Complete review of Plenti P2P lending from a long-term investor. Find out if this Peer to Peer lending platform is right for you.

Plenti (RateSetter) is a peer to peer lending platform which lets investors lend their money to borrowers, according to an interest rate set by the lender. Borrowers then make monthly repayments (principle plus interest) which are credited back to the lenders account. Lenders can choose how much they want to loan, the rate they want to charge, and the time-frame they want to lend the money for.

Plenti listed on the Australian Securities Exchange (ASX:PLT) and has a market cap of around AUD$180M, making it a significant company with large regulatory oversight from ASIC.

The Good

- Protection of the provision fund

- Get started investing with as little as $10

- Plenti has brokered over $700 Million of loans

- 100% of all Plenti P2P loans have had principal and interest returned

- Fully regulated and licensed by ASIC

- Straightforward to set up an account

- Listed company (ASX:PLT) which means more regulatory oversight

The Bad

- Interest you can earn depends on money market rates

- Fairly low 1 month rates

- Lenders often pay their loans out early and then re-loan the money from someone else if interest rates drop

- Must commit to longer time frames to get higher interest payments

- Auto re-invest options aren’t great – you need to log in at least weekly to keep an eye on everything and make sure your cash is on loan

Verdict: Plenti is probably one of the best-known and easy to access Peer to Peer lending platforms

CaptainFI is not a Financial Advisor and the information below is not financial advice. This website is reader-supported, which means we may be paid when you visit links to partner or featured sites, or by advertising on the site. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

How I started using Plenti Peer to Peer Lending

I was referred to Plenti by a friend who has been using the platform for several years. She has used it as an alternative to term deposits in a bank (due to banks woeful interest rates), as a form of fixed interest investment. I won’t go into asset allocation here, but depending on your personal circumstances a small investment in fixed interest is usually a smart move.

I used her referral code and got a $100 sign up bonus when I signed up and deposited $1000 into the program. I’m still getting used to how the system fully works but this is an awesome ongoing experiment I am doing in order to diversify my income sources.

The details of Plenti Peer to Peer Lending

RateSetters mission:

“To create an online marketplace which provides a straightforward and secure peer-to-peer investing facility to match Borrowers and Investors. We are seeking to change the way people think about Investing and Borrowing.”

RateSetter.com.au

Plenti was created in 2009 in the United Kingdom, and is the worlds largest Peer to Peer (P2P) Lending platform. To date, globally, they have serviced over 520,000 loans and have managed over $5 Billion worth of loans. In Australia alone, Plenti has over 18,000 registered investors and brokered over $600 million in generated loans.

The majority of their loans go out to individuals (69%), with the remaining 29% going to property developers and 2% to businesses. As such, the overwhelming majority of these loans are unsecured consumer or personal loans.

RateSetter works by matching investors with borrowers. Investors are able to choose which type of loan market they want to invest in, how much they want to invest, and what rate they are willing to accept. RateSetter calls this a ‘lending order’.

RateSetter then matches this lending order with qualified borrowers (borrowers who have met their credit requirements), with the lowest rate lending orders being matched first. This means that investors return on investment is ultimately a floating or market rate determination.

Investors don’t need to manually approve individual loans, and as such their lending order may be matched to one or several borrowers, across multiple loans.

As the borrower repays their loan, the principle and interest are credited to the lenders account. There are options for automatic reinvestment into the original lending order, which enables you to benefit from the compounding effect of the interest repayments. Otherwise you can select to withdraw the repayments into your nominated bank account, just like receiving a dividend or monthly interest from your savings account.

The Plenti (RateSetter) Provision fund

RateSetter consider themselves responsible underwriters; they have strict criteria for loan eligibility as the first line of defense. However, if a borrower misses a monthly repayment or defaults on their loan, lenders may have their investments protected by the provision fund.

In Australia, RateSetter’s provision fund currently holds over $11.5 Million, which currently represents about 6% of outstanding loans, and an estimated 162% coverage protection against suspected loan defaults.

As a first point of call, RateSetter will refer the failed loan to their debt collection agency to secure the missed payment or recover the default. Should this fail, investors may have access to reimbursement of their capital and/or interest from the provision fund.

This is an important aspect, because the majority of RateSetters loans are unsecured; debt collectors might find themselves with nothing to repossess!

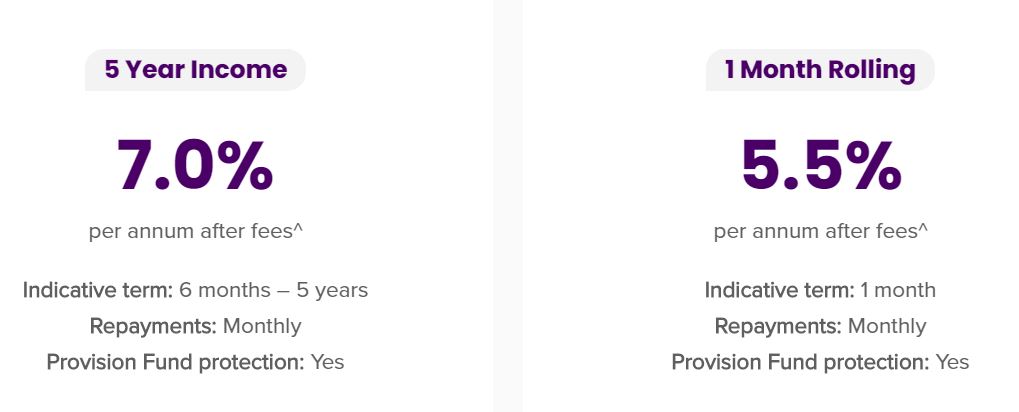

Performance of Plenti Peer to Peer Lending

RateSetter currently provides a return of about 5.5%, which is more than is currently being offered with banks savings accounts or even their term deposits. This is somewhat comparable to interests in the long term fixed interest (bond) market.

Its important to note that the 1 month rolling returns are a market rate and as investors gradually enter into the system, this will likely continue to trend downward – unless there is an increase in eligible borrowers that meets or exceeds this influx. You need to check out the Website www.RateSetter.com for the latest yield figures.

How Risky is Plenti Peer to Peer Lending?

With over 1500 positive online reviews, multiple awards and their provisional fund, my personal opinion is that it is probably one of the safer P2P lending platforms. However, like any investment, you have to realise that your capital is at risk, and you could possibly lose it all.

RateSetter have a four pronged approach to reducing risk;

- They have strict eligibility criteria about who they loan to

- They have access to a specialist debt collection agency to help retrieve missed payments or defaulted loans

- If the debt collectors fail, they have a large provision fund with the intent to protect lenders

- They undergo strict financial services audits every year to maintain their Australian financial services licence (AFSL) and Australian credit licence (ACL).

Despite their word about how they screen borrowers, loans can be both secured or unsecured, and investors have no option to choose between these types. The Provision fund is not an insurance product, and basically they will make a decision if you get repaid or not and you will have no way to challenge or redress this decision – investor beware.

My personal opinion is that it is all good while the system is working properly and everyone plays the game, but I just don’t know enough to comment what might happen if it all starts to go wrong and enough people start defaulting.

I am willing to invest a thousand for now which is a small percentage of my net worth, and as I gain more trust in the system and see returns its likely I will increase this amount.

Have a detailed scour of the Risks section, as well as the PDS to educate yourself on some more of the unique risks of P2P lending with RateSetter. Ultimately;

- You could lose your money – There is no guarantee, insurance or government protection that you will get any of your money back or be paid any of the interest on your lending order agreement.

- Missed payment or default – If any of the borrowers that make up your loan miss a payment or default, this could reduce the performance of your lending order. There is no guarantee RateSetter will reimburse you or make up the difference, although they suggest they might.

- Market interest rates could rise – If the number of borrowers exceeds the number of lenders, the market rate could rise. If you have set a fixed time period on your lending order, you could get stuck underperforming the market for the duration of your lending order.

- Your funds might be locked up – Withdrawing your capital early might not be available and your application to withdraw might be rejected by RateSetter, who need to find another lender to ‘take-over’ your loan. Furthermore, during a ‘run’ on RateSetter such as spooked investors in a crash, your funds may be frozen.

How much does Plenti Peer to Peer Lending charge?

Plenti charge a pretty hefty service fee, equal to 10% of the total interest received. This means on a standard 1 month floating loan rate of 5.5%, your investor fee will be .55%, or 55 basis points.

This is pretty hefty when compared to other money markets, but given the higher rates of return, simplicity of the process and protection of the provision fund, I think its reasonable.

There are no account keeping fees, and the minimum investment amount is $10, meaning there is practically zero entry barrier for someone wishing to learn more about finance and investing.

How to use Plenti Peer to Peer Lending

Signing up to RateSetter is pretty easy, no more tedious than a standard bank account. It is a three stage process;

- Sign up to an online account and verify your identity

- Transfer in the amount you wish to invest

- Become familiar with the system and set your lending order

- Withdrawing your earnings

Signing up to Plenti Peer to Peer Lending

Signing up is pretty simple, and takes less than 5 minutes. Just follow the bouncing ball and then verify your identify online.

Transferring money to your Plenti Peer to Peer Lending account

Transferring money to RateSetter to earn money online is as easy as completing an online bank transfer or BPAY into your account. The money usually arrives within the next business day or two, and you will then be ready to set up a lending order. I chose to initially BPAY $1001 into the fund and have been choosing the rolling 1 month reinvestment market.

Choosing your Plenti Peer to Peer Lending lending order

Setting up a lending order means selecting a lending market, setting a rate and waiting to get matched with eligible borrowers. The lending orders will get filled from lowest to highest, so essentially the lowest rate loans will fill first. This floating order ensures ‘market rate’ is paid.

If there are too many investors, this will usually drive down the market rate and lower investor returns – good news for borrowers eh?

Setting up your Plenti (RateSetter)lending order

Setting up my lending order literally took 30 seconds; I’ll show you here in four screen shots.

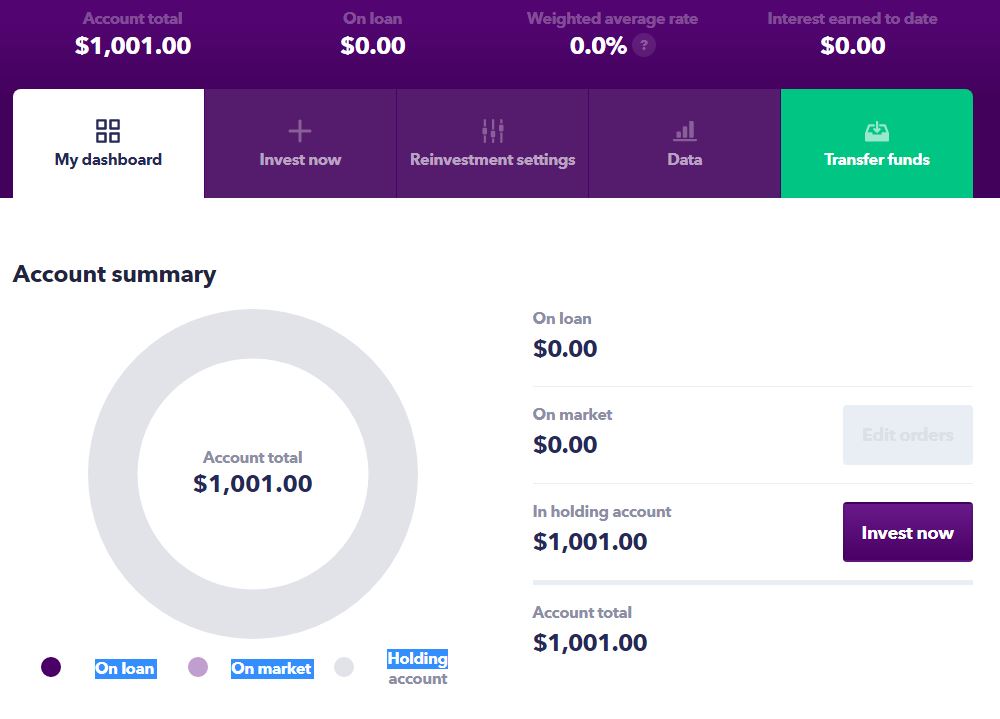

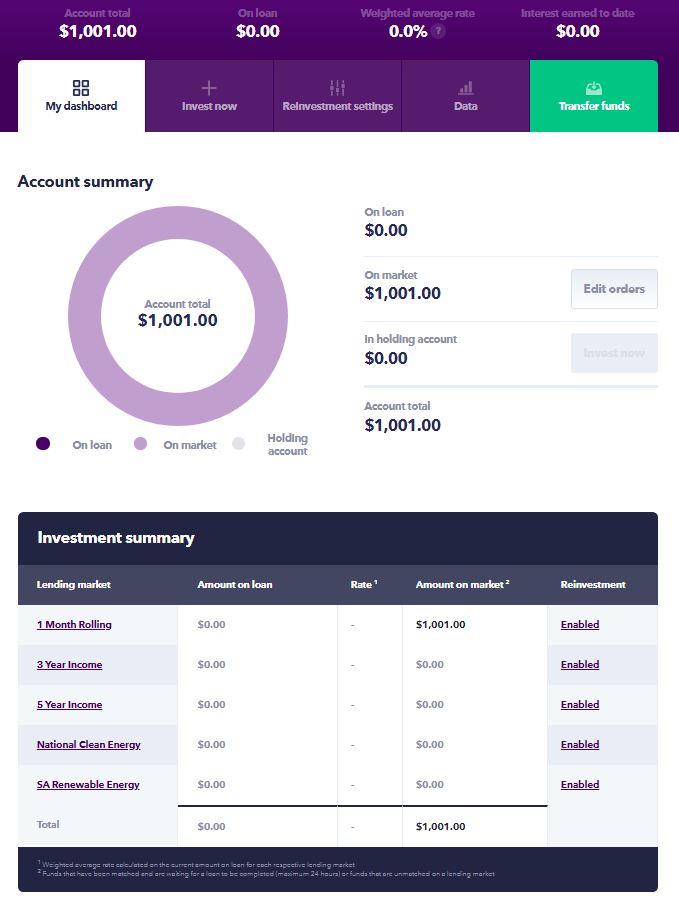

Step 1: Log in to your Plenti (RateSetter) Member dashboard (I use the beta interface)

Log into your RateSetter member area dashboard, and check your account total (top left) to make sure you have available funds. If you havent got any available funds click the ‘transfer funds’ in the top right to get details (account details and BSB or a BPAY number) to put money in. Click the ‘Invest now’ Button on the top or on the bottom right.

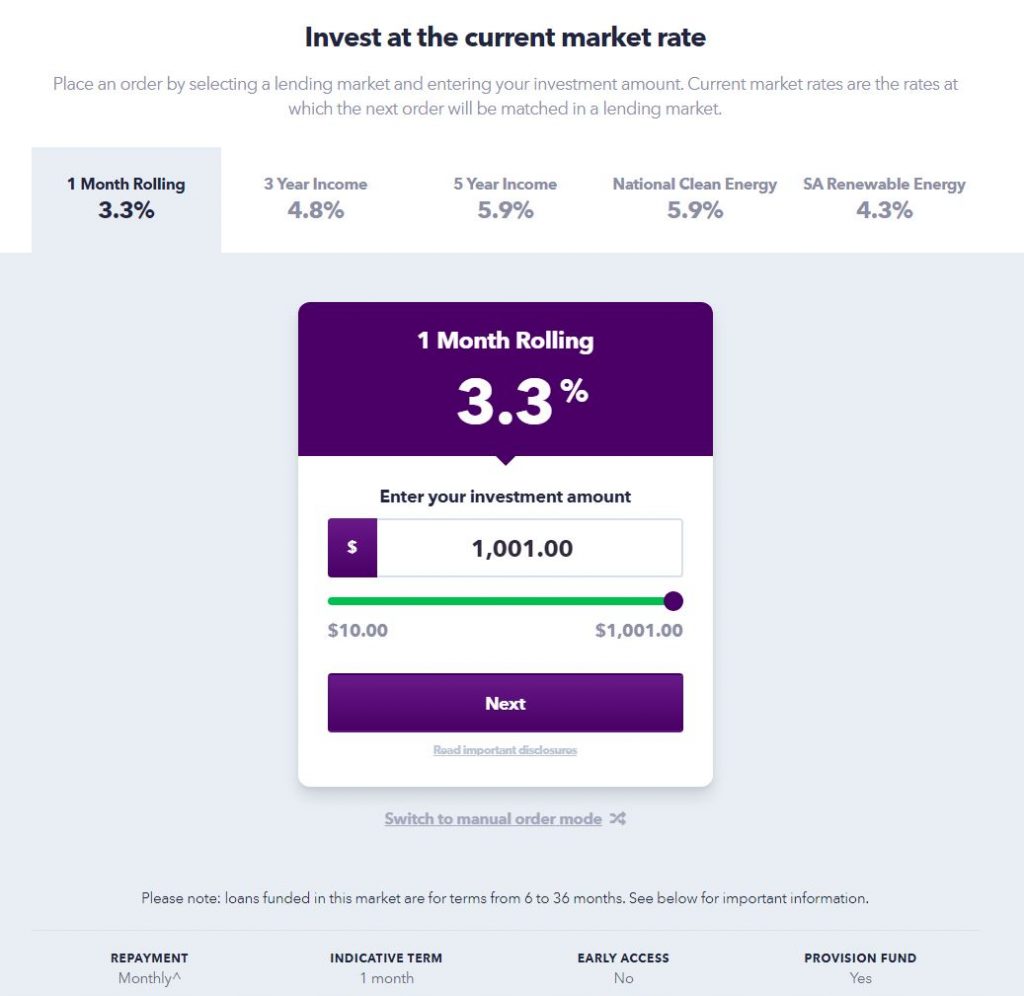

Step 2: Select your chosen Plenti (RateSetter) lending order

Once you click ‘Invest now’ the page will defaut to the 1 month rolling lending order. As you can see here, my rate is 3.3% – this fluctuates depending on whats available in the market at the time. You simply then Enter your investment amount (minimum $10) and click ‘Next’

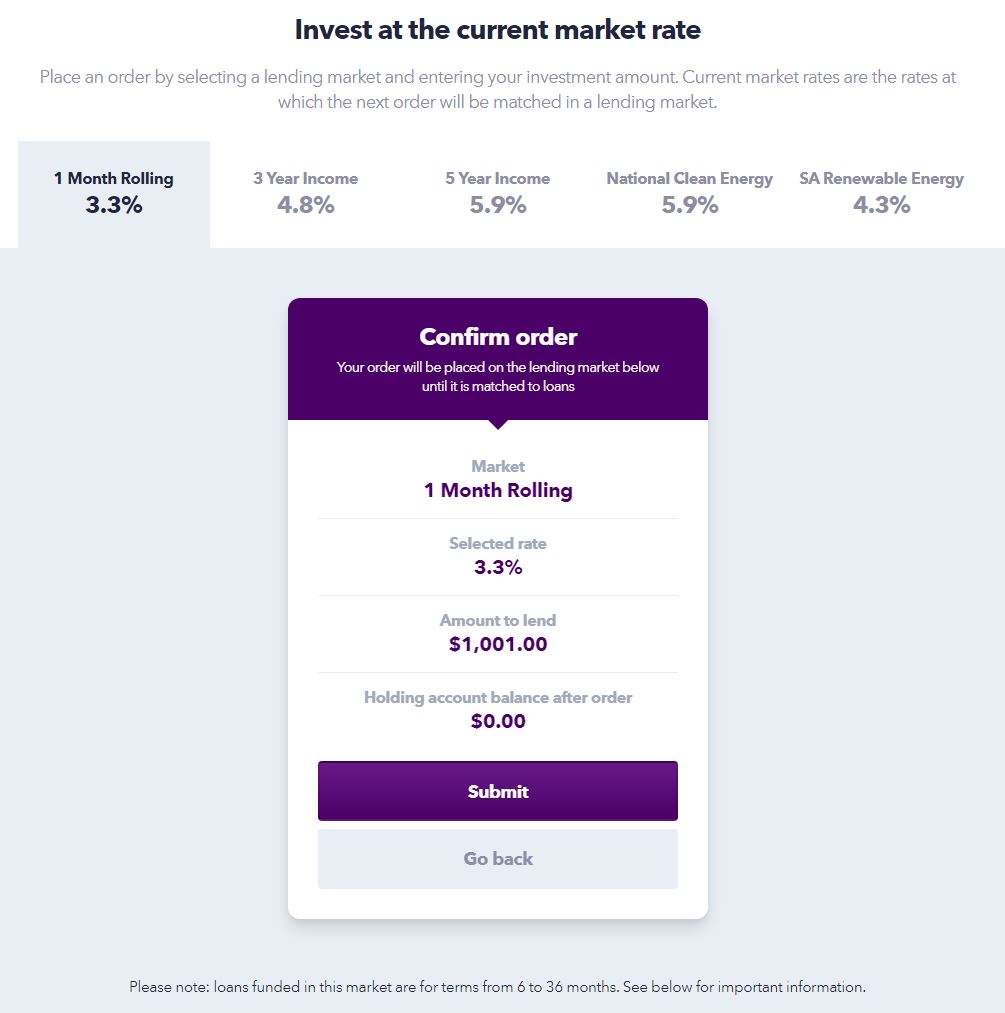

Step 3: Confirm your RateSetter lending order to list it on market

This screen is just to make sure your happy with everything before your lending order goes life. Make sure you have read the Terms and Conditions and Product Disclosure Statement before you click accept. I read them ages ago and am happy with how it all went, so I was happy to proceed.

Step 4: Wait for your Plenti (RateSetter) lending order to go on loan

Once your RateSetter lending order is on market, it then gets matched to borrowers. This process can take a while, and whilst it is ‘on market’ it isn’t earning any interest. Ideally you want it to go on loan as soon as possible! Once you get to this stage though, you just sit back and relax.

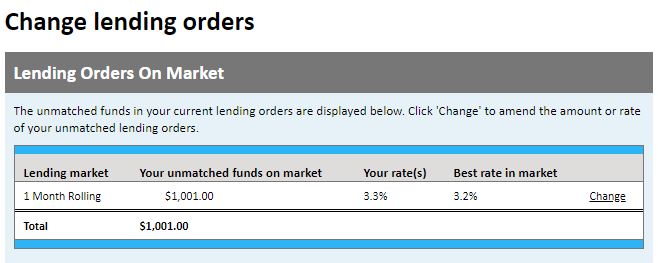

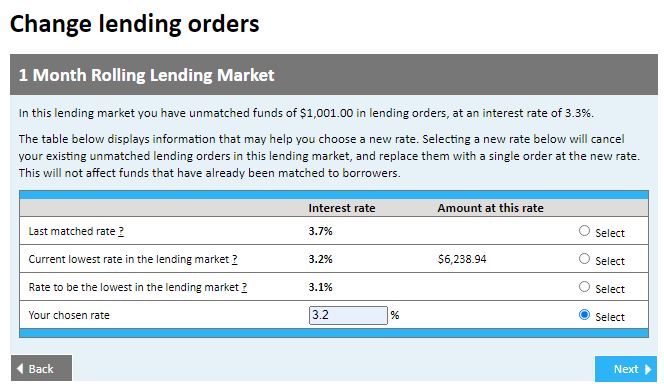

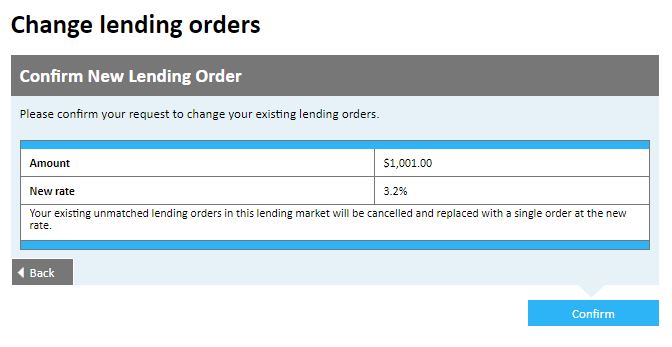

Step 5: Editing your Plenti (RateSetter) lending order so it gets matched quicker

If you really want your order to fill quicker, just like buying shares you can fiddle with the price – lowering the rate you will accept means you will be at the ‘top of the cue’ to be matched to a loan. You will get a lower return on your investment, but it will start earning you money quicker. See pictures below – unfortunately you cant use Beta mode for this and have to switch to classic view!

Withdrawing your earnings from Plenti Peer to Peer Lending

After your lending order has been matched and once your loan period has elapsed, your account will be credited with the appropriate interest plus your original capital back.

You can choose to either reinvest this back into your lending order for a ‘floating order’ (month-to-month) or simply transfer this back out to your nominated bank account.

Just make sure to keep detailed records of all transactions, because…

Frequently asked questions about Plenti Peer to Peer lending

Answers to frequently asked questions about plenti peer to peer lending.

Do I have to pay tax on earnings from Plenti?

Yes! You have to pay tax on interest you have earned from Plenti, which is classified as income for the purposes of Australia’s marginal income tax system.

In this regard, income from your lending orders is treated no differently to that earned from a PAY-G slip, dividends, bank interest or rental income. RateSetter do charge a service fee, but do not withhold tax, so it’s important that you retain detailed records to complete your annual tax return, and tuck away an appropriate amount of your profits (equal to your estimated marginal tax contributions) so you don’t get any unexpected suprises after lodging.

How much money can you make peer to peer lending?

You can typically make between 1-20% per annum peer to peer lending depending on the level of risk you accept and your agreed investment timeframe. For moderate to low risk using Plenti P2P lending, this currently ranges from 1.5-6.5% per annum.

Is P2P lending safe?

P2P lending is not a guaranteed return and your capital is at risk, it should be considered like a junk corporate bond. Plenti P2P lending have a provision fund which to date has meant over 20,000 investors who have loaned over $700 Million of funds have never been out of pocket for interest or capital repayments

What is the best peer to peer lending company?

Plenti is the best peer to peer lending company

Is Ratesetter safe to borrow from?

Yes, Ratesetter – now renamed to Plenti – is safe to borrow from. You must apply and pass all normal credit checks, and repay the money borrowed just like a personal loan or credit card.

Is Plenti safe?

Plenti is not a bank and your deposit is not guaranteed by the government deposit scheme. It is regulated by ASIC as a managed investment product, and there is no guarantee you will get a return or your capital back when investing in P2P lending through Plenti. To date however, thanks to the provision fund, Plenti has administered over $700 Million worth of P2P lending contracts with a 100% success rate – investors have never lost their interest or invested capital.

How do I withdraw my money from Plenti?

It is very simple to withdraw your money from Plenti. Simply select the ‘withdraw’ funds option and follow the prompts. I have withdrawn $1000+ from plenti and it has been in my bank within a week.

Plenti sign up code

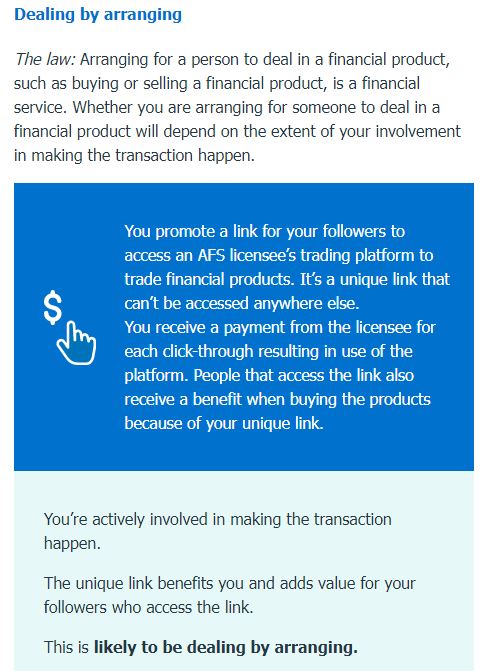

You can find an affiliate sign-up code for Plenti by Googling it, asking a friend who uses it for theirs, or potentially asking for one on most personal finance groups on social media. Due to ASIC guidance on ‘Dealing by Arranging’, I can’t provide an affiliate link for my readers anymore for any Australian investing-based services, groups or companies. However, you should still be able to get a code from another personal user somewhere online.

Summary of Plenti Peer to Peer Lending

I got involved with Plenti (RateSetter) as it peaked my interest when I kept reading about it online. As you would all know, I am a big proponent of 100% equities or as close to it as you can get, especially in the accumulation or working phase of your journey to Financial Independence.

However, cash and fixed interest does have its place in a portfolio. I always keep a few thousand dollars of cash as an emergency fund, and when I retire I plan to keep around 5% of my portfolio or about a year in cash and fixed interest securities to smooth the effect of volatility and protect my dividend portfolio from having to be sold down during a market crash.

Within this 5%, I expect to diversify this cash between bank high interest savings accounts, term deposits, P2P lending (RateSetter) and maybe even a bond index fund (ughhhh).

I plan to continue P2P lending through Plenti and exploring and learning how this system works so I know just how much I can rely on it during my retirement phase. If you sign up through a referral link you’ll get a bonus sign up of $50 which nicely boosts that first months return!

As with any financial product, always do your own research to see if its appropriate to your individual circumstances, and check out as much as you can about them online. Check out this MoneyMag review of RateSetter here

Make sure you read the bloody Product Disclosure Statement before investing a cent!

Financial Disclaimer

Financial Disclaimer: CaptainFI is NOT a financial advisor and does not hold an AFSL. This is not financial Advice!

I am not a financial adviser and I do not hold an Australian Financial Services Licence (AFSL). In this article, I am giving you factual, balanced information without judgment or bias, to the best of my ability. I am not giving you any general or personal financial advice about what you should do with your investments. Just because I do something with my money (or use a particular service or platform) doesn’t mean it is automatically appropriate for your personal circumstances. I do not recommend nor endorse any financial or investment product, and my usage or opinion of any product should not be interpreted as an endorsement, advertisement, or intent to influence.

I can only provide factual information based on my journey to Financial Independence, and that is provided for general informational and entertainment purposes only. I make no guarantee about the performance of any product, and although I strive to keep the information accurate and updated as it changes, I make no guarantee about the correctness of reviews or information posted.

Remember – you always need to do your own independent research and due diligence before making any transaction. This includes reading and analysing Product Disclosure Statements, Terms and Conditions, Service Arrangement and Fee Structures. It is always smart to compare products and discuss them, but ultimately you need to take responsibility for your use of any particular product and make sure it suits your personal circumstances. If you need help and would like to obtain personal financial advice about which investment options or platforms may be right for you, please talk to a licensed financial adviser or AFSL holder – you can take the first steps to find a financial advisor by reading this interview, or by visiting the ASIC financial adviser register and searching in your area.

For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

For our needs cash needs to be pretty much immediately available – that’s the point of cash in our household. For our needs Plenti is too clunky to fit that bill and now that the returns are not as generous it’s too much of a price to pay.

I can get the same accessibility & return (or better) by buying a monthly distributing ETF like Betashare’s CRED.

Another very thorough write up Captain – really enjoyed the read

Thanks Phil – that is really good feedback and I agree for me its just not practical to be throwing in all your money if your cash flow is an issue and you need it all available, if you can get higher yields on a bond or fixed interest ETF and have the flexibility to sell that ETF if needed then thats a pretty good solution. However something that is worth considering with Plenti IMO is the ‘annuity’ style payouts that the longer loan terms give you. I know for some people who are keen on fixed interest and receiving regular income then allocating a chunk could be useful – for example if you put $100K in on the 5+ year term at 6.5%, then you could get paid a monthly interest of $540, plus principle repayments – which is a pretty decent stream of reliable interest and something people might choose to do depending on their risk/return tolerance.

Hmm – the annuity approach is something I had not thought of – very clever thinking. I might have to rethink Plenti then. Thanks for rattling my paradigm 🙂

I actually had not thought of it either – but the clever marketing people at Plenti made sure to remind me a few times when I was on the phone to them when I said I was going to do a review and was looking for more information

I have been happy with Plenti, but can now receive good rates through Judobank which has the gov guarantee. Minimum investment $1000 for 3 months