What are the Barefoot Investor Buckets and how you can set them up to manage your budget and grow your wealth? Read on to find out

The Barefoot Investor Scott Pape is a household name in Australia when it comes to personal finance, and his Barefoot Investor buckets strategy is a really simple way to start taking control of your finances and applying some basic budgeting and cash flow management techniques to improve your financial future. By using several bank accounts to manage your income, savings and investments you can simplify and automate your finances, helping you to pay off debt and grow your net wealth towards financial freedom.

The Barefoot investor is all about helping you build financial literacy and confidence so you can effortlessly manage your finances across all stages of life. Scott makes it clear that he isn’t a huge fan of budgeting due to the time investment required for all the planning, and how inflexible they can be. Instead, he presents his barefoot investor buckets to show you how to spend less time dealing with your money whilst achieving the same thing.

Setting up your Barefoot Investor Buckets is step two of his nine step financial plan, but for some, it can all start to get a bit confusing here. So how exactly does it work – How many buckets do you need, how do you actually set it up, and what percentages or splits should you use?

“I decided to make our financial strategy so simple that I could draw our plan on the back of a serviette.”

The Barefoot Investor.

The Good

- Simple and proven money management strategy

- Provides baseline for your monthly budget spend

- Keeping emergency fund separate from daily accounts removes temptation to spend

- Automated process requires no ongoing effort

- Many online banks provide the appropriate online savings account needed to set up the barefoot buckets

The Bad

- Tedious to change all your direct debits

- Need to use multiple banks

- Not all banks will issue multiple debit cards

Verdict: The Barefoot Investor Buckets strategy is a basic budgeting and cash flow management technique with proven results of financial freedom. Setting up your buckets is quick and easy, and simplifies your money management. Check out some of the best barefoot investor bank accounts here

CaptainFI is not a Financial Advisor and the information below is factual review information, not financial advice. This website is reader-supported, which means we may be paid by advertising on the site, or when you visit links to partner or featured sites. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Introduction to the Barefoot Investor buckets

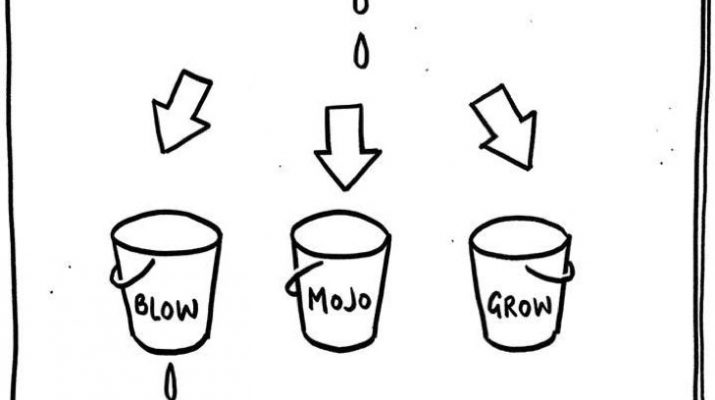

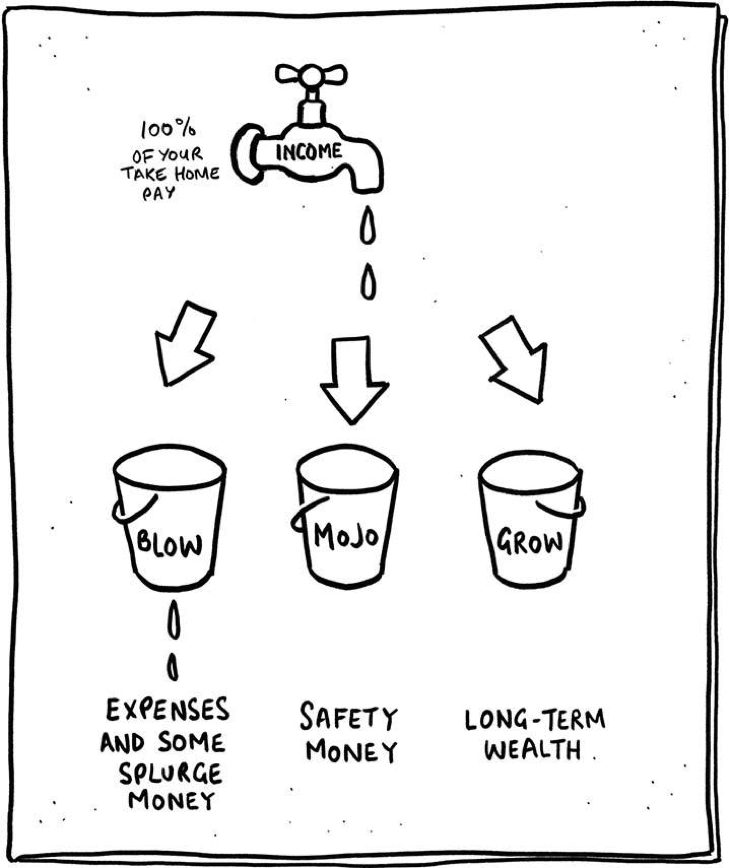

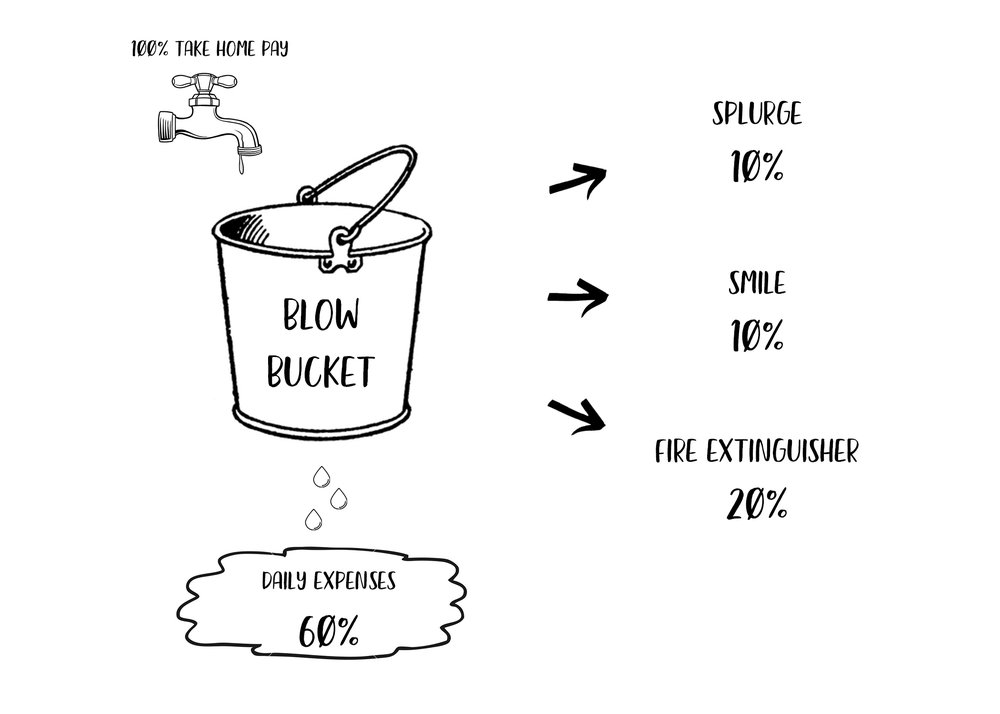

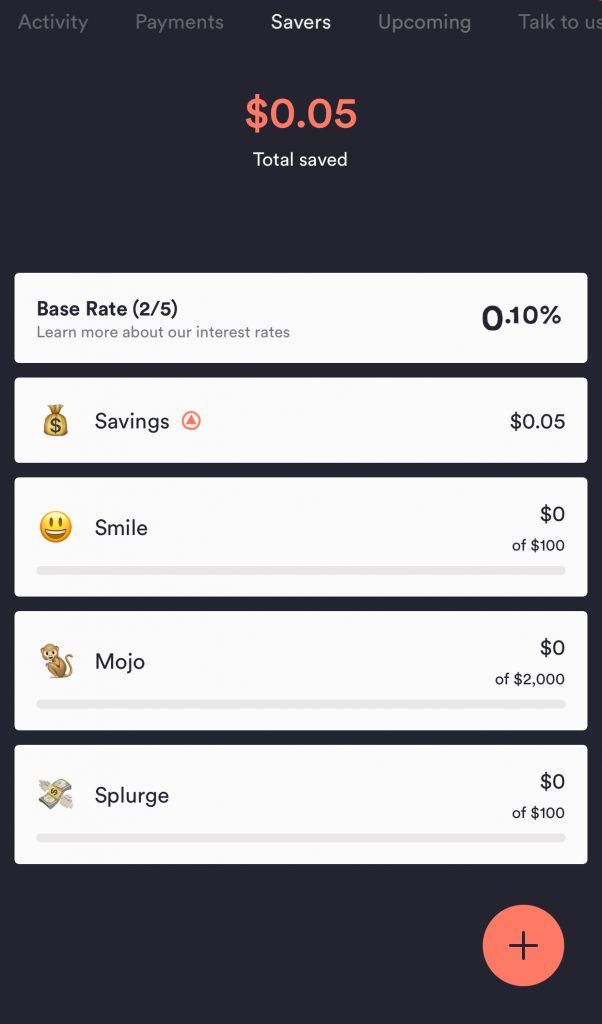

The barefoot investor bucket strategy is a great way to start taking control of your finances and applying budgeting and cash flow management to your situation to get ahead on your journey to Financial freedom. The Barefoot Investor Buckets strategy starts by splitting your regular household income into three main savings accounts or ‘buckets’ – the Mojo bucket (emergency fund), the Grow bucket (long term wealth building), and the blow Bucket (cost of living and lifestyle expenses).

- Mojo bucket savings account – Emergency fund, ‘F U Money’ or Rainy Day fund.

- Grow bucket savings account – This is your money maker or long term wealth building account

- Blow bucket expenses Account – Money that is used to live on / fund your day to day lifestyle

The Blow bucket (or expenses account) is then broken down again into four separate accounts or ‘sub-buckets’: the Daily Expenses account (your regular bills), The Splurge (goes without saying), The Smile (long term savings for things like holidays), and the mighty Fire Extinguisher account, which you can use to put out spot fires and propel yourself towards FIRE!

It is recommended that you split your three main buckets up between separate institutions – that way you cant get them mixed up. Personally I have my Mojo with ING, my Grow account with Pearler, and my Blow account with Up bank.

If you don’t get paid a regular income (maybe you get paid on a per project basis or you run a small buisness), you can do this by splitting up your lump sum payments, or if you really wanted to you could put all of your lumpy income into an additional bucket or buffer account and then pay yourself a regular income out of there – just divide your yearly income into weekly or fortnightly splits and set up an automated payment (be mindful to keep a small buffer in there so you don’t run out though).

What are the Barefoot Investor Buckets?

Lets break down the Barefoot Investor buckets into each separate account one by one

Barefoot Investor Buckets: Mojo

Your Mojo is your emergency fund. This is the simplest of all the buckets and is money you have tucked away just in case. Mojo is your rainy day fund. Mojo is your stress-free fund, Mojo is your back up plan, baby! This is single handedly the most important barefoot bucket for financial freedom.

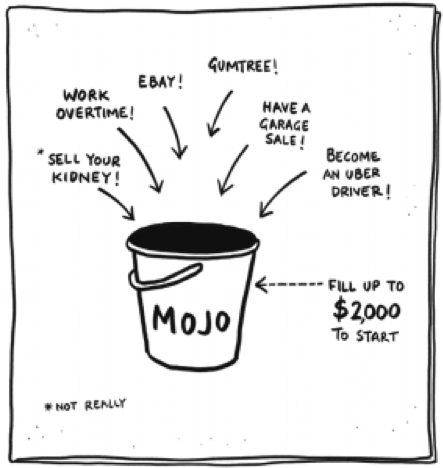

In accordance with the FIRE for beginners article, to get started you want at least $2,000 in your mojo bucket, and eventually, you want to grow it to 3 to 6 months worth of your living expenses (depending on your risk tolerance). You need to get the money anyway you can – try selling your old stuff online (a modern garage sale), or picking up a side hustle or two, such as renting out your unused car space, selling t shirts or doing online surveys.

You will learn about the ‘Fire Extinguisher’ bucket below, and you can direct this fire extinguisher into your Mojo bucket to build it up to a healthy balance in no time. Once you have $2,000 in your Mojo, your next job is directing all of your surplus cash into paying down any forms of bad debt like credit cards, personal loans or car payments which have a high interest rate (anything above 5% is pretty bad really).

Once that bad debt is knocked down, turn the fire extinguisher back to the Mojo to build it up even bigger. The Barefoot Investor suggests to at least 3 to 6 months of living expenses, but I would suggest that 6 to 12 months is a bit more of a safer or more conservative number.

You can put some of your Mojo into a long term savings account, but beware you may forfeit any interest if you withdraw it prior to the term maturing.

Barefoot Investor Buckets: Blow bucket

The Blow bucket is there to cover your cost of living. It actually gets split up into four separate smaller buckets itself, which makes it a little easier to manage your cash flows and helps you to spend guilt free.

Blow account – Daily Expenses account

recommended to be 60% or less of your total household income (Rent, Mortgage repayments, Groceries, Utilities, Petrol, Car registration, Insurance etc). Now you have an incentive to work towards – slashing those bills. The Barefoot Investor gives some great tips on how to cut your daily expenses down, including some scripts you can use with things like your phone provider, mortgage provider and utilities provider. You will also find lots of awesome tips right here on this blog.

Blow account – Splurge

10% or less of your income on impulse spending and life’s little luxuries and conveniences: Orange-mocha-frappe-chino-lattes, Date nights, small gifts and fluffy dice for your airplanes cockpit. If you have a physical card, people like to mark it with ‘Splurge’ for guilt-free spending money. The only rule is when its gone – its gone! You cant dip into other accounts for splurging!

Blow account – Smile account

10% or less of your income to save for long term goals like family vacations, a new car, Christmas or Birthday gifts, or that new kitchen renovation you’ve been wanting!

Blow account – Fire extinguisher account

20% or more of your income to be directed to paying down non productive debt – credit cards, personal loans, car loans, student loans. After that’s done, use it to boost your Mojo to three to six months living expenses, and then to boost your super contributions to 15% (of your wage) and finally, use whatever is left over to pay off your mortgage quicker. Once this is done and you are debt free, then the Barefoot Investor suggests you direct it into your Grow account to build your long term wealth. Although, you don’t always have to do it in this order (as you will find out when you read how I do the barefoot buckets…)

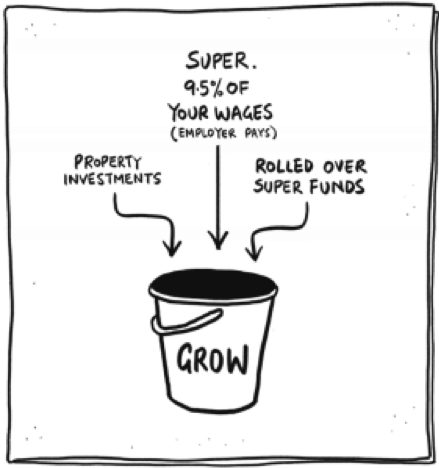

Barefoot Investor Buckets: Grow bucket

Your Grow bucket includes things like your Superannuation, Investment properties, Investing in shares through brokerage accounts or maybe even Starting up a small online business. These are all ways to grow your Net Worth.

These are all ways to grow your net worth and passive income become wealthier over the long term. Personally, I think the grow bucket should get A LOT more attention than it currently gets, because this is the bucket that will let you reach Financial Independence and Retire Early (if you should so choose to).

Your Superannuation will automatically be paid a percentage of your wages by your employer – and this figure is set to increase with governments superannuation contribution indexing in a series of increases that will bring that up to 12% by 2025. This is a great thing for workers, but The Barefoot Investor reckons we can go one better – make some salary sacrifice contributions using your Fire Extinguisher bucket to raise your personal super contributions to at least 15% of your wage. Actually, its a bit tricky to do with your Fire Extinguisher bucket, but you get the notion, right?

To increase your personal super contributuons, you can engage with a salary sacrifice company, contact your HR / payroll department, or engage with your superannuation fund directly, and of course make sure to visit the ATO to double check any rules and regulations (including potential lodgement of an intent to claim a concessional contribution to your super if relevant to you). Check with the ATO for the current concessional cap (at the time of writing it is $27,500 per year), but there are a few quirks and interesting rules to wrap your head around. If your finding it all a bit confusing, a good, independent, fee-for-service (hourly rate) financial advisor is a wise investment!

Once you’ve boosted your super to levels that will automatically provide you a very comfortable retirement in a very tax efficient manner, the Barefoot Investor recommends to use whatever remaining surplus Fire Extinguisher funds you have to fully pay off your mortgage. After that – its open slather on shares and investment properties! Be sure to check out a mortgage broker to find out the best rate possible to help pay off your PPOR and any investment property you might pick.

Of course, For those on the path to FIRE we might choose to instead invest sooner in conventional brokerage accounts and investment properties – after all, we want to build up streams of passive income that we can access earlier than our superannuation to cover our cost of living! Check out my Net Wealth updates to see how I have been investing using my Fire Extinguisher

Want to make more money to fill your buckets?

Before we go any further, if you are interested in knowing how to make more money to fill your barefoot buckets? Check out my detailed article how to make money online.

Setting up your barefoot investor buckets

There are a heap of great bank accounts that you can use to set up your barefoot investor buckets – check out Barefoot Investor Accounts: Best Online Bank Accounts for the full list of the barefoot investor bank accounts (the best online banks to use for a savings account) but for now I will focus on what I think are two of the best right now – ING Bank and Up Bank.

Barefoot Investor buckets with ING Bank

ING Bank makes it easy to set up your barefoot buckets for managing money. Once you have your account opened, you can use the online banking portal to open any number of accounts. You can create multiple Orange everyday transaction accounts which come with their own debit cards for the spending accounts, as well as a number of savings maximiser accounts for the accumulation accounts. Be warned however, you only will receive bonus interest on one savings maximiser that is linked to an orange everyday transaction account.

Mojo: Savings Maximiser (however personally many people, including the Barefoot Investor, reccomend you go with a completely different institution for this account so you aren’t tempted to use the funds in anything other than an emergency)

Grow bucket: ING do not offer a brokerage account for investing, however they do have superannuation products and offer home loans for your mortgage. I personally do not have much experience with these products and to be honest, I haven’t really heard great things about them anyway. Stick to the providers you know and love for Super and Brokerage, and hit up a mortgage broker or get Googling to find the best rate to switch your mortgage to

Blow – Daily Expenses: Orange Everyday Transaction account

Blow – Smile account: Savings Maximiser

Blow – Splurge: Orange Everyday Transaction account

Blow – Fire Extinguisher: Savings Maximiser

Barefoot Investor buckets with Up Bank

Up Bank lets you create infinite number of saver accounts which you can label, assign an Emoji to, set goals, and set up automated transfer into. They only have one main transaction or ‘Everyday account’ which will display activity on though, so it could make it tricky if you wanted to fully separate your ‘splurge’ accounts. My trick would be to just immediately transfer out of the ‘splurge’ account back into your transaction account to maintain its float.

Mojo: Saver account (however personally many people, including the Barefoot Investor, recommended you go with a completely different institution for this account so you aren’t tempted to use the funds in anything other than an emergency)

Grow bucket: Up Bank do not offer a brokerage account, Superannuation or any lending products at the moment, and to be honest – that is fine! We just want to use it as a transaction and cash account anyway!

Blow – Daily Expenses: Everyday account

Blow – Smile account: Saver account

Blow – Splurge: Everyday account OR a Saver account (and simply transfer the money before or after splurging!)

For more information directly from Scott Pape about his Barefoot Buckets, you can hit up his blog

How CaptainFI uses the barefoot investor buckets

I use the barefoot investor bucket strategy to set up my bank accounts myself – with a little tweaking, of course. It is just such an awesome strategy and such catchy names not to use! Although, I would probably refer to myself as ‘the half arsed investor’ since I am pretty lazy when it comes to finance and I want to automate and simplify this process as much as possible.

I am also not focused on paying down my debt like the Barefoot Investor suggests you do – I like the loan on my investment property and I treat it sort of like a business. Because I don’t have toxic debt, I have instead chosen to rename the fire extinguisher to my ‘fire hose’ and direct this into my Grow account (brokerage), so I can buy ever increasing streams of passive income through broad market index ETF and LICs. These provide passive income which increasingly cover my cost of living and hence bring me closer to reaching Financial Independence.

Captain FI personal barefoot investor buckets

- Mojo bucket bank account (Emergency fund): I keep a few thousand of Mojo for unexpected bills, and I can currently access over $100,000 from a mortgage offset account against the properties interest only loan. This will effectively be my new ‘Mojo’ – combination of the offset for emergencies, and cash in my savings account for day to day expenses. My current living expenses are around $40K per year, so this represents a few years worth of living expenses which for my level of income security, insurances and passive income generation I feel is more than adequate.

- Grow bucket bank account (Long term wealth like Superannuation, Investment properties or Shares) – I have previously contributed extra to Superannuation (currently rolling it over to HostPlus) however I don’t add any extra now, and instead choose to allocate all surplus funds through my ‘fire hose’ into my brokerage account where I buy ETFs and LICs to grow my net worth and stream of passive income. After IP1 is finished and refinanced, I will be using surplus equity from that and some cash from my ‘Fire Hose’ to form the deposit for IP2. Now that I have FIRE’d, my dividends and other forms of income land in here, and the surplus gets reinvested.

- Blow bucket bank account – Daily Expenses: I tried to keep this below 20% of my income – in order to maintain a target 80% savings rate (although I relaxed this a little toward the end of my FIRE journey).

- Blow bucket bank account – Splurge: 0% – I do not allocate anything from my regular income to the splurge account and to be honest, I just buy stuff whenever I want to. However, my rule is I have to find the money by selling something else, or earning the money on top of my regular income (like picking up an extra side hustle). I am pretty disciplined when it comes to spending though, and this is the only way that this will work.

- Blow bucket bank account – Smile – 0% – what makes me truly smile is having an increasing stream of passive income. That is why I don’t allocate to smile, and instead put all of my savings into my fire hose. If I really really still want something significant after a long time, I use the same strategy for splurge, and I exchange something that I already have or I put my mind to work generating extra money to afford it.

- “Blow” bucket bank account – FI/RE hose – 80% of my income was directed to growing my passive income through investing.

Captain FI business barefoot investor buckets

I also use a similar buckets approach with my “Business” buckets – My business account has got a few buckets which I use to manage business cashflows from making money online

- Income bucket – Earnings from invoicing goes here initially, where it can then be divided up into the;

- BAS bucket – GST that gets collected with invoices goes straight into here from the Income bucket to pay quarterly BAS Tax

- Blow bucket – Transaction bucket for daily business expenses such as website hosting, contractors and virtual assistants

- Grow bucket – The profit that the business makes is collected here for distribution

- Blow bucket – Tax for profits is collected here for annual tax payment – I move 27.5% of any distributions into here so I am never short at tax time

Conclusion

The Barefoot Investor bucket strategy is bloody great way to get started taking charge of your finances. Splitting your finances into these six ‘buckets’ or accounts is actually a lot simpler than it sounds, and helps you to start responsibly allocating your funds against your goals and your personal circumstances. You don’t have to apply the rules verbatim, and can adapt them to suit your needs as required – you have seen how I have adapted the bucket strategy to my ‘Half-arsed Investor’, renaming my FI/RE extinguisher to my FI/RE hose to maximise investments that grow my passive income.

Why not give it a go, and join the Barefoot cult and then level up by also joining the FIRE cult by renaming your ‘Fire Extinguisher’ into your ‘Fire Hose’ and use this torrent of cash to buy growing streams of passive income and propel yourself towards FI/RE! My pick for two of the best bank accounts to set up the barefoot buckets are either ING Bank or Up Bank, and you can read a bit more about these two banks with my detailed reviews. Setting upa savings account with them is quick and easy.

Tread your own *flight* path?

CaptainFI is not a Financial Advisor and the information below is factual review information, not financial advice. This website is reader-supported, which means we may be paid by advertising on the site, or when you visit links to partner or featured sites. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Additional Reading

Check out the following barefoot articles

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Barefoot Investor opened my eyes up a lot and I’m yet to properly set up my ‘buckets’.

I have the ING account though which is a good start and thanks for suggesting Up bank, I’ve heard of them, wasn’t sure of the exact benefits of joining them as well though..

No worries – they have been pretty good so far as a transaction account, but I think its good to have at least 2 free bank accounts so you can have one for transactions and one for stashing away your emergency fund

Good idea.. I think my EFund is too easily accessible at the moment.. haha.

haha yeah you got to keep it at arms reach… get rid of the debit card maybe and just have it like 24h to wait for transactions or something… or freeze the card in a cup of water in the freezer