Inflation is the gradual rise in living costs that occurs as a currency slowly devalues. The rate of devaluation of a currency is called the inflation rate, and on average, in most developed nations this sits somewhere between 2 to 3%.

Introduction

To fully understand inflation and the serious effect it has on you today, I will offer a brief explanation on the history of money and why currency devalues. It is an interesting topic on monetary policy and economics, and it’s important to first draw a line between what is money, what is currency, and what they are used for. A smart investor should have a masterful understanding of inflation, especially if they have their sights set on FI, financial freedom or early retirement (you might eventually find out that today’s $1 loaf of bread doesn’t always stay at $1 throughout your retirement days).

Currency Vs Money

In years past, societies have used money rather than currency. Money should be thought of as a tangible item that holds its value – so over time it could be used as a store of wealth and hold its purchasing power. Often rare gems or precious metals have been used as forms of money – like gold, silver, diamonds or rubies.

Currency on the other hand is simply a form of payment; a tool for trading one’s time and freedom using notes (certificates) or placeholders which have no intrinsic value. Currency simply represents ‘implied’ money, in a convenient or easy to use form (but has some serious issues, which we will cover later). Smart investors know the difference between Money and Currency; the rate of return for all currency is always negative in the long term, but more on that later.

At the end of the day, money and currency are both used for a similar purpose. And that is to trade your time – just like how you might do with bartering goods and services. Employees trade their time working for money (their wage) which they can use to buy food, housing or other needs from other workers. The money circulates through society, as an efficient mechanism for trade and business. This led to the rise of professions within the financial industry, such as banks and lenders.

The Roman empire case study

In ancient civilisations like the Roman empire, precious metals like Gold and Silver were mined, refined and stamped into coins which were then used as money to pay for goods or services. This had the advantage that Roman citizens didn’t have to barter or trade strictly in goods only, and money improved the efficiency of the market and trade systems.

The Roman empire initially used silver coins called the Denarius. This was used to pay workers, fund projects and for international trade. One Denarius was worth about a day’s pay for skilled workers, and was about 5 grams (one 6th of an ounce) of minted pure silver (silver that had been officially cast and stamped).

As the Roman empire grew, it needed more money to fund its growing civilisation. Unfortunately its mines or war chest could not keep pace with the growing demand for silver to be minted into the Denarius. Roman officials found a way to overcome this; they ‘diluted’ the silver with copper and other metals during the minting process to stretch it further. By decreasing the purity of the coins, they could make more ‘Silver’ Denarius with the same perceived value.

The Romans began pumping more and more debased Denarius into circulation, with ever decreasing silver content. Over a 300 year period, the silver content of the Denarius fell from being 100% to below half a percent – By the time Gallienus ruled the Empire, each Denarius was actually just a bronze coin with a thin Silver coating. This would eventually wear away, to show the bronze core within. Eventually people caught on and realised that their Denarius were not worth as much as they used to be; so they started demanding higher wages and raising prices.

This rise in prices is exactly what we refer to when we say inflation. This occurred because the value of the Roman Denarius was gradually being destroyed by Roman monetary policy (debasement of the Denarius). The Denarius started out as money (being a store of wealth with intrinsic value) and gradually transformed into a currency (being a form of payment with no intrinsic value).

This inflation led to soaring prices and logistical burdens. The Romans increasingly raided enemy silver stockpiles and silver mines became a strategic centre of gravity for the Empire. To fund military campaigns and administrative costs, soaring taxes and levies were introduced as well as the production of vast quantities of debased Denarius for the government to spend – one pure Denarius could be melted down and made into hundreds of ‘new’ Denarii.

These taxes combined with the effects of inflation eroded the people’s wealth. Inflation became a ‘hidden tax’ – by creating more Denarii each one was worth less, but overall the government controlled a higher portion of them. This initially gave the Roman government more purchasing power, but the resulting hyperinflation led to the collapse of the Denarii.

The perceived worthlessness of ‘new’ Denarii led to a loss of faith in the currency. Citizens hoarded older (purer) coins, and the destruction of trade paralysed the economy and the power of the Empire. Amongst civil war the Empire was split into three feuding states; the Gallic, Roman and Palmyrene empires.

The states were subject to constant Barbarian invasions which they were less able to fend off, and infectious diseases such as the Plague became rampant due to poor health spending policy. These factors heavily contributed to the collapse of the Roman Empire which was almost completely destroyed by 475AD.

This highlights the role that the economy plays in the success of a nation and the critical importance of good monetary policy.

The US Dollar

The term dollar actually originates from the Spanish Empire, where it was used to refer to a ‘Piece of eight’ or ‘Peso’ which was a coin minted from about 29g of pure silver.

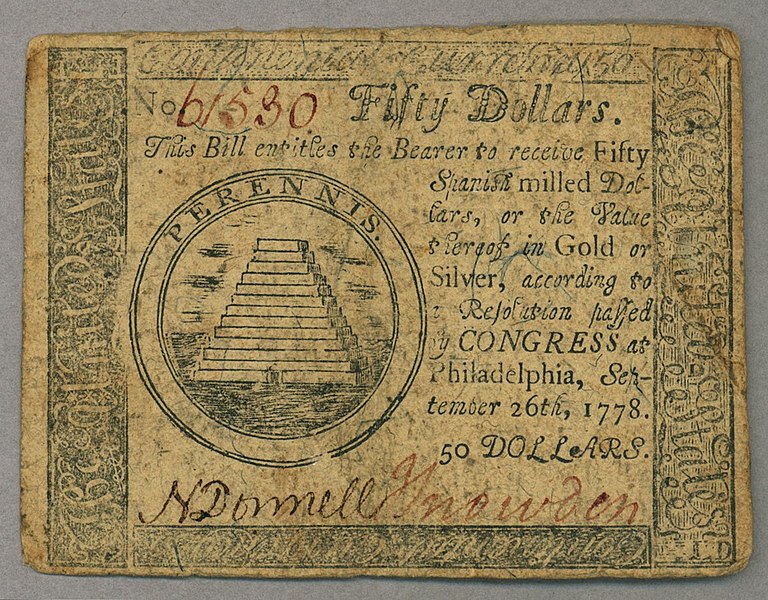

Continental Currency

A fledgling United States government seeking independence wanted to develop its own monetary policy. The Bank of North America was created (based on a loan from France which was helping the US to seek independence from the British) which issued notes convertible into Gold or Silver. In 1795, these style notes were authorised by Congress to be issued as a new currency. This ‘paper money’ was referred to as ‘continental currency’ and represented a number of Spanish silver dollars or gold.

During the American Civil war, perceived value of ‘continental currency’ bills dropped and inflation meant they became so worthless that nobody used them anymore. Benjamin Franklin suggested that the depreciation of the currency had acted as a hidden tax on the population to pay for the war (just like it had in ancient Roman civilisation).

Gold and Silver

To overcome this, US monetary policy was overhauled in 1787. An amendment was made to the US constitution banning individual states from issuing currency; Article one prohibited anything but Gold and Silver coin from being official tender.

In 1792, the United States Congress passed the Coinage act of 1792, and created the United States Dollar as their country’s standard unit of money. The United States Mint was created, and charged with the authority of converting precious metals into standard coinage for use as money. This coin was backed by 1.6g of Gold.

This use of Gold and Silver backing specifically is referred to bimetallism, a form of monetary policy where a dollar is equivalent to a certain amount of metal, creating a fixed exchange rate. This was done for convenience, as smaller denominations are easier to use in everyday transactions. This generally worked well throughout the 1800s, with only small tweaks to monetary policy taking place.

Silver debasement and inflation

Due to a large influx of silver from huge silver deposits found in the US in the late 1800’s, the value of silver decreased in line with the basic economic principle of supply and demand. The intrinsic value of the silver in US coinage dropped which led to the concept of the dollar inflating.

Political debate raged on monetary policy; some parties wanted to retain the bimetallic standard and allow the dollar to inflate to reduce the cost of repaying debts, whilst other parties campaigned for ‘sound’ or ‘hard’ currency that held its value and wanted to switch to the gold standard as a fiscally responsible policy.

In GOLD we trust

Between 1873 to 1900, the use and value of Silver slowly diminished through legislative changes and the Gold standard was eventually adopted. In 1900, the Gold Standard Act was passed, which equated one US dollar to approximately 1.672 grams of Gold.

This system worked well but was far from perfect. Global economic pressures during World War One and the Great Depression meant that the US government had to intervene with various legislative changes to monetary policy.

To deter people from ‘cashing in’ their money for physical gold they implemented controls such as higher interest rates which satisfied bank deposit holders and thus helped to protect the Gold standard. These included the Gold reserve act, the emergency banking act and numerous Executive Orders.

But these high interest rates were hurting the US economy. It was costing too much for people and businesses to borrow which is a key factor in economic growth. During the 1930’s countries all over the world began cutting ties between their money and Gold. The US too began to cut ties with Gold, choosing to devalue its currency in Gold by over 40%. This was done in order to pump more currency into circulation and reduce interest rates to try and stimulate the economy. Over time, the precious metal content of US coinage was reduced. This is a very simplified explanation, but you get the idea.

In GOD we trust

In 1971, President Nixon cancelled the direct convertibility of the USD to Gold for foreign nations. This meant that the USD was no longer backed by Gold (or any other physical asset) but was instead backed by a debt to the United States government.

This meant if the US government owed a nation money, or if they had a bunch of US dollars that they could no longer ‘Cash it in’ for some of the US gold stockpile. Instead, they could only exchange the US dollars for debt and receive an interest payment on the debt. Thus, the USD ceased to be money, and again became a Currency (just like the original Continental Currency).

This allowed the US to print vast quantities of USD bills, which were used to increase national debt. The USD or Greenback is considered one of the most stable international currencies due to the economic and military power of the United States government. There is an estimated $1.5 Trillion physical USD in circulation, a lot of which is used as tender internationally in countries with weaker economies or lesser trusted currencies.

Fiat currency

Fiat currency is the name given to money which has had its physical asset backing removed – just like the US dollar did when they cancelled gold backing fully in 1971. A Fiat currency is backed by national debt, that is to say, the goodwill of the nation. It is a currency backed by confidence in the country. In general, due to the overwhelming military and economic power of the United States, international currency exchange rates are almost unanimously ranked in terms of their position against the USD (and there are many investment hedge funds to the USD).

Exchange rate

Strong nations with good monetary policy can maintain a strong dollar exchange, whereas more irresponsible nations might have a ‘weaker’ dollar. The exchange rate or dollar value is not the only factor when considering economic strength. Although a ‘stronger’ dollar may allow a nation to import more resources from a ‘weaker’ nation at a discount, the weaker dollar of that nation will attract more buyers and boost its level of exports – if a nation makes money by taxing or placing duties on exports, this can boost a country’s national savings or ability to spend.

Printing currency

The trap with Fiat currencies comes down to nations individual monetary policies. For example, a fiat currency can be printed freely, and a nation that prints too much currency can find that the value of that currency can drop in value quickly. ‘Printing money’ gives a government an ability to spend but results in an inflation rate, penalising anyone who is holding currency (and rewarding anyone currently holding debt). It also penalises the working class, who are paid a set wage – hence wage growth must occur to protect workers, but this typically lags behind inflation in what some describe as an act of class warfare (as my very frugal Scottish Grandad used to say, ‘The rich get richer and the poor have children!’)

The cost of things such as food generally stays the same relative to true money such as Gold, however when looked at through the lens of the inflating fiat currencies, the prices just go up and up. It could be said then, that Fiat currency could be a tool used by governments, the status quo and the financial sector to leech away the time and freedom of citizens? At any rate that is a very negative way to look at it, I prefer to think of it as a ‘tax on the selfish’ and a very good encouragement to invest (for the benefit of all society).

The currency cycle

To fund deficit spending, the treasury ‘borrows’ currency by issuing a bond (an IOU). A Bond is a contract that allows the treasury to ‘borrow’ currency with the promise of it being paid back with some interest (the coupon rate) at bond maturity (the agreed life of the loan).

This means a government can spend currency now, and pay it back later. This is beneficial so long as its spent on income producing assets, but that is not always the case. It can be hard to justify and rationalise the economic impact of nation building projects, but its clear that infrastructure projects like roads, power stations and hospitals have a positive impact on improving quality of life.

The Treasury Bonds (national debt) are created and then sold, usually to large banks which are purchasing the bond to receive the interest payments they produce and make a profit. These bonds can then be exchanged on the open market. Some of which are sold to the Federal Reserve; which provide a ‘cheque’ redeemable for currency which is printed at the mint. The banks can then use this currency to purchase more bonds, and the cycle continues.

Fractional reserve banking

When you deposit your currency in a bank, the banks are allowed to reserve only a fraction of your deposit and loan the rest out as credit. For example, if you deposit $100K of currency, using the most common 10% fractional reserve limits, the banks must retain $10K but can loan out the remainder of your $90K.

This might be to someone wanting to borrow it to buy a home, and so take out a mortgage. The bank can make a profit on the interest they charge on the home loan. The $90K credit is taken by the debtor and given to the person selling the house. When the home seller deposits this currency into their bank, the system repeats itself and their bank is then able to lend out $81K. This process repeats itself such that the original $100K of currency can create $1000K worth of credit (bank loans).

This expanding supply of currency (and credit) puts pressure on prices, driving them upward in an inflation of the currency.

Income taxation

To help pay the interest on the bonds generated by the treasury, workers are then taxed on the income they earn. Governments take a slice of your wage, which is used to pay the coupon rate on the bonds that make up the national debt. In this way, you and future generations are made to pay for the deficit spending of the government.

National debt

In addition to using collected tax used to pay the interest on the national debt, nations can simply issue more bonds. There in lies one of the biggest dangers with central banking; the creation of currency simply creates ever more debt cycles (as the currency is backed by debt).

Governments can spend the currency into circulation before its inflationary effect on the economy happens. The effect of national debt is to silently erode an individual’s wealth; transferring wealth from the working class into government and banking sectors.

“The decrease of purchasing power incurred by holders of money due to the inflation imparts gains to the issuers of money” US Federal Reserve

The cash rate

Reserve Banks set the prices on the official cash rate on their currency, which also indirectly influences the rate of inflation. The cash rate is influenced by the general health of the economy and things like the unemployment rate.

The cash rate is the price that banks pay when settling overnight loans with each other, and serves as a benchmark rate for the nation. This rate is then taken by the banks, along with other factors like risks of default, lending costs and inter-bank competition to determine a retail loan interest rate, or the savings rate offered on cash savings accounts.

Loans on ‘stable’ assets like a mortgage against a house is seen as fairly low risk, so retail interest rates on mortgages are generally lower than things like car loans or even unsecured loans such as personal loans or credit cards.

If the reserve banks increase the cash rate, then loans become more expensive. Banks will pass on these costs to their customers through higher interest rates on loans, as well as higher fees and charges. The net effect on the economy is that less lending takes place, as well as less spending as people tighten their purse strings and start hoarding cash in savings accounts. Raising the cash rate is generally seen as ‘putting the brakes’ on the economy, and retailers may need to lower their prices to entice spending – a deflationary outcome.

Lowering the cash rate on the other hand, makes cash cheap. People are much more happy to loan money from the banks, for example buying houses. This new supply of money pushes the price of housing up. Similarly a low cash rate means savers won’t be rewarded by hoarding cash in savings accounts, encouraging them to either spend or invest their money, lifting economic activity. By definition then, lowering the cash rate is an inflationary outcome.

Protecting yourself from inflation

One of the simplest ways to protect yourself from inflation, is to ensure your portfolio generates a higher return than the effect of inflation, after you account for taxation. Yes, income tax is taken out of your earnings before the effect of inflation reduces your purchasing power.

Whatever you are left over with, is your real return. So long as you are spending less than your real return, your income should always increase. This means it’s important to work hard, and live well below your means, and invest your savings. And as Warren Buffet says, practically speaking investing in a low cost stock market ETF index fund makes the most sense, most of the time. Once you have enough invested in a portfolio that its real return covers your cost of living, you have reached financial independence.

So just how much can you spend? It’s a complicated topic, but the general consensus is that you can safely live on about 4% of your portfolio without losing any purchasing power or quality of life. This is generally accepted as the safe real return of a typical portfolio, or the safe withdrawal rate. To work out how much investments you need to retire then, just multiply your yearly living costs by 25 (or to be more conservative, 33). I write more in depth on this in my article on safe withdrawal rates.

If you’re interested, there is a couple of great YouTube Videos by Mike Maloney on the hidden secrets of money which I found really informative. I enjoyed the series, but can’t help but think that they are somewhat pushing ‘investments’ in Gold and Silver since they likely own significant holdings and want to see their portfolio rise. I’m naturally pretty skeptical though, so take out of it what you can 🙂

For the record, I don’t own Gold or Silver or any other precious metals or commodities directly. I just buy rock solid ultra low fee ETFs and LICs. Since some of those have big holdings in mining companies, I guess you could say I have exposure indirectly.

Sure, the price of Gold has risen in line with inflation and through investor fear sentiment, but I just don’t see gold as a productive asset because it doesn’t really do anything. It provides no dividends so I can’t live off it, and making profit by selling it really only works the same as cryptocurrency which is on the ‘greater fool’ principle – that is, you need to find a greater fool than yourself to pay more for it than you did.

The only way I could think of gold being profitable, is if you somehow were able to predict a market crash and magically sell all your ETFs and buy gold, then after the crash sell the Gold and buy back the ETFs at a discount. This is wildly impractical – how could a smart investor ever possibly predict a crash or subsequently know you are at the bottom of the market? You Can’t! (A smart investor knows it’s about time in the market, not timing the market).

If you decided to follow the advice of ‘financial advisers’ and buy gold or bonds (aka fixed interest) as a part of a “balanced portfolio” you could then sell your gold or bonds during a market crash to buy ETFs when they are on discount. Then when the share market (ETFs) recovered, you could sell them at a profit and buy back even more gold and bonds, and wait out to repeat the cycle.

Sounds like a lot of timing the market, and brokerage. For one thing, all those transactions will help make your financial adviser and brokers richer, but not you. History and statistics show that it’s impossible to predict the market, meaning it is about ‘time in the market, not timing the market’. Even the world’s richest and most successful investors like Warren Buffet promote investing in good quality, low fee market index ETFs and don’t invest in Gold.

Summary

In summary, inflation is something that affects us all. A good understanding of inflation and how to mitigate its effect on your wealth is critical to financial independence and being able to reach FIRE and maintain it. You could even try using the Inflation Calculator on the RBA website. It could be quite eye opening for you.

Whilst Fiat currencies can philosophically seem pretty evil, it’s just the financial system we have at the moment. At the end of the day, there is nothing you can really do about it anyway so the answer is to try and use it to your advantage. For the most part, that means investing in productive businesses and assets like stock market ETF index funds and real estate. It is a bit unsettling to see that every 40-50 years the world sees a fairly big change to financial policy.

I know I have probably presented a gross over simplification of monetary policy, but I hope it’s helped you to understand why you need to keep your wealth invested in productive assets, like in high quality businesses through stock market index ETFs or cash flow positive real estate (and not sticking it under your mattress or in your knickers draw!)

Get FI !

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.