This month I made the difficult (but right) decision to take the rest of the year off flying work, so that I could spend quality time with my family amidst a pretty difficult time for us. Whilst this meant that my main income was reduced (and will continue to be), I started to see some revenue from my digital business (which I continue to invest time and money into) as well as continued to sell my stuff to make up the short fall. Overall the savings rate took an appreciable hit, but I am way happier and less stressed out.

September update

So it turns out that both of my (separated) parents will need major surgeries throughout the remainder of the year. There is a decent level of risk with each procedure, so I do not want to take the risk of not being home with my family while I can which is why I have taken a ‘sabbatical’. The travel home was difficult and expensive, and due to COVID-19 I had to isolate for two weeks upon arrival. It was worth it, and being back home with close access to my family, friends, pets, animals, gardens etc has made a huge difference. I feel much calmer and less stressed out, now that I can actually help support my family and spend quality time with them while I can. I’ve been able to get a good nights sleep, and I feel like I’m not grinding my teeth in my sleep as much.

My old man has pretty much been in the hospital for about two months now ever since he was medivac’d from the farm with septacemia. He was subsequently airlifted to the city hospital thanks to the Royal Flying Doctor Service (which is an amazing organisation to get behind and support!) for major surgery. He is is dealing with some pretty nasty complications from his chemotherapy treatment resulting in some amputations, vascular surgery and upcoming heart surgery. It is very difficult to see someone who was previously so capable and who used to be your idol in such an state, but ultimately his lifestyle choices have led him down this path.

I have no idea how the situation will pan out, but if he doesn’t change his lifestyle he will drink and smoke himself into an early grave. I am currently wading through paperwork reading about aged care and needs assessments, and it is increasingly looking like he may not return to the farm which might turn into a massive financial / estate shitfight. Despite his grumpiness he has been fantastic with my nephew though, playing games and telling him stories and jokes whenever we visit, and I can already see the respect and admiration my nephew has for his ‘naughty grandad’ as we call him.

Mum will also need a big operation soon to correct a complication from her previous cancer surgery. It turns out when they ‘stitched her up’ a few years ago after she had all her ‘bad bits’ removed, the surgeons didn’t exactly do the best job and now shes having some significant health issues. As a result of this she has had to ‘retire early’, and I am working closely with her to organise her finances and superannuation so that she doesn’t have to sell her home to fund her retirement. Being a single mum, her super balance is far less than the average and much less than what I think she needs for a comfortable retirement – so we are exploring other options to supplement her income (exploring welfare eligibility, casual contract work, taking in a border or exchange student etc).

I think I have got her super mostly skun, but we are meeting with a financial advisor to chew the fat. I am highly skeptical of the financial adviser, especially so after our phone call together (they want to manage her estate and charge percentage fees plus extra for reports, whereas I would prefer to pay a flat hourly rate for advice).

Personally, I have also relished the time to work on a heap of overdue stuff I wanted to explore on CaptainFI. This has included getting draft articles released, interviewing guests for the podcasts, web dev and optimisation stuff as well as negotiating with potential sponsors (such as for the podcast). I’m looking forward to being able to secure sponsors so I can afford to ‘lash out on a better editor (than myself!) and focus my efforts on the ‘creative’ stuff rather than the ‘doing repetitive jobs’ stuff.

I have also continued to work on my group of other sites which will be the main income earners (although they are much less fun and creative than CaptainFI), as well as working on DIY projects and rennovations for my family. I am back on the tools building another couple of fences, as well as the usual gardening duties in the veggie patch and the orchard.

End of financial year tax return is still outstanding…

When the tax statements for the ETFs and LICs in my portfolio are all finalised (around October-ish) and I am back home, I will print Sharesight tax summary for my index funds and then take it down to my accountant, pay $300 and walk away with an estimated $5,000 tax return. I am not banking on getting this return, but when I do get it I will be putting it half into the mortgage offset account and half into my brokerage account for buying more index funds.

Saving rate

My Saving rate was 61% in September. This is because of reduced income, increased personal discretionary spending (traveling home as well as working on DIY projects for the family) as well as spending on my personal business startups which don’t have a formal structures yet.

Income

Income from this month was down significantly. I am now on an extended period of leave from flying (basically using up all forms of leave before taking a ‘sabbatical’) so I got some baseline income from there however no additional flying pay or allowances. However on the plus side, my online businesses managed to produce nearly $1,000 this month – I obviously have to declare and pay tax on this eventually, but I have been reinvesting earnings back into the business and hope to grow its ability to produce income. I was paid about $190 in dividends this month and chose to reinvest this along with the $3 of interest on my P2P lending.

Spending

Spending was significantly up in September. Travel costs were high as I headed interstate (and quarantined for two weeks!), plus a heap more business expenses saw the savings rate take a nose-dive. Since I have been home I have also just been generally spending more as I work on renovations and projects for my family, as well the odd discretionary spending here or there. I actually bought McDonald’s for the first time in years because of the Monopoly deal (spoiler alert I didn’t win anything and it gave me the squirts) so I fairly instantly regretted that purchase.

Investing decisions

This month I invested $5,445. Technically I also invested a further $2,500 into my business however I am not sure how to account for these expenses for now until I establish a proper framework and see some good cash flow from them.

$3,542 went into the share market this month through SelfWealth with a purchase of 15 shares of Vanguard Total US Market index fund (ASX:VTS). This was because it was one of my lowest splits and the US share market had experienced a bit of a dip (compared to VEU), so I tried not to overthink it and just click buy. Surely the US election presidential debates will result in more volatility.

Property

I transferred $900 into the property fund, as well as $1000 into the mortgage account.

P2P lending

I didn’t invest anything more into P2P lending through Plenti, but I did get $3 of ‘interest’ which was then re-invested into the fund.

Personal business

$2500 went into paying various costs for my personal business; I’m technically I am chalking these up to personal costs at the moment, but they will pay off eventually. The websites are making some money, but considering the amount of money and huge amount of time I am putting into the 5 sites, the return isn’t quite there yet.

Because I recently set up my trade confirmation emails between SelfWealth and Sharesight, my portfolio accounting is completely hands free. I simply log in to confirm all the trades and dividends over the year when needed for my tax return, or to produce these monthly updates for you guys. The following section contains Sharesight reports for;

- Monthly

- Financial year to date

- Rolling 12 months

- Since Inception (since I started tracking it with Sharesight).

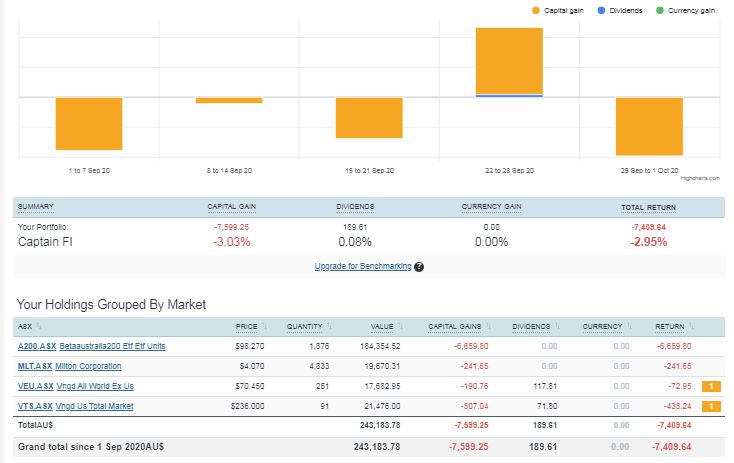

From the Sharesight reporting, the portfolio is overall down by about 3% in September. I am expecting rocky times ahead for the rest of this year, but sticking to my buy and hold investment strategy.

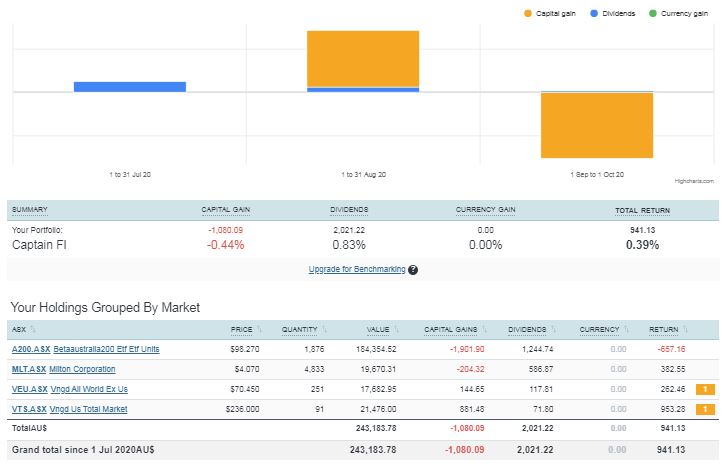

This financial year to date has basically broken even. Dividends that were paid out have offset share prices going down. This kind of thing annoys me because I feel like I am being taxed on the dividends but it seems like the dividends are coming out of the share price, so my net position doesn’t change but I get a tax bill, and I’m up for brokerage when I re-invest the dividends (I mean I am going to reinvest them anyway, and I only pay a flat fee brokerage with Selfwealth so it doesn’t matter too much). This has got me thinking, perhaps during the accumulation phase (pre-FIRE) it might be a more tax effective strategy to invest in growth ETFs like VTS, VGS and property with higher capital growth, and then during the retirement phase (FIRE) to slowly sell them off or switch them into a higher dividend yielding investments like LICs or Aussie ETFs Betashares A200 or Vanguard high yield VHY. Of course, I know that the dividend approach is more ‘crash proof’ due to dividend stability, so maybe it is ‘much of a muchness’ and I just need to crack on and continue to buy and hold a mix of both.

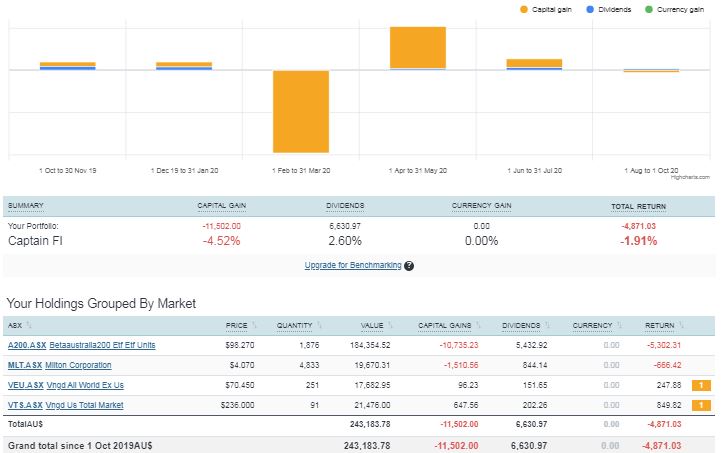

The rolling 12 month performance is still in the negatives due to the COVID-19 crash, but when we put things into perspective its not even a 2% drop in total return. I am expecting over time for the portfolio to recover and get ‘back in the black’ however I am not holding my breath as it will be a rocky road ahead with the impact of COVID-19 on the economy (especially small businesses).

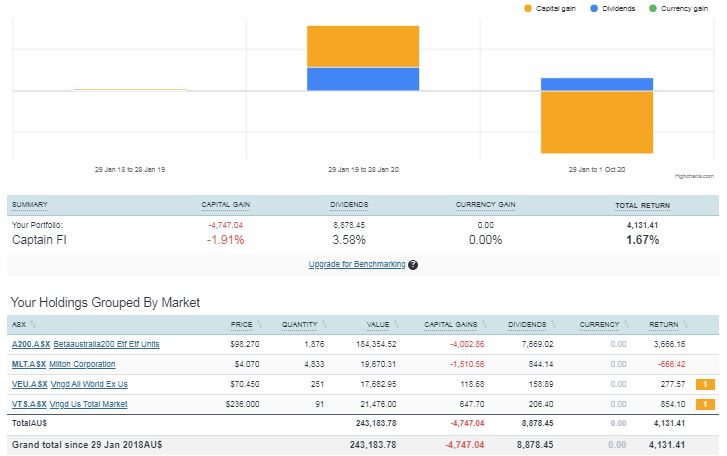

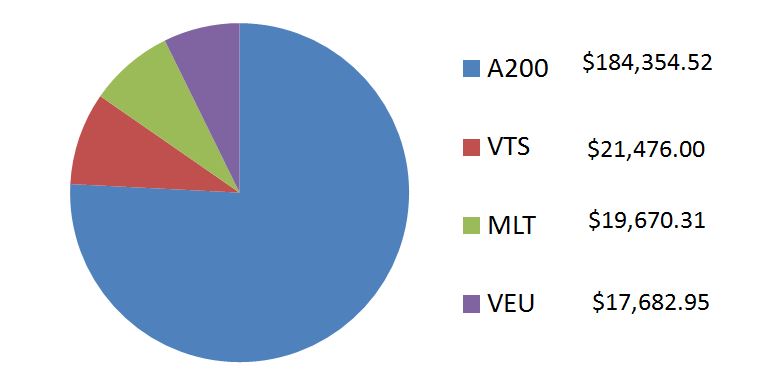

This is the total return since I started using Sharesight and switched to a core holding of A200, VTS and VEU complimented by LICs (currently Milton). I guess I would have been better off just putting my money in a term deposit right? Ha-ha not really, the COVID-19 market crash has had a significant impact on share markets globally, and no one can predict these ‘black swan’ type events which seem to happen every 10 years or so.

“Whilst past performance is no indicator of future performance” with incentives for those in power to maintain the status quo and world order, fiat currency and inflation the way it is, I would have a very hard time imagining the price of equities wouldn’t continue to trend upward in the long term the way they have for hundreds of years – with gut wrenching volatility (like this) along the way of course – what other options to you have anyway?

Pie chart

Because sometimes you just need a pie chart to visualise what a portfolio looks like

Investment Property

Nothing much to report here, everything is ticking along exactly the same and I continue to add money to the mortgage offset and buffer. The next big milestone will be the DA approval so we can pour the slabs, which I am hoping will happen by the end of this year.

Buisness portfolio

My buisness portfolio includes a number of websites which make income from;

- Advertising (direct with Google ads).

- Affiliate marketing.

- Digital products.

- E-commerce.

Last month was my biggest return yet, with $960 of “revenue”. This was mainly down to ad revenue and affiliate marketing. Of course, this was all reinvested back into the development of the sites, alongside another $2,500 of my own money. As web buisnesses are conservatively valued at 30x monthly earnings (depending on niche and content, I have seen some websites trade as high as 70x, but some average sites that need a lot of work might go for 20x), this makes the portfolio valued (conservatively) at around $29,000.

Retirement

Because of the additional work and repetition in this section every month, I am moving it to its own dedicated article which I will periodically update and link to in my ‘about me’ section – I am thinking each year I might provide an update on what the situation is rather than spending so much time fussing over it each month.

For now though, I have smashed my ‘Single FIRE’ goal of $2,000 per month, and am still working toward my ‘Family FIRE’ goal of $6,000 per month. When looking at the future trust structure, to earn $6,000 per month after tax it will more or less take $6,800 of gross portfolio income. Currently, I am at $2,500 out of the $6,800 goal, or just over a third of the way to ‘Family FIRE’!

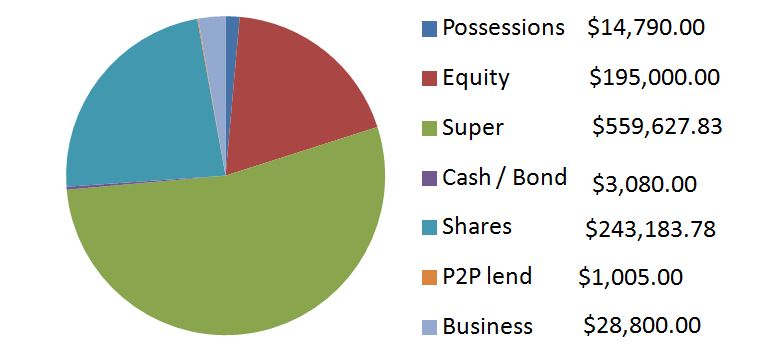

Captain FI Net worth August 2020

The Net Worth pie chart is still dominated by my super. Clearly Cash / bond and my P2P lending experiment make up very minor fractions. Listed in order of size is;

- Super

- Shares (ETFs + LICs)

- Equity (Investment property)

- Business (digital portfolio)

- Physical posessions (stuff that I own)

- Cash / Bond

- P2P lending

Captain FI Net Worth Progression

Tracking your Net Worth over time is one way to monitor and compare your progression to FIRE. A better way though, is to track your passive income – such as dividend income. Because that is what you are going to be using to live off if you do choose to retire early. Because of how I have my finances structured as an Australian investor with a significant amount invested in Superannuation, my NW number isn’t really all that reflective of my ability to FIRE, but I still think it is an important metric to track since its growth is representative of performance – the rate of change of net worth is more important than Net worth by itself, in my opinion.

CaptainFI Net Worth Progression – Graph

The Net worth progression graph is rather crudely constructed in Excel, but still demonstrates the ‘somewhat exponential’ journey over the past 12 years.

CaptainFI Net worth progression – table

I decided to include a Net worth table which provides a bit more information on my journey for anyone wanting to go back and see how individual years or months went at a quick glance.

| Date | Net worth | Difference | Saving Rate | Notes | |

| Jan 09 | $5,000.00 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK | |

| Jan 10 | $24,000 | +$19,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 11 | $40,000 | +$16,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 12 | $92,000 | +$50,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 13 | $130,000.00 | +$38,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 14 | $161,000.00 | +$31,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 15 | $200,000.00 | +$39,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 16 | $281,000.00 | +$81,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 17 | $340,000.00 | +$59,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 18 | $482,000.00 | +$142,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jan 19 | $542,000.00 | +$60,000 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK |

| Jul 19 | $578,900.00 | +$36,900 | 84% | Finally began tracking NW this like a proper adult. | |

| Aug 19 | $560,100.00 | -$18,800.00 (-3.2%) | 78% | Share market slight correction, Ok savings. | |

| Sep 19 | $584,744.88 | $24,644.88 | 72% | Share market rebound, savings rate not so good. | LINK |

| Oct 19 | $600,386.00 | $15,641.12 | 84% | Good saving this month. Normal salary, plus allowances, dividends from index funds, tax refund, eBay selling and was working abroad in asia where things are cheap. | LINK |

| Nov 19 | $612,917.21 | $12,531.21 | 76% | Falling short of my savings goal of 80%. Mostly domestic legs this month with higher costs. Also invested in hydroponics. | LINK |

| Dec 19 | $625,350.00 | $12,432.79 | 76% | Good savings of cash (for development) and investment, however higher spending due to Christmas period (Travel and Gifting). | LINK |

| Jan 20 | $865,212.00 | $239,862.00 | 55% | Super settlement was a HUGE boost to NW. $9K growth from stock market. Expensive month lots with lots of unexpected bills – weddings, travel, Booking flights, fines etc. | LINK |

| Feb 20 | $851,802.0 | -$16,592 (-1.9%) | 52% | Large increase in spending on myself this month, still managed to tuck away $5K to put into shares and property. Corona Virus market scare resulted in a correction and gave NW a small negative trend. Time in the market not Timing the market! Became Single again. | LINK |

| Mar 20 | $819, 354.6 | -$31,806.95 (-3.7%) | 80% | Another small step backwards in the NW due to the ‘corona crash’ in full swing. FIRE Portfolio of ETF/LICs down about 15% this month, however due to high savings rate and structure of my superannuation annuity the NW is only down 3.7%. Savings rate good at 80%, higher than usual income (with some slightly higher spending, too). Picking up shares on discount – this is the best outcome for someone in the accumulation phase with good income! | LINK |

| Apr 20 | $847,023 | +$27,668 | 85% | $11,000 in rebound of stock market capital prices alone (up 6%), plus first quarter dividends paid (heavily reduced due to banks withholding dividends). Great savings rate due to COVID-19 lock-down = no spend. Increased entrepreneurial efforts and selling down of physical possessions provided side hustle income. Two standard paychecks from flying activity; domestic day trips only so no allowances. All cash unfortunately had to go into the property development due to contract timing, I am chomping at the bit to buy some more index funds before they go back up in price too much – hence why I am selling most of my toys! | LINK |

| May 20 | $857,859 | +$10,836 | 92% | Some Great sales as I let go of my Super Sport Motorcycle, Some gym gear, expensive flying equipment and a few other various bits and bobs and invested this money. Flying still reduced, but increasing from April. The share market grew as I continued to make my fortnightly investments. I also wrote down the ‘value’ of some of my possessions (liabilities) such as my car, tools and furniture by around $10K to align them to market price (“tell him hes dreaming…!”). | LINK |

| June 20 | $858,650 | +$791 | 90% | Small Net Worth gain as I continue to declutter and simplify my life, despite being off work due to a family emergency. Share market not doing much. | LINK |

| July 20 | $888,218 | +$29,568 | 68% | Majority gain due to share market going back up, low spending due to being on the family farm and at home because of lock down. | LINK |

| Aug 20 | $1,029,293 | +$141,075 | 74% | Became a millionaire. Achieved this massive milestone I set out for myself in Dec 2019. Included unrealised gains in my property development as well as website business. Good savings rate due to not much spending, invested in Aus and total world shares. Investing in my web business. Starting to shift focus away from $$$ and more into looking after my mental health. | LINK |

| Sep 20 | S1,045,486 | +$16,193 | 60% | Officially took time off work for the rest of the year to be close and look after family during major operations. Continued to sell down physical possessions and work on digital business while at home. NW gain mainly due to valuation of websites. |

Monthly question from the Captain

Have you ever tried Matched Betting? I have been experimenting with it lately (and even published this article) and would love to hear if anyone has had any success stories!

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Just looking at the portfolio, Super Balance is awesome, can almost let it run :o)

With the Investment Property and awaiting DA, is the equity the increase in value of the land since purchase?

G’day Baz, it’s probably not the kosher way to look at it but I’ve simply taken the banks valuation on completion and subtracted the loan amount I owe against it, and hen each month I’m factoring in extra repayments against it. When it’s all finished I’m hoping to continue with an interest only loan and won’t make any extra repayments

Congrats on becoming a millionaire! Appreciate how detailed your posts are. Great to see what your income, savings rates and investment activities are.

Thanks Jordan! I don’t think it changes much for me but certainly a nice milestone moving forward. Appreciate the positive feedback mate, it does take a whole to put these reports together so I am glad you are getting value out of it! Cheers