You’ve read The Barefoot Investor and want a Mojo Account, but need more information on how to actually set up the barefoot investor bank accounts? Check out the best bank accounts here withthe barefoot investor bank accounts explained

Barefoot investor bank accounts

The Barefoot investor Scott Pape is known for his ‘no nonsense’ and straightforward advice in his easy to read personal finance book ‘The Barefoot Investor‘. In the Book he gives readers very simple, actionable advice on everything from how to reduce your bills, setting up your super, and of course, where the best bank accounts are. This article will delve a bit more into The Barefoot Investors account recommendations for online banks, as well as what some of the best online banks are at the moment to use for setting up your barefoot buckets.

“Do I still use the ING Orange Everyday account? Yes, I do, though there are plenty of good accounts on the market at the moment (they change all the time). However, as of June 2022, here are some that are as good as ING and possibly better, depending on the feature set you’re looking for…”

The Barefoot Investor, Scott Pape

The Good

- Simple and proven money management strategy

- No sign up or ongoing fees

- Keeping emergency fund separate from daily accounts removes temptation to spend

- Automated process requires no ongoing effort

The Bad

- Annoying to change all your direct debits

- Need to use two different banks

- Not all banks will issue multiple debit cards

Verdict: Setting up the barefoot investor bank accounts is a simple money management technique with proven results. It is easy to do with the banks reviewed below

No products found.

CaptainFI is reader supported, which means we may be paid when you visit links to partner or featured sites

Introduction to Barefoot Investor bank accounts

We all know the Barefoot Investor Scott Pape is legendary at sniffing out all the best deals and calling out companies on their bullshit deals. So what does he think about bank accounts, and what are the bank accounts the barefoot investor recommends?

The best way to get a good bank account with no fees and a decent interest rate is to go with a discount online bank, seperate from any lending products you might have. By saving on overheads like offices and front of house customer service representatives, they can pass the savings on to you by charging little to no fees and giving you a decent rate. In Australia, at the time of writing, the following are my top picks for an online bank to use the barefoot investor accounts strategy with; however with the RBA changing the cash rate, it is important to realise their rates are constantly changing. You should keep an eye out online for any changes in interest rates and fee structures.

Be warned though – there are many banks out there that offer a short introductory periods of higher interest, but these quickly fizzle out and leave you with a paltry 1% or so. That is only going to assure you lose purchasing power through inflation and taxation! There are options for term deposits too, but I would steer clear of these as you don’t typically earn much more than these online savings accounts, and your money is locked up and can’t be used in an emergency – you might be better off using this for extra mortgage repayments (or putting it in your offset account), for investing, or contributing it to your super.

Typically banks will give you a good online rate and no fee accounts on a condition though; they want you to use them as transaction accounts, have your salary deposited into them or make a regular monthly contribution to your savings accounts. This is because the bank wants you as a customer (to potentially up sell loan products or insurance to) and then they also get to access and collect to your spending information which they can add to their consumer database to sell on to advertisers, researchers and investing firms.

This isn’t really a problem for most of us though, and these transaction accounts are some of the best ones I have found – ING charges no fees ever, and provides a great exchange rate for overseas purchases, Ubank wants at least $200 a month deposit to qualify for the higher interest rate, however Rams is the only one which will penalise you for withdrawing from your savings account. These terms and conditions are frequently changing though, so make sure to read the Product Disclosure Statement to keep abreast of any requirements

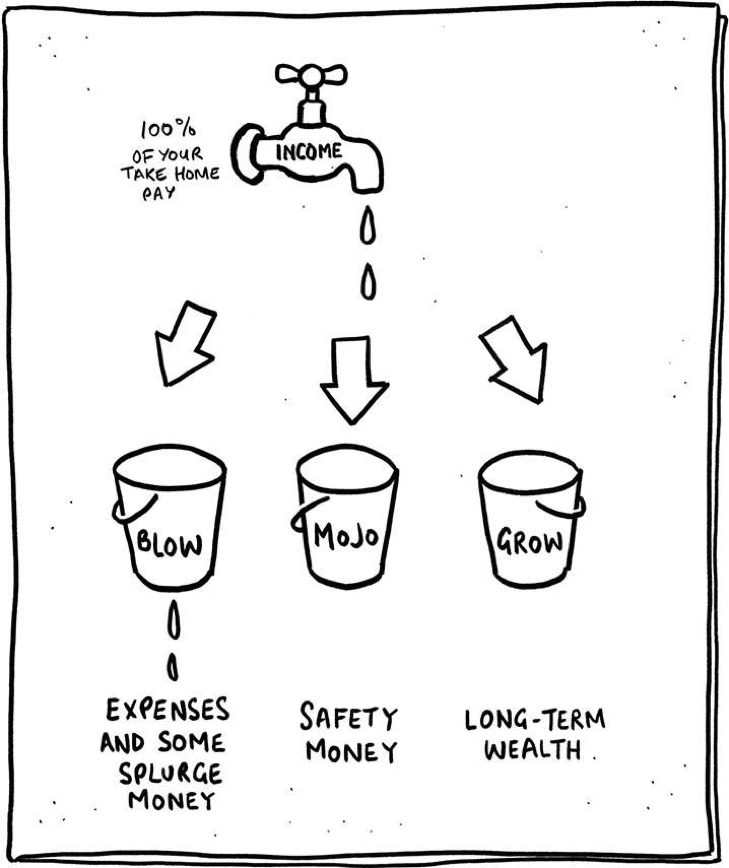

Barefoot investor buckets

These bank accounts can be used neatly to set up your barefoot investor buckets, and automate your splits (transfers). If you want a refresher on the Barefoot Investor Buckets, check out my full article: Barefoot Investor Buckets – How to set up your barefoot buckets. As a quick refresher, the barefoot investor recommends you set a budget and set up your accounts up as follows;

The first two are savings accounts where you want to park some money

- Mojo account (Emergency fund) – Savings acount

- Grow account (Long term wealth like Superannuation, Investment properties or Shares) – Savings account

The remaining four are transaction accounts which sit under the blow bucket

- Blow bucket account – Daily Expenses account (recommended 60% or less of your total income for living expenses)

- Blow bucket account – Splurge account – 10% of your income on impulse spending

- Blow bucket account – Smile account– 10% of your income to save for long term goals

- Blow bucket account – Fire extinguisher account – 20% (or more) of your income directed to paying down debt – credit cards, personal loans, car loan, saving a family home deposit (and then paying off your mortgage), and then direct it into your Grow account to build your long term wealth). This is for you to fight financial fires.

Once you have chosen your banks, open 3 fee-free transaction accounts, and 2 high-interest online savings account as shown below to set them up;

I still use my barefoot buckets, for both my personal finances and for my business accounts which I use for managing cashflows from making money online.

Want to make more money to invest?

Before we go any further, if you are interested in knowing how to make more money in order to invest towards reaching financial independence? Check out my detailed article how to make money online.

Without any further adue, the following banks provide good website and app interfaces, low or zero fees, as well as a highly competitive rates among the other banks.

ING Bank

I’ve been a personal customer of ING bank for over 8 years now, and to be honest, I couldn’t ask for a better bank. I use it conservatively (no credit cards for Captain FI just yet!) with just a couple of Orange Everyday accounts for my ‘barefoot buckets’ and a Savings maximiser for my emergency fund. I don’t think I have ever paid a cent in fees or ATM charges – and I even get a bit of interest paid out to me on the balance of my emergency fund (though it is not much at all!). This is a perfect bank for me, since I am frequently travelling the globe and need an easy way to access my cash without getting stung with hefty international transaction fees or ATM fees. ING Bank has actually saved me thousands in fees since I switched! It is quite handy for a daily expenses account and an online savings account, and you’ll definitely be noticed as a ‘barefooter’

“Flash Of Orange Bank Card Fair Indication Someone’s Been Reading Self Help Literature”

The Betoota Advocate

You can read my Full review of ING bank here.

Up Bank

Up Bank is an innovative Australian digital bank that offers entirely digital, cloud based personal banking through the Up mobile application. Because of this, and their strong focus on technology and rapid development, they are often categorized as a ‘neobank”. With over 200,000 customers, Up bank is targeted at a millennial audience and has had two years of proven functionality with outstanding reviews, winning Up several industry rewards such as ‘Digital disruptor of the year’ and ‘Best digital bank’.

I will be using Up bank more and more for my personal daily expenses account uses (but I still use my ING account too). I keep pressuring them to remove all ATM fees. When Up Bank can assure me they will remove all ATM and international transaction fees, I will happily make the full switch.

You can read my full review of Up Bank here.

UBank

I have had a U Bank account for going on 10 years now, and its been…. acceptable. These guys are the ‘no frills’ subsidiary or ‘low cost branding’ branch of NAB bank (think of them as being the NAB version of what Jetstar is to Qantas). They offer a very competitive interest rate on their online savings account, and have a very useful sweep functionality which can allow you to automatically move money from a transaction account into a savings account and vice versa, which is quite novel.

However, I will be brutally honest, the customer support is very average, their IT system sucks and the user interface is very archaic – typical of a big 4 banking system, and the opposite of newer ‘neobanks’ like Up bank. I have also been locked out of funds from my savings account for days at a time when their system goes down. When I tried to get support in person from an NAB bank branch, they wouldn’t help me. This could make a great account for sticking your mojo account (emergency) funds in to make it hard to get to unless absolutely necessary (and then keeping the linked debit card somewhere handy) but I just can’t see myself using them full time as a transaction account. Of course, if it was a real emergency, you’d probably want quick access to that cash.

They also aggressively market online for home-loans and offer some pretty amazing rates – I’m sure you are all familiar with the green advertisement bars for U Bank popping up on Google Ads or banners all over various websites and social media pages. This is something that worries me – if a product is good enough, it shouldn’t really need to waste money advertising itself – should it?

In August 2022, uBank took over 86400 smart bank (both owned by NAB) and merged to become a new, rebranded uBank using the 86400 IT systems. I noticed an immediate improvement in uBank and have not had an issue with being locked, moving money around or using the transaction card since, so I think it is a serious contender to pick to set up your barefoot accounts.

ME Bank

ME Bank, or Members Equity Bank, is actually owned by a conglomerate of 26 different Superannuation funds, which is really interesting. This includes AustralianSuper, UniSuper, Cbus, HESTA, and Hostplus. It actually used to be called ‘Super member home loans’, and has been around since 1994 where it has had a few mergers with other financial services organisations. They are also massive, managing over (AUD) $27 Billion worth of assets. They only have a few offices and follow the structure of most modern online banks, but still employ over 1800 people.

They offer competitive interest rates for online bank accounts, as well as home loans and other financial products.

I’ll be honest here – I haven’t had much experience with Me Bank at all! I opened a transaction and an online savings account when it was competitive with ING bank and I had a significant emergency fund saved in cash ($80,000!) – However, I invested this money into a mix of shares and a deposit on a property and when I realized I was only keeping a few thousand in my emergency fund, suddenly it seemed like to much effort to have multiple online savings accounts. The 12 cents per month difference in interest that I would be gaining over ING did not sway me and I didn’t want yet ANOTHER bank account I needed to keep track of, so I didn’t bother doing anymore with my account.

RAMS

RAMS are actually a bit of a strange one to add to the list but bear with me. Whilst the company is actually better known as financial services or mortgage broker franchisee service, they also offer a ‘no frills’ online savings account called myRAMS. This is actually a subsidiary of Westpac banking corporation. I have found the MyRAMS saver account to have a competitive interest rate in the past, and so I had used this interchangeably with U Bank for my Mojo (emergency fund).

Of course, these days I run a pretty tight ship, and my finances are much leaner. I keep much less in cash, and consider a mortgage offset a much better place to have my traditional ’emergency fund’ because it saves me on interest, and interest savings are tax free – meaning a mortgage offset account is always going to blow an online savings account out of the water anyday!

This means I don’t use myRAMS anymore, but it was a very straightforward online account to use. I didn’t use a linked debit card or anything – purely a place to stash my cash, but these days my small Mojo stays with ING.

Frequently asked questions

Answers to frequently asked questions about the barefoot investor bank accounts

What bank accounts does the barefoot investor recommend?

The Barefoot investor recommends looking into the following banks: ING, Up Bank, Me Bank and Ubank.

What are the barefoot investor bank accounts?

The barefoot investor accounts are a set of 6 labelled accounts to manage your money with a proven cashflow strategy. There are;

The first two are savings accounts where you want to park some money in a savings account

- Mojo account (Emergency fund)

- Grow account (Long term wealth like Superannuation, Investment properties or Shares)

The remaining four are transaction accounts which sit under the blow bucket

- Blow account – Daily Expenses account (recommended 60% or less of your total income for living expenses)

- Blow account – Splurge account – 10% of your income on impulse spending

- Blow account – Smile account– 10% of your income to save for long term goals

- Blow account – Fire extinguisher account – 20% (or more) of your income directed to paying down debt – credit cards, personal loans, car loan, saving a family home deposit (and then paying off your mortgage), and then direct it into your Grow account to build your long term wealth). This is for you to fight financial fires.

How many accounts to use Barefoot investor?

You will need six accounts, split across two different banks (to keep your emergency fund separate from your day to day finances).

What are the barefoot investor account names?

The Barefoot investor account names are Mojo account (emergency fund), Grow account (long term savings), Daily expenses, Splurge, Smile and Fire Extinguisher accounts

Barefoot investor offset accounts?

A smart way to set up your Mojo or Grow accounts are to use offset accounts on your mortgage (PPOR). This way you earn more interest and it is tax free as compared to opening a high interest savings account.

How to set up the barefoot investor bank accounts?

Setting up the barefoot investor bank accounts is just a matter of opening two seperate bank account memberships with transaction and online savings account options. Once you have opened and verified these accounts, you create two savings accounts (Mojo account and Grow account) and four transaction accounts (Daily expenses account, Splurge account, Smile account and Fire extinguisher account) and label them as such. Then set your income splits appropriately.

Conclusion to Barefoot investor bank accounts

The Barefoot Investor Scott Pape gives readers very simple, actionable advice on setting up your personal banking using the ‘Barefoot Buckets’ technique. This is as simple as opening a no fee online savings account, directing your wage into it and then automating your income to be split between the various buckets – Your Blow accounts (Splurge, Smile and Daily Expenses), your Grow accounts (Superannuation, shares and investment properties), Your Fire Extinguisher account (for paying off debt) and of course your Mojo account (emergency fund).

ING Bank and Up Bank are two of the best online bank accounts to do this with, and both make it incredibly easy – these are the two banks I predominantly use these days. Other banks to consider looking into for setting up your barefoot investor accounts are U Bank, ME bank and RAMS – I have had accounts with these banks but I don’t really use them much anymore or have closed them as they were not as competitive as the former.

Remember though, the personal finance space is constantly evolving and changing in response to new technology and buisness demands, so keep abreast of whats going on by periodically conducting a financial health check each year or so, and looking into what the latest and greatest offers are.

Financial Disclaimer

Financial Disclaimer: CaptainFI is NOT a financial advisor and does not hold an AFSL. This is not financial Advice!

I am not a financial adviser and I do not hold an Australian Financial Services Licence (AFSL). In this article, I am giving you factual, balanced information without judgment or bias, to the best of my ability. I am not giving you any general or personal financial advice about what you should do with your investments. Just because I do something with my money (or use a particular service or platform) doesn’t mean it is automatically appropriate for your personal circumstances. I do not recommend nor endorse any financial or investment product, and my usage or opinion of any product should not be interpreted as an endorsement, advertisement, or intent to influence.

I can only provide factual information based on my journey to Financial Independence, and that is provided for general informational and entertainment purposes only. I make no guarantee about the performance of any product, and although I strive to keep the information accurate and updated as it changes, I make no guarantee about the correctness of reviews or information posted.

Remember – you always need to do your own independent research and due diligence before making any transaction. This includes reading and analysing Product Disclosure Statements, Terms and Conditions, Service Arrangement and Fee Structures. It is always smart to compare products and discuss them, but ultimately you need to take responsibility for your use of any particular product and make sure it suits your personal circumstances. If you need help and would like to obtain personal financial advice about which investment options or platforms may be right for you, please talk to a licensed financial adviser or AFSL holder – you can take the first steps to find a financial advisor by reading this interview, or by visiting the ASIC financial adviser register and searching in your area. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Hey Captain,

Been reading your blog for a few weeks now. Love your insights.

What do you think of this so called 3% p.a. savings account. I’m 18 and just switched. Because I am under 21 the fees are waived. Am I missing something, is there some huge catch here. I looked into it quite a bit the only conditions are to use the card 5 times a month and make sure the savings account goes up by the end of the month and deposit $200, all things I can do.

See link below

Keen to hear your thoughts.

https://www.westpac.com.au/personal-banking/bank-accounts/savings-accounts/spend-save-ntb/?pid=iwc:tr:youth_2007::car_hmpg

Hey Daniel, I don’t think there are any catches here. This is a loss-leader promotion from Westpac to try and attract a younger demographic, which are being targeted by digital banks like Up or 86400 and the like. To be honest mate, this sounds like a good place to stash some cash for an emergency fund if you can’t put it on a home loan offset etc, 3% interest is better than the 1-2% I think I am getting in my banks. If you can meet the terms to qualify for the bonus interest then I’d say go for it. Just make sure to regularly check around and see if there are any better deals… of Course Westpac are hoping you don’t, and that you just blindly stay with them forever, and use their credit cards, home loans etc. Check what happens after you turn 21 too. Cheers