It has been a big month, and well, a big year. Lots of changes have happened to me, and a lot of personal growth.

June update

Probably one of the biggest things that happened to me this month was I took time off work to go and look after my sick Father, due to an unexpected and rapid downturn in his health. He has Leukemia and is going through chemotherapy (lots and lots of pills!), but also has some further complications with other health issues that needed surgery and specialist attention.

One of the things that has been pretty heart-breaking to watch is him down his cancer medication with a cigarette and can of beer in the other hand. I am slowly coming to terms with ‘the circle of life’, and understanding that this is the man that I once looked up to as the ultimate Alpha-male.

We don’t know how much longer he has left, but he isn’t really doing himself any favors. He claims it is too late to change, but this is something we don’t see eye to eye on. Regardless, he is my Dad and I love him, and I am forcibly salvaging what I can of a father/son relationship while I can.

I am thankful for this opportunity, and made the long interstate trip from Sydney down to the farm, crossing three borders and driving border police checkpoints nuts as they try to combat the spread of COVID-19. I had special permission to travel on compassionate grounds, but not one officer asked to see the approval or cared when I presented it.

Since arriving I have been slashing, mowing, burning, cleaning, building chopping, stacking and stoking my days away – that last one is more referring to keeping the shacks internal combustion heater going, but is probably an apt description of much passive cigarette smoke I have inhaled.

I am also incredibly thankful for some of my best mates who actually themselves made their own road trips from various parts of the country to lend a hand getting the property back up to scratch. That’s one of the best things about the country I think – the sense of community and mate-ship.

I have started dreaming about buying an old tradie van like a Hiace or Transit van and doing it up into a mini mobile home or camper van. I have spent far too long researching vehicles, carpentry and the electrical system (4 big solar panels, a regulator, two deep cycle sealed heavy marine batteries, an inverter and some LED lights are all I would need!). I think I could set up an awesome camper for under $10,000, and could easily get half of this by selling my current ride. Perhaps a project for retirement.

End of financial year tax return

One of the big issues now is the end of the financial year is of course doing my tax. I used Sharesight to prepare my tax return for my share portfolio. Of course, part of my big changes this year was really simplifying the way I invest. This means I have sold some shares, and mainly bought ETFs and LICs to replace them.

Thanks to Sharesight I can ditch the excel spreadsheet and just print off their completely free report. All I did was then sub in my work related tax deductions, gathered all my payslips and payment summaries for other taxable things (like bank account interest, RateSetter and affiliate income) and printed off all these documents and collected receipts into a big envelope. When the tax statements for the ETFs and LICs in my portfolio are all finalised (unfortunately around October-ish), I will reprint the Sharesight tax summary and then take it down to my accountant, pay $300 and walk away with an estimated $5,000 tax return.

Blog update

The Blog is going pretty well, I have now got a bunch of posts and articles cued up which will be released at the rate of one per week. This should take the blog well into 2021, with some exciting stuff planned.

One of the topics I am having a lot of fun researching and writing about is about the cost of raising children. I’m actually looking right into it, speaking to hundreds of parents and reading lots of published journal articles from economists. There is some awesome stats, and its also leading me perfectly into my Australian Healthcare (and health insurance) article.

I have set up affiliate programs with Sharesight which is my tax accounting software, and with Selfwealth which is my stock broker. Both links give readers of the blog access to a premium subscription for free – 4 months and 90 days respectively. SelfWealth also gives you 5 free trades (the normal cost is $9.50 each).

These Affiliate programs don’t just benefit the reader – I should get a small payment from Sharesight (but I haven’t yet), and Selfwealth gives me the same deal you get – 5 free trades. This helps me offset the cost of running the blog which is has so far been $1800 (quite cheap since I have done it all myself). I will never recommend a product or service that I don’t personally use myself, trust 100%, and will help you and I reach Financial Independence.

I have also gone back and forth about whether I should use Google adSense on this site – the banner advertisements that are placed by Google. Some have argued that it cheapens the site which I tend to agree with, and I also feel a bit hypocritical since a lot of the content on this site focuses around ‘unplugging from the media’ and disconnecting yourself from advertising. Either way, Google has paid me something like $100 to date, and I would like to at least extract my invested costs before switching it off. I hope this doesn’t detract from the user experience too much. If it really annoys you, please let me know in the comments. If enough people complain I will switch it off.

In terms of traffic, the blog has finally hit the milestone of 1,000 unique visitors each week. Google tells me that you guys on average read three of my articles, spending 4 minutes on each. Unfortunately 30% of the people instantly regret this decision and ‘bounce’ away from the site immediately. Some individual posts have had nearly 3,000 views in only a short time frame, which tells me those are more relevant to what people want to read.

Overall, I am quite pleased with these metrics as it tells me people are generally happy with the content and getting value out of it. This is reinforced by the hundreds of emails and inboxes I am receiving each month – which I do my best to reply to. As a hint, if you leave your question as a public comment on any of the posts / threads, I will reply to it much quicker, and we can all learn from the conversation.

I have also been posting daily on the CaptainFI social media accounts, Instagram and Facebook. If you use these platforms then please check it out and give me a like or follow to support me – I think we are nearly up to 2,000 on Instagram and 400 on Facebook. I post condensed versions of the articles you read here, as well as entertaining tidbits and educational info-graphics about personal finance, saving and investing, self sufficiency (including gardening, cooking, homebrewing and DIY), minimalism and aviation. If you like this site, you’ll love the feeds.

Saving rate

Despite being off work and driving half way across Australia, living on the farm has been pretty cheap. I am still paying rent of course for an empty apartment in Sydney. As a result, my savings rate has stayed fairly high and I came across the line with a figure of 90%. It certainly helps when you can siphon ULP out of the mill to fill up your cars petrol tank 🙂

Income

Side hustles this month from selling things wasn’t as good as previous months but still totaled over $2000, as I continued to declutter and downsize at home. I still have an estimated $5,000 worth of things to move on, and I am eager for these items (liabilities really) to be converted into productive assets (ETFs!).

I’m very lucky to have a couple of great neighbors who have been kind enough to take custodianship of my listings while I am interstate, and who have been wiring me the proceeds of the sales (minus a little something for them, of course!)

I finally got scammed on eBay – this time by a buyer who claims his parcel was never delivered. This is quite frustrating as I have the tracking details which show it was delivered – I suppose the item was stolen from their mailbox or they are lying. Either way its cost me $45, which in the grand scheme of things isn’t too much (like the $50 I was scammed out of on Gumtree the other month), but the principle of it is still annoying.

Given I have recouped nearly $20,000 from selling and downsizing this year, I’m not going to complain too hard over scams that don’t amount to even $100, or half a percent of the total. We can’t control what happens to us, but we can frame our response and take it as a learning opportunity – I have learned that it is super important not to buy useless shit, since it can be hard to sell or get rid of it when you realise you don’t need it. I have also learned there are some less fortunate than me in this country, who perhaps have to resort to compromising their morals to try and feed themselves

Website Portfolio income this month is around $60 in Google adSense income, and $20 that I have saved in brokerage thanks to the Selfwealth link that I shared.

I haven’t flipped anything this month because I spent most of it

Spending

Spending was very low this month, despite all the driving. Because of the COVID-19 quarantine restrictions and the need to self isolate, I haven’t left the farm and so haven’t spent a dollar since getting here. The only bills I have really had is the petrol, which wasn’t even that much since my wagon is pretty fuel efficient and the cost was on average under $1 per litre. And now that I am on the property I can just fill it up with ULP intended for farm machinery.

Whilst it doesn’t necessarily match my usual diet, I have been eating a lot of Kangaroo, Deer and Rabbit, stewed with winter vegetables and lots of rice. All of which has been taken on surrounding properties and cost the pricely sum of 80c per large animal (1 x .308 round), and 5c per rabbit (1 x .22 round).

I will make this clear that I don’t condone animal killing for the sake of killing. If you respect the animal, take its life quickly and cleanly and then efficiently and fully use everything, then I think its ok. I think this is a much happier life and less cruel end than the millions of unfortunate livestock that are shunted around in factory farms and feedlots.

Furthermore, the amount of food waste that comes out of most shops is insane. My Uncle sends my Cousins for the big trip into town to visit the local bakeries and supermarkets to pick up ‘expired’ food and produce to supplement the feed for the livestock on their hobby farm. 9 times out of 10 its literally bread that has been baked that same day, yet still is all headed for landfill. This usually goes to the sheep, but sometimes they can salvage some of the best stuff – I literally have half a dozen of ‘baked yesterday’ sourdough in the freezer that they brought over, and its perfectly fine!

The local forests also grow literally tonnes of mushrooms (which I am slowly coming around to), and there are various vegetables growing on the property – more out of neglect than anything. There is enough rhubarb to feed an army, since the Wallabies don’t seem to touch the stuff. Otherwise, I am working my way through what looks like a nuclear fallout shelter’s worth of tinned food my Father has stockpiled over the decades. Some cans are rusty or with no labels, so its a bit of a lucky dip what you end up getting.

FIRE Portfolio

The FIRE portfolio continues to grow, despite the market not really doing much, and I have been making regular contributions to it as soon as I get any amount of money. Since my income has dropped by more than 20% due to not flying, I was eligible for the superannuation withdrawal scheme.

I have decided to pull money out of my Super and since I am able to live extraordinarily cheaply and don’t necessarily need to spend it right now, I have decided to invest it into ETFs to boost my income now (prior to preservation age), but this also gives me the option to sell the ETFs if needed in an emergency. Some have suggested this goes against the spirit of the early withdrawal scheme, but I see it as prudent financial planning in uncertain times.

The FIRE Portfolio is currently sitting at $213,400 with the following breakdown

- Betashares A200 ETF: $178,479

- Milton LIC: $16,784

- Vanguard VTS (USA) ETF: $14,532

- Vanguard VEU (Total world ex USA) ETF: $3,547

Investing decisions

This month I invested into Vanguards all world ex US ETF – VEU, and also into Betashares Australian stock market ETF – A200. I am also continuing to invest into the build of investment property 1 and still have to make my mandatory superannuation contributions.

Real Estate

I put another $1000 into the build fund for IP1, and continue to pay the mortgage on the land and the construction and project fees. The level of paperwork on the project has been insane, and the banks are asking for triple the usual required information.

Thank goodness I have a great mortgage broker that I trust and who knows his shit, or else I would have probably walked away from the deal already and just funneled the money back into ETFs.

The total investment and cash reserved for the project is about $107,000 so far.

Retirement

Click here to see what my Transition to retirement financial planning process looks like

Net worth

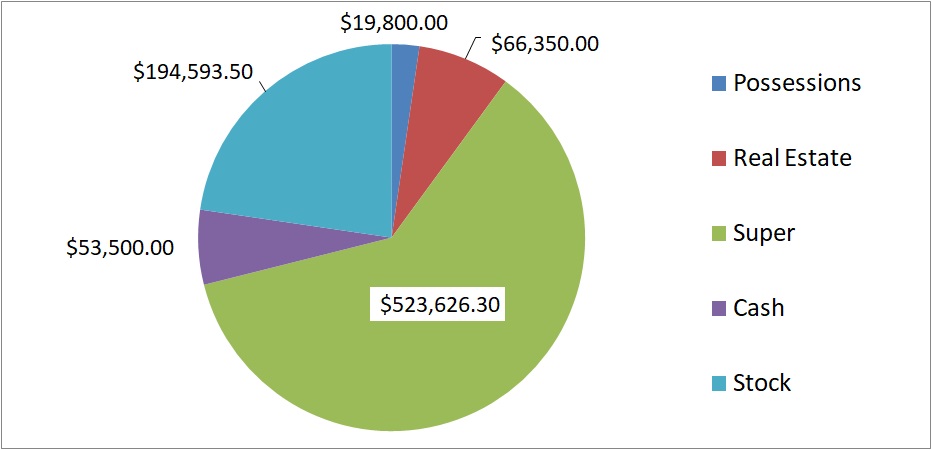

As per my current warpath I am continuing to de-clutter and minimize my lifestyle, selling things I don’t use on Gumtree and similar ‘online garage sale’ sites. I was pretty stoked to keep reducing my physical possessions, which now make up just under $15,000 or under 1.7% of my total net worth. The proceeds have been going straight into the brokerage account, and getting added to the fornightly investment decisions.

- Physical Possessions: $14,900

- Things for Sale: $5,400

- Real Estate equity: $107,000

- FIRE Portfolio: $213,400

- Cash: $3,600

- Superannuation: $514,350

- Total: $858,650

Overall through, I have only seen a gain of + $791 on the total net worth as the market hasn’t really been going anywhere and there is a lot of volatility and uncertainty still. There has been some reshuffling of assets, as cash has been moved across into the development funds and money has been moved out of super and into outside investments. I am hoping to receive around $5,000 from my tax return later this year later in October, but won’t count my chickens until they hatch.

Net Worth table

| Date | Net worth | Difference | Saving Rate | Notes | |

| Jul 19 | $578,900.00 | | 84% | Finally began tracking this like a proper adult. | |

| Aug 19 | $560,100.00 | -$18,800.00 (-3.2%) | 78% | Share market slight correction, Ok savings. | |

| Sep 19 | $584,744.88 | $24,644.88 | 72% | Share market rebound, savings rate not so good. | LINK |

| Oct 19 | $600,386.00 | $15,641.12 | 84% | Good saving this month. Normal salary, plus allowances, dividends from index funds, tax refund, eBay selling and was working abroad in asia where things are cheap. | LINK |

| Nov 19 | $612,917.21 | $12,531.21 | 76% | Falling short of my savings goal of 80%. Mostly domestic legs this month with higher costs. Also invested in hydroponics. | LINK |

| Dec 19 | $625,350.00 | $12,432.79 | 76% | Good savings of cash (for development) and investment, however higher spending due to Christmas period (Travel and Gifting). | LINK |

| Jan 20 | $865,212.00 | $239,862.00 | 55% | Super settlement was a HUGE boost to NW. $9K growth from stock market. Expensive month lots with lots of unexpected bills – weddings, travel, Booking flights, fines etc. | LINK |

| Feb 20 | $851,802.0 | -$16,592 (-1.9%) | 52% | Large increase in spending on myself this month, still managed to tuck away $5K to put into shares and property. Corona Virus market scare resulted in a correction and gave NW a small negative trend. Time in the market not Timing the market! | LINK |

| Mar 20 | $819, 354.6 | -$31,806.95 (-3.7%) | 80% | Another small step backwards in the NW due to the ‘market crash’ in full swing. FIRE Portfolio of ETF/LICs down about 15% this month, however due to high savings rate and structure of my superannuation annuity (guarantee – thank you unions!) the NW is only down 3.7%. Savings rate good at 80%, higher than usual income (with some slightly higher spending, too). Picking up shares on discount – this is the best outcome for someone in the accumulation phase with good income! | LINK |

| Apr 20 | $847,023 | +$27,668 | 85% | $11,000 in rebound of stock market capital prices alone (up 6%), plus first quarter dividends paid (heavily reduced due to banks withholding dividends). Great savings rate due to COVID-19 lock-down = no spend. Increased entrepreneurial efforts and selling down of physical possessions provided side hustle income. Two standard paychecks from flying activity; domestic day trips only so no allowances. All cash unfortunately had to go into the property development due to contract timing, I am chomping at the bit to buy some more index funds before they go back up in price too much – hence why I am selling most of my toys! | LINK |

| May 20 | $857,859 | +$10,836 | 92% | Some Great sales as I let go of my Super Sport Motorcycle, Some gym gear, expensive flying equipment and a few other various bits and bobs and invested this money. Flying still reduced, but increasing from April. The share market grew as I continued to make my fortnightly investments. I also wrote down the ‘value’ of some of my possessions (liabilities) such as my car, tools and furniture by around $10K to align them to market price (“tell him hes dreaming…!”). | LINK |

| June 20 | $858,650 | +$791 | Small Net Worth gain as I continue to declutter and simplify my life, despite being off work due to a family emergency. Share market not doing much. |

Get Financial Independence!

What did you think of the update? Let me know in the comments below!

Monthly question from the Captain

How do you calculate your saving rate? I calculate it as the total savings and investments, including super contributions, divided by the net influx into my bank account (total of my income and all side hustles)

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Firstly well done for what you’ve been able to achieve at a young age. All the best for your future plans. You’ve personally helped me by introducing SelfWealth to me (I used your referral link).

Onto my question, which I hope isn’t intrusive: Was that boost in superannuation from you double checking what was paid into your super and then finding out it was not the correct amounts? If so, can you suggest any tools or methods of doing this or how you went about this?

Or was it something unrelated to the above and therefore no learnings for other people leverage.

Cheers

Hi Saffa, what clued me on was that my salary hadn’t been paid correctly, and I knew that the super is paid as a percentage of what the salary should have been. So I just worked out the difference in salary and then using the percentage, the difference in super.