Teaching kids money management has come a long way from a toy cash register and coins in the piggy bank. Spriggy app and card can help teach kids the fundamentals of financial management in a cashless society that turns cold hard cash into an abstract concept, and where money never physically changes hands and relies on fund transfers and tap-and-go purchases. Read on for the full Spriggy review.

The Good

- Teaches kids about personal finance in a way traditional accounts don’t

- Kids can be independent with the money management, with parental supervision

- Parents can see what their kids are spending money on, in real-time

- Instant fund transfers if your kid needs money in an emergency

- Instant card lock is activated through the app if the card is lost or stolen, which can be turned off again if the card is found

- Easy app for kids (and parents) to use

- 30 day free trial is a great incentive to try – no obligations

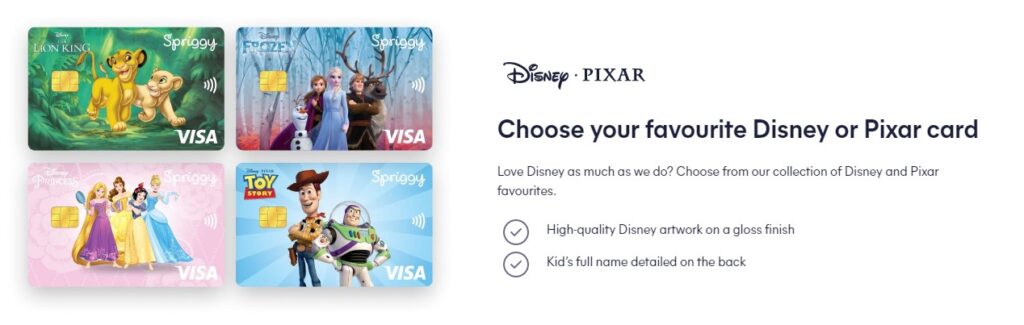

- Cards come in fun colours and designs – marketed to be fun for kids

The Bad

- Annual fee

- No interest on savings accounts

- 3.5% surcharge on overseas transactions

- Maximum balance of $1000 across any one child’s account

Verdict: Financial literacy from a young age is vital. Fees are a bit high but the 30 day free trial is a no brainer. Decide from there.

CaptainFI is not a financial advisor and this article is not financial advice. This website is reader-supported, which means we may be paid when you visit links to partner or featured sites, or by advertising on the site. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Introduction – Spriggy Review

The art of teaching kids money management is an ever-changing landscape. Compared to the education you or your parents may have received, money management has entered a strange new world where even the Barefoot Investor’s saving, spending and giving jars may not be up to the challenge of current-day methods of payment.

In this age of cashless transactions, the tangible aspect of notes and coins has been replaced with the abstract concept of electronic fund transfers and a card to pay for our hearts’ desires.

This makes teaching kids how to manage money, all the more challenging. Spriggy app and card aims to bridge the gap between saving pocket money notes and coins in a piggy bank, with the modern-day reality of tap and go.

What is Spriggy?

Spriggy is a pocket money mobile phone app and pre-paid debit card. Spriggy is the next generation savings style account to teach kids about budgeting, saving and spending. The app and card give kids some firsthand experience in making financial decisions about their money, in what’s becoming a cashless society.

Kids can use their Spriggy debit card to spend their own money on things they want to buy. The Spriggy app lets kids visually see how they plan to budget their pocket money, whether for spending or saving money to reach a set goal, such as a new bike.

Parents have full oversight of the app, and with it, a birdseye view of their kid’s spending habits. Parents transfer funds from their own account into their kid’s pocket money app and card, so they know how much their child has to spend.

Spriggy – Pocket Money. Updated.

How does Spriggy work?

Spriggy app is a mobile phone app for kids’ pocket money. The app is compatible with both Android and Apple mobile phones. Parents can access all features and kids have access to some of the features in the app and card.

Spriggy has a number of features such as instant fund transfers, scheduled fund transfers, a card lock feature in case the child’s card is lost or stolen, and alerts such as when the card is declined. Also, the Spriggy app supports multiple kids on the one family account.

What are the fees for Spriggy?

The annual fee for Spriggy is $30 per child or $2.50 per month, and the card expires each year. They do have a 30-day free trial as well.

While not a fee per se, Spriggy savings accounts don’t earn any interest, which represents an additional cost to using the platform compared to some bank accounts for kids.

The card can be used overseas, but there is also a 3.5% surcharge, which represents another cost to using the app.

Best kids savings accounts in 2022 | Savings Accounts | Mozo

Where can Spriggy be used

The Spriggy card is a Visa prepaid debit card and can be used wherever Visa cards are accepted. This means online and in-store purchases are possible with the Spriggy card.

Spriggy card can be used overseas, with a surcharge of 3.5% for international purchases.

How old do you have to be to have a Spriggy card?

Spriggy is designed for 6 to 17-year-olds.

Spriggy is a step up from coins in a piggy bank, and aims to teach kids about budgeting, saving money, how to spend money responsibly, using a debit card and keeping track of incoming and outgoing funds via the app.

It’s a modern approach to money management for kids.

Can you shop online with a Spriggy card?

Yes, you can shop online with a Spriggy card, as long as Visa is accepted by the site.

Spriggy Cards can be used all over the world, anywhere a pre-paid VISA is accepted. Given this, we also want to be sure parents are confident that their kids are safe when spending and have introduced merchant blocking. This means that the Spriggy Card will only be able to be used at age appropriate places.

Intercom.help/spriggy

Does a Spriggy card really teach kids good money habits?

Research conducted by Spriggy suggests that 66% of kids find saving easier with Spriggy and 51% of kids are motivated to earn more money.

Spriggy seems to be the next step up in teaching kids about money in what is often a cashless society. While coins in the piggy bank have their place with the little kids, the fact is, money can become an abstract concept with the likes of payWave and tap-and-go purchases.

Spriggy appears to fill the void between the piggybank and the PayWave. The debit card, combined with the Spriggy app creates a tangible link between the money and the purchase that otherwise can be missing.

Spriggy seems to go beyond the money, into personal finance and digital money management that can help prepare kids for the real world.

Teach Your Kids Good Money Habits – Forbes Advisor

Advantages of using Spriggy

- Teaches kids about personal finance in a way traditional accounts don’t

- Kids can be independent with the money management, with parental supervision

- Parents can see what their kids are spending money on, in real-time

- Instant fund transfers if your kid needs money in an emergency

- Instant card lock is activated through the app if the card is lost or stolen, which can be turned off again if the card is found

- Easy app for kids (and parents) to use

- 30 day free trial is a great incentive to try – no obligations

- Cards come in fun colours and designs – marketed to be fun for kids

Disadvantages of using Spriggy

- Annual fee

- No interest on savings accounts

- 3.5% surcharge on overseas transactions

- Maximum balance of $1000 across any one child’s account

“We believe that the best way for kids to learn is to let them give it a go.”

Spriggy.com.au/aboutus

How do you set up a Spriggy card?

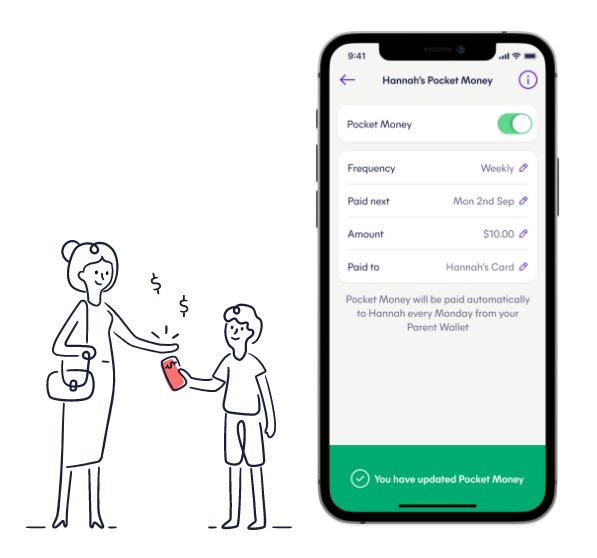

To start, a parent needs an Australian mobile number, email address and Australian bank account. Download the Spriggy app onto your and your kids’ phone. Register in the app, and enter your details, such as your bank account. The app needs to be linked to a parent’s bank account or debit card account. Parents can then transfer money into the Spriggy Parent Wallet, which your child can’t see or access. From there you can transfer all or part of the money into your kid’s Spriggy pocket money account. For example, you can transfer $100 once a month to the Parent Account, then $25 per week to your kid’s Pocket Money account.

With cold hard pocket money in their Spriggy account, your child has two choices; either transfer the money into the Savings Goals account to save for a set goal or send the money to the Spriggy Card account for spending via the child’s Spriggy card.

The app lets your child set up a number of savings goals, so they save for a number of goals at the same time.

It takes about 7-10 days for the card to arrive, after which you can activate it by entering the last four numbers.

FAQs about Spriggy:

Is Spriggy owned by a bank?

Spriggy is not owned by a bank. Spriggy is owned by its team members. Money received by Spriggy goes into an account held by a bank called Indue which is a Brisbane-based Authorised Deposit-Taking institution that falls under banking regulation.

Spriggy also has a relationship with NAB, who pays the Spriggy fees for eligible families.

What is the relationship between Spriggy and NAB? | Spriggy Help Centre (intercom.help)

Money App Spriggy Review 2021 | Australian Money App Spriggy | Mozo

How do you withdraw money from Spriggy?

To withdraw money from Spriggy, you have to do an electronic fund transfer from your child’s account to yours.

ATM cash withdrawals are not enabled on Spriggy cards. Currently, Spriggy is testing this feature with some families, but it is not available as standard.

Can you add Spriggy to Apple Wallet or Google Pay?

You can connect your child’s Spriggy card to Apple Pay if they are over 13 years old.

If you log on to the App with your parent login, go to “Settings and tap “Help”, then “Member Help”. From there, tap “Start a conversation”, then tap “Apple Pay” (or “Google Pay”) and follow the prompts.

How can I set up my child’s Spriggy Card on Apple Pay? | Spriggy Help Centre (intercom.help)

Do Spriggy cards have a PIN?

Spriggy cards have PIN-protected access.

Is Spriggy safe?

Spriggy is not a bank, and as it doesn’t hold your money, if Spriggy went out of business, your money should be ok.

However, the Spriggy program is not covered by the Australian Government’s Financial Claims Scheme (FCS) which gives financial protection when banks go bust. Your child’s money isn’t covered by FCS because the Spriggy program uses prepaid debit cards through a bank called Indue, not deposit accounts. If Indue went broke, your child’s money could go with it.

Conclusion – Spriggy Review

It’s a new frontier when it comes to teaching kids how to manage money in this digital age. In the past, kids were given cash as pocket money. With the evolution of a cashless society, preparing kids for the realities of modern money management has changed.

Spriggy app aims to bridge the gap, introducing kids to budgeting, saving and spending with a phone app and prepaid debit card.

While Spriggy is not a bank and doesn’t pay interest on savings, many families see value in the $30 annual fee when it comes to being able to teach their kids the concept of how to manage money in this cashless society, from a young age.

Further reading – other Bank reviews

Check out my list of bank reviews here to see how the competition stacks up, and to find the right bank for your journey to Financial Independence

- Commonwealth bank

- NAB Bank

- ANZ Bank review

- Westpac Bank review

- ME Bank review

- ING Bank review

- UBank review

- HSBC Bank review

- Up Bank review

- 86400 Bank review

- Finspo review

- Spriggy review

- Up Bank review

Financial Disclaimer

Financial Disclaimer: CaptainFI is NOT a financial advisor and does not hold an AFSL. This is not financial Advice!

I am not a financial adviser and I do not hold an Australian Financial Services Licence (AFSL). In this article, I am giving you factual, balanced information without judgment or bias, to the best of my ability. I am not giving you any general or personal financial advice about what you should do with your investments. Just because I do something with my money (or use a particular service or platform) doesn’t mean it is automatically appropriate for your personal circumstances. I do not recommend nor endorse any financial or investment product, and my usage or opinion of any product should not be interpreted as an endorsement, advertisement, or intent to influence.

I can only provide factual information based on my journey to Financial Independence, and that is provided for general informational and entertainment purposes only. I make no guarantee about the performance of any product, and although I strive to keep the information accurate and updated as it changes, I make no guarantee about the correctness of reviews or information posted.

Remember – you always need to do your own independent research and due diligence before making any transaction. This includes reading and analysing Product Disclosure Statements, Terms and Conditions, Service Arrangement and Fee Structures. It is always smart to compare products and discuss them, but ultimately you need to take responsibility for your use of any particular product and make sure it suits your personal circumstances. If you need help and would like to obtain personal financial advice about which investment options or platforms may be right for you, please talk to a licensed financial adviser or AFSL holder – you can take the first steps to find a financial advisor by reading this interview, or by visiting the ASIC financial adviser register and searching in your area. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Great review! I’m considering getting the Spriggy card to help teach my kids about saving and budgeting. Thanks for sharing your experience with this product.