Debt recycling can be risky but it can also provide homeowners with tax savings and help to build wealth. Learn how debt recycling can benefit your financial situation with this thorough guide from an experienced investor.

This article is my research and learning into debt recycling before I buy my farm and start debt recycling in the next couple of years. I am not an expert in this and I will consider this a ‘live’ document and share my ongoing experiences. Please feel free to critique and comment as this evolves.

CaptainFI is not a Financial Advisor and the information below is factual review information, not financial advice. This website is reader-supported, which means we may be paid by advertising on the site, or when you visit links to partner or featured sites. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Introduction to debt recycling

Debt recycling is a different way to look at debt on your home (primary place of residence). Many people are using this strategy as a way to pay off debt, invest at the same time and reduce tax payments.

As the name implies, debt recycling involves recycling borrowed money. This is most often the mortgage you have on your home, and these funds are then paid and then re-borrowed to invest. This is where the ‘recycling’ comes in. Debt recycling is a way to turn your PPOR mortgage into a Good debt. A Good debt1 is one in which the debt brings an increased value of returns, or capital growth, in the long run. This is opposed to bad debt, such as consumer debt, which is usually unrecoverable without yielding any returns. Debt recycling also comes with additional tax benefits.

The process of debt recycling involves putting additional payments onto your home (PPOR) mortgage, and then taking the equity out of your home and investing it into shares, turning non-tax-deductible mortgage debt into tax-deductible investment debt, and ideally earning a higher rate of return. Because an investment loan is tax-deductible, it means you can claim the interest costs on your investment loan as a tax deduction against any capital gains or dividend yield from the investments.

When interest rates were at an all time low in the last couple of years, it was a pretty appealing premise, but as interest rates are rising, you need to do your homework, and make sure it is something you can manage financially, especially if rates continue to rise. If you’re looking into debt recycling as part of your financial planning, it’s important to be fully informed, understand the process and risks involved and be confident that it is the right thing for you.

So in this article let’s explore the meaning, how debt recycling works, its pros & cons and one example.

“With a debt-free home the strategy is even simpler: You put up the property as security for a line of credit. This ensures your interest cost will be a lot less than a margin loan where the shares are used as security. It also means you will never have a margin call.

Theoretically the loan should be at the best home loan rate the bank has to offer as the security is exactly the same as if you were borrowing to buy a property. Also, the amount will be nothing like a ‘home loan’ so the banks security is very high.

Look at a principal and interest loan as they will try and charge you more for an interest-only loan.

Despite all that they will try and stitch you up with a more expensive rate so negotiate hard or use a mortgage broker. Point out to the bank that if they deal with you direct they won’t have to pay a trail commission to the broker!

Back to the main game; the loan interest will be tax deductible as will any other costs associated with the transaction as it is being used to purchase income producing investments.

Without a mortgage, the dividends can be streamed straight back into the line of credit which can then be redrawn at will.

We use this as a means of amalgamating a number of smaller amounts (dividends) and investing that in lump sums. Usually when the listed investment companies have a rights issue of new shares or offer a share purchase plan to existing shareholders.

Both of these come with zero brokerage fees and often at a small discount to the then current price. It was a great discipline for our 3 sons as they took them up when they arrived without a debate about whether it the right time to invest. Looking back now, Frieda and I have 22 purchases of Argo over the years. Some high, some low but all less than where they are today.

Also, you buy lots when they are cheaper and less when they are more expensive. I defy anyone to time the markets successfully.My comment about borrowing 2-3 years’ worth of current dividends is aimed beginners. If the property is currently debt free you can borrow whatever you are comfortable with.

We are currently paying 4.8% fully tax deductible and the shares are producing about 4.3% plus franking credits. We are ever so slightly positively geared.

Can I just say that in the eyes of most Australians that would be perceived as silly; most aim for negative cash flow so that you can claim a tax deduction for the amount you are losing; go figure!!”

Peter Thornhill on debt recycling2 using Listed Investment Companies, 2019. Peter Thornhill is the Author of Motivated Money and earns over $500K per year in passive dividend income.

What is debt recycling?

Debt recycling is a way of rearranging your personal finances so you can convert a non tax-deductible mortgage into a tax-deductible investment loan. The money that would have gone towards paying off your PPOR mortgage and building equity is ‘redrawn’ in an investment loan structure secured against the property (and your income) instead. Because this loan is purely an investment loan to buy shares, you can claim a tax deduction for the interest to offset the dividend yield or capital gains of the shares.

A common method in debt recycling is to buy high dividend-yielding Australian shares such as Vanguard VAS or Betashares A200 which are index tracking Exchange Traded Funds. These ETFs pay a nice dividend yield (my total portfolio investments has averaged 4% dividend yield, which after considering the franking credit (30% tax credit) is boosted to approx 5.7%) and that combined with the fact that the debt recycling investment loan is tax-deductible (you can subtract the cost of the loan against the income created before paying tax), the dividends alone are often enough to service (mortgage) loan before even considering the capital growth aspect (typically another 6% for Australian shares).

Using dividends from a debt recycling investment loan portfolio to pay the original mortgage is a smart option, you can arrange for these to be automatically paid to your loan balance as soon as they are distributed – this increases your equity (reducing your LVR) allowing you to draw more out on the investment loan. Some people prefer this method as they are in control of the entire process themselves and can then go straight out and buy more index funds using the investment loan. It also works if you have any extra earnings or windfalls during that month – you simply pay it off the mortgage and then draw it straight back out on the investment loan and buy more shares.

With the capital growth of shares ticking away in the background, debt recyclers ideally want to get into a position where the investment balance exceeds the remaining loan balance (both the remaining non-tax deductible mortgage portion and the total tax-deductible investment portion). From there you can decide to sell enough shares to pay off the entire debt balance and be totally mortgage-free, or just sell off enough shares to pay the balance on the remaining non-tax-deductible mortgage portion and keep the tax deductible loan to continue investing using leverage.

Debt recycling can reduce the number of years you have to pay off a loan and may reduce overall interest charges – making it a better option than remortgaging or extending a loan term. However, because you are buying shares that have volatility and could always go down in value, debt recycling can be a riskier option than simply just paying down your mortgage. Especially if you get freaked out by market corrections and would be likely to make knee jerk decisions (such as selling shares in a downturn).

Financial institutions provide debt recycling services (such as the NAB equity builder program3) but some banks charge hefty fees for this service, and you will typically also have to pay a higher rate than a standard home loan. If you can get a low enough interest rate, a Line of Credit mortgage can also be a good option for debt recycling.

People often get stuck on the question whether they should invest or pay off their mortgage. Debt recycling4 is basically the act of investing in an income-producing asset using your equity, to pay off your home loan quicker. With debt recycling, you pay off the mortgage BY investing, essentially killing two birds with one stone and using the higher investment returns from shares to pay down the mortgage quicker.

Debt recycling can provide a source of capital for numerous investments, but some debt recycling programs such as the NAB equity builder have limitations on what equities you can buy – for the NAB equity builder they don’t really want you taking massive risks with speculative punts on penny stocks, so in exchange for a good overall deal and competitive interest rates they require you choose from over 950+ approved investments.

How does debt recycling work?

The first step to debt recycling is buying a primary place of residence using a mortgage (home loan). As you build equity on your property – either from market growth or from paying down the mortgage with your wages, you can start looking at debt recycling to accelerate the process. After you have got your equity position to a qualifying LVR, when approved through a lender for a loan redraw or line of credit, you can withdraw that equity money back out and start a separate, dedicated investment loan. After redrawing the funds from your mortgage account specifically for investing purposes, the loan is then rendered tax-deductible. This means you can claim the costs of the loan (interest, fees etc) against the investment income, or the income produced by the shares.

The overall idea behind debt recycling is to reduce the non-deductible loan while increasing the tax-deductible investment loan – meaning you pay less on the mortgage loan and gain more from the investment loan.

Why is debt recycling tax deductible?

Generally, a tax-deductible5 investment loan implies that certain expenses can be subtracted from income gained before factoring in taxes. While in non-tax deductible loans, you can’t subtract expenses before factoring in taxes.

Debt recycling and the tax benefit that is associated with debt recycling is perfectly legal so you don’t need to worry that the tax office will come and hunt you down for tax evasion, it just needs to be done carefully and effectively, and should be well documented / accurately recorded.

Debt recycling involves paying off a debt in order to use the same funds again in order to invest. The Australian Taxation Office will allow you to claim any losses from this debt recycling activity as a tax deduction against your taxable income. This means that for every dollar lost to interest, fees, and other costs incurred through debt recycling, you can potentially offset it against other income sources such as employment or investment earnings. This is in exactly the same manner as negative gearing for investment properties (just switch out the investment property for an investment share).

If the money is in an offset account, it’s regarded as savings, any money you withdraw from an offset account cannot be claimed as a deduction6. If you actually paid the money directly into your loan, and you’re drawing down on that amount to invest in a CGT asset, then the interest would be deductible7. Any amount used for private purposes is not deductible, and you would need to apportion the loan.

Australian Taxation Office6

You must ensure the investment loan drawn against the mortgage is used only for investment, and not for personal uses such as a new car or holiday. If you muddle personal uses then your entire loan could potentially be disqualified from getting a tax deduction as it could be considered a non-tax-deductible personal loan – for example a simple mortgage redraw to pay for home renovations or a pool is not considered tax-deductible.

As far as I am aware, to get the tax deduction on the investment loan, you need to hold the shares privately and not in a company or trust structure. Some debt recycling products such as the NAB equity builder will actually hold the shares for you in a trust, which is a similar custodian structure to how brokers like Superhero and Stake US share trading work.

You should chat to an accountant to confirm for your specific personal situation, but I believe you may also be able to claim expenses incurred in debt recycling such as publications and journals (such as the Barefoot Investor, Motley Fool or Money Mag), internet costs, financial advisor costs and if you hold ETFs then the Management Expense costs (derived from the funds MER and your total balance) which can all be considered investment management costs that directly help you to earn more money – and thus pay more taxes in the future!

Debt recycling techniques: Manual vs Automatic vs Incremental Debt recycling

You can do debt recycling in more than one way – typically you can either debt recycle upfront in large chunks (lump sum investing), incrementally (dollar-cost-averaging) or pay-as-you-go debt recycling.

Debt recycling in chunks (manual lump sum debt recycling):

This method involves investing in large chunks as soon as possible. This is made possible by either accessing all available equity to redraw at once, or by paying off a large chunk of your mortgage using your savings (or offset), immediately followed by redrawing this money for investment. You then repeat this process as soon as you have an opportunity to again draw on the investment loan until it is fully drawn (original non-tax deductible loan is fully paid off and has been redrawn). There may be a minimum limit for the size of a ‘chunk’ that the bank will let you split into a separate loan.

Automatic Debt recycling (dollar cost average debt recycling):

This method involves getting an approved investment loan balance ‘ready to invest’ such as a line of credit, or manually splitting (withdrawing) the funds from your home equity ready for share investment and then putting these funds into an offset account against the investment loan. You can then set up your regular fortnightly or monthly share investment which is drawn from the investment loan or the investment loan offset account over time. As time progresses, you gradually draw out the investment loan until you meet your limit. Once you meet your limit and don’t have any ability to draw anymore, you then need to engage with the lender to try and increase your limit (based on the LVR which will hopefully decrease as the shares go up in value). Given you typically have to keep paying P+I on both loans, you should be in a more favourable equity position so this shouldn’t be an issue.

Incremental debt recycling (Pay as you go debt recyling)

Instead of investing your fortnightly or monthly savings directly into your shares, you can simply pay it all off your home mortgage. Next, you draw the exact amount out of your investment loan / line of credit and use it to buy shares just as you normally would have.

Benefits of debt recycling

Some of the benefits of debt recycling include;

- Increases ROI: The debt recycling strategy is a potential way to increase returns of investment. This is due to the effect of leverage, and also tax savings due to the converted tax-deductible loan. Since the investment loan is tax deductible, you pay less in total taxes as you get to subtract interest and fees from your returns before paying taxes.

- Diversified portfolio: With a long-term investment focus, it’s important to have a diversified portfolio8. This will help to protect you from possible risks and losses. Investment from your debt recycling investment loan can help to branch out your portfolio so that you don’t just have exposure to property, allowing exposure to index fund shares or other income-producing assets.

- Provides income growth: Debt recycling provides you the opportunity of increasing your income streams. It is often used to invest in income producing shares such as Australian index funds or good old fashioned listed investment companies. These can be great income-generating assets, leading to more money for you over time (this dividend passive income can be used to pay the interest and principle payments on the investment loan!)

- Future financial security: Investing in assets, especially long term, can help build financial security for the future. As time passes, these income producing assets help to get you closer to financial freedom.

Risks of debt recycling

We have shown some of the benefits of debt recycling, mostly that it can be a helpful investment strategy9, but it’s not for everyone. There are some risks when it comes to debt recycling, with serious consequences, such as:

” – Investing in the share market (domestic and international) comes with risks and many factors can cause market volatility.

– Using leverage can magnify both gains and losses.

– If you miss a monthly repayment, your investments may be sold. This may have capital gains tax (CGT) implications.

– If the interest rate increases, your P&I repayments may be greater than what you originally budgeted for.

– If one of your chosen investments is removed from the Approved Investment List, you may need to switch to another investment. The sale of an existing investment may have capital gains tax (CGT) consequences.”

NAB equity builder10 Website, March 2023.

Increased losses due to debt recycling leverage

Leverage magnifies both gains and losses. Debt recycling can be a risky strategy if you invest without due diligence, or when buying individual shares. When you invest, you take the risk that the market can drop, therefore that returns are not always guaranteed. If your investment value goes down, and you panic, you may crystalise your losses and that could hinder your progress and have a serious impact on your investment loan and the mortgage loan initially pulled out. If you are an emotional investor or don’t have a long term outlook, debt recycling could be too risky for you.

Increased interest rate of investment loan

With debt recycling, there might be a rise in the interest rate of your loan. Therefore, you would need to make enough from your investment to cover your interest repayments. Recently, we had historically low levels of interest rates, but interest rates are rising. If you don’t make enough from the investment yield, you will have to contribute from your own wage/income in a similar manner to negative gearing property.

Loss of income

You may lose your home if you are unable to meet your mortgage repayments. Having both loans demands more responsibility because you would need to make sure that all requirements are met. It’s vital, therefore, that you have a secure, regular income source, as well as surplus cash flow for other expenses.

Time constraint

Like many loan methods, debt recycling investment loan capital repayments are expected to be paid within a particular timeframe. You might get into trouble with your lenders if you are unable to pay up within a certain timeframe. Debt recycling is usually only recommended to those who can continue the cycle for at least a minimum of 5 years, however with a good lender you should be able to refinance periodically.

Who should consider debt recycling?

Debt recycling certainly has many strong benefits and there are obvious risks so it’s important to seek professional advice for your personal situation, but as a general guide, here are some indicators that show that you might be a good fit for debt recycling:

- Steady income: Investors should note that it is always important to have other options in case one does not work out. This is why you need a steady, diversified means of income. With a steady income stream, you should be able to handle your loan repayments in case your investment drops or you have a hiccup with any one income stream. Lenders will obviously scrutinize your income for serviceability requirements.

- Well-informed: It’s important to do your own research to find out if this strategy would be beneficial for you and your situation or if it poses too much risk. There are many other helpful guides on debt recycling out there, as well as financial advisors who can help you to decide.

- Homeowner. You obviously need a home (primary place of residence) to conduct debt recycling. You should never let the tax tail wag the investment dog, so buying a house just so that you can do debt recycling is probably a pretty dumb idea.

- Someone who understands and accepts the risk of share market investing. There is risk involved in debt recycling, including market volatility and the possibility that your investments could dramatically decrease in value and have protracted periods of stagnation before recovery (or they may never recover!)

- Long-term focus. You need to have a long-term focus to be a share investor (investing for a 5 to 10 year plus timeframe)

- Able to refinance. If you are a homeowner, you should be able to refinance which means you typically need to have enough equity in your home (20%+) for lenders to consider you.

Debt recycling strategy – example one (my property build)

To fully understand debt recycling, we will make use of a scenario. I will use the figures from my current property development project (NB that there is no point debt recycling an investment property as its expenses are already tax-deductible). Let’s pretend that I live in the house rather than it was an IP for argument’s sake.

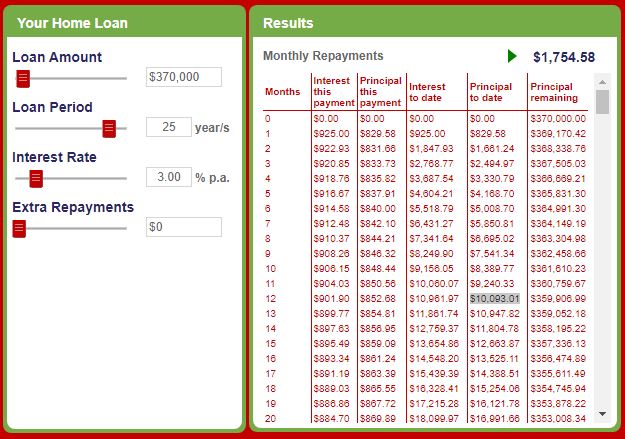

The value of the home is $570,000. Out of that amount, I have a $370,000 mortgage, so approx $200,000 in equity, but also built up $20,000 of savings in my mortgage offset account – so effectively only paying a $350,000 mortgage, and the total LVR is 65% (effective LVR with offset is 61%). I want to apply to borrow money out of the $200k equity to begin the debt recycling process.

Depending on personal circumstances (family, expenses, wage, assets, and liabilities such as car loans etc) and lender legislative requirements, you will never be approved for the full $200,000 of equity. Lenders don’t typically want the LVR going above 80% (you start running into problems such as LMI etc), so realistically the maximum a lender may be willing to re-mortgage my $570K property for would be a $456K loan, so given I still owe $370k, the maximum offer for a debt recycling re-draw out on this property is about $86K.

Assume my lender gives me approval for a more conservative $80K, and creates a mortgage split with the initial $370K mortgage as split 1, and a new $80k line of credit as split 2.

I take the $80K from my line of credit and transfer it to my brokerage account. Because I like round numbers, I then take my $20K in the offset, use it to pay off $20k of the mortgage split 1, and then draw it out of the split 2 line of credit and transfer it to my brokerage account. The reason for paying and then redrawing the $20k is that it has now become tax-deductible as it is being used purely for investment. Now I have a nice round $100k to play with.

I then proceed to use this investment loan11 to buy shares, in just the same way as I do with my personal brokerage portfolio. Using the example of my personal portfolio (aims to hold an equal weight mix of A200, VTS and VEU) in 2021 the performance was 9.4% capital growth and 3.5% dividends. So I would have made $3500 in dividends (with a franking credit of $1275 based on 85% franking) and $9400 in capital growth in the investment account which is now showing a balance of $109,400.

Assuming an interest rate of 5% for the investment loan and a $1500 fee I would have paid $5500 in interest and fees, as well as with an average .06% MER I have paid $600 in management expense fees for the ETFs held (unfortunately you cannot claim brokerage costs).

This means my total return in terms of cash flow is +$3500 dividend, +$1275 franking credit tax refund, -$4000 interest, -$1500 fees, $-600 management expenses = -$1325, so according to the tax office I have ‘lost’ money. I need to obviously pay the bank this amount out of my income and I can get my accountant to claim a $1325 deduction on the tax return for the year, saving most Australians anywhere from between $250 to $622 depending on tax brackets.

However on paper, just like with real estate negative gearing, I know due to capital gains of $9400 I am actually up $9400-1325 = +$8075. So as far as the bank is concerned they are happy to see my ‘total equity position’ increasing with an investment balance of $109,400.

For the sake of simplicity, say this continues in 2022 and I don’t bother to redraw any of the approx $10,093 in principal mortgage contributions I made to date in 2021 to split 1 to make further debt recycling purchases;

I assume my expectations for an average market return of 6% capital growth and 4% dividends (see my most recent total returns here) I expect to get a $6,564 capital gain, $4,376 dividends, and $1595 in franking credits (approx 85% franked). Again, accounting for -$4000 in interest, -$1500 fees, $-600 management expenses the cash flow is -$129 (nearly cash flow positive), a total return of $6,435, and a cumulative investment balance of $115,964.

So after only two years, I have paid an extra $925 ($1,325 minus approx $400 tax return) and $90 ($128 minus approx 38 tax return) for a total of approx $1000 out of pocket, but my total investment balance is $115,964. I have nearly doubled my initial $20K mortgage offset and still only owe the $80K investment loan.

If I wanted to cash out and sell the shares now I will have $15,964 of capital gains, and with the 50% discount (for holding 12+ months), it would be approx $8000 CGT liability, or around $2600 in tax for the 32c in the dollar marginal tax rate, for a total after-tax profit of $13,364, or $12,364 after factoring in the $1000 in negative cash flow these first two years. So I am $12,364 better off for having done the debt recycling strategy for these two years.

This is a very simplified example, but if you consider you can actually redraw additional mortgage payments you made into split 1 (in my case $10,093 at the 12 month mark), and then redraw it out of the split 2 (investment loan) to buy more shares, the effect of debt recycling is sped up a bit (in this case, by another approx $400 in dividends and $600 in capital growth).

Now I wouldn’t suggest doing debt recycling if you only plan on it for a couple of years, personally I plan to use debt recycling when I buy my farm until I can completely pay it off, which will probably take around 10 years because I plan to supercharge my extra contributions using income from the website portfolio.

Over time, provided the market continues to grow and home loan interest rates don’t increase much more, you will reap a more and more positive cash flow each year until the dividends paid become greater than the total interest and fees, and you can start using it to pay down your original mortgage on split 1 (and subsequently redraw it out of split 2 to buy more shares!).

The investment account (shares) will also ideally be going up in capital value, and when the total value of the investments matches the total value of the remaining mortgage (split 1 + split 2), you can decide to sell enough shares to pay off the entire debt balance and be totally mortgage-free, or you could just sell off enough shares to pay the balance on the remaining non-tax-deductible mortgage portion and keep the tax-deductible loan (split 2) to continue investing using leverage. If you are dead set on the leverage aspect, you could even then negotiate to re-draw that equity from the split 2 to continue investing with more leverage (but I personally will not be doing that).

Debt recycling strategy – example two (my farm)

When I start debt recycling for my hobby farm I will publish the ongoing results here. I will be using the strategy from example one, except this will be a ‘live’ example from the farm I am living on. The mission is to get the farm paid off as soon as possible, ideally within ten years.

Is it easy to get a debt recycling investment loan?

The simple answer to that is it depends. There are many companies that will happily offer you a loan to invest in property, shares, business or just about anything else. Unfortunately, the devil is in the details (and the interest rate and fees), and if you don’t understand what goes into the application and screening criteria, or how to make money from your investments, it’s not always going to work out positively for you.

The ability to get a loan approved will of course depend on your financial situation, the equity in your home, your property value, whether you have a regular income or not, how much is in your cash account and several other factors including whether you have dependants or any previous debts. A mortgage broker can of course help with this process.

Is debt recycling worth it?

Debt recycling can be a great way to pay off a mortgage, increase your returns on investments and increase tax savings, but it does pose some risk because you are investing in the share market which is volatile and can be unpredictable in the short term. Whether it is worth it or not is going to be very individual, based on your personal financial situation, your income streams and your assessable income, your borrowing power, house prices, the reliability of income, your risk profile, whether or not you’re paying off an interest-only loan or a principal and interest loan. For debt recycling to be worth it, you need a great understanding of how it works, as well as have a good ability to manage your income and your home loan repayments and other repayments effectively.

Frequently Asked Questions

Frequently Asked Questions about Debt recycling

How is Debt Recycling different to a margin loan?

Traditional margin loans also allow you to invest in shares using leverage (a loan), with the shares being held as the loan security. Shares are volatile investments, and although generally a total market index fund increases in value, they are volatile meaning their value goes up and down every day.

If there is a market correction or crash, your loan security goes down in value meaning your loan can exceed the maximum LVR ratio and you will receive a margin call requiring you to either contribute a lump sum payment to the bank, sell some of your shares, or buy additional shares to provide increased loan security to the bank. If you don’t, the bank can take your shares and liquidate them to meet the LVR ratio requirement as per your margin loan contract.

Most debt recycling solutions such as lines of credit or the NAB equity builder do not have margin calls in the arrangement, since it is the property and your income earning potential that is used for loan security, not the shares that you have used the investment loan to buy.

Should I borrow to invest?

If you are comfortable with borrowing money to invest in financial assets, then a loan could allow for a larger initial investment exposure. The effect of compound returns is much stronger when invested early, so your investments could perform better over time. This comes at the risk that investors who rely heavily upon gearing (leverage) may experience crippling losses due to leverage magnifying both potential losses as well as gains. If your investments drop below their initial cost base or theoretically go to zero, not only will you lose on your initial capital, but you will now owe the bank the balance of the investment loan (difference between the value of the shares and the value of the loan). Debt recycling typically uses the equity in your home as collateral in case this happens.

Summary of Debt recycling

By understanding debt recycling, you can view your home and your mortgage as an investment opportunity, rather than a liability. There are risks involved which are vital that you understand, as well as you must fully understand your own financial situation. You need to run the numbers and compare this to your risk tolerance to see whether this would be beneficial for you or not. For those that are taking full advantage of debt recycling, it can act as a great long-term tax advantage strategy, help build wealth, pay down home loan debt faster and get you closer to financial freedom.

I will personally be applying to use a debt recycling package to pay down my hobby farm quicker, alongside making additional payments to convert the non-tax-deductible mortgage into a tax-deductible investment redraw quicker.

Have you tried debt recycling to pay off your home faster or for the tax deductions? How did it go for you? Let me know in the comments!

If you’re not sure whether debt recycling is right for you or not, or you want further info on home loans and investing, tax advice or investment funds, it makes sense to speak to a financial planner who can give you advice based on your personal situation.

Reference List:

- ‘Good Debt vs. Bad Debt’, Equifax. Accessed online at https://www.equifax.com/personal/education/credit/report/understanding-credit-good-debt-vs-bad-debt/#:~:text=In%20addition%2C%20%22good%22%20debt,home%20will%20be%20worth%20more on March 10, 2023.

- ‘Peter Thornhill: Debt Recycling strategy’, Darren. Retire on Dividends. Accessed online at https://www.retireondividends.com/peter-thornhill-debt-recycling-strategy.html on March 10, 2023.

- ‘PODCAST – NAB EQUITY BUILDER’, Aussie Firebug. Accessed online at https://www.aussiefirebug.com/nab-equity-builder/ on March 10, 2023.

- What is debt recycling?, AMP. Accessed online at https://www.amp.com.au/home-loans/managing-home-loan/debt-recycling on March 10, 2023.

- Tax Deduction Definition: Standard or Itemized?, Julia Kagan, Investopedia. Published (updated): Jan 27, 2023. Accessed online at https://www.investopedia.com/terms/t/tax-deduction.asp on March 10, 2023.

- ‘Tax deduction from offset interest used for investment’, ATO Community. Accessed online at https://community.ato.gov.au/s/question/a0J9s0000001E1REAU/p00030208 on March 10, 2023.

- ‘Interest expenses’, ATO. Accessed online at https://www.ato.gov.au/Individuals/Investments-and-assets/Residential-rental-properties/Rental-expenses-to-claim/Rental-expenses-you-can-claim-now/#Interestexpenses on March 10, 2023.

- ‘Diversification’, MoneySmart.gov.au. Accessed online at https://moneysmart.gov.au/how-to-invest/diversification on March 10, 2023.

- ‘Investment Strategy: Ways to Invest and Factors to Consider’, James Chen, Investopedia. Published (updated): May 17, 2022. Accessed online at https://www.investopedia.com/terms/i/investmentstrategy.asp#:~:text=An%20investment%20strategy%20is%20a,%2C%20risk%20tolerance%2C%20and%20goals on MArch 10, 2023.

- NAB EQUITY BUILDER, NAB. Accessed online at https://www.nab.com.au/personal/super-and-investments/investment-lending/nab-equity-builder on March 10, 2023.

- ‘Investment lending’, NAB. Accessed online at https://www.nab.com.au/personal/super-and-investments/investment-lending on March 10, 2023.

- Principal & interest calculator, St George. Accessed online at https://www.stgeorge.com.au/personal/home-loans/home-loan-calculators/principal-interest on March 10, 2023.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

My understanding is, using your first example, borrowing against the home equity is not debt recycling, but leveraging. Lots of examples where people come across debt recycling they also borrow to invest, but the recycling would be using your $20K offset to pay into the non-deductible debt, then split to invest and the interest on that $20K would be tax deductible. The idea being with debt recycling you are using funds (that you would have invested anyway) to convert interest from being non-deductible to deductible, and your overall debt position doesn’t change. Its the tax savings, dividends, and possibly franking credits that accelerate your debt recycling and allow you to convert your debt faster along the way.

Lots of lenders are allowing this, it really just relies on the split loan option and being able to adjust those figures later on. From my reading, this is easier if you are an employee. For self employed people the AMP Master Limit facility may be the most streamlined for future splits.

Family Finance on YouTube has done leveraging and debt recycling and has some good videos on the process, I believe they have their mortgage with BankWest.

There’s a Facebook Group called “Debt Recycling Australia” that you might get more first hand accounts on how others have made this work for them.

My spouse isn’t comfortable with leveraging to invest, but debt recycling to reduce tax paid is fine with them. We’re in the middle of refinancing to an appropriate lender to start the process. If (when) interest rates rise we can review how mush debt recycling we’re doing and pay down the mortgage faster for the “sleep at night” factor