Finspo is an online mortgage broker with an app to help you find a home loan and pay it off as soon as possible. So are they really worth it and is it free? Read on..

The Good

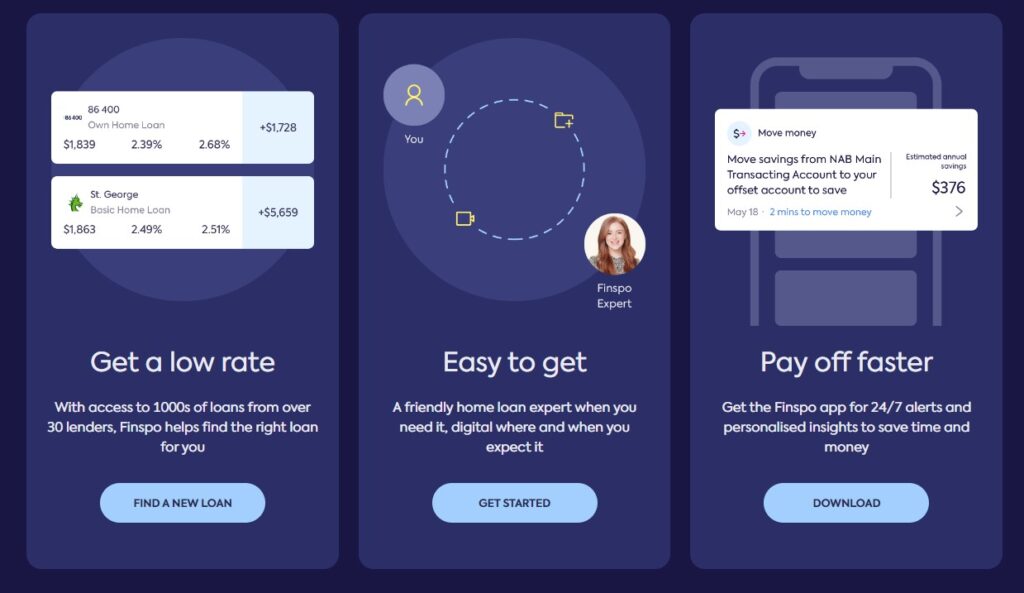

- Finspo can guide you through the process of getting a home loan.

- Finspo is good for people who want to save time on doing the research or are not confident to do the research necessary to get a home loan.

- Finspo has financial experts who may be able to make suggestions that you haven’t thought of.

- If you deal with Finspo, you may be able to get better terms on your loan than if you go to the lender directly.

- Everything is done online

- If you use the app, you will receive automatic notifications about changes in interest rates and other information

- Finspo website has a blog with helpful articles

The Bad

- Finspo works with lenders that they have an arrangement with. By using Finspo you might be losing out on a better deal because Finspo does not work with that specific lender.

- It might be more time consuming to deal with a mortgage broker instead of going directly to the lender.

Verdict: Finspo may not have access to all lenders but they have access to many. It makes sense to try them out for free!

Introduction

Finspo is a digital-first mortgage broker that works with a number of lenders and allows its customers to get better deals on home loans. With the help of the Finspo app, customers can manage their money more effectively and possibly even pay off their home loans faster. Finspo does not charge its customers. Instead it takes its commission from the lender, but despite this, Finspo may still be able to get its customers a better rate than if they negotiated directly with the lender. Before applying for a home loan, it is probably worth consulting with Finspo and comparing its rates with lenders’ advertised rates.

CaptainFI is not a financial advisor and this article is not financial advice. This website is reader-supported, which means we may be paid when you visit links to partner or featured sites, or by advertising on the site. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

What is Finspo?

Finspo, which was established in 2019, is an Australian company that has the aim of helping Australians to pay their home loans faster. They are a digital-first mortgage broker with a team of mortgage brokers, software developers and designers who work together to help users to get a home loan and to pay it off faster. Finspo takes a commission from the lenders, not the borrowers, so whether or not you use Finspo, you will not pay more for your mortgage.

“The universe of mortgage lending has gotten to the point where there is a place in it for everybody.”

Joe Mays

Is Finspo just an online mortgage broker?

Mortgage brokers are financial professionals which specialise in helping their clients find home loans, so it is fair to say that Finspo is a mortgage broker. While they do not call themselves an “online mortgage broker”, they can be defined as online mortgage specialists as they do the work online through the website or the app. The term that Finspo uses is “digital-first” which means that they try to use technology as much as possible. To learn more about mortgage brokers, see this article on Canstar.

Is it free?

Both the Finspo website and the app are free for users. You do not have to use the Finspo mortgage brokers to use the app. Anyone can connect their bank accounts to this app.

How does Finspo make money?

Finspo makes money by receiving commissions from lenders. Finspo has agreements with more than 30 lenders. When you get a home loan through Finspo, the loan rate will be the same as if you have approached the lender directly, but the lenders will pay Finspo.

Is a home loan more expensive through Finspo?

According to the Finspo website, users do not pay more if they use Finspo. They also say that they might be able to negotiate a better deal than the advertised rate.

How many lenders do they have access to?

The website says that they have agreements with more than 30 lenders. They do not specify exactly which lenders on their website.

Does Finspo help you pay off your home loan quicker? How?

Bank products are complicated and it is difficult to know how much you can save when dealing with banks. Banks are free to change their prices or introduce new fees without asking their customers. For example, it is easy for banks to raise interest rates, and they may not even tell their customers. As well as charging their customers more, banks may not tell their customers when they are doing something that is costing them money. For example, if you need to pay interest on your credit card, they might not tell you in a timely manner, resulting in late fees. When customers connect their accounts to the Finspo app, Finspo can give customers an idea about what their banking is costing. The app will give you information about your specific banking product and how to save. There are 3 main ways to save money:

- New customers pay less interest than older customers. According to Finspo, the average difference is about 0.5%. It may be worthwhile to consider refinancing your loan with a different lender after a few months to take advantage of these low interest rates for new customers, or you may be able to renegotiate with your current lender for a better rate. Finspo can help you with this.

- Many bank customers are unaware of all of the fees that they may be paying. For example, when you buy a product online, the bank may charge foreign exchange fees. Finspo can help customers choose options that allow them to avoid paying those fees.

- Finspo can help customers manage their cash balances across all their different accounts. It is not in the best interests of the bank to help you reduce the amount of money you pay them. The bank won’t tell you that your money is in an online savings account that is at the end of its bonus period so you are earning very little interest. They will also not point out that when you have a credit card accruing large amounts of interest, it would be better for you to pay it off rather than keep your money in savings which are not earning much interest.

The advantage of using Finspo is that they can give advice that will allow customers to make better financial decisions. By connecting your accounts to Finspo, they can analyse your accounts and make sure that you are doing what’s best for you, not what’s best for the bank.

For more information about how to pay your home loan off faster, see this article on nano.com.au.

Advantages of using Finspo?

- Finspo can guide you through the process of getting a home loan. Getting a home loan can be complicated and time consuming. Not everyone knows what they need to do. With advice from the financial experts at Finspo, you will not make any mis-steps that slow down the process.

- Finspo is good for people who want to save time on doing the research or are not confident to do the research necessary to get a home loan. You can save a lot of time as Finspo has already done the research and negotiated with the lenders for the best possible deal. Finspo has access to more than 30 lenders, saving you the time and effort of contacting each one separately.

- You may not have all the information that you need to get the best possible home loan. Finspo has financial experts who may be able to make suggestions that you haven’t thought of.

- If you deal with Finspo, you may be able to get better terms on your loan than if you go to the lender directly.

- Unlike banks, there is no need to go into an office for meetings as everything is done online through video calls, emails, or even the app.

- If you use the app, you will receive automatic notifications about changes in interest rates and other information such as how to pay your loan off sooner and how to reduce fees and interest.

- Finspo website has a blog with helpful articles related to home loans, interest rates, refinancing and mortgage brokers.

“We know all about the fine print. In fact, when it comes to home loans, we have a fine time in the fine print. We have a professional interest in interest. We’re drawn to redraw. And offset? I’d say we’ve got everything lined up. So now, we banking insiders are on your side.”

finspo.com.au/about

Disadvantages of using Finspo?

- Finspo works with lenders that they have an arrangement with. By using Finspo you might be losing out on a better deal because Finspo does not work with that specific lender. Therefore, it is a good idea to research a number of mortgage brokers before making a decision.

- It might be more time consuming to deal with a mortgage broker instead of going directly to the lender. If you know which lender you want to use, it may be quicker and easier just to make a loan application directly to the lender.

FAQs about Finspo:

Who owns Finspo?

The 3 founders of Finspo are Angus Gilgillan, Bill Armour, and Josh Brougham. Currently, Angus Gilgillan is also CEO of the company. All 3 of the founders have decades of experience working for the big four banks (NAB, ANZ, CBA & Westpac).

Where are they based?

Finspo has their headquarters in Melbourne, but as a digital-first company, they are easily contactable all over the country.

Is there an app?

The Finspo financial app is an additional service as the app lets you know when a better rate is available for your loans, how your money could work harder for you, and/or where you can save on fees. If you have connected your bank accounts to the app, then alerts will show you when you are being charged a fee or when your interest rate changes. You can also see how much faster you might be able to repay your loan.

Are Finspo trustworthy?

Finspo seems to be a trustworthy company as they claim that they have the same level of security as a bank. They point out that banking credentials are not stored in the app and that data is encrypted for transfers and storage on SSFL/TLS connections, since they are using bank level security protocols.

Finspo has an Australian Credit Licence (ACL) For more information about what activities someone with an ACL can do, see this article on the CPA Australia website. Australian Credit Licences are regulated by the Australian Securities and Investments Commission (ASIC). All of their home loan experts are fully qualified with industry certification.

Conclusion

If you are thinking about getting a home loan, it pays to do research, especially with rising interest rates. A mortgage broker can often help you to get a better deal from the lender. Finspo can help you to find and negotiate a home loan with one of the 30 lenders that it deals with. In addition to its services as a mortgage broker, Finspo has an app. Customers can connect multiple accounts to the app and receive notifications about changes in fees and interest rates and information about how to manage their money. When you start doing research, it is a good idea to see what Finspo can offer you. You can also look into options such as debt recycling to pay off your home loan quicker. You can read my article about Debt Recycling HERE.

CaptainFI is not a financial advisor and this article is not financial advice. This website is reader-supported, which means we may be paid when you visit links to partner or featured sites, or by advertising on the site. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Further reading – other Bank reviews

Check out my list of bank reviews here to see how the competition stacks up, and to find the right bank for your journey to Financial Independence

- Commonwealth bank

- NAB Bank

- ANZ Bank review

- Westpac Bank review

- ME Bank review

- ING Bank review

- UBank review

- HSBC Bank review

- Up Bank review

- 86400 Bank review

- Finspo review

- Spriggy review

Financial Disclaimer

Financial Disclaimer: CaptainFI is NOT a financial advisor and does not hold an AFSL. This is not financial Advice!

I am not a financial adviser and I do not hold an Australian Financial Services Licence (AFSL). In this article, I am giving you factual, balanced information without judgment or bias, to the best of my ability. I am not giving you any general or personal financial advice about what you should do with your investments. Just because I do something with my money (or use a particular service or platform) doesn’t mean it is automatically appropriate for your personal circumstances. I do not recommend nor endorse any financial or investment product, and my usage or opinion of any product should not be interpreted as an endorsement, advertisement, or intent to influence.

I can only provide factual information based on my journey to Financial Independence, and that is provided for general informational and entertainment purposes only. I make no guarantee about the performance of any product, and although I strive to keep the information accurate and updated as it changes, I make no guarantee about the correctness of reviews or information posted.

Remember – you always need to do your own independent research and due diligence before making any transaction. This includes reading and analysing Product Disclosure Statements, Terms and Conditions, Service Arrangement and Fee Structures. It is always smart to compare products and discuss them, but ultimately you need to take responsibility for your use of any particular product and make sure it suits your personal circumstances. If you need help and would like to obtain personal financial advice about which investment options or platforms may be right for you, please talk to a licensed financial adviser or AFSL holder – you can take the first steps to find a financial advisor by reading this interview, or by visiting the ASIC financial adviser register and searching in your area. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.