You can reach financial independence through property investing but you need to be smart about it. Let’s take a look at the pros and cons of using this asset class to build wealth.

Introduction

I hear all the time about how people have successfully used real estate investment to create wealth; from family and friends at barbecues, on television, advertising and online. The plain truth is that property is a great asset class and the principles are simple, but putting these into action to make money from it isn’t so straight forward and there can be a lot of ‘hands in the cookie jar’ taking their cut along the way. Not all debt is the same, and a mortgage can be a smart way to invest.

Real estate

When talking about property, there are two main sub classes: residential and commercial property. Residential property as it sounds is property in which people live: units (duplex, triplex more etc), detached houses, townhouses, and apartments. Commercial property ranges from offices and drafting studios, through to stock warehouses and factory sites; anything that a business can use.

Due to relatively high costs of real estate, most purchases are financed through a third party such as a bank using a mortgage. The most common type of finance is an owner-occupier mortgage for residential property, where the buyer produces a deposit and gets a loan for the remaining portion. Under this type of agreement, the homeowner lives in the property and pays regular repayments (ie the mortgage) back to the lender. These repayments consist of the principle amount loaned, plus a portion of interest agreed upon in the mortgage contract. There are many types of loans, including interest-only arrangements.

The amount borrowed is expressed as LVR: loan to value ratio, ie the amount borrowed as a ratio of the total principle value of the property. Bringing a larger deposit means you have to save up longer, but you instantly have more equity, and a lower LVR. High LVR ratios are thought of as risky by the banks, as the owner will not have much equity in the property and repayments will be higher due to the larger amount borrowed. Typically anything above 80% LVR will trigger lenders mortgage insurance – a once off payment which can be upwards of $10,000.

Both classes of property derive their value from two main mechanisms – capital growth, the ‘buy/sell’ value of the property, and rental income, the ‘hold’ value of the property (or its dividend, if you will). For more information on property investing, you can listen to my podcast with Amy Lunardi.

Cashflow

Some investors aim to achieve a positive cashflow by earning a high rental yield that exceeds the holding costs of the investment property (such as mortgage repayments, rates, property management fees etc). Other investors target capital growth to build equity (the percent of the property you own) so that they can either sell the property for more than it’s worth, or refinance a loan against that property.

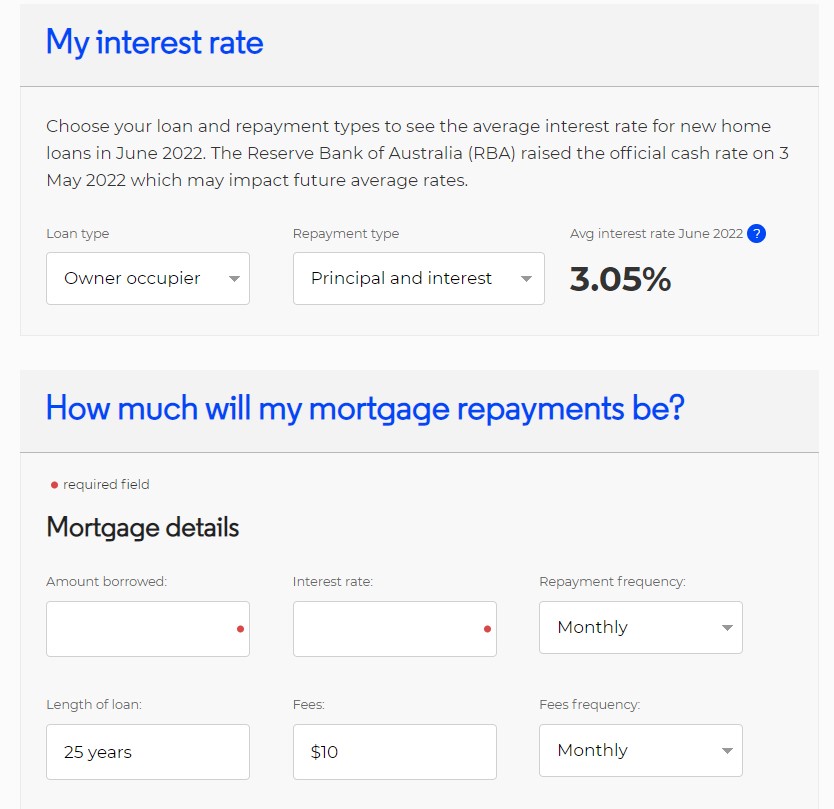

For example, follow along on a typical principle plus interest repayment investment loan on an average $400,000 family home in Adelaide, South Australia. Using a home loan calculator or a mortgage calculator we can get an idea of what investing in the following property would cost.

The Details

- House value: $400,000

- Agreed LVR 80% (to avoid LMI)

- Required deposit: $80,000

- Stamp duty: $10,000

- Bank fees, legal fees and misc costs: $3000

- Total cash upfront: $93,000

- Total home loan value: $320,000

- 30 year timeframe

Weekly Costs $449 v $424

- Mortgage Repayment (P+I 3.5%): $332

- Mortgage Repayment (Interest only 5%): $307

- Council rates / land tax: $25

- Annual bank fees $5

- Water Connection fee: $4

- Emergency services levy: $3

- Property management fee: $40

- Home insurance $20

- General maintenance costs: $20

Weekly rent: $400 (typical for Adelaide)

The Bottom line: cashflow

- P+I: -$49

- Interest only: -$24

In this situation, the mortgage calculator says both options are cash flow negative. Although the interest-only loan with a higher interest rate gave a smart investor a ‘better’ weekly cash flow outcome, it’s still negative and doesn’t pay down the value of the loan over its life – we would have to wait for inflation to slowly raise the value of the rent over time. The negative cash flow is a key concept of negative gearing; a tax minimisation strategy (avoiding payment of capital gains tax) that offsets any losses experienced on an investment property against your salary. Depending on which tier of the marginal income tax rate you are on, you could save up to $25 per week on the P+I loan (those on the top income tax tier earning over $180,000 and paying a 49% marginal rate), halving your weekly loss.

Not all property investing is cash flow negative though. By buying in an area of high rental demand, getting a good deal on the house price and subsequent finance, and negotiating lower management fees you may be able to make the deal work. As a rule of thumb, it’s a good idea to look for properties where the weekly income is higher than the total price of the property in hundreds of thousands – this is called being above the 1:1 rule. In our example, we would need at least $450 a week of rent, which you may be able to generate by renovating or improving a property. Positive cash flow is one property investment strategy where the investor is not ‘out of pocket’.

“A negative cash flow property, or what is often called a negatively geared property, is when your income is less than the sum of all your expenses – or in other words, the rent does not cover all of your costs.

This structure can offer a number of tax benefits in the form of tax deductions and is popular among investors that are making the most of capital gains. Your investment strategy will depend on your income and it is very important to talk to your accountant about the right structure for you. “

mcgrath.com.au/manage

In both loan situations, the borrower is out of pocket, so this kind of investment would be driven towards capital growth; the property owner will hope that the property market will rise. If the market rises 5% in one year, in both situations the owner stands to gain $20,000 in capital growth; this gives them equity (and lowers the remaining LVR). In this situation, they would then own $100,000 of equity; their original 20% deposit of $80,000, plus the $20,000 gain. If the investor had simply placed their $80K deposit into a low-cost index fund, they may have only generated the market average of just over $7,000 – so investments like property where you can leverage (borrow money to invest) are more profitable in rising markets.

In some circumstances, the property owner is then able to refinance, and pull this $20,000 of equity back out of the property. This could potentially be used towards a deposit for a second property (along with their income savings over that year). Others may choose to refinance over another 30 year period, in effect resetting the loan, to achieve a lower weekly repayment – potentially making the property more cash flow positive. Some people even pull the equity out to live on it, or buy a new car. You can read my article on Debt Recycling HERE.

Market fluctuations

So what happens if the market goes down? Well, homeowners and investors alike could face the possibility that their home may not actually be worth as much as their mortgage, and be stuck making their repayments. We saw this during the subprime crisis in the United States when property prices crashed. Many homeowners with high LVRs simply walked away from their properties and defaulted on their loans. Banks allow for certain percentages of defaults; hence the lenders mortgage insurance fees on high LVR properties.

Interest rates

What happens if the interest rate goes up? Here is where we need to go into a little bit more detail. The most common form of mortgage is a variable rate loan, which is a floating rate set by the bank.

The bank’s retail mortgage rate is influenced by the Reserve bank. The Reserve bank sets the ‘interest rate’ which is the rate used for overnight bank to bank loan settlements (and technically not really to do with individual investors or homeowners). The RBA uses this as a tool to control inflation which is one of the major levers it can pull to manage the economy.

Lowering the interest rate makes ‘cash’ cheaper, and banks typically pass this effect onto their customers by providing a lower return on savings account and term deposit rates (bad for savers), but also by lowering their mortgage interest rates (good for borrowers). By discouraging saving and encouraging borrowing, the net effect is an increase in spending and the economy grows. If the economy is growing too fast, the RBA can raise the interest rate to ‘put the brakes on’ to ensure economic growth is sustainable and reduce the risk of ‘bubbles’.

Interest rates were at record lows recently, so cash was cheap. Savers weren’t really rewarded, but those who borrowed to finance productive assets were the real winners in the economy. Interest rates are now rising again and so this flips the coin again.

So back to the question: what happens when interest rates go up (as they have and will continue to)?

When interest rates go up, you pay more on a variable-rate loan. Simple. There are types of loans where lenders allow borrowers to agree to fix the interest charges on the loan (or a portion of the loan) for certain periods (often up to 2-5 years) which provides more certainty for repayments, however there are drawbacks such as losing flexibility to be able to pay the loan down quicker, or take advantage of their interest rate drops. Most banks calculate your serviceability (ability to repay your loan) at an interest rate of 6.5%, alongside fairly hefty cost of living expenses. So this shouldn’t really be a major factor for most investors.

Where this becomes an issue is with borrowers cutting margins thin, on high LVR loans, with risky properties such as speculative growth, or ‘boom and bust’ mining towns. For example a mining town rental property may provide fantastic cash flow initially, which drives their price up. But once site Infrastructure is commissioned and the nature of the workforce changes from construction to maintenance (ie reduces in size) or the mine is exhausted and the workforce moves on – the demand for rentals drops dramatically, and in turn, the rents and prices drop accordingly.

“When looking for a good deal on a home loan (mortgage), the interest rate matters. A home loan is a long-term debt, so even a small difference in interest adds up over time.”

moneysmart.gov.au/home-loans

For this crowd, rising interest rates can result in mortgage stress and eat away at cash flows until the deal doesn’t work anymore, or until borrowers can’t meet their repayments where they can default on the loans; they simply can’t afford them. They can negotiate with the banks to ease the stress temporarily, or renegotiate terms of the loan if they have enough equity, but ultimately will have to sell if they don’t have cash reserves to weather the storm. These motivated sales, called distressed sales, can often be a great bargain for future investors.

So when interest rates rise, loans will generally become more expensive and increasingly difficult to get approved. This will mean less people will be able to afford to finance property; demand will fall and economics says prices will too. Still think it’s a good time to buy an ‘asset’ that takes money out of your pocket?

Types of property

When looking at investment properties or types of property in general, we have residential and commercial properties.

Residential properties also include units, such as duplexes which are essentially a house split into two residences with a common wall, and triplexes, quadplexes etc. These can be effective forms of investment as a low-maintenance rental, and depending on the titles, land taxes. These could also be townhouses, which is typically a two or three story house on a low square meter block with a very small garden or courtyard (if any). Going one step further, an apartment complex (or complex of units, flats) uses vertical extent and can have tenants living above each other. Units are typically thought of differently to freestanding houses as they don’t own the land beneath, are subject to sometimes complex strata laws etc, and there is a different market accordingly.

Commercial property is a little different to residential property. It is thought of as slightly riskier due to the more dynamic nature of business, but provided you have a stable, boring long-term business as a tenant you should be right. The basic concept is identical to residential property investing, however, the tenant is now a business of some sort looking for a place to work rather than an occupant looking for a place to live. Examples may be an accounting firm or drafting studio renting an office space, or a steel fabricator or logistics company renting a warehouse for working space.

Commercial property contracts typically are interest-only loans attracting higher interest rates (of around 5-7%) and are subject to higher fees. Contracts with tenants are ideally yearly but can be shorter or longer rolling contracts depending on the business and the economic climate. Either way, property investors will typically refinance these interest-only loans every year to manage cash flows to produce better cash flow positive income.

ASIC’s MoneySmart Mortgage calculator

ASICS MoneySmart Mortgage calculator is a great way to quickly run the numbers on prospective property deals. It’s a free tool that’s quick and intuitive to use – check it out at https://www.moneysmart.gov.au/tools-and-resources/calculators-and-apps/mortgage-calculator

Summary

A property investment purchase can be a viable alternative to investing in the stock market if you’re wanting to achieve FI (financial independence). The two can be quite complimentary strategies, and real estate gives you the fantastic option of leverage to control greater assets – which is fine as long as the cash flow works, you hold a good cash buffer and you don’t stretch/expose yourself too much.

The Australian property market can fluctuate a lot so it’s important to keep an eye on market trends, as well as interest rates and costs involved in holding a property portfolio.

Have you used a property purchase as part of your investment journey? Let us know your experience in the comments!

Just remember this is not personal financial advice. You should always do your own research and seek professional advice about investing from a financial advisor, based on your own personal circumstances.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Great post! Where else can you have an investment that provides a tax benefit every year, while your tenant pays off your mortgage, and it appreciates over time? Real Estate Investing is one of, if not the best way, for an average person to build wealth over time. Bar None!