CaptainFIs financial and personal update for the third quarter of 2024

Captain FI is not a financial advisor, does not hold an AFSL and this article is not financial advice. This website is reader-supported, which means we may be paid when you visit links to partner or featured sites, or by advertising on the site. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer

Captain FI’s personal update

The past months have seemed to fly past. It has been a pretty special time for my Wife and I, as we navigate the later stages of her pregnancy. Everything has been going as smoothly as could be, and we are ready for the baby any day now.

My wife has finished up work, and we spend the days slowly, starting with sunrise and a cup of tea on the deck, and then pottering about the gardens. when it gets too hot or the UV is getting strong, we go inside to cook and eat breakfast, and then hang out with a book, watch movies or do whatever . We are putting the final things in order in the nursery and cataloging the masses of baby hand-me-downs we have received from friends and family – we still have a few bags we haven’t even opened yet!

I still have many projects on the go outside. I have slowly been clearing our fencelines of trees and bushes, and been starting to install fencing in preparation for the sheep. I was getting annoyed at constantly having to mow around trees/bushes on the fence line and there being a big build up of weeds and grass around them, so I cleared our fencelines to make maintenance easier.

It looks much tidier now, and an easy clean run for the ride on or slasher. I have also cut down a dozen large trees from around our water tanks, in order for a contractor to prepare a large tank pad so we can double our current water storage – we have 70,000L but it wasn’t quite enough to get us through last winter with the wedding and irrigating the orchard and lawns, so we are going to put another 3 x 25,000L tanks in.

Unfortunately my chainsaw overheated and seized because I hadn’t tuned it correctly – I will need to buy another $40 saw from the local men’s shed!

I have also installed about 150m of fencing as trellis in the vegetable gardens, which has been working really well for growing snake beans, pepino and cherry tomatoes, which we are still getting masses of every day. We have harvested our first pumpkins, sweet potatoes, and lots of okra and other veggies like spinach and even carrots.

7 new fruit trees went in recently, mostly different varieties of banana, but also a new type of loquat (vessel brown) and mulberry (white shahtoot). We are starting to get fruits now (6 months since the first major planting effort) and I am loving the abundance. Its hard to do though, but I mostly try to pick off the fruit just after the flowers set as I want to encourage the trees to put down good, strong roots first rather than fruiting.

30kg of honey was harvested in December for Christmas gifts, and I am about to do another few hive splits to expand the apiary.

I will need to get a dozen old motorcycle tyres soon for our dragonfruit project, as the vines are starting to get long enough to grow over the tops of the poles now, and will need the tyres for support.

Had our first ‘proper’ ride on mower breakdown and had to send the deck away to be overhauled, hopefully get that back soon as paying a contractor has been expensive!

Finally finished putting together our bushfire kit, and picked up a couple of full face mask respirators

We have been getting out on the boat a lot, after a false start to our crabbing season in October (about 6 trips with no crabs!) I made friends with a local who passed on some advice, and we have since found some good spots and with the warmer weather and a lot of rain coming through and flushing the mangroves we have done exceptionally well – two weeks of fishing and bagging out nearly each trip has meant that all of our friends and family here have all had a bloody great feed of mud crab.

I was doing some rough figures, and I think that going off the cost of mud crabs in the Brisbane seafood markets, we have pretty much paid the boat off in terms of how much crab we have eaten! We bought some mud crabs from Costco just in case we didn’t catch any because we had guests visiting, and gee the costco crabs are pretty crap and tiny size in comparison to the locally caught ones!

We also welcomed a new addition in our family – ‘Dobby’ the labrador. He is nicknamed after those big floppy ears, which somehow manage to point straight outward if he gets too excited. Well, that and the fact that the first day we brought him home, he threw up a sock!

I went for a trip down to Melbourne to get him, and whilst I was down there, I caught up with some family and friends. I visited a mates farm and got some advice on livestock and farm life while we went out for a target shoot – I was pleased to find out that even after a couple of years I am still a good shot. Later that night we went out for rabbits and the next day I tried my first eve smoked rabbit – it was great!

Unfortunately with all this effort in the property and on the water, I have overdone things a bit, and combined with a bit too much Christmas cheer (food and alcohol) I have been having some flare ups with my back and joints, so I am trying to take things easy and I suppose won’t do much till bub arrives.

Captain FI podcasts

I am setting up my podcast recording studio as we speak, and hope to put out a few episodes early this year. You can still check out the previous episodes of the Financial Independence Podcast on Spotify or now they have been uploaded to the CaptainFI YouTube channel!

Captain FI blog articles

As I mentioned, I have been slowing down with blogging while we get settled into the new place and adjust to our new life – incase you missed it, my last net wealth update is below

- Thursday, October 31 | Captain FI Net wealth Update Q3 2024

Captain FI 2024 spending figure – $144,000

As I have talked about in my last few updates, our spending has increased since we bought the farm and started our family.

We have had a deliberate lifestyle inflation, and that is ok. There are trade-offs to be made, which we are very happy to do – for example now that we are settling down and starting a family and putting down roots (literally), we won’t really be doing international travel for a while – so that previous spending we are more than happy to re-direct towards some nicer furniture, food, spending more on electricity (running air conditioners more!) and some help around the property (cleaners and gardeners).

For reference, as a family unit whilst renting in Adelaide in 2023, my Wife and I had a combined spend of just under $69,000 a year for all of our living costs (food, accomodation, travel, insurance, vet bills, etc).

Now that we have a farm, house, mortgage, and more mouths to feed, that figure increased to $144,000 for 2024.

Of that $144K, $12,400 came from my wife’s accounts and $131,600 came from my accounts. My wife has been working casually, and been regularly investing into her super and brokerage index funds.

This was a little over twice our 2023 spend, however a lot of this is related to setting up the farm and our house. Going forward into 2025, our estimated cost of living should be closer to $95,000 per year, plus whatever we will need to spend on future fertility treatments for pregnancy #2.

Expensive things I had splurged on in the first year of setting up the farm and house included;

- Home CCTV system

- Council Rates!!!! (why are they so high!?!?!?)

- Home Insurance!!!!! (again, why is insurance so expensive?!?!)

- $7,000 Pest control property termite barrier – Termidor HE trenching (lasts 10 years)

- A large, beautiful, hardwood dining table with live edges

- Brand new Super King mattress

- 85 Inch Sony Bravia flat screen and paid for wall mounting

- Bose home movie surround sound system

- Pair of nice leather couches ($500 off Facebook Marketplace!)

- High speed internet, router and Wifi extenders for the property

- Assorted tools, power tools and machinery (chippers, blowers, chainsaw, hedge trimmers, whipper snipper, brush cutter, pole cutter, jerry cans etc)

- Bushfire safety box – including full face mask respirators, fireproof overalls, boots, radio, wool blankets, first aid kit etc. Check your local fire service website for what you need to put inside yours.

- Over

300400550 fruit trees - Expanding our Apiary (7 Beehives) – investment in updating/refurbishing older equipment, replenishing consumable stock and upgrading to a larger, electric centrifuge honey extractor, purchasing AA native australian bees

Ride on mower for the house lawns and paddocksA Larger, faster, stronger, more capable ride on mower for the lawns, orchard and paddocks (which is actually currently BROKEN and I am paying a contractor to slash for me!)- A Scotty Bonnar 45 cylinder mower for the terraced lawns (yep – I’m going for that ‘golf course green’ look at the moment)

- Additional furniture and appliances for the house – a second fridge, coffee machine and TV, couches, setting up guest bedrooms etc

- Ziggler and brown gas barbecue, table and chairs, outdoor lounges and umbrellas for the pool area

- Wedding costs (including some landscaping)

- The Fishing boat, trailer, rods, tackle, new crab nets etc

- A second hand Snoo baby bassinet (Cheers to the Aussie Firebug for the recommendation, mate!), Owlet baby monitor (new), baby cameras, bottle steriliser, and various other baby paraphernalia to the tune of around $2,000 – strangely enough, this was the cost I had ‘guesstimated’ in 2022 in my research article into family planning and the cost of kids – obviously high inflation between then and now has pushed prices of new stuff up, but the second hand market is still very reasonably priced. To be fair we were also gifted about a thousand dollars worth of baby stuff too (clothes, swaddles, nappies etc).

- Several Costco shops… (I swear its not any cheaper than Aldi, but my wife loves going there)

2025 and beyond are also shaping up to potentially be somewhat expensive as we have a few major projects planned over the next few years…

- Fixing the paddock fencing for sheep

- Fencing and housing for chickens near veggie patch

- Fencing and housing in orchard for poultry (ducks and geese)

- Raising the children – Fertility, Childcare, enrichment etc

- My wife wants to go to Japan in 2025…..

- Buying a second car – we almost bought a cheaper 2010 model last year, but we think we may actually splurge on a 2020 for better features and lower mileage and just cop the price hit.

- Extra water tanks and tank pads put in

- Bushfire safety sprinkler system for the house

- New water bore to be drilled (plus pump and plumbing…)

- Sprinkler irrigation system for orchard and paddock

- Hail / fruit fly netting for orchard

- Retaining wall, slab and shed for workshop, boat and trailer.

Captain FI’s Investments

I don’t calculate a Net Wealth or Savings Rate Figure each month anymore, but I do try to keep a rough track of everything for these quarterly updates

My investments (outside super) are split across the following areas;

The ‘FIRE’ Portfolio of Index ETFs(SOLD Dec’23 to fund dream home – awaiting debt recycling to rebuild portfolio).- My primary place of residence – hobby farm / acreage in Queensland.

- Investment Property – Residential duplex in New South Wales

- My company – which runs a portfolio of content marketing websites

- Cash (mortgage offset accounts)

- A small Angel Investment in the investing platform Pearler

NB – A while ago I ended up divesting in various things such as RoboAdvisors, Micro investing funds, Managed funds, Metals/resources, and a few other speculative investments or experiments I had invested in, in order to simplify my finances. I had racked up a complex mix of investments as I wanted to try out and review various investing services but this became unmanageable in the end and I needed to simplify my life.

In December 2023 I also sold off the ‘FIRE’ Portfolio (mix of Index ETFs) to fund my dream acreage purchase, but I will be rebuilding this to build passive income through debt recycling over the next 10 years to reduce our families reliance on my business and my wife’s income.

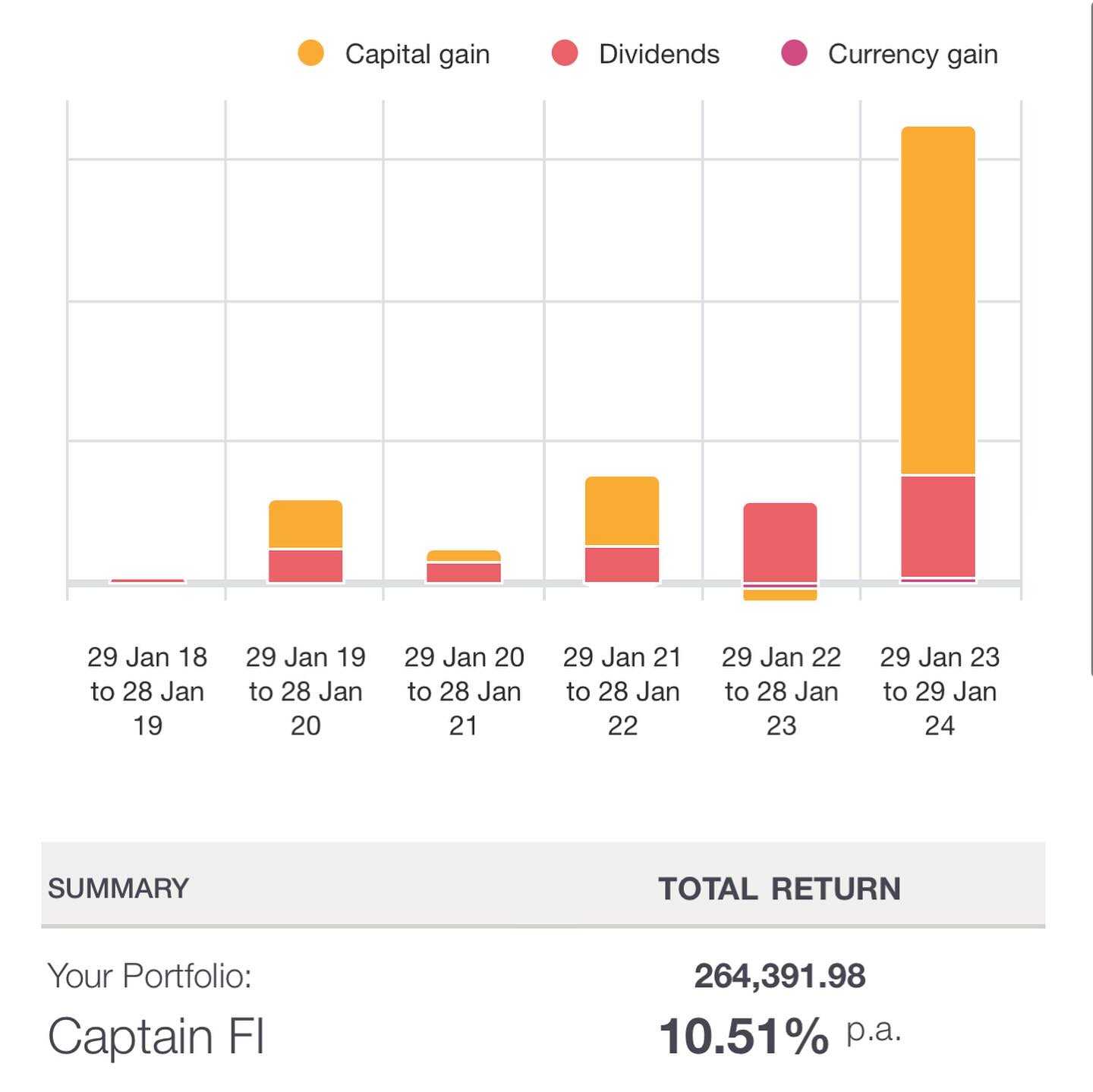

The ‘FIRE’ Portfolio (Exchange Traded Index Funds)

As you may have known, my ‘Financial Independence Retire Early’ ETF Portfolio was a simple, passive share portfolio split between three parcels of low-fee, index-tracking Exchanged Traded Index Funds (ETFs) to achieve global diversification.

I began switching to this passive index approach to investing in 2018, firstly by adding new contributions, and then over time by divesting in other assets (individual shares, managed funds, LICs etc) and rolling the investments over to it.

- I tracked my share portfolio using Sharesight, which means my portfolio accounting and tax reports are completely automated.

This was sold in December 2023 to fund the acquisition of a hobby farm, after six years of passive index fund investing. Going forward I will be first building up cash again for an emergency fund in the mortgage offset, and then when we are ready to invest I will be redrawing from the mortgage to invest (debt recycling) using something like the Betashares DHHF ETF which is an ‘all-in-one’ ETF in order to keep things simple.

Cashing in the chips with a total return of 10.51% was a good feeling. I know the market has continued to grow in the six months since we have sold, but you know what, I achieved what I set out to do which was to become financially independent and retire early from the rat race / grind, and buy my dream acreage to start hobby farming and raise a family. I will get some skin back in the game with the share market soon!

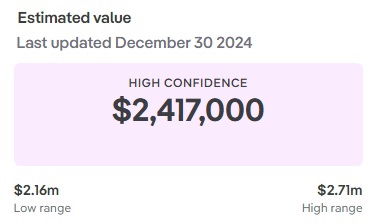

Captain FI’s PPR (acreage)

To keep things simple, I just value it as a residence only and use an online valuation tool. The current PropTrack automated online valuation estimate is $2.417M, which is down $19,000 from the last time I checked it for the Q3 2024 net wealth update, but still $64,000 less than I paid for the property.

As I said last time we probably did overpay for the property a bit, but the Aus property ponzi scheme does seem to only go up, so it shouldn’t really matter, right? LOL.

I still owe $765K on the PPR mortgage, with $265K in the mortgage offset account for a net mortgage of $500k (6.39%) of which I pay $1250 weekly repayments.

Opting to pay $1250 weekly, instead of $5000 monthly repayments shortens our mortgage by SIX years – from 29 years remaining to only 23 years. This is because I am making one whole extra monthly repayment per year ($65,000 vice $60,000 per year), and paying off chunks sooner means less interest is due.

Additionally, keeping the cash in the offset account reduces the total interest due, saving me around $1400 a month in interest, which goes to paying down the capital. Because this is a debt and not income, it isn’t taxable – it is effectively like getting a 9% return on the money, risk free (6.39% grossed up for tax). The net effect is reducing the remaining mortgage from 23 years down to 12.5 years!

Debt recycling plans

I eventually plan to use the money I currently have in my offset account to pay down the loan, and then immediately re-draw it as a new loan soley to be used for investing (this process is called debt recycling). I will be leaving a six month emergency fund in the offset account though, for peace of mind, which I will aim to grow to 12 months or around $100k.

Despite my love for the VTS/A200/VEU split, I think I will probably just use something like the Betashares DHHF or Vanguard VDHG ETFs as the investment vehicle for simplicity sake.

Assuming I kept the mortgage for the full remaining 23 year term, if the investments grew at the average long term rate of 10%, inflation remains within the target range of 2-3%, and assuming I make ZERO further debt recycling contributions, they would be valued at $2.17M, which would be approximately the equiavalent worth (buying power) of $1.228M in todays (2024) dollars, adjusted for inflation (assuming a 2.5% inflation rate).

Which I think is pretty awesome share portfolio to have alongside a paid off home – that portfolio alone could reasonably kick off just shy of $50K a year income (in 2024 dollars purchasing power) which is probably enough for us to live off with a paid off home and produce from our farm, especially when you add in future superannuation, business income etc.

In practice, there would be a cross-over point where the remaining mortgage balance (both tax and non-tax deductible loan portions which are being paid down) would be the same as the dollar value of the growing share portfolio, and one could potentially just sell the shares (keeping in mind any tax due on CGT) if they ever needed to wipe out the remaining property debt. Good for the sleep at night factor!

I had a bit of a play around on https://debtrecyclingcalculator.com and assuming I debt recycled the tax savings (around $3500 a year) once a year, and comparing that to my mortgage amortisation documents (where I see how the loan gets paid down over time) then it seemed like that crossover equal point for me was the 11.5 year mark – which is pretty bloody exciting – and that doesn’t even include any additional debt recycling contributions I could potentially make along the way too which would speed it up further.

Unfortunately, debt recycling is just not as attractive for me now that I am not a high income earner as it used to be, and now interest rates are higher. .Furthermore, even just keeping that cash in the mortgage offset account massively speeds up the mortgage being paid off because it offsets a big chunk of interest – and due to the compounding interest effect, having that money in the offset early on helps a lot.

Using the ASIC moneysmart calculator shows that just keeping the money I was going to debt recycle in the offset account actually reduces the mortgage life down to 12.5 years – a 10.5 year reduction, and only one year longer than the debt recycling option, but with none of the market risk. Its actually a pretty hard decision to make, which is probably why I have been dragging my feet on executing this plan.

Captain FI’s Investment property

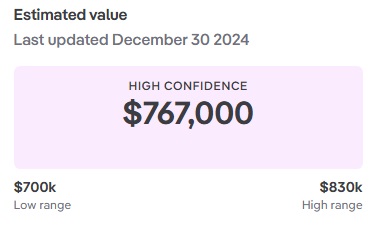

The current PropTrack automated online valuation estimate is $767K, which is up $36,000 from the last quarters estimate. The property has a $530K mortgage (6.39%) attached, for an equity position of $237K. I have seen some similar properties being advertised at the $850K mark lately, so it will be interesting to review the sales figures over the next quarter.

I have a small offset of a few thousand (to help manage cashflow for property management expenses) and pay $850 weekly repayments for the loan, and collect $700 weekly in rent. Other costs (insurance, rates, water, sewage, property management) adds up to about another $50 a week, so at the moment it costs me about $200 a week or $10,400 a year to hold.

This means it is negatively geared (which is annoying for someone who is trying to be retired) but the interest and other costs are tax deductible, and that combined with the depreciation schedule does give me something for the tax return – although I am not a high-income earner anymore, so I don’t get much back. I remember an advisor telling me” don’t let the tax tail wag the investment dog”, so I am not too worried – the capital gains are amazing.

The goal of the Investment Property is to build wealth (diversified outside of super, shares and the farm) through the capital growth of the property. Over time, it will also become positively geared and provide us a source of income. The current estimate is that the cross over point should be in a couple of years (2027 or 2028), however rents seem to be rising quickly with inflation and our real estate agent told us that similar properties are getting $750 a week already.

We obviously want our investment to do the best possible, but we also value having a good relationship with our tenants so they look after the place and we have less turnover – so we are happy to have it rented out slightly below market value.

With my current income, it’s not really possible to refinance due to serviceability issues – but if I could, I would access the equity to buy shares.

I would also have preferred an interest only loan as we would still be gaining equity with the capital growth of the property anyway as the housing market continues to grow over time.

For this reason, I don’t put much money in the IP mortgage offset – a few thousand dollars only for cash flow management.

I have previously written a full separate article on the IP build if you want to know more about the process – CaptainFI’s residential property development investment.

Captain FI’s Online Business (website portfolio)

I have a small website portfolio of content and affiliate marketing sites. These make money semi-passively from display Advertising through managed ad networks such as Adsense and Mediavine, and affiliate programs such as Amazon Associates and other direct affiliate deals.

I need to do more work on this and get some more income coming in!

The overheads are pretty low – just some software subscriptions, my Virtual Assistants, and the cost of producing content – either writing it myself or subcontracting it out and paying specialist writers and editors

I’ve written a pretty detailed article here about how to make money online, and I recently published a few more articles about how to start making money online for beginners, as well as an ultimate list of blog income reports for anyone wanting a peek into the industry.

I have been pretty slack with the business because I’ve got a big chunk of savings so I don’t really have the fire lit under my ass anymore. I think some of the sites I am just sick of working in that niche and its just not as interesting to me anymore.

I have actually since sold a number of my smaller sites, and am just focusing on the larger ones which are more of passion projects for me. This is probably for the best as I’m just going to end up neglecting them anyway – someone else can take them over and grow them with the enthusiasm and time/effort investment needed.

I have a couple more for sale around the $5,000 mark, depending on how established and how much time, money and effort I have put into them. They range from 3 to 6 years old, with various backlink profiles, number of published articles, and traffic. You can check out this article on website operation if you are keen as I’ve listed all the details in there. Feel free to send me an email through the contact form or get in touch on social media if you are interested in buying one.

I originally learned these skills through the eBusiness institute over the past 5 years – I have done a pretty comprehensive review of the eBusiness institute as well as interviewed Matt and Liz Raad about this on the podcast again recently where we go over a huge list of frequently asked questions about online business if you want to learn more about this. They also provide some free introductory training for CaptainFI readers.

Check out these podcast episodes for more information

- Podcast | Q and A Session with Matt Raad – Part THREE

- Podcast | Q and A Session with Matt Raad – Part TWO

- Podcast | Q and A Session with Matt Raad – Part ONE

- Captain Fi Podcast | Online Business with Matt Raad

- Podcast | Digital Marketing with Richard

- Podcast | Entrepreneurship with Liz Raad

- Podcast | Digital entrepreneurs Matt and Liz Raad

I have also recently finished the Authority Hackers TASS (The Authority Site System) Course as well as the Making Sense of Affiliate Marketing course which has been a cool way to consolidate the skills I have learnt from the eBusiness Institute, and I have published a few comparison review articles such as Authority Hacker vs Making Sense of Affiliate Marketing and eBusiness Institute vs Authority Hacker which might help you choose between training providers.

Angel Investing

I have a small ‘Angel Investment’ in the Financial Independence brokerage platform Pearler. This was the maximum allowable private investment of $10,000 (AUD) made in July 2021, with the total number of ‘private equity’ shares based on their June company valuation.

I am not tracking the exact company valuations for Pearler, but I know the company has had its valuation more than triple and has raised over $10m through VC funding rounds, with more to be raised in later rounds, so I assume the shares are worth a bit more. How much exactly, though? I am not sure.

Cash – Mojo and emergency fund

Cash reserves are high at the moment – $265,000 in cash waiting to be debt recycled through the PPOR home loan. As I said, with the interest rates being so high at the moment, its actually not a bad idea to just keep the cash parked there – ultimately I do want to deby recycle, so I will eventually get around to it soon.

After Debt recycling, I will look to build back up to 12 months worth of expenses in the offset account, which is probably around $100K (including my mortgage repayments) for the sleep at night factor.

Captain FI’s Net Wealth progression

During my journey to FI I roughly documented my net wealth progression via monthly updates and a graph which was rather crudely constructed in Excel. It demonstrates the ‘somewhat exponential’ journey over my 14 year ‘working’ career. You can access the archives for my Net Worth updates here to see how it’s gone over time. Check out the graph and all the updates below to see how it has gone since the beginning.

When I FI/RE’d, I stopped putting out regular net worth updates and stopped calculating my net worth, and tried to just put out quarterly ‘updates’ but I was pretty slack. I am trying to keep up with quarterly tempo, and recently calculated my net worth after selling shares to buy my dream farm (hence the lack of data points on the graph below lately).

| Date | Net worth | Difference | Saving Rate | Notes | |

| Jan 09 | $5,000.00 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK | |

| Jan 10 | $24,000 | +$19,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 11 | $40,000 | +$16,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 12 | $92,000 | +$50,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 13 | $130,000.00 | +$38,000 | ? | Estimate NWbased on historical Super, Bank statements and assets at the time | LINK |

| Jan 14 | $161,000.00 | +$31,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 15 | $200,000.00 | +$39,000 | ? | Estimate NWbased on historical Super, Bank statements and assets at the time | LINK |

| Jan 16 | $281,000.00 | +$81,000 | ? | Estimate NWbased on historical Super, Bank statements and assets at the time | LINK |

| Jan 17 | $340,000.00 | +$59,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 18 | $482,000.00 | +$142,000 | ? | Estimate NWbased on historical Super, Bank statements and assets at the time | LINK |

| Jan 19 | $542,000.00 | +$60,000 | ? | Estimate NWbased on historical Super, Bank statements and assets at the time | LINK |

| Jul 19 | $578,900.00 | +$36,900 | 84% | Finally began tracking NW this like a proper adult. | |

| Aug 19 | $560,100.00 | -$18,800.00 (-3.2%) | 78% | Share market slight correction, Ok savings. | |

| Sep 19 | $584,744.88 | $24,644.88 | 72% | Share market rebound, savings rate not so good. | LINK |

| Oct 19 | $600,386.00 | $15,641.12 | 84% | Good saving this month. Normal salary, plus allowances, dividends from index funds, tax refund, eBay selling and was working abroad in asia where things are cheap. | LINK |

| Nov 19 | $612,917.21 | $12,531.21 | 76% | Falling short of my savings goal of 80%. Mostly domestic legs this month with higher costs. Also invested in hydroponics. | LINK |

| Dec 19 | $625,350.00 | $12,432.79 | 76% | Good savings of cash (for development) and investment, however higher spending due to Christmas period (Travel and Gifting). | LINK |

| Jan 20 | $865,212.00 | $239,862.00 | 55% | Super settlement was a HUGE boost to NW. $9K growth from stock market. Expensive month lots with lots of unexpected bills – weddings, travel, Booking flights, fines etc. | LINK |

| Feb 20 | $851,802.0 | -$16,592 (-1.9%) | 52% | Large increase in spending on myself this month, still managed to tuck away $5K to put into shares and property. Corona Virus market scare resulted in a correction and gave NW a small negative trend. Time in the market not Timing the market! Became Single again. | LINK |

| Mar 20 | $819, 354.6 | -$31,806.95 (-3.7%) | 80% | Another small step backwards in the NW due to the ‘corona crash’ in full swing. FIRE Portfolio of ETF/LICs down about 15% this month, however due to high savings rate and structure of my superannuation annuity the NW is only down 3.7%. Savings rate good at 80%, higher than usual income (with some slightly higher spending, too). Picking up shares on discount – this is the best outcome for someone in the accumulation phase with good income! | LINK |

| Apr 20 | $847,023 | +$27,668 | 85% | $11,000 in rebound of stock market capital prices alone (up 6%), plus first quarter dividends paid (heavily reduced due to banks withholding dividends). Great savings rate due to COVID-19 lock-down = no spend. Increased entrepreneurial efforts and selling down of physical possessions provided side hustle income. Two standard paychecks from flying activity; domestic day trips only so no allowances. All cash unfortunately had to go into the property development due to contract timing, I am chomping at the bit to buy some more index funds before they go back up in price too much – hence why I am selling most of my toys! | LINK |

| May 20 | $857,859 | +$10,836 | 92% | Some Great sales as I let go of my Super Sport Motorcycle, Some gym gear, expensive flying equipment and a few other various bits and bobs and invested this money. Flying still reduced, but increasing from April. The share market grew as I continued to make my fortnightly investments. I also wrote down the ‘value’ of some of my possessions (liabilities) such as my car, tools and furniture by around $10K to align them to market price (“tell him hes dreaming…!”). | LINK |

| June 20 | $858,650 | +$791 | 90% | Small Net Worth gain as I continue to declutter and simplify my life, despite being off work due to a family emergency. Share market not doing much. | LINK |

| July 20 | $888,218 | +$29,568 | 68% | Majority gain due to share market going back up, low spending due to being on the family farm and at home because of lock down. | LINK |

| Aug 20 | $1,029,293 | +$141,075 | 74% | Became a millionaire. Achieved this massive milestone I set out for myself in Dec 2019. Included unrealised gains in my property development as well as website business. Good savings rate due to not much spending, invested in Aus and total world shares. Investing in my web business. Starting to shift focus away from $$$ and more into looking after my mental health. | LINK |

| Sep 20 | S1,045,486 | +$16,193 | 60% | Officially took time off work for the rest of the year to be close and look after family during major operations. Continued to sell down physical possessions and work on digital business while at home. NW gain mainly due to valuation of websites. | LINK |

| Oct 20 | $1,064,399 | +$18,913 | 80% | Base income (retainer) and leave loading, dividend and websites provided income, as well as raiding my P2P lending capital. Significant bill for property due to design not meeting standards which effectively lowers my equity position, as well as fence being stolen. | LINK |

| Nov 20 | $1,143,433 | +$80,394 | 82% | Big gains came from share market growth (influencing both the Financial Independence share portfolio and Invested superannuation), Business gains (due to increased earnings) and a $30K boost to my annuity thanks to me logging in and checking the fine-print on the accumulation stats. I only invested around $7K. Insane that in one month, I accumulated nearly more net worth than I did in four years from 2009-2012 | LINK |

| Dec 20 | $1,152,920 | + $9,487.32 | 84% | Share market slight drop, Earnings from Business, Contract work, Selling possessions. No share market investments this month (oops! I forgot and money was tight). Invested a lot into the website business this month (way more than planned) and it is still running at a decent loss (plans to turn it cash flow positive in 3 months). | LINK |

| Jan 21 | $1,165,678 | +$12,757 | 79% | Great returns from the share market. Earnings from Business, Dividends, Flying wage, flipping items on consignment. Regular share contribution, investing in micro investing platforms, P2P lending, Investment property and big reinvestment into the business (still running at a loss) | LINK |

| Feb 21 | $1,135,272 | -$30,406 | 76% | Significant write down on property development due to council DA rejection and redesign requiring more money and creating less equity. Offset by small increase to Business value and investments. Simplified my investments and switched over to Pearler. | LINK |

| Mar 21 | $1,155,594 | +$20,322 | 71% | Continued investment into the portfolio as well as growth of investments and business. Gave my notice at work and looking for part time job at home for ‘Barista FI’ | LINK |

| Apr 21 | $1,242,220 | +$86,727 | 74% | Property development back on track | LINK |

| May 21 | $1,379,469 | +$137,248 | 72% | Massive gains in the website portfolio due to revaluation based on recent business income, big growth of superannuation due to annuity increasing (salary increment) and shares generally went up. Crypto went down by about 40% or so. | LINK |

| June 21 | $1,469,989 | +$89,757 | 41% | Quit flying role and moved to Adelaide. Great month for investments, websites producing serious income so accordingly they are valued higher. Spent a lot on furnishing the new apartment and on enjoying some more luxuries. Seeing a therapist to help deal with anxiety from leaving work. | LINK |

| July 21 | $1,543,959 | +$74,732 | N.A. | Set myself up in Adelaide. Did basically nothing for the whole month except spent time with family, relax, sleep and go to doctors appointments. Massive boost to website portfolio AdSense and affiliate incomes, as well as general share market performance. | LINK |

| Aug 21 | $1,624,116 | +$70,156 | N.A. | Relaxed again, focused on mental and physical health, and spending time with family and my partner. Big increases to spending (too afraid to calculate a ‘savings rate’) but also big increases to NW through website portfolio income growth. Finally got the slab poured on the investment property (foundation). | LINK |

| Sep 21 | 1,640,663.85 | +$16,547 | N.A. | Stocks, super etc went down, but business income from websites increased, plus business valuation increased. Property build. got to frame stage, and I also got a dog! Expenses for vet surgery well worth it. Moved into a nicer apartment | LINK |

| Oct 21 | $1,705,907 | +$65,243 | 30% | Big boost from website valuation due to securing new affiliate contracts for recurring income, shares went up nicely. No massive changes to this month. Calculated a savings rate and found myself pretty low due to spending a lot on my garden and going out quite a lot – I don’t think I will calculate this savings rate figure any more. | LINK |

| Nov 21 | $1,739,144.23 | +$33,236 | – | Great month. Relaxing (somewhat). Spent a lot of money doing ‘fun’ things like winery tours, a fine dining experience and self education. Shares moved sideways (well slightly down) but everything else went up. Building got to enclosed stage (roof, walls, windows and doors) but have had some issues with build quality and weather / covid delays. Put a $1000 deposit on the puppy. Stopped tracking Savings Rate. | LINK |

| Dec 21 | $1,764,516 | +25,372 | – | Spent nearly the whole month with family, did some work on the website portfolio. Traffic recovered from google algorithm changes. Invested $10K into Stockspot and Sixpark, $1K into ACDC, $100 into Comsec pocket and $100 into Bamboo, $260 into BTC, $4K into ETFs through pearler. Paid the $3000 balance for the puppy. | LINK |

| Jan 22 | $1,826,633 | +$62,117 | – | Stock market slightly down, Massive boost to website traffic (overall its more than doubled). Invested $10K VTS, 2K VEU through pearler, Paid for Angels cancer surgery, bought more BTC and ETH, bought a parcel of ETHI on commsec pocket. | LINK |

| Feb 22 | $1,757,210.57 | -$69,422.93 | – | Stock market down, Website business revenues down and additional spending on content and staff for business, Additional property development bills, some unexpected expenses, Wrote down the value of some of my personal property (and gave stuff away). | LINK |

| Mar 22 | $1,701,410 | – $55,799 | – | My last ‘regular’ monthly Net wealth update as I give notice at work and finish up my non-flying job. | LINK |

| Q3, 2022 | Over $2M | N.A | – | Six months of Early Retirement in Rest mode! I stopped tracking my net wealth post-FI, my dog passed away, I gave away most of my physical stuff and moved to become my mums live-in carer, met a lovely girl, bought a puppy. Had some incredible months with semi-passive website income but overall neglected the business and regular (stable) revenues decreased. | LINK |

| Q1, 2023 | Over $2M | N.A | – | One year of Early Retirement! A lot of (sad) changes, the passing of my mother and family feuding resulting in temporary homelessness, selling my ‘nursery’ of plants, and traveling overseas for a few months. Finding a new home to settle, couple of domestic trips flying to Tasmania and Queensland a couple of times, and plenty of camping and road trips within SA. Did not work much on the business at all and lost a few more contracts and had to cut staff. | LINK |

| Q2, 2023 | Over $2M | N.A | – | Getting back on top of things with podcasting and blogging more regularly. Focusing on building our ‘rich life’ and deliberately increasing spending in areas such as food, travel and convenience. Did a few interviews and went on a few podcasts. | LINK: CaptainFI Q2, 2023 Net Wealth Update |

| Q3, 2023 | Over $2M | N.A | – | Big focus on health and fitness, fixing diet and losing excess weight. Continue to sell a few websites from portfolio and focus on largest ones. Attended some FIRE events and lots of road trips | LINK: Captain FI’s Q3, 2023 Net Wealth Update |

| December 2023 | $2.26M | N.A | +$260K (21 months since last calculated) | Interim calculation due to share sales prior to purchasing property – no update published | No update published |

| Q2, 2024 | $2,417,426 | 12% – Calculated to see where we sat | +$157,426 (6 months since last calculated) | Mid year 2024 Net Wealth update. Sold shares, crypto and 5 websites, Purchased the farm in Queensland, received $250K inheritance, significant cost in setting up the property. | LINK: Captain FI’s Q2, 2024 Net wealth update |

| Q3, 2024 | $2,485,000.00 | N.A | +$67,574.00 (3 months since last calculated) | Q3 2024 update. Lots of spending on wedding and bought a boat, preparing to debt recycle. Properties saw great paper gains. | LINK: Captain FI’s Q3, 2024 Net wealth update |

| Q1, 2025 | $2,482,000.00 | N.A | -$3,000 | Q1, 2025 update. Write down of business valuation due to reducing income. PPR valuation estimate down, IP up. Slowly paying off debt. Farm life is great! |

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.