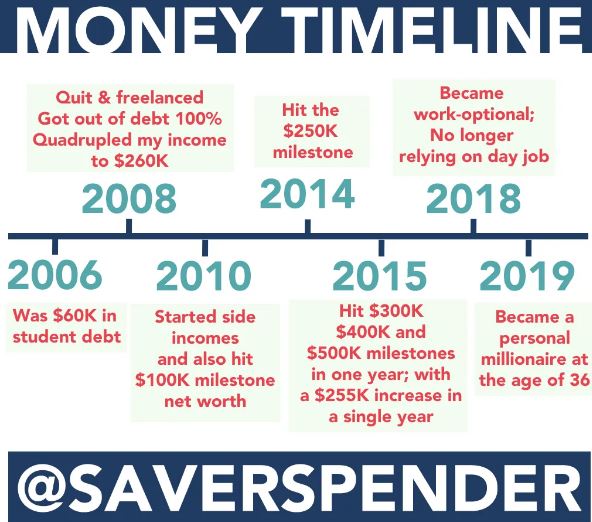

For the past few years I have been following Sherry from Save Spend Splurge on both her Instagram and Blog, and I think I might just have a little crush on her. Sherry quit her day job to become a freelancer (contractor), and in doing so wiped out over $60,000 in personal debt, quadrupled her income and became a millionaire by age 36. She enjoys living work optional, and still freelancers when she feels like it – earning hundreds of thousands per year from this and her other hobbies and interests.

“I am my own sugar Daddy”

Sherry of Save Spend Splurge

She is Financially Independent (ferociously so), insanely successful, very generous with her time and money, and also incredibly stylish. She is also an accomplished author, and shares the secrets of her success through her book series. Not only is she killing it with her own personal finance, she sets an amazing example and helps coach and empower other women to become financially independent, too! I had an absolute blast getting to know her, and working together to conduct this featured interview (and also a podcast episode in the works coming up, too!)

An Interview with Sherry from Save Spend Splurge

After back and forthing for ages over social media and email, Sherry and I thought it would be a great idea to put everything into a neat featured interview. Sherry and I actually spoke for hours on the phone which was great (and there is an awesome podcast episode coming out soon). I asked Sherry a bunch of questions and this is what she had to say

1. Can you tell us a little about your background?

I am from Montréal Canada, but grew up in Toronto. I work as a consultant in STEM (Science, Technology, Engineering, Mathematics) as my day job. Hobbies are pretty standard – I enjoy talking about, reading, and thinking about money obviously.. but aside from blogging about it on SaveSpendSplurge.com, I like fashion, reading and I am a little bit obsessed about food (eating it that is) as I like to watch all sorts of food shows, read chef biographies and food-related books and so on.

2. You quadrupled your income in 2 years, diversifying into 12+ income streams. How did you get started diversifying and increasing your income?

I started thinking about it back when the 2009-2010 recession hit. We had taken the year off at the peak of the economy to travel the world, and had a great time, and came back to an economy that crashed. I spent the next 2 years slowly freaking out, selling off investments in the red to pay for my rent and living expenses, and vowed to never ever let that happen again. When I finally landed a contract in 2012, I started building up multiple streams of income to try and see where I could just live off my side incomes & not rely on my day job.

The average advice I can give is that you have more streams of income than you think – you can apply for bank promotions (that brings about $600/year for me) when you sign up for chequing accounts, bank interest off your high-interest savings, dividends, to name 3 off the top of my head. You can also sell things, sell your services/time/skills like tutor or coach others — there are lots of ways to make money. It may be pennies at the start, like when I started blogging, but if you stick with it and are consistent, you’ll see it pay off.

3. What gave you the idea to start writing? Writing a book sounds like such an incredible hurdle – how did you do this and what keeps you motivated?

I started writing on a blog back over a decade ago called “Fabulously Broke in the City”, and I started a second major one as well called “Everyday Minimalist”. It was to chronicle getting out of $60,000 of student debt on a $65,000 salary. I ended up freelancing near the end of 18 months and I quadrupled my income and cleared my remaining debt with a single cheque.

For writing books – I just kept getting so many questions about it, I figured I should write a book to pass on my knowledge. It’s a lot of experience in my books, and I usually walk the walk first before I write about it.

To keep motivated in general – I am always thinking and I find it interesting, so it never feels like I have to work at it – it’s truly a hobby. I always have lots of ideas and I am scheduled for my blog to post daily until the end of 2020, actually. I am always thinking about money, as a hobby, and I enjoy talking about the social aspects of it especially in regards to women, more than what I call the basic b*tch stuff like what a budget is, what an index fund is, etc. I’m not as interested in those topics as I used to be 10 years ago.

4. How exactly do you publish a book? It sounds very daunting with big publishing companies and executive meetings critiquing and changing your books – how did you overcome this?

I didn’t do any of this. I am self-published on Amazon. I was originally offered a book deal and a TV show pilot back when I was “Fabulously Broke”, but I am not into publicity or fame and all of that would have meant revealing who I was, which is something I do not want to do even to this day. I’ll take the fortune, but you can keep the fame. I treasure my privacy.

5. You have been a finance and life coach to a lot of women, helping to inspire and empower them. How did you get involved in coaching and what exactly do you do for people?

I started just because people kept asking me so many questions, and it was taking up quite a bit of my time. I don’t mind helping but I sometimes have a full-time job, and definitely a full-time family on top of it, so I figured might as well be somewhat compensated for it.

I help them reach their actual potential. There are things you cannot ask or find out about in each specific, individual situation until you get into a one-on-one coaching session with someone or a couple.

For instance, a woman I recently coached was supposed to get out of debt in about 15 years based on her current trajectory. I help them get back on track either career-wise or money-wise. I will never ever shame or tell people what to do with their money. I suggest options, I lay out the pros and cons, I remind them of the risks and I let them decide on their own what is best for them. Obviously if I were in their position, I may do a lot of things differently but personal finance is personal, and I am there to make sure they skip all the BS and hard-earned learning I have experienced, and get right to the heart of the matter so they can decide for themselves. Kind of like a fast tracked, individually-created plan to financial independence.

6. Your fashion is pretty on point. You also mentioned you’d op shopped and resell as a hobby, is this something you do as an income stream?

I do resell as an income stream, but I am not 100% fixated on it. You can’t tell sometimes what will sell and what won’t. Some items I have, I thought would sell (like a cute basset hound sweater), but people either aren’t interested or want it for practically free. It’s a hit and miss, I do it for fun not really for profit.

Mainly, I resell what’s in my wardrobe I can no longer fit into (lovely dresses, skirts, etc), and try to just streamline my love for fashion (very difficult), as my tastes have changed over the years as well.

7. Can you tell us a bit about your family? I like your stories about ‘little bun’ and hope to be a father one day myself, how has being a mum influenced your finances and how do you manage finances within your partner ?

We keep our money 100% separate. I have all of my own investing and savings accounts, and he has his own. We only have joint expenses with Little Bun or household/food, and we track our spending in these categories. We split the bills fairly evenly, such as, I pay the condo fees, municipal taxes and online shopping, and he handles groceries, errands, and utilities bills (all). Every quarter or so, we reconcile our budgets together of what he spent and what I spent, and the difference gets e-transferred to each other. He usually owes me $3000 every 3 months.

We’ve gotten some flack about having separate finances but I will never do anything differently, even after we get married (which we will eventually when we get around to it). We don’t fight about money at all. Zero resentment, stress, and he doesn’t need to know that I spend that much money on fashion, massages, pedicures, etc. I am 100% financially independent with or without him and that’s extremely empowering.

As for being a mother, nothing has changed except I have to control myself from buying Little Bun ALL of the sticker books and cool storybooks I see. I have to rein myself in.

What I have picked up on, is trying to maximize his returns on his investments – we invest all of the government money we get for him into an account (we started the year he was born), and get 20% back on these contributions. I’m aiming for $100K for his education by the time he is 18 and ready for university, and he will take over managing his own accounts when he is old enough, after having read my money books. HAHA!

8. Since you are now work optional, what are your plans for early retirement? Do you have any big plans or how do you plan to enjoy your time now that you’ve bought back your freedom?

I don’t think I will ever retire. I’ve always been more free than most people, as I have been a freelancer for over 12 years now. I only work 50% of the time, so the only time I really felt stressed about money was back during that recession and while I was on maternity leave (unpaid by the way, as I am a freelancer).

Other than that, I’ve always felt freer than when I was an employee — I could choose my own contracts (with low commute times for instance), and I am very well compensated for a lot of contracts, so I was able to grit my teeth through some terrible clients.

These bad clients I stuck with, helped pay my house and car in cash, and that’s another huge relief/weight off my mind as well, as I only have living expenses to worry about.

I’ll just keep doing what I was doing before. Hanging out, waiting for a good contract, working a bit, relaxing the rest of the time… nothing changes for me except now I have mental security in never ever having to take a contract again if I don’t want to. If I stop contributing to my accounts more or less, I will have about $2.5M by the time I am 55, and more if I wait until 65.

9. What is a passion project you will be working on now?

Why women don’t invest more and get involved with money more. This is a main focus for me, so expect to see more great thought provoking content.

10. If people want to get in touch with you, what’s the best way to find you online?

My two main platforms are my Blog SaveSpendSplurge.com and also my Instagram @saverspender

If anyone wants to get in touch, Social media is great and I am often online so you can find me there, but I also answer anonymous “Ask Sherry” questions every Friday via Google Forms on my site.

Conclusion

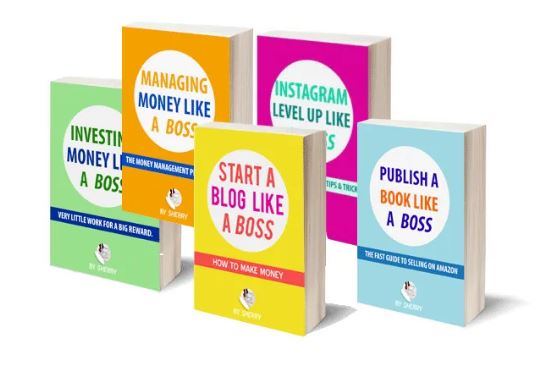

I had a blast chatting with Sherry, and I think you’ll get a lot out of checking out her blog, books and Instagram. I follow her on instagram where she posts regularly, and I also am the proud owner of her eBook series too (which was super cheap to pick up online) – these cover everything from investing, to social media influencing, to how to start a blog and make money online. I have implemented a lot of her tips and tricks, and find her a valuable source of information and coaching. Often when I get stuck on something or need a hand or to bounce an idea, I just flick her across a message online and being the generous socialite that she is, she is always happy to offer an opinion or some helpful advice.

Standy-by for an even more awesome podcast episode, where I interview Sherry about her journey and her passions, and we unpack this even deeper!

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.