CaptainFI May Update

The end of May, that means the end of the Financial Year is approaching. Sigh. Time to think about my Tax – hopefully this means getting a tidy little tax return that can be put toward the ETF portfolio.

The good news is I have managed to simplify my tax accounting over the past few years for my stock portfolio using sharesight – I plan to simply use my free profile to print off my statement and hand this to my accountant to help get me my maximum return.

So I am pretty impressed with how well this little blog is going; I just checked the Google analytics , and it looks like each and every month there is now around 3,000 unique visitors to the site, and just shy of 10,000 page views. This is great feedback and tells me you guys are liking the content! I’m also posting nearly every day on Instagram, so check that out if you want to see some regular updates or get in touch.

I will endeavour to continue posting my tips and tricks on saving and documenting how I invest and the results. I’m pretty amazed that so many of you guys are interested to read the adventures of an average bloke trying to reach Financial Independence.

Like anything though, I tend to dive in with both of my left feet (!) so I am mindful of the time I am spending writing and on the social media; I am finding it a great outlet to help deal with my stress (of which there is no shortage of!) and learn more about my passion of becoming more self sufficient and investing. But I also need to be mindful of my own mental health and enjoy downtime and physical activity, and growing my garden, rather than getting obsessed with finance stuff.

Recently my mother told me a story of how I used to act when I was only a kid. I used to love bubble gum, and would do anything for a stick (or roll!) of hubba bubba chewing gum. Even now it gives me the nostalgic feels and I have to fight not to add it to my shopping bag! My sisters used to exploit this weakness, telling me there was a bubblegum tree – and if I only did their bidding then one day they would take me to it. In my innocence I often obliged, and found myself working for not only my, but their allowances too doing chores like sweeping, vacuuming and weeding the garden.

Often I would ask my dear mum for a stick of Hubba Bubba, but secretly she knew about my stash – the back of my sock draw usually had at least a dozen or so sticks that I had hidden away there, for future tough times.

I don’t know why but that story kind of made me a little sad when I was reminded by it, but also probably explains why I was so drawn into the FIRE crowd and became so excited about it. I think my Mum reminded me about it because she didn’t really understand my FIRE journey or why I was amassing such a portfolio of assets rather than just enjoying spending the money now. I wouldn’t consider myself a hoarder, but I possibly sit somewhere on the borderline – I like to be prepared and my shelves are always stocked with a few months worth of food – Just in case, right? Same goes for my emergency fund and ETFs – they are just in case 🙂

Another little interesting thing is I have started cycling to work on my $40 ‘gumtree special’ deadly-treddly (as my late grandfather used to call them). Just a bog standard mountain bike which I have added some safety lights to. After the first day (40km – 20km each way) I was a little sore, but it was very satisfying and I slept soundly. I am enjoying the exercise and changing up my commute so I can rely on my clown car less and less and even sell it one day, although secretly I want to trade my station-wagon for a Toyota Tarago minivan (8 seater) which will be perfect for when I have kids, and double as an inbuilt trailer for buying and selling furniture or other errands!

The balcony ‘Frugal Garden’ is growing strong and generating a lot of attention online, I received no less than 53 messages asking for more information so I recently posted a short video of it on Instagram. Then today I made it bigger, adding a Black Fig, Tahitian Lime and Navel Orange (both dwarf citrus) which I got on discount from Bunnings. This brings my total up to 73 pots of assorted sizes, taking up approx 8m by 1m deep strip along the fence railing.

At this rate my 100L reservoir is supplying now around 7L per day (each plant gets about 100ml over the 3 minute daily watering cycle) so it lasts about two weeks without being refilled. I am tempted to replace it with a 200L reservoir which will make it last a month! Having said that, this is only a ‘life support’ system to keep everything alive when I have to disappear for work, so when I am home I give it all a 10L watering can most days.

Saving rate

I have done a pretty good job this month on the old saving front. Although today I did splurge a bit at Bunnings – adding two dwarf citrus to the frugal garden (Tahitian Lime and Navel Orange) as well as a big ol’ bag of cow manure. Despite this ultimate luxury splurge (for future citrus fruity goodness) I have managed an incredible 92% Saving rate this month.

This was of course, attributed to some incredible selling this month as I downsize my life and adopt more minimalist philosophies for how I live my life. I sold my motorbike, some of my home gym equipment (which I plan to buy back at a massive discount after COVID-19 dies down by the way!) and some flying equipment (pilot helmet and other equipment) which I haven’t used in years!

Income

Two standard paychecks from my flying wage however due to the reduced flying roster I only received $600 worth of allowances for a couple of short hops, which just meant going straight from the aircraft to the hotel with no outside interaction due to COVID-19. They were long days anyway so I just went straight to sleep!

This month I enjoyed the benefits of my previous diligence in listing items; its pretty incredible and I was able to turn nearly $12,000 of my possessions back into cash, which went into both buying ETFs and funding the build of IP1! I am super happy and this has reduced my footprint of crap that I own that takes up space, and instead put it into investments which will pay me in the future. On this list of things sold included some Gym equipment, My Motorcycle and flight equipment I used for contracting (but hadn’t touched in years since my current employer supplies everything!)

I had to take a few risks i.e. sending items through the post before PayPal released the funds, but everything worked out fine in the end! This is a good example of how collective trust enables us to achieve more – you sometimes need to take a step of faith (but obviously protect yourself as much as possible) in order to conduct business deals and get things done.

Website Portfolio income is still zero as I have turned adds off to improve user experience, but I am thinking of switching these on provided they don’t piss anyone off too much just to help cover hosting costs. Due to affiliate links going in the background I saved about $30 in brokerage thanks to a SelfWealth referral, and I have just added a ShareSight referral code to the blog – since I have been using them for years anyway – lets see what happens!

The flip game was also strong, and I managed to sell a bunch of stuff for a profit, including a heap of plants which I grew from seed or propagated. I also have a sneaky habit of buying discounted plants from Bunnings, reviving them to full health and then selling them on using online classifieds.

If they aren’t discounted then I am shameless in haggling on the grounds of any slight imperfection in the plant! If the plant section attendant wont give you a discount, try your luck with the checkout chick or docket dude instead! They will often oblige, as I found out today receiving a 75% discount on my Tahitian Lime (which was perfect apart from a very minor infestation of leaf miner insect which is easily remedied with pruning and a small application of herbal pesticide)

Spending

Spending is well and truly reigned in from earlier this year, although I did splurge on some citrus trees and cow manure for the Frugal Garden today 🤣

I spent $40 or so on some bits and bobs for the car (oil and oil filter, air freshener etc) which I plan to service in the next month or so – approaching its 10,000km service although I haven’t been driving much lately so it hasn’t really been approaching this milestone as quick as I would expect. Actually speaking of spending and driving cars, I got very excited after reading a Mr Money Mustache article on electric bikes – I am looking at a few this weekend and considering spending up to $1000 on a second hand one!

I estimate that this would save me around 40kms of travel per work day, translating to about $6 in Petrol and another $6 in maintenance and other vehicle related costs. Its incredible to think that saving $12 a day means I would recoup the cost of the electric bike in as little as 84 days, or just over 4 months of commuting! All the while enjoying more fresh air, exercise (albeit assisted) and less risk of vehicle related injury. I also HATE traffic lights and traffic in general, and being on the bicycle gives me an insane amount of smugness as I zip past kilometers of backed up traffic on the bike lane!

I also sent some presents off through Australia Post to friends and family around the country, and hand delivered a few to some friends, as my many collective ‘Niece and Nephews’ reached milestones which needed celebrating! I love being able to give meaningful gifts, like books and learning toys (but I always avoid tacky plastic crap)

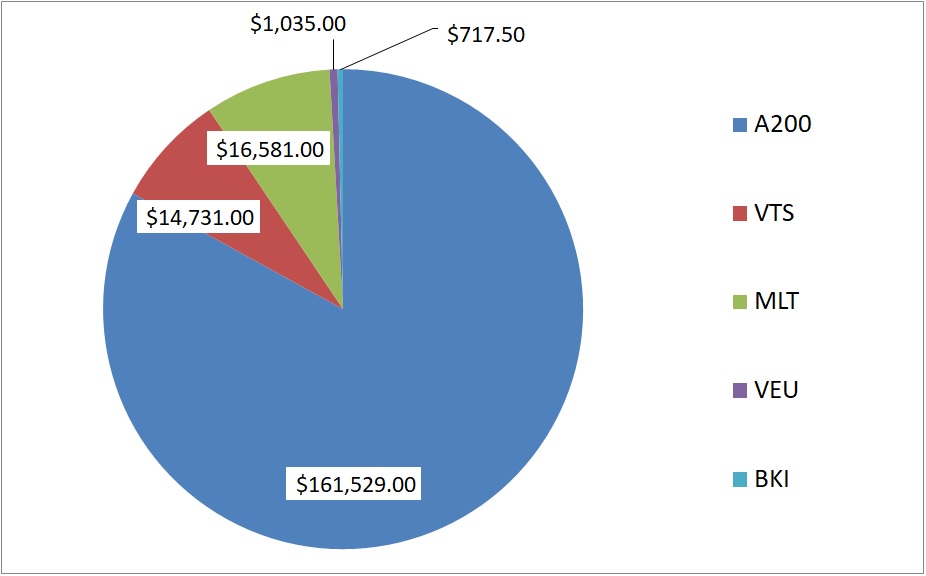

Get FIRE Portfolio

The FIRE portfolio is up 34% from the April update, which includes contributions I have made into the portfolio, but mostly due to the uptick in the market as it swings its way back from COVID-19 in true volatile fashion (it continues to wildly swing about).

It is now hovering close to the $200K mark again which is nice to see and I conservatively estimate would cover my cost of living for close to an 17 year draw down based on my FIRE number of $1700 per month and having it invested in mainly Aussie ETFs. Its good to know I have 17 years of F U money socked away without even having to touch the investment property

As I keep earning more over the next two years before I think I will hit my ‘FIRE’ number by age 30, which is around $300K of ETFs plus the investment property (and potentially even purchasing a second IP), which will fully support me through the 25 years of retirement phase 1 (early retirement through to super access at age 55). There is scope to continue work towards some kind of ‘Fat FIRE’ but we will cross that bridge when we come to it later.

Investing decisions

This month I directed my surplus funds into the build for IP1, as well as investing in Betashares A200 and Milton LIC. This is because the Aussie dollar was relatively low, and Milton has been trading below NAV – my ‘value drive bargain meter’ was directing me to pick up bargains and avoid buying anything too expensive!

I also noticed that the Australian Foundation Investment Company, AFI, and Argo investments, ARG, had been trading a significant premium for a while, so cashed in on the mania and sold mine at a tidy 7% premium or so, and directing all of this ‘profit’ into the A200 fund. Nicely, I sold at a slight loss which means I am not liable for any capital gains tax, and can actually carry forward this loss to offset any future capital gains from selling stock later on.

Property

I socked away about $4000 into the build fund for IP1 this month, which was annoying but a necessity. Money has been coming out for the interest on the loan for the land, plus construction site insurance, and our mortgage broker had really been dragging their heels on getting us the construction loan.

In the end we FIREd! them (LOL) and switched to a second mortgage broker who were able to secure a construction loan for us. It meant copping some claw back fee’s, but hey that is just the cost of business, and this will allow our project to continue sooner and overall will save us more money on the project.

Honestly, despite the property even being built, I would suggest that someone on the path to FIRE would probably be better off just aggressively investing in ETFs and LICs. I started this project chasing cash-on-cash returns (benefit of leverage), a mortgage offset account to stick my emergency fund in (rather than a piddly online savings account), and tax deductions against my relatively high income – but it has already been stressful and a pain in the arse with more paperwork than I have ever, ever had to do for any form of shares investing. Consider investing in property and developments very carefully before getting involved! I still don’t regret it yet, but we will see how it turns out.

Retirement

Click here to see what my Transition to retirement financial planning process looks like

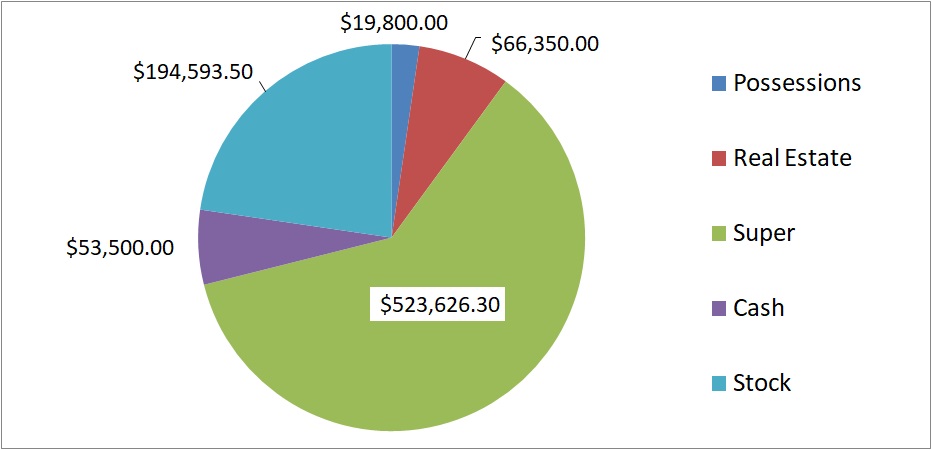

Net worth

I was pretty stoked to keep reducing my physical possessions this month, with them now making up only 2.3% of my net worth. Some people don’t like that I include these in here, but since I could sell any of these items I think its worth keeping them in here – it also sparks the debate about how much is appropriate to own and keeps me focused on minimising this slice of the pie and having as much of my Net Worth invested as possible.

The Cash stack has over $50,000 allocated in the IP1 build fund, so realistically the other $3,500 is made up of my $1000 emergency fund, $300 in my checking account (for ‘lumpy’ bills like car insurance and internet) and $2200 tied up in the bond for my apartment.

I also revalued my possessions by approx $10K to align them to market value, for example smashing down the crazy number I had in my head for my car from $15,000 down to the market average of $8,000 (the market doesn’t seem to value that it has about 30% of the mileage of the average model under its belt!), which explains for why my Net Worth chart didn’t really progress as high as it might of based on my portfolio growth, income and all the money I got from selling down my possessions.

Net Worth table

| Date | Net worth | Difference | Saving Rate | Notes | |

| Jul 19 | $578,900.00 | | 84% | Finally began tracking this like a proper adult. | |

| Aug 19 | $560,100.00 | -$18,800.00 (-3.2%) | 78% | Share market slight correction, Ok savings. | |

| Sep 19 | $584,744.88 | $24,644.88 | 72% | Share market rebound, savings rate not so good. | LINK |

| Oct 19 | $600,386.00 | $15,641.12 | 84% | Good saving this month. Normal salary, plus allowances, dividends from index funds, tax refund, eBay selling and was working abroad in asia where things are cheap. | LINK |

| Nov 19 | $612,917.21 | $12,531.21 | 76% | Falling short of my savings goal of 80%. Mostly domestic legs this month with higher costs. Also invested in hydroponics. | LINK |

| Dec 19 | $625,350.00 | $12,432.79 | 76% | Good savings of cash (for development) and investment, however higher spending due to Christmas period (Travel and Gifting). | LINK |

| Jan 20 | $865,212.00 | $239,862.00 | 55% | Super settlement was a HUGE boost to NW. $9K growth from stock market. Expensive month lots with lots of unexpected bills – weddings, travel, Booking flights, fines etc. | LINK |

| Feb 20 | $851,802.0 | -$16,592 (-1.9%) | 52% | Large increase in spending on myself this month, still managed to tuck away $5K to put into shares and property. Corona Virus market scare resulted in a correction and gave NW a small negative trend. Time in the market not Timing the market! | LINK |

| Mar 20 | $819, 354.6 | -$31,806.95 (-3.7%) | 80% | Another small step backwards in the NW due to the ‘market crash’ in full swing. FIRE Portfolio of ETF/LICs down about 15% this month, however due to high savings rate and structure of my superannuation annuity (guarantee – thank you unions!) the NW is only down 3.7%. Savings rate good at 80%, higher than usual income (with some slightly higher spending, too). Picking up shares on discount – this is the best outcome for someone in the accumulation phase with good income! | LINK |

| Apr 20 | $847,023 | +$27,668 | 85% | $11,000 in rebound of stock market capital prices alone (up 6%), plus first quarter dividends paid (heavily reduced due to banks withholding dividends). Great savings rate due to COVID-19 lock-down = no spend. Increased entrepreneurial efforts and selling down of physical possessions provided side hustle income. Two standard paychecks from flying activity; domestic day trips only so no allowances. All cash unfortunately had to go into the property development due to contract timing, I am chomping at the bit to buy some more index funds before they go back up in price too much – hence why I am selling most of my toys! | |

| May 20 | $857,859 | +$10,836 | 92% | Some Great sales as I let go of my Super Sport Motorcycle, Some gym gear, expensive flying equipment and a few other various bits and bobs and invested this money. Flying still reduced, but increasing from April. The share market grew as I continued to make my fortnightly investments. I also wrote down the ‘value’ of some of my possessions (liabilities) such as my car, tools and furniture by around $10K to align them to market price (“tell him hes dreaming…!”). |

Get Financial Independence!

What did you think of the update? Let me know in the comments below!

Monthly question from the Captain

I have a question I want to ask everyone regarding portfolio construction. Do you invest in both ETFs or LICs? Or just one? I would love to hear your opinion on whether you go for LICs for dividend smoothing tax efficiency, or whether you go for the raw power and simplicity of ETFs. Which one do you think is better for Financial Independence? I value simplicity, and so have been thinking of adopting a purely ETF based approach with the A200/VTS/VEU split, but can still see the value of buying the LICs at a discount!

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Nice work, I finally started adulting at end of Aug 2019 and started tracking everything also, certainly does wonders to see whats going where

Great start Baz, keeping track of your net worth can show you exactly where your money is going and is a great way to ensure your on track to reach FI as soon as you can

I am really enjoying your blog posts as I am sure you can tell by all my comments. When you mention a drawdown rate of 7% up to the age of 55, do you mean you will sell shares once a year for this amount? I am still unclear how to access the money built up before our access to super at 60, thank you 🙂

Hi Mel, yep that’s right, I get about 3 to 4% in dividends already, and so plan to sell small parcels of shares as required to make up the difference in order to keep my cash account set at around one to two years living expenses. I haven’t fully ‘tweaked’ this plan for the retirement phase yet since its still a year or so away. I also get access to an annuity through my super from age 55 onwards, so this is why its a little earlier than some other people. cheers

very well explained, I’m off to do some calculations, thank you