Dividends vs Capital gains (Thornhill vs Boglehead) investing strategies explained. Is one better than the other? Let’s look at each strategy in detail..

Capital growth investing also referred to as “growth investing” or Boglehead investing (named after the late Jack Bogle the founder of Vanguard investing) is a style of investment in which the primary goal is to achieve capital appreciation in the capital asset by holding stocks for an extended period of time. This strategy involves purchasing shares of companies with strong potential for long-term growth, and long-term capital growth investors receive special tax treatment.

Dividend investing also referred to as Thornhill investing (after Peter Thornhill, a champion of Aussie Industrials shares) is a style of investing that seeks to generate income by holding shares in companies that regularly pay dividends. It generally involves buying stocks from companies with strong financials, consistent dividend payments, and an ability to sustain those payments over the long-term. Dividend investors are typically looking for steady income rather than capital growth.

In Australia, index investments are typically geared towards producing strong franked dividend payments due to the large portion of banks and industrials (mining) in the index. Frank credits are simply a tax mechanism given to investors to prevent ‘double taxation’ on dividends that company profits have already been paid on.

But what’s best for your journey to FIRE? Should you follow the Thornhill approach for increasing franked dividend streams, or the more traditional Boglehead approach?

Quick Verdict: Investing for capital growth typically produces the highest long-term total portfolio return performance and provides the most tax-efficient income source for retirement, as you can time the capital gains event to correspond to a favorable tax situation, and as a long-term investor you receive a 50% CGT discount. This allows your portfolio to essentially grow tax-free (tax-deferred), without losing money to tax payable on dividends. However, this can cause anxiety due to volatility and the requirement to sell – from a behavioral psychology aspect, there are significant benefits to investing for dividends and seeing a growing passive income stream of stable, franked dividends. In the real world, sensible, diversified investing usually means a combination of both investing styles.

CaptainFI is not a Financial Advisor and the information below is factual review information, not financial advice. This website is reader-supported, which means we may be paid by advertising on the site, or when you visit links to partner or featured sites. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer

Dividend vs Capital gain investing

Consider the case of someone earning up to $18,200 in investment income from their FIRE portfolio. Person A receives this from fully franked high dividend yield LICs. Person B receives this by selling some of their ETFs which rose in capital value (and because they are tax savvy, they only ever sell parcels that they have held for over 12 months so they get the 50% CGT discount).

The dividends are essentially taken out of the company’s total capital pool, so according to a rational market theory spending dividends vs selling off shares should make no difference – however taxation and brokerage are two factors to consider. Modern brokerage with low cost ‘flat fee trades’ such as Pearler or Stake eliminates one of the costly variables, so tax advantages/minimisation is going to be the major driver of which strategy to use.

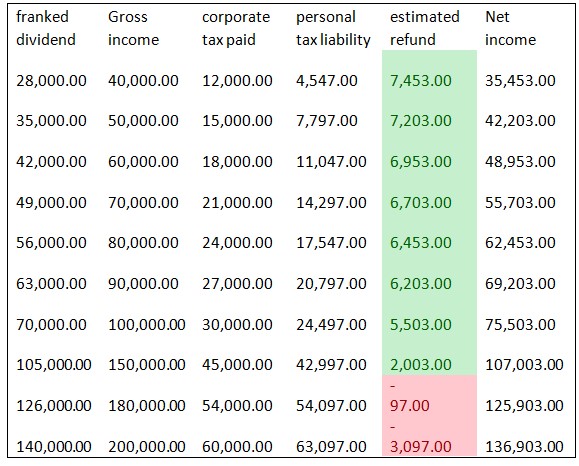

Previously, my current Aussie LIC and ETF holdings on average are returning around 4.5% in fully franked dividends (around 6% if you gross it up due to franking credits), and the remaining growth in capital value of the share (share price increase) of 5%. The LICs tend to have more dividend yield, and the ETFs more capital growth. If you chose to spend all of those dividends, you would be exceeding the 4% rule, so I still want to reinvest some of them where I can. If you spend them all, you’d potentially over time start chewing down on your portfolio – which is not an issue if you have planned for this, and also have superannuation and low living costs in early retirement. I calculated I could draw down my FIRE Portfolio quite conservatively by around 7% for it to last me the 25 years until I reach preservation age for my super.

Dividend yield investing – Thornhill method

Person A using a Thornhill approach has amassed a FIRE portfolio of about $492k of an Aussie LIC and receives $18,200 in fully franked dividends (3.7%). Those dividends paid have already been taxed at the company rate of 30% so $5460 of tax has been paid on them. This means twice a year, they have had $9100 hit their account (most LICs distribute biannually) to live on. When they file their tax return at the end of the financial year, because of the franking credit their total taxable income was actually $18200 + $5460 or $23,660 (thanks to the 5.2% grossed up dividend yield), but they’ve effectively already paid $5460 in tax.

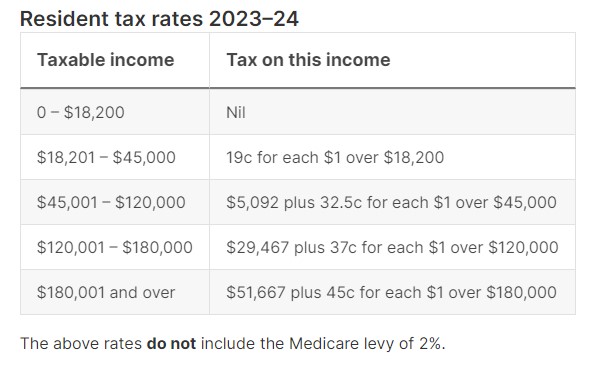

As per Australia’s marginal income tax rates they must pay 19c for every $1 they earn over the tax free threshold of $18,200, meaning their adjusted tax bill is only $1482. Since the companies already paid $5460 in tax on their behalf, person A is entitled to a franking credit tax refund of $3978 – a tidy amount, which boosts their effective after tax / net dividend yield to $22,178. Person A has also got some capital growth on that portfolio (the average performance of ETF and LICs is a total return of 10%), but you can’t spend capital gains as easily and we already have 5.4% in grossed up dividends.

Since we know that the 4% rule is a pretty safe bet, if you wanted to stick to drawing on your portfolio according that rule, you’d actually want to reinvest most of that sweet tax return for future years when the dividend isn’t as strong. If the future dividend was lower and your bills needed paying, you could just sell down a small portion of that portfolio so that your total expenditure is in line with the 4% rule. Obviously a strong cash buffer of around 1-2 years expenses could also help to absorb some of the system shocks and iron out volatility.

To put numbers to the case above, the simplest tactic is to just reinvest ALL of the tax refund, which means you would be living off the ‘3.7% rule’ which is more conservative than the 4% rule, and so your portfolio should be ‘safer’. But if you wanted to adjust your spending in line with the 4% rule after your tax return for the purposes of figuring out how much investments you need to reach financial independence, you could spend some of the tax return on living costs. For example, 4% of person A’s portfolio is $19,680 – the difference ($19680-$18200) being $1480. So the remaining $2500 of the tax return should be invested back into the portfolio.

You can use this argument to work backwards to see how franking credits can reduce the amount of capital you need invested to reach financial independence. It all depends on your cost of living, and the lower you can get this, the more lucrative franking credits will be. That’s because anything under $18,200 is currently tax free income, so your franked dividend will be boosted by 30%.

The Thornhill method is SUPER passive, and extremely easy. There is no need to sell shares (unless the dividends stop flowing) so there isn’t a need to find a ‘good time’ to sell (no need to agonise over the movements and price of the market or the costs of brokerage). You just watch your fully franked dividends roll in consistently, use them to fund your cost of living and then reinvest the surplus back into the portfolio.

You have a simple tax return at the end of the year which will generally put money back into your pocket until you exceed a gross income that puts you in a tax tier above 30%. For example, once you reach $37,000 per year you will begin paying a 2.5% ‘top up tax’ on any higher earnings (32.5% personal rate vs 30% corporate rate), which increases according to the marginal tax scale. This ‘top up tax’ is deducted from the franking credit refund you receive, however it takes some ridiculously high earnings of $126K of franked dividends ($2.68M portfolio) before you start having to actually pay the difference out of your pocket – by this stage, your obviously earning enough to comfortably pay it.

However, this tax burden can be either eliminated or reduced when shared between a married couple or income distributed through a discretionary (family) trust as opposed to just being in one person’s name.

Nil tax scenario – Thornhill method

Say in the example above that you only needed an after tax income of $18,200 during retirement (for example you have a fully paid-off apartment so your living costs are lower). You could therefore live off a fully franked dividend of $12,740 from an LIC. The LIC has already paid 30% tax on its earnings of $18,200, and passed on the fully taxed $12,740 franked dividend. You get the tax paid at the corporate tax rate (30%) back, thanks to the franking credit refund when you do your annual tax return. The $5460 tax refund each year would bring your total income up to $18,200, which of course you pay no personal income tax on because it is below the $18,200 tax free threshold.

This means that in this situation, the number to work off is ($12,740/4%) or $318.5K of investments in the franked Australian LIC – rather than ($18,200/4%) or 455K worth of an unfranked income source or dividend. The difference is $136.5K and this could represent years of saving for even the most frugal person.

Where this gets really handy is when there are two of you – you can basically double your household dividend income without any further tax repercussions because you would both be under the tax free threshold, yet the household now has $36,400 of tax free yearly income to work with which is a very doable position with a paid off house (that’s not to say you can’t earn more, you just pay a tiny bit of tax on it).

To read more about Capital Gains Tax, visit the ATO HERE.

Capital Growth investing – Boglehead method

There are tax advantages using the Boglehead method too – given that you can choose when (and if) to sell your shares and you can time this capital gains event to correspond to favorable tax scenarios (such as when your income is lower if you are taking time off work).

“When you sell an asset that is subject to capital gains tax (CGT), it is called a CGT event. This is the point at which you make a capital gain or loss.”

ato.gov.au/Individuals/Capital-gains-tax/CGT-events

Person B is focused on a Boglehead style investing approach and has focused on building a portfolio which pays out little if any dividends but instead has consistent capital growth. We know that again, we want to stick to a 4% withdrawal rate for sustainability, so for the theoretical target income of $18,200 we need a portfolio of around $455K of shares. The portfolio should grow much higher than that (on average 10%) but we only ever want to harvest 4% so that the remaining growth (6%) will offset the erosive effects of inflation (long term 2-3%) and the inevitable bad years when the share markets go down (corrections) or inflation spikes.

Every year you can sell up a parcel of shares from your portfolio according to the 4% rule, and as long as your profits from the sales (current price minus cost base) don’t exceed $18200, you won’t pay any tax since your personal income tax is below the tax free threshold. However, once you start needing more than this (with corresponding larger portfolios), you may run into the requirement of having to pay tax – right? Well, not if you’ve held the parcel of shares for more than 12 months thanks to the CGT discount rule!

If you hold a stock for over 12 months (or a house, cryptocurrency etc) then you will also receive a 50% Capital Gains Tax reduction. You simply minus the sale cost from your purchase cost (or average cost base), half your profit, and then add that to your income for which you are liable for paying personal income tax on according to the ordinary income tax rate and the marginal tax rate scales.

Nil tax scenario – Boglehead method

For example, you had bought a parcel of shares for $32,400 and kept this invested where they perform over the long-term average at 10% for around 7 years and had doubled to $64,800. You sell these shares, and the capital gain applicable is $32,400. Because you have held them for over 12 months, you are eligible for a 50% Capital Gains Tax discount, bringing your capital gains to $18,200 and (eh-hem conveniently) the tax-free threshold. In this case, you pay Zero Tax on your $32,400 of income!

For a portfolio to sustainably produce a capital gain of $32,400 each year, you would need approximately $810,000 according to the 4% rule, and to get the 50% capital gains tax reduction you simply have to have held that parcel of shares for over one year (easy to do).

Again as with the Thornhill approach where a couple both can hold fully franked dividend-paying stocks in their name, with a Boglehead approach a couple can do exactly the same thing in each of their names and sell large chunks of shares completely tax free – meaning a household can bring in up to $64,800 worth of tax-free capital gains each year! Which is truly more than enough to live an extremely comfortable life with kids and lots of travel (and interestingly, almost exactly the target number my partner and I are working towards in terms of passive income from a portfolio draw down strategy).

Dividends and Capital Gains investing strategies

When it comes to Dividend vs capital growth investing It is almost always better to own and sell capital growth shares, even with the favorable tax credit policy in Australia regarding dividends.

The primary reason is you get to choose when your tax liability occurs (capital gains event). But if that isn’t enough then consider the fact that even if you utilise the franking credits strategy you are still essentially paying tax (once past the tax-free threshold) it is simply being paid for you by the company/trust earning the income on your behalf. Let’s look at a likely FIRE scenario under both strategies.

In this scenario there is James (the dividend guy) and Jim (the cap gains guy). Both have a cool $1 million invested in two ETFs. James in the DIV fund and Jim in the CAP fund.

For argument’s sake let’s propose neither fund is fantastic with both returning a consistent 5% a year with no market crashes or corrections and let’s assume zero inflation (obviously there would be these things in real life but we would typically see investments return around 10% which offsets these negatives).

Let’s look at James first. James, DIV fund seeks a fully franked return of 5% (after credits) meaning that James is paid $50,000 a year. Comprising $28,572.43 in cash payments of dividends and $21,458.57 of franking credits. As a relatively frugal retired man, James has no eligible deductions and therefore with his franking credits only pays $1550.99 in tax each year. James’ total after-tax income is $48,449.01. After 10 years of this process James has earned after-tax $484,490, and has $1M remaining in his DIV fund.

Now for Jim. Jim’s, CAP fund does not pay a dividend and as such Jim must sell $50,000 of stock each year to fund his lifestyle (James thinks Jim is silly because he is reducing his number of units). Lucky for Jim he understands that what investors care about is value not units, Jim also understands his tax law. Now every year on June 30 Jim sells his $50,000 in stock and the next day prepares his tax return. Since all of Jim’s stock has been held for more than 12 months he is entitled to the 50% CGT discount.

But this is not all, because Jim is a meticulous record keeper he also has the purchase price of every share he has ever Purchased in CAP (for simplicity’s sake we will assume a more limiting scenario that initially, the shares have doubled in value which is usually isn’t going to occur until after 7 years). Therefore after selling $50,000 in stock to fund his lifestyle Jim’s actual capital gains liability is $25,000 for the year (the other $25,000 from the sale being his capital and therefore tax exempt). After applying his 50% discount his actual liability is $12,500. Jim pays no tax.

After 10 years of consistent 5% growth in value and selling Jim still has $1 million dollars invested (the number of units invested has decreased but now the remaining units have nearly tripled in value compared to their original starting point – however the number of units is irrelevant it is only the value that matters). He sells $50,000 of which $12,500(ish) is capital and the remaining $37,500 is capital gains. He applies his 50% discount and to his dismay, he is for the first time over the tax-free threshold of $18,200 but thankfully he has the $700 Low-income tax offset to offset against the $104.50 he owes in tax. After 10 years of his CAP strategy Jim has paid no tax at all and has earned $500,000 – $15,510 more than James. The ability to sell long term held shares at the 50% discount can make the process an essentially tax free endeavour.

Investing in the real world

Unfortunately, the world doesn’t work perfectly like in our example cases above – we DO have inflation, we DO have volatility and market fluctuations, and we as investors DO have emotions. We aren’t great at predicting these and as human beings with emotions we are naturally flawed investors, so we should aim to rely on automation to the greatest degree possible, and we should be excited to see growing income streams that help reinforce positive investment feedback loops (even if we do have to pay a bit of tax).

“The market can just as well go up as quickly as it can go down. Keeping your cash invested throughout the fluctuations is what helps your money grow over time. Reassure yourself that experiencing volatility is part of the price of putting your money in the market — and it will happen again. The best thing you can do as an investor when the market collapses is usually nothing.”

Patrick Geddes – cnbc.com/select/tips-to-avoid-emotion-based-investing-younger-investors

And at the end of the day, in the FI community what we are looking to do is basically to do just that – to set up increasing streams of income that can cover our cost of living.

From what I can see, a modified approach to investing that combines elements from both the Franked dividend yield investing (Thornhill approach) and Capital growth investing (Boglehead approach) methods works the best for those just getting started.

Lump sum investing any large cash stockpiles and then setting up an automated regular investment into Aussie shares (ETFs or LICs) is probably the quickest way for Aussies to get a fairly tax-effective and “crash-proofed” passive income stream, due to our unique tax laws and franking credits. If the dividends from dividend stocks do stop (which historically they don’t, they usually just reduce a bit in a crash) and for some reason, you are desperate to sell (your 1-2 year emergency fund wasn’t enough?) you can then benefit from the 12-month holding 50% CGT discount to sell some of your shares to fund your cost of living.

The growing stream of juicy, juicy stock dividends and franking credits is very satisfying and helps condition your brain to love investing, although you will be paying a small amount of tax on this along the way even if you do choose to reinvest it (which you should obviously).

Personally, this is what I did, and how I invested up to my first $350K. Once I had this baseline, this fortress of solitude in passive income, I began to hedge this bet on just Aussie stocks by including ETFs that tracked the international markets – the US market through Vanguard VTS and the total world minus US markets through Vanguard VEU. Diversification is important, and if you are just investing into one market then you are exposed to a higher concentration of risk to that one market.

Even though international shares produce lower dividends, they are geared toward higher capital growth such that the total return is the same – and actually, since I am not paying tax on the capital growth until I ever sell, it makes it more efficient for long-term holdings as that capital growth can effectively compound tax-free (and then I get a HUGE 50% CGT discount when I do decide to sell it!)

I like that I am diversified outside of just Australia – which is only 2% of the global economy (although a lot of Australian companies themselves service overseas markets) and also not fully reliant on the franking credit refunds scheme which is a bit of a political hot topic.

Summary

In summary, a Boglehead investing style that aims to invest for capital growth (as opposed to Dividend income) will generally always produce the highest long-term portfolio results and provides the most tax-efficient income source, since you can time the sales (capitals gains event) to correspond to a favorable tax situation (such as you taking time off work, or retiring!) and you can receive a 50% CGT discount on the sale as a long term investor. This allows your portfolio to essentially grow tax-free (or should that be tax-deferred), unmolested by tax payable on dividends (which most people then reinvest anyway).

However, investing is not black and white, and as flawed human investors with emotions, franked dividend investing is a powerful feedback mechanism to build positive investing habits and a nice way to combat anxiety regarding investing and volatility. With the Thornhill approach, you see increasing streams of franked dividends drop into your account (or into your DRP), which is incredibly motivating and is a very simple system to understand. You also typically don’t need to track share prices or sell parcels of shares as the dividends from Australian ETFs and LICs are usually quite close to the 4% rule (or even above – meaning you should consider even reinvesting some back into the portfolio). The Dividends are also quite stable, meaning in a market correction they may only drop 20% whereas share prices could plunge 50%), so you don’t need to stress about selling shares in a crash (although technically speaking some economists might argue that at the end of the day, dividends and selling shares are actually the same things just under a different name – a return of capital!)

At the end of the day, you should invest according to your risk tolerance, but my suggestion is to consider doing a bit of both – which is exactly what I did. I focused on franked Aussie dividend-yielding shares through LICs and ETFs until I had my first $350K invested which was enough dividends to get me to the tax-free threshold. Then, to reduce the amount of tax I was going to be paying on dividends, I diversified by adding international shares for capital growth. If I had my time again, I would have just invested in a broadly diversified portfolio that focused on long term capital gains from the start.

Be sure to check out the following reviews on brokers that offer online trading to buy Australian and international shares. As always, make sure you are fully educated before making a choice on any particular one.

Big 4 banks

- CommSec Share trading [this is who I started out investing with]

- NAB Trade

- ANZ Trade

- Westpac Trade

Fintechs and smaller banks

- Pearler [This is who I currently invest through]

- MooMoo

- SelfWealth

- Stake

- Superhero

- OpenTrader

- eToro

- CMC Markets

- IG MarketsGroup

Microinvesting platforms

- SpaceShip – A pooled investor micro-investing app

- Raiz Invest – An awesome tool that lets you ’round-up’ your purchases to the nearest whole amount and invest the difference

- CommSec Pocket – CommBank’s response to micro-investing tools

- Stake – A cool investing tool that lets you shop for more than 3,500 American shares and ETFs with zero brokerage fees

- Pearler Micro – Pearlers Micro investing tool that lets you invest into 8 ETF based funds using Auto invest and roundups.

Financial Disclaimer

Financial Disclaimer: CaptainFI is NOT a financial advisor and does not hold an AFSL. This is not financial Advice!

I am not a financial adviser and I do not hold an Australian Financial Services Licence (AFSL). In this article, I am giving you factual, balanced information without judgment or bias, to the best of my ability. I am not giving you any general or personal financial advice about what you should do with your investments. Just because I do something with my money (or use a particular service or platform) doesn’t mean it is automatically appropriate for your personal circumstances. I do not recommend nor endorse any financial or investment product, and my usage or opinion of any product should not be interpreted as an endorsement, advertisement, or intent to influence.

I can only provide factual information based on my journey to Financial Independence, and that is provided for general informational and entertainment purposes only. I make no guarantee about the performance of any product, and although I strive to keep the information accurate and updated as it changes, I make no guarantee about the correctness of reviews or information posted.

Remember – you always need to do your own independent research and due diligence before making any transaction. This includes reading and analysing Product Disclosure Statements, Terms and Conditions, Service Arrangement and Fee Structures. It is always smart to compare products and discuss them, but ultimately you need to take responsibility for your use of any particular product and make sure it suits your personal circumstances. If you need help and would like to obtain personal financial advice about which investment options or platforms may be right for you, please talk to a licensed financial adviser or AFSL holder – you can take the first steps to find a financial advisor by reading this interview, or by visiting the ASIC financial adviser register and searching in your area.

For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.