self-proclaimed as “Australia’s favourite money guy”, he provides no-BS personal finance advice and recommendations, and recently re-trained as a not-for-profit financial counsellor.

While he recently closed the Barefoot Investor Blueprint which contained his Barefoot Investor shares recommendations and Barefoot Investor ETF recommendations, he did provide some further recommendations – which I’ll get into later.

What does the Barefoot Investor think of index funds?

Well, it turns out the Barefoot Investor thinks index funds are great. Actually, one of his favourite investment firms and one he recommends everyone starts with when they buy shares is the Australian Foundation Investment Company – AFIC. This is a solid company that was my first share purchase.

Although, if we are getting technical here, AFIC isn’t an index fund, but it sticks pretty darn close to the index and it also has pretty low fees. I prefer to call it an ‘old school granddaddy LIC’!

The Barefoot Investor has designed a couple of index-based portfolios over his time, which he has distributed to his readers. While he has dabbled in stock picking and used to provide a subscription stock tip service, he has since cleaned his act up. He is now providing free financial counselling through his charity to some of the most vulnerable Aussies, which I think is a very noble thing to do, and completely makes up for his previous stock-tipping-dodgy-ness.

He initially suggested the Barefoot ‘Breakfree Portfolio’, and has since revised this and called it the Barefoot ‘Idiot Grandson Portfolio’.

I’ll get into both of these portfolios in this article and explain what each includes.

No products found.

No products found.

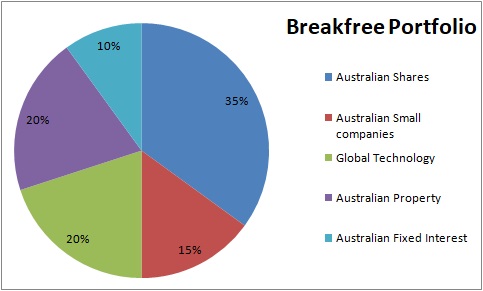

The Breakfree Portfolio was designed by the Barefoot Investor with the idea of “breaking free” from dealing with your portfolio all the time. It’s a fairly simple portfolio that predominantly includes Vanguard ETFs:

- Australian Bluechip Shares: STW – 35%

- Australian Small companies: VSO – 15%

- Global Bluechip Shares: IOO – 20%

- Australian Property securities: VAP – 20%

- Australian Fixed interest: VAF – 10%

The Barefoot Investor suggests re balancing once a year in the following ratios

State Street Global Advisors (SSGA) are the fund manager for STW which seeks to track returns according to the S&P ASX 200 fund (ASX:STW). The MER is .13% and since April 2020 their 1, 5 and 10 year returns have been -17.96%, -2.14% and .71%.

The Barefoot Investor recommends holding the bulk of your portfolio (35%) in STW to concentrate your returns on the majority of blue-chip Aussie stocks. These pay good dividends (approximate current dividend yield of STW is 6%) with quarterly dividends that are approximately 70% franked.

Australian Small companies ASX:VSO

Vanguard MSCI Australian Small Companies Index ETF (ASX:VSO) seeks to track the MSCI Australian Shares Small Cap Index. With a MER of .3%, its one of the more expensive ETFs, and as of March 20 its 1,3 and 5 year returns are -21.24%, -1.81% and 1.84%.

The Barefoot Investor recommended holding 15% of your Breakfree portfolio in VSO to diversify within the Australian share market sector, weighting your portfolio to small size companies which have been shown to provide higher risk but higher reward. For example, during COVID-19 a number of these small-cap stocks have suffered greatly, and many smaller businesses have even gone bust.

The BlackRock iShares Global 100 ETF (ASX:IOO) is an ETF which tracks the Global S&P 100 index. It has a fairly high MER of .40%, and its 1, 5 and 10 year returns (as of April 2020) have been 7.14%, 10.01% and 13.17%.

The Barefoot Investor recommends 20% portfolio exposure to global bluechip shares to spread your investment risk out of Australia and diversify into some of the worlds biggest companies like Microsoft, Apple, amazon and Nestle.

Australian Property ASX:VAP

Vanguard Australian Property Securities Index Fund (ASX:VAP) tracks the Standards and Poor’s ASX 300 A-REIT index (Australian Real Estate Investment Trust). Its one year return is -31.39% (OUCH), 3 year return is -4.88% and 5 year return is .39% (as of March 2020). The management fee is .23% –

This portion is to provide investors exposure to the Australian property market to provide diversification into a non correlated asset class. The Barefoot Investor recommends to hold 20% of VAP in the breakfree portfolio.

Australian Fixed interest ASX:VAF

The Vanguard Australian Fixed Interest Fund ETF (ASX:VAF) seeks to track the benchmark of the Bloomberg AusBond composite 0+ year index. As of 31 Mar 20, the 1, 3 and 5 year returns have been respectively 6.67%, 5.58% and 4.09%. This has a management fee of 20 basis points (.2%).

This portion is suggested to be 10% of the portfolio, and exposure to Fixed Interest bonds seeks to reduce volatility in the Breakfree portfolio

Want to make more money to invest?

Before we go any further, if you are interested in knowing how to make more money in order to invest towards reaching financial independence? Check out my detailed article how to make money online.

After releasing the Breakfree Portfolio, the Barefoot Investor took another closer look at index funds in general. He started by looking at over 315 different index style funds – a combination of 201 true index-tracking exchange traded funds and also 114 index-inspired listed investment companies (LICs), and whittled them down to a final list of ten potential index funds worthy of investing in.

Barefoot Index fund first pass

The first iteration of the Barefoot Investor Idiot Grandson index fund portfolio looked at over 315 individual funds (no I will not list them here LOL!) and cut them down based on management costs.

Management costs are a massive deal and you only need to play around with compound interest calculators to work out why. Paying a 1% management fee doesn’t sound like much, but in the long term (30 years) when dealing with stocks for the average investor, this can add up to hundreds of thousands, if not millions, of dollars.

It is known that on average, investors have up to 40% of their investment returns gobbled up due to high management fees and charges.

The first pass cut away any index fund with a management expense ratio (MER) above 0.40% (which equals $4 per every $10,000 invested each year).

This cut the list down to 60 ETFs and 10 LICs to choose from (and no I won’t list them, there is STILL too many)..

Barefoot Index fund second pass

The second pass analysis of the Barefoot Idiot Grandson Portfolio of index funds cut away funds based on undesirable fads and those that contained risky financial products like synthetics and derivatives

These are second or even third order financial products that don’t actually track or represent underlying holdings, but rather are a gamble or speculation on how their prices move (for more detailed explanation watch the movie The Big Short).

The second pass also removed any ‘outliers’ such as funds geared towards producing really high dividends. High-dividend stocks often suffer in terms of total return due to a lack of capital growth, a form of dividend trap. Both dividend yield and capital growth that should be considered together.

The second pass similarly removed small company funds (which was ironic as we were recommended to buy these in the form of Vanguard’s ASX:VSO fund in the Breakfree Portfolio).

Similarly, equal weight portfolios were discarded. These are portfolios which include the same dollar or percentage value of all the stocks they hold, which by definition gear a portfolio more heavily toward small caps than a typical index fund.

Finally, in a move which could be considered a one finger salute to investing legend Peter Thornhill (who loves Australian industrials), all industrial funds were also dropped. You can interpret that how you wish but I am not sure why the Barefoot Investor has done that.

This left only 6 LICs and 13 ETFs to choose from.

Barefoot Index fund third pass

The Barefoot Investor index fund third pass cut the remaining 19 index-style funds down to just 10 by considering the management style of the funds. This pass was more of a judgement call, where the Barefoot Investor opted for funds owned and run purely to benefit its shareholders (not-for-profit funds), such as Vanguard.

This is because they have the lowest MER and the management themselves are shareholders, meaning they make decisions and act in the shareholders’ best interest.

Personally I was a bit miffed that BetaShares A200 didn’t make the cut since that’s something I invest heavily in (I suspect it’s because the Barefoot Investor doesn’t like BetaShares), instead of Vanguard’s VAS fund.

So, without further ado, here is the final list of the recommended Barefoot Investor shares that make up the Idiot Grandson Portfolio.

Barefoot Investor Idiot Grandson Portfolio: Australian LICs

- Australian Foundation Investment Company (ASX:AFI) MER = .14%

- Milton investment corporation (ASX:MLT) MER = .12% – Taken over by Washington H. Soul Pattinson WHSP (ASX:SOL)

- Argo Investments (ASX:ARG) MER = .16%

- AUI: Australian United Investment Company (ASX:AUI) MER = 0.12%

- DUI: Diversified United Investment Company

Barefoot Investor Idiot Grandson Portfolio: Australian ETFs

- Vanguard Australian shares top 300 (ASX:VAS) MER = .10%

Barefoot Investor Idiot Grandson Portfolio: International ETFs

- Vanguard Total world ex US (VAS:VEU) MER = .09%

- Vanguard Total US Market (ASX:VTS) MER =.03%

- VGAD: Vanguard MSCI Index International Shares (Hedged) ETF

- VGS: Vanguard MSCI Index International Shares ETF

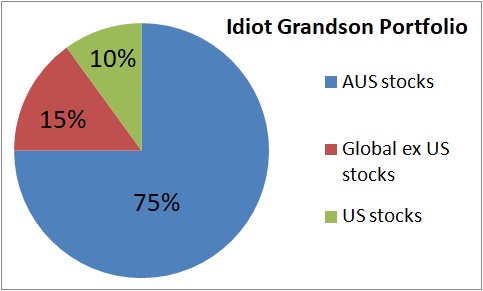

The Barefoot Investor Idiot Grandson Index Portfolio

As the Barefoot Investor says, the sheer power and simplicity of the exchange traded fund trumps all. Pick whatever index funds you want from this third pass, and put them in these percentage allocations:

- Australian total share market index fund: 75%

- US total share market index fund: 10%

- Global ex US total share market index fund: 15%

How I use the Barefoot Investor Idiot Grandson Portfolio

The Barefoot Investor Idiot Grandson Portfolio could be cheaply and simply constructed using a split of A200 / VTS / VEU – interesting that this has been the core of my investment holdings and my financial independence investment strategy for some time!

Of course, the Barefoot Investor suggests you could use any index funds or from his final third pass to meet this asset allocation. My personal investing preferences have evolved somewhat over time,

If you’re already familiar with my investment strategy, then the below won’t be a surprise to you – I focus on making money online and then investing that into a diversified portfolio of index funds, property and reinvesting some into my websites, but I thought I’d focus here just on my index fund investing strategy to show how you also can create something similar to the Barefoot Investor’s strategy.

BetaShares A200 ETF aims to track the Solactive Australia 200 index, that is the top 200 Australian publicly traded companies by market cap. This is effectively the biggest blue chip Australian stocks. It has a MER of .07% and as of March 2020, its 1-year return has been -14.56% (exactly the same as the index it tracks).

Check out my detailed review: BetaShares Australian top 200 index fund

Vanguard US total stock market index fund (ASX:VTS)

Vanguard US Total Market Shares Index ETF (ASX:VTS) tracks the CRSP US total market index (approx 3500 stocks). With a MER of .03% it is one of (if not the) cheapest ETFs on the market, and its 1, 3 and 5-year returns as of March 2020 are 5.32%, 11.91% and 10.53%

Check out my detailed review: Vanguard Total US Market

Vanguard World ex US total stock market index fund (ASX:VEU)

Vanguard All-World ex-US Shares Index ETF (ASX:VEU) tracks the FTSE all world ex US index. Its MER is .08% and as of March 20 its 1, 3 and 5 year returns are -2.25%, 5.33% and 4.01% respectively.

Check out my detailed review: Vanguard Total world ex US

Aussie Listed Investment Companies

I don’t choose to invest in LICs anymore, but these are ones that I have previously invested in. If this is something you are considering, you can use these review articles as a starting point for your own research or a discussion with a financial advisor to see if they are suitable for your own circumstances.

- Australian Foundation Investment Company (ASX:AFI) MER = .14%

- Milton investment corporation (ASX:MLT) MER = .12% Taken over by Washington H. Soul Pattinson WHSP (ASX:SOL)

- Argo Investments (ASX:ARG) MER = .16%

- Brickworks investments (ASX:BKI) MER = .10%

No products found.

No products found.

How to buy the Barefoot Investor index funds

Alright, so that was a lot to get through, I know. But now hopefully you have a good idea about what the Barefoot Investor index funds actually are.

Buying the Barefoot Investor index funds and building your own portfolio can be easily done using pretty much any online share trading platform. Check out my Pearler review (This is the broker I currently have my Barefoot Investor Index Fund portfolio with).

I personally like the security and peace of mind that comes with using a CHESS sponsored broker in Australia.

Once you have a brokerage account opened, buying the Barefoot Investor index funds to set up your own portfolio is actually super simple – its just a matter of choosing the funds you want to invest in, and buying them in the ratio you have decided on.

Tracking your Barefoot Investor index funds

The beauty of index funds really lies in the fact that a handful of holdings can literally give you global diversification to not only every single blue chip stock, but also small caps and emerging markets.

But luckily you don’t need some crazily complicated spreadsheet that tracks thousands and thousands of companies. I started using Excel spreadsheets to track my index fund holdings, but it quickly became an unwieldy beast and overwhelmed me.

I discovered Sharesight, a free accounting tool. Finance professionals and companies often use a paid Sharesight subscription to help them manage massive amounts of data (such as multiple client portfolios etc), but for you and me, we can use Sharesight completely FREE because we have under 10 holdings.

The free account is more than enough for the average person, but you can upgrade to a paid subscription which gives you some more features.

Check out my detailed review of how I use Sharesight to manage my index funds, or Captain FI readers can actually get thisbonus sign up offerwhich gives you four months of premium for free if you do upgrade.

Summary of Barefoot Investor Index funds

After trying to stock pick, value invest, and time the market I eventually transitioned to the Barefoot Investor Index Fund portfolio in an effort to simplify my life and investments, whilst also trying to maximize returns and decrease long term risk. However, as with any investment, it may not be appropriate for everyone, and you certainly need to do your homework and consider whether it is right for you.

Want to learn more about the Barefoot Investor?

Check out the Barefoot Investor’s award winning books

The Barefoot investor

Scott Pape’s original book the barefoot investor is a great read and highly reccomended.

No products found.

The Barefoot investor for families

The barefoot investor for Families is Scott’s second book, with a focus on how parents can educate their kids and teach them the value of a buck

No products found.

The Barefoot investor for kids

Scott Pape wrote this third book recently, the Barefoot Investor for kids. If you want the kids in your life to be good with money, hand them this book. Teaching kids about money isn’t easy – so let Scott Pape do it for you. His books have sold millions of copies and counting.

No products found.

Check out the following reviews on brokers that offer online trading to buy Australian and international shares. As always, make sure you are fully educated before making a choice on any particular one.

Big 4 banks

- CommSec Share trading [this is who I started out investing with]

- NAB Trade

- ANZ Trade

- Westpac Trade

Fintechs and smaller banks

- Pearler [This is who I currently invest through]

- SelfWealth

- Stake

- Superhero

- OpenTrader

- eToro

- CMC Markets

- IG MarketsGroup

- Interactive Brokers

- plus500

- Tiger Brokers

- Moo Moo

- Superhero

- Bell Direct

- Bendigo Invest Direct

- WeBull

Microinvesting platforms

- SpaceShip – A pooled investor micro-investing app

- Raiz Invest – An awesome tool that lets you ’round-up’ your purchases to the nearest whole amount and invest the difference

- CommSec Pocket – CommBank’s response to micro-investing tools

- Stake – A cool investing tool that lets you shop for more than 3,500 American shares and ETFs with zero brokerage fees

- Pearler Micro – Pearlers Micro investing tool that lets you invest into 8 ETF based funds using Auto invest and roundups.

Roboadvisors

- Stockspot – A Roboadvisor which automatically invests your money into a mix of ETFs (Shares, Bonds, Cash and Gold) according to your personal situation and risk tolerance

- Six Park – A Roboadvisor which automatically invests your money into a mix of ETFs (Shares, Bonds, Cash, Infrastructure, Property) according to your personal situation and risk tolerance

Financial Disclaimer

Financial Disclaimer: CaptainFI is NOT a financial advisor and does not hold an AFSL. This is not financial Advice!

I am not a financial adviser and I do not hold an Australian Financial Services Licence (AFSL). In this article, I am giving you factual, balanced information without judgment or bias, to the best of my ability. I am not giving you any general or personal financial advice about what you should do with your investments. Just because I do something with my money (or use a particular service or platform) doesn’t mean it is automatically appropriate for your personal circumstances. I do not recommend nor endorse any financial or investment product, and my usage or opinion of any product should not be interpreted as an endorsement, advertisement, or intent to influence.

I can only provide factual information based on my journey to Financial Independence, and that is provided for general informational and entertainment purposes only. I make no guarantee about the performance of any product, and although I strive to keep the information accurate and updated as it changes, I make no guarantee about the correctness of reviews or information posted.

Remember – you always need to do your own independent research and due diligence before making any transaction. This includes reading and analysing Product Disclosure Statements, Terms and Conditions, Service Arrangement and Fee Structures. It is always smart to compare products and discuss them, but ultimately you need to take responsibility for your use of any particular product and make sure it suits your personal circumstances. If you need help and would like to obtain personal financial advice about which investment options or platforms may be right for you, please talk to a licensed financial adviser or AFSL holder – you can take the first steps to find a financial advisor by reading this interview, or by visiting the ASIC financial adviser register and searching in your area.

For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Good read.

I had a look at the Idiot Grandson paper a while back and was surprised, perhaps even a bit reassured that the allocation I went with for Australian/International (which suits my own personal goals) was very similar to what Scott Pape proposed in that paper.

That said I hold a mixture of ETF’s and LIC’s so it’s still different from his final portfolio.

I only have five holdings but I have also been tempted to just roll it into a basic VAS/VGS split which I’ve been adding to more over the last 9 months, however I think I’ll hold onto the LIC’s as a smaller percentage of the overall portfolio as I feel more comfortable with them during major downturns like the current pandemic.

Hi mate, I did some research into VGS and came out with the conclusion that I will be sticking to a VTS/VEU split instead of VGS.

Excellent article! I am surprised by the high allocation of Australian funds though. Vanguard’s VDHG has it closer to 40% which is still considered high by some.

Hi David,

I think its a consequence of the awesome franking credit system, the strong Aussie dividend yields and the home bias. I agree, 75% is a high allocation to national funds. My portfolio is a bit out of ‘whack’ and heavily weighted to Aussie shares as I think they provide a quicker path to FIRE, but less diversification. As I get a higher net worth, I will endevour to diversify overseas more. I am thinking my ‘ideal’ post FIRE portfolio might look something like: 50% AUS – A200, 30% US – VTS, 20% total world ex US -VEU. Or maybe even 40:40 AUS/USA. What do you think?

I am 15 years old and I am thinking about investing in a simple share fund (annual contribution – $5000). Would you recommend that I invest in different index funds (AUS – 75% US – 10% Global – 15%) or should I just invest in just one index fund? If so, what index funds would you recommend?

Hi Arihant, First up thats just downright amazing that you are thinking about this at 15 – if you maintain even a 50% savings rate which is incredibly easy, you could be financially independent by 31, or bumping it up to 60% that would mean financial independence by 27! incredible! (https://networthify.com/calculator/earlyretirement). Unfortunately mate I can’t really recommend any particular investment or financial product – and its important to note that nothing here is financial advice. What I can recommend though is to work hard, keep reading and save hard so you can invest hard. As your friends increase their income they will likely lifestyle inflate, but if you manage to keep tucking away a good portion into your investments, you will become rich. That is a fact. I personally choose low management fee total index fund ETFs, and low management fee old school LICs, across the Australia, US and Global markets – you can check out exactly how and what I invest in my portfolio on my monthly net worth updates. You need to work out which product is right for your personal circumstances though! Best of luck mate.

Just found this article today and am so happy to see your thoughts on this, silly me didn’t

t save all the articles from Blueprint as I thought we were getting them bundled together. I’ve signed up for notifications and will be having a good read around your site.

Hi Melanie,

I also did not save the Blueprint reports but saw a recent post on the Barefoot Facebook page from someone asking if it was too late to download. Scott replied and suggested an email to [email protected] and he’d “see what he could do”. So I emailed also on Wednesday night and by Thursday morning, Louise had answered with a personal temporary link to 80 of the most popular files to download. The link lasts for 14 days only and it’s much easier to download the lot in one hit- it is 2 gigabytes in total. So, not access to everything, but certainly better than nothing!

Good luck,

ps. I have just come across Captain FI too and am finding it fascinating and very helpful to increase my (basic so far) knowledge….thank you Captain!

Cheers

Awesome. thank you so much, hopefully it works, I was so devastated the site closed down and I missed downloading everything. I was under the impression we would be sent a link.

Hi,

Love your work. I have recently set up a Commsec account and have become interested in investing for my long term financial future with the hope of setting up my son financially in 20-25 years (He is currently 3) I understand ETFs and LICS are the way to go due to a DRP and dividend strategy, but I had a couple of questions.

1. Is it important to just look at the ETFs and LICs with the lowest MER?

2. What other factors are most important to look at?

3. Is it worth having a split of ETS and LICS

4. Is it worth investing in a Gold and Silver ETF also?

Would love your advice before I start investing. Would be looking to start with around 5-6k and gradually keep investing annually.

Any light you could shed would be greatly appreciated.

Hi Bret, Glad to hear your on the on the right path mate. I started out with CommSec too, but I switched to a cheaper broker in the end because the fees were killing me. I can’t provide any financial advice (I am not a financial advisor) and besides it takes a lot more information to figure out what is appropriate for someones individual circumstance than just an online forum, but I can only show you what I personally do myself – I personally Don’t invest in gold or silver, I have a core holding of domestic and international ETFs and then buy aussie LICs as well. MER is very important but not everything, you also need to consider the index its tracking, what your portfolio splits are between domestic and intl., how many stocks in the fund, whether DRP is important to you etc. It sounds like youve got a lot of reading ahead of you but luckily you have come to the right place!

Hi Captain, you said you switch to the cheaper broker because the fee of Commsec is killing you. Which broker you are with at the moment. Thanks

Hi Kate, at the moment I am using Pearler

Hi There, I was wondering why you sold VAS ?

With the low interest rates on cash & term deposits and cash on hand I am adding to my EFT’s or one EFT (STW).. Via More EFTS, (Also have AFI) I have put some cash in VAS and added to STW.. But I will need to buy more. Dividend imp is good so I like Aussie EFTs. but I am not sure if to go an intl ETF’s say S&P 500 but cautious of any others. Bit of a conundrum. I guess the other question (besides why did you sell VAS) are your thoughts on a 58 y/o looking to retire in 3 years what the ideal percentage of asset allocation (shares, cash etc) would be now until retirement for amount of $1.5m available, existing is E1m in super. & no debt. EFT’s Aussie preferably or other suggestions.

Thanks

Hey Mark! Sold VAS to buy A200, because of the cheaper management fee. We probably have very different investing requirements because of your timeframe approaching retirement. Personally, I will be holding a slightly larger emergency fund of cash in retirement (1-2 years living expenses) than I do now (6 months ish worth) but will keep the same core strategy of buying index funds, investment properties and websites.

Hi,

I have recently read barefoot investor and now keen to start investing in shares and secure our future. But i have absolutely no idea about the shares and where to start. In the book itself, it says to invest in index fund but which and how?

I am 30 years old and have decent 100k+ income. I generally save40% of my income and not where to invest it. I have also read couple of books in property investment and that looked fancy – Positively Geared and Steve knights 1 to 130 properties.

So, not sure in which exact path I should be going?

Cheers!

G’day Sandeep – Sounds like you are in an awesome position. Check out the blog guides on how to buy vanguard index funds on the blog, I have a review of a few share trading platforms too, so have a look and see which one you like. If your not confident, its probably a good idea to chat to a good independent, fee-for-service financial advisor. Check out the ASIC MoneySmart blog for recommendations about how to find one (its a government website). Otherwise just read this blog, The Aussie Firebug, Mr Money Mustache etc LOL

Thanks for the reply Captain!!

Will surely do.

Do you also recommend some books which can help me educate from the basics in this area?

Cheers!

No worries mate. Check out my reading list here https://captainfi.com/best-investing-books/ there are a few really great ones. You sound like you are off to a great start, but perhaps rich dad poor dad might be really helpful in establishing how powerful investing in productive assets is!

Thanks!! Will go through them.

👍🏻

Loving your articles!

You’ve explained the reasoning of you selling your VAS FOR A200. Can I ask, what was your thoughts/reasoning behind the shift from IVV to VTS? Thanks!

Good Morning Miss K! The main reason was to avoid ‘double ups’ which made my portfolio unnecessarily complex, because IVV and VTS essentially give me a similar exposure to the US markets. Specifically for VTS, it is a more broad index fun which holds a larger amount of US companies, and its actually cheaper by 1 basis point (.03 vs .04). I also really like Vanguard as it is a’not-for-profit’ style company which is run to benefit members. However, IVV does have benefits over VTS – it has a Dividend reinvestment plan and I think might be domiciled in Aus? Can’t remember will need to double check that. Anyway, I am happy to submit the W8 tax form through my share registry every few years and stick with VTS for now.

Hi Captain, Your thoughts on the Beta Shares QUS, in caparison to IVV & VTS and then with it changing in Dec to an Equal Weight Index S&P 500 . Management fee also being reduced to .29%.

Also sorry if you have answered this in previous threads. As a global fund is your preference still VEU over VGS, can you explain why please

Thanks

Mark

Hi Mark, I haven’t looked this up but Straight away the management fee is .29% is ridiculous given VTS is like .03%. When I googled it, IVV was 500 companies, QUS was 1000 companies but VTS was like 3500 companies. Obviously its market cap weighted so they are all probably very similar in terms of the top end (top 10 holdings). QUS looks like its changing to be similar to IVV. I think the only thing QUS has going for it, is if it might be Australian domiciled – but I am not even sure. But then if that is what you want, you’d just go with BlackRock iShares IVV, and pay .04% to get aus domicile and DRP. Seems crazy to be paying like 8 times the MER for the same thing? Also QUS only has like $61M funds under management, so its a really small fund.

In terms of global funds, I go for a combo of VTS+VEU. However, that’s because I like tinkering. If am honest, and I was doing this all over again, I would probably just have gone for VGS rather than VTS+VEU, for simplicity sake since VGS is only like .18 MER… (which is what, double that of the VEU+VTS combo?). Having the A200+VEU+VTS as the three ETFs gives me an ability to rebalance a bit better, and I am thinking of adding a small cap fund to the mix just for stamps… but not sure!

Yeah Your right.. Thanks I was thinking it was 0.029.. @ .29 it too expensive.. I will work it all out.

Hiya Captain,

Must admit, this is alllll very new to me, and I’m hoping I could get some thoughts? On a major learning curve, here – I’ve read the 2017 Barefoot Breakfree Portfolio and am keen to get started, but with things as they are (four yrs later, COVID etc.) I wonder if all of the info is still current/relevant? Like I said, new to this. I’m sort of juggling if using Breakfree as a template is where I should begin, or if I should K.I.S.S. and go for his AFIC more ‘set it and forget it’ style investing from his book to get started…? I’ve read comments above and much goes over my head, I’m embarrassed to admit. But there’s no time like the present, right!? Thanks so much in advance for your thoughts…

Hey Mate – the book has a lot of great lessons, the most powerful of which is controlling your spending and living within your means. Provided you are in a solid foundation to be investing (i.e. decent emergency fund, paid off any debt, got some breathing room / equity in your property/mortgage etc) then my personal belief is you cannot really go wrong with index funds, broad market stock index funds. I have looked at three main ETFs (you can read my Net worth reviews etc to see what I personally invest in) for global diversification, and I occasionally look to purchase LICs like AFI, ARG, MLT and BKI if they are trading below NTA because I feel like I am getting ‘free’ value (noting I then sell them when they trade above NTA and I immediately buy index fund ETFs). Ultimately the best thing you can do is just start small mate, and snowball from there. Even if you get it wrong, you will learn and thats more powerful than just sitting on the side lines

Many thanks for the thoughts and encouragement – my husband and I are looking forward to diving in!

Good luck guys! The most important thing is starting (and regularly investing)

Hey Cap,

Love the content, alot of helpful info. I have a specific question i’ve tried to get answered from several sources but haven’t had much luck.

I have no debt and no house and have been investing in ETFs on a monthly basis for a while (2 years). I’ve built 50k so far. So the question. In the next 2 years or so i plan to buy a home but i hate hate the thought of selling my shares…. As far as i see it, i have 3 options and no idea which makes more sense:

1. Stop investing now and put my savings into a bank account for the house deposit. Then only use the cash i have for the deposit in 2 years and keep my shares.

2. Sell shares at market high now and put everything into a bank account and use the lot for a bigger house deposit in 2 years.

3. continue my monthly investing strategy and at the time i want to buy, sell the amount of shares that i want for a home deposit (shares should be 100k+ at this point).

The thought of selling my shares is horrible….. but also having a small deposit obviously is not ideal at all.

Do you have any general advice for people trying to build a portfolio and a house deposit at the same time?

Thanks

Hey mate. The commonly accepted practice is if you need the money within 3-5 years to keep it as cash. I am not a financial advisor and can’t recommend you do anything, but personally I just invest everything into shares and other investments and I plan to sell off a portion of my investments to fund the deposit for the property (10+ acres for a hobby farm I am looking for). I will then probably look into debt recycling to turn the PPOR loan into a tax deductible loan, and aim to pay it down as quickly as possible using income from the shares and websites. I am still undecided about selling my *full* share portfolio to just pay off the loan in full quicker, as like you I wouldn’t want to give up all the passive income that the shares provide. I couldn’t answer it untill I am in that situation, but to be honest I don’t really like debt at all. It feels shit and I have got a $370K mortgage against an investment property I am developing and even that makes me nervous about potential interest rate rises etc

Thanks for the speedy reply! I like the sound of your method more, just sell some shares to fund the deposit. I invest 50% of my take home and have 10k cash account for emergencies. So i am not stressed about needing the money. If the markets are down when i want to buy, i will just save for another year and reassess then. The debt recycling is super interesting. It keeps coming up on podcasts and blogs recently. Will you be documenting your experience with debt recycling when it comes to it? Also, your reading list. Tough ask, but do you have a top 3? My next buy is ‘Motivated Money’.

Hey Chuck, sounds like a solid plan! I auto invest about 50% of my pay, I keep a few thousand and then I spend the rest on other investments like property or speculative things like managed funds. I will most certainly document the debt recycling journey if I embark on it, but my aim is to have a fully paid off PPOR for when I have kids. Reading list top 3 – Barefoot Investor – 4 hour work week – Your money or your life

Hi, awesome content!

I am 35 years old with a stable job and a lot of savings. Looking to start investing.

This is my first pass ever to build a portfolio.

20% Aussie market – VAS and VHY (high divided) 50/50 split.

25% US market – VTS (higher percentage because I don’t want small caps currently).

15% International – VEU (as an edge for Aussie / US markets).

20% Aussie REIT – VAP.

10% – Aussie Interest Fund – VAF.

10% – looking to invest in one of ARK etf’s.

Highly appreciate any thoughts!

Certainly looks diversified! What are your reasons for wanting to create your own portfolio, over say, one of the all-in-one funds like VDHG or DHHF? Have you had a look at them and their make up to see if that might influence your own portfolio construction?

Thank you, this is brilliant, I wasn’t aware of VDHG.

I wanted to create my own portfolio to keep things diversified.

50% VDHG, 30% VAP, 20% VAF.

Although VDHG contains a bit more aussie stocks than I wanted but that’s alright.

Hi captain

Would love your opinion on my portfolio I’m currently building.

Schd vas vgs75% int 25% aus vep and argo. What’s the difference in performance between a 200 and v a s would I be overlapping if I threw ivv Blackrock in there earlier

Thanks captain fi

Hi Captain

If you were a new investor now

What would be your combo portfolio of etfs? As a new investor currently its more difficult to decide yiur thougjts

G’day Kylie, honestly if I was starting again it would be very hard to not choose VDHG or DHHF. It is literally everything wrapped up in a neat parcel and very simple. Just simply automate purchasing it through Pearler and your sorted. I must admit though, I do like to tinker, so even the VAS/VGS two fund split would be attractive. But honestly,knowing what I know now, I would just keep it simple with VDHG or DHHF.

A200 is top 200 aussie companies, VAS is top 300. Basically the same thing, A200 just has slightly lower fees. IVV is an S&P500 index tracker, and yes VGS is 68% US funds so I wouldnt bother with IVV if you already have VGS

As far as purchasing Vanguard ETF’s, is there any downside in purchasing via the Vanguard Personal Investor Account rather than a Broker?

Hi Jack, the VPI looks like a really awesome tool. I haven’t looked at it in depth but on what Ive googled it does like good. You will just need to compare options against a traditional broker, and of course, they will heavily try to encourage you into vanguard products. I do personally like vanguards ETFs, but I like the option to buy others without penalties (such as Betashares A200).

Hey Captain Fi,

Love your content and how open you are about your financial decisions. I’m also a big fan of both Barefoot Investor and Barefoot for families too. I decided to invest in a similar way to you.. I’ve gone with A200 for myself, as well as VEU & VTS and I found out that I would pay too much tax opening up a minor account for my son (something like 66% if it was to earn more than $400 per year, which it would have) so I decided to invest his money under my name (I’m also using Pearler, like you do – so happy I made the switch from SW), and I have bought VAS shares for him, so I can track exactly what is his. I think it’s easier this way, and once he’s 18 or 21, I can transfer the shares to him.

Hi Captain!

I’ve just found your blog and find it very helpful!

My question is. I am wanting to get into the property market before the 2032 games (Im from Brissy). Ideally sooner rather than later.

I am not sure if its a smart move or not to invest my current $22’000 (which is my home deposit savings thus far) in the share market in the suggested things above first to grow my wealth to have more for a home deposit, or if I wait until I’ve secured a home deposit first (townhouses is what I’m looking at).

Which is the best direction to go if I am looking to secure a home within the next 3-5 years.

Thanks!

Amazing and simple breakdown. After a long time investing I’ve finally gotten into a portfolio I’m happy with for the long term. This includes VTS, VEU, VAS, and a few other awesome ETFs I like (ETHI and NDQ). Took me a while to have a bit of fun and finally come full circle to what actually works haha. I’ll need to think a bit more about actual percentages and weighting, but I like your noting from one of the comments on the benefits of the dividend yield for Aus funds

Hello Captain,

Thank you for your excellent analysis into the world of investing and finance. Enjoy your content very much.

I am interested to know how you deal with the tax implications from purchasing VTS and VUE.

My understanding is that if I purchase VTS / VEU, then I will be subjected to the legal and tax system of the US. The US has severe estate tax laws for non US citizens. However, Australia has a tax treaty with the US, so I can avoid the estate tax by completing W8-BEN form every 3 years. Furthermore, I believe I read somewhere that Pearl automatically lodge the W8-BEN on your behalf.

I am interested to know the ins and outs of purchasing and owning VTS/VAE? Would be great if you could point me in the right direction.

Hi Ned, yes you will need to fill out the W8BEN form every 3 years or so, I do this through the share registry. From memory its either Link or Computershare, I think Vanguard is Computershare. Log into your account on computershare and there is a section to complete the W8BEN, where you really just follow the bouncing ball. You may need to print, sign and upload, or it might even be purely electronic – I havent done mine for a couple of years you might be able to tell haha. Either way it takes under 30 minutes

Hey! I’m an Aussie, I’m 22 and about to invest in a 3-fund portfolio: 50% IVV, 30% VAS, 20% VEU. I’m going to implement dollar-cost averaging ($2000 every 2 months from my income). However, I currently have some money saved up in my bank account and was wondering if I should lump-sum it into my 3-fund portfolio or should I just add extra to my dollar-cost average or just leave it in my savings account? Some assistance would be helpful, cheers. Also, what’s your thoughts on my portfolio? Btw I chose IVV over VTS due to it being Aus domiciled and having a DRP.

Hi Patrick,

Its great that you are starting this early, you have got a great future ahead.

I was in similar position whether to dump all our savings as lump sump or DCA. Eventually I ended up going with lump sump. But thats me. Do your analysis before proceeding.