June and July were both pretty big months for me, but now I am back in Sydney and ready to return to work. With the ‘calmer’ pace over the past while as I spent time with my family, I have been thinking more about my short term (1 year plan) as well as my medium (5 year) and long term plans (10 years), re-evaluating them and starting to put things in motion to ensure I reach them. I think this has really helped me to feel less anxious about what has been going on in my life (and the world) lately and given me a bit of ‘inner calm’ to know that my current way of life won’t be forever. My 5 year plan involves buying a block of land in the mountains / hills, and my 10 year plan involves lots of children!

July update

So July marks a whole year of tracking my Net Worth,10 months of sharing this data openly and freely online, and 6 months on the CaptainFI blog (I previously started using a different blog before I started CaptainFI). Hopefully you can get some good lessons out of going back through them and seeing how my strategy has evolved and how my investments have done.

One of the things I have found myself checking out heaps of when I was at home was YouTube Videos about Tiny Homes and Camper Vans. I know this might sound super lame, but there is this whole secret society of ‘stealthcampers’ out there and a genre called ‘Van lifers’ which are people that literally live in unmarked white vans and drive around the country (and the world)… although not through any borders at the moment due to COVID checkpoints.

They usually have everything they need in a large Ford Transit or Mercedes Sprinter Van to sustain themselves pretty much indefinitely (with supply runs for food, water and fuel of course). They even have heated showers and toilets! I really like the idea about being sustainable using solar panels and an AGM or lithium battery bank, and you can always take a backup bottle of propane which can be used to cook or heat water if your running low on electricity. Its basically a caravan all squeezed into a van, making use of the ‘tiny home’ efficiency principles. You can then go and free-camp wherever you like, and when you get sick of it you just drive away!

I am so interested in this Van Life concept that I am building my own! Yep, a fun project for something to do when I FIRE and no longer fly full time. It fits well with my principles of minimalism and efficiency, and I am super excited to get my base van and start decking it out. Eventually, I plan to live in this Van as I travel Australia looking for a big patch of land (4+ acres) that I want to buy and then set up my permaculture farm. Lots of study, research and planning will have to happen before I buy a van, but its looking like I will get a second hand extended wheel base Mercedes Sprinter or similar, and then design and install all the cabinetry, wiring and plumbing myself. If this is something you think is interesting, then standby because I will be documenting it all in a dedicated separate blog.

The reason why I am going to start a second blog on the Camper Van is because I don’t want to detract from the core topic of Captain FI; which is Financial Independence. Whilst what you do with FIRE is very individual to each person, the Earning, Saving and Investing part is ubiquitous to everyone. So I am going to keep the focus of this blog specifically onto the core topic of Financial Independence and those three key areas, with some kick-ass book and product reviews, and of course my net worth updates. Similarly, I found myself diverging into the Parenting and Gardening/Permaculture space quite a bit, which I have tried to link into FIRE but find might be getting a little too off topic. So watch this space, and if/when these blogs get released and there is some good stuff on them then I will be sure to put a link to them for those that are interested.

Unfortunately whilst on the road I had some unscheduled servicing required – one of my rear wheel bearings on the car packed in, so I opted to replace both rear bearings. I took the opportunity to get another oil and filter change since I had racked up a lot of driving on outback dusty roads, as well as to replace the front brake pads (I had the pads in the glovebox for ages). This added up to just shy of $1000, which was frustrating because I could have easily done it all for under $300 had I been home with my tools. But that is just the price of car ownership, and it was awesome I was able even do the trip to start with!

End of financial year tax return is still outstanding…

Its now well and truly the end of the financial year so I can start thinking about doing my tax return... almost. Because I had invested in some LICs, they can take a while to sort out their tax paperwork. This usually means I have to wait till October to actually submit my paperwork to the ATO.

Because I use Sharesight I can ditch the excel spreadsheet and just print off their completely free report for all the shares stuff.

All I did was then sub in my work related tax deductions, gathered all my payslips and payment summaries for other taxable things (like bank account interest, RateSetter and affiliate income) and then left it aside in a folder and will re attack it when I have the final paperwork from the shares registries

When the tax statements for the ETFs and LICs in my portfolio are all finalised (unfortunately around October-ish), I will reprint the Sharesight tax summary and then take it down to my accountant, pay $300 and walk away with an estimated $5,000 tax return.

Saving rate

My saving rate was a pretty paltry 68% this month. I’m still pretty happy its in the positive figures though!

Income

Income from this month was reduced heavily as I was on leave and not earning my usual pay and allowances. Thankfully though, I got just under $1250 in Dividends from the FIRE portfolio dropped into the account which was great, and I also continued to sell things to de-clutter my apartment; everything I made went into the investments and replenishing my emergency fund.

Spending

Spending continued to be pretty low, but I had to fork out for some expensive car repairs (I needed both rear wheel bearings replaced and unfortunately did not have any of my tools with me to do the job) , I spent a lot on Petrol for all the driving, and the miscellaneous costs involved with DIY renovations to both my Dads Farm and my Mums property.

Investing decisions

This month I invested $6253 between Shares, Property and Peer to Peer lending.

$3253 went into Milton Corporation LIC (ASX:MLT) which I bought through SelfWealth, since it was on a downswing during my purchase day (down by 1% or so and the ASX was up half a percent) which meant I was buying it at a discount. The metrics I got said I bought at a 1.5% discount, which seemed good enough. I know I need to focus my efforts overseas to diversify, particularly I need to buy VEU, but I can’t help but be tempted by the dividend yield boost that franked Australian shares produce – allowing me to FIRE sooner. I know there is a concentration risk into the Aussie Market, but I am happy to accept this risk for the increased dividend yield. I also believe we (Australia) will swing back stronger than other nations from COVID-19, so I am concentrating my investments inside of Australia.

Property

I also transferred an extra $2000 into the property build fund as a buffer, since those nasty mortgage repayments are about to really start adding up now that the construction loan has been approved and I will have to pay the mortgage on that and the seperate loan for the land.

P2P lending

I finally bit the bullet and invested $1001 into RateSetter’s Peer to Peer lending system! I had so many questions about this so just thought I would dip a toe and see what happens. Standby for a full article detailing my experiences!

The FIRE portfolio continues to grow, as I slowly continue to feed money into it. The portfolio has recovered a little from the COVID drop, and provided a small amount of dividends which I have reinvested in the portfolio. I have transitioned away from the Excel Spreadsheet and into using Sharesight for my portfolio metrics here which a lot of you had been asking for, so here it is no bull! You can use this link to sign up and get 4 months for free on a premium subscription for Sharesight, but be sure to check out my review of them first here – Captain FI reviews Sharesight.

Investment Property

We have progress! The duplex build is finally starting to go ahead, with the bank now approving construction to start (…again?!). The final documents were signed with the mortgage broker a few nights ago, and I am the proud owner of $370,000 in mortgage debt, which thankfully is an interest only loan at a ripper rate of 3% so the fortnightly repayments are only just over $400. It is still over $10K a year just in interest alone so its scary stuff when its not making any money back yet! The bank property valuation estimate should come back soon, which will be a good place to start to figure out how much equity I have etc, but it was designed around being a completion value of $570K before COVID-19 affected property prices which really spooked the bank and stalled our progress. This means on paper at the moment I have about a 35% equity stake in my unit, which I have put about 20% of my cash into, and the other 15% is ‘manufactured equity’ – or about $85K worth.

To date, I have invested $109,000 of cash into the property project and I am estimating something like 6 months until the slab is poured, and then hopefully 12 months from pour to tenancy. It is going to hurt not getting rent and having to pay the mortgage for this whole period, but I have to remember about the ‘manufactured equity’ we are making from the build which more than offsets this period of no rent, since the numbers all added up when we started the project. The interest repayments account for about $20K during the build, so it still came out about $65K ahead to go ahead and do the build, provided our current valuation remains the same. Unfortunately, the prices will likely drop by around 10% or more, meaning the manufactured equity might be closer to only $10K!

In terms of cash-on-cash return expectations, its still ok, since I would have invested around $110K for 18 months and made $10K; a 9% return over 1.5 years so about 5.97% annualised rate of return, with some sweet tax depreciation starting to be able to be claimed. But all these numbers really mean nothing until the property is built and properly revalued, and even then the valuation doesn’t really mean that much until IP1 gets sold (unless I am allowed to do a cash out refinance to take equity out of the property as a downpayment for IP2).

I will feel much more comfortable once the slab is poured and we can see the frame going up, but for now its just a matter of continuing to throw money into the hole. At least during the build the construction loan is interest only, but I am paying P+I on the land portion. Once the build is finalised, we will do the deed of partition (split the jointly owned title into one title for each dwelling) and I will refinance the loan against my dwelling to consolidate it, suck out the maximum equity I can, and set it up properly for with an offset to hold at least $5000 of cash to act as a buffer / emergency fund.

The Rental cash flow on the property is fairly ‘low’ – its basically slightly cash flow positive so it pays for itself with some tax depreciation benefits. Why I did it is for the cash-on-cash rental yield, Some capital growth (conservative estimates), the depreciation schedule whilst I am a ‘high’ earner, and finally manufactured equity of the deal. Its also a hedge against inflation, since inflation erodes the value of the loan over time – I take the loan out in 2020 dollars, and pay it back in 2030 dollars, which are much larger or have less value. This is in line with my financial independence strategy to basically max out my serviceability on cash flow positive properties and then invest the surplus into index funds.

After the unit is built I will see a financial adviser to go through the numbers and work out if its better to keep it, or sell it and use the equity as a down-payment on a couple of regional rental properties. I’m thinking I will probably keep it for 10 years or more though, and suck all of the juicy depreciation schedule out of it since it wont cost me a thing (except opportunity cost, but when I refinance I will take as much out as possible)

I am still actively looking for a second site potentially in Adelaide or Brisbane to conduct a second duplex build or subdivide so if any one has any ideas or is interested in a collaboration, then get in touch and I can organise my property development manager to have a chat.

Retirement

Click here to see what my Transition to retirement financial planning process looks like

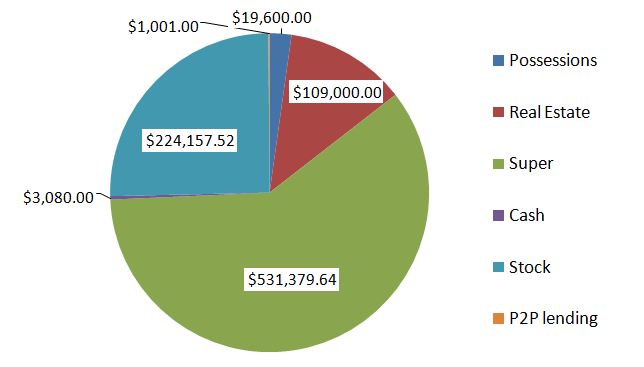

Net worth

The Net Worth pie chart looks a little different now as I have pushed all of the cash into the property development with an estimated $109K of equity in the deal (standby for a more accurate description over the coming months of the equity position as we get a detailed bank valuation and the loans get paid down).

I have also included the *very small* Peer to Peer lending slice, which kind of acts like a bond (technically you would probably call it a CCC rated Junk Bond I guess). At the moment RateSetter are giving me 3.2% which is better than the emergency fund I have in a savings account (2% or so) but really I just wanted to learn more about P2P lending and whether the longer term loans could provide an attractive source of interest / yield. It’s not a lot of money, but was enough to qualify for the bonus $100 for signing up thanks to a friends link (so that will boost the return for the first month!)

The possessions also include about $5000 worth of things I am trying to sell, which the cash will help me on my path to my long term plan. Some of the things I might buy back in the future when I need them again, but for now they just either don’t get used, take up space or are going to be too expensive or hard to store.

At the end of the day, this NW tracking thing is all a bit of a wank, or an ego stroke. What really matters is the dividend yield or the income all of the assets generate, because really that is a measure of my passive income or lifestyle in FIRE. Because of the unique way I have my finances structured to be optimised for an Australian investor with a significant amount invested in Superannuation, the NW number isn’t really all that reflective of my ability to FIRE. What really matters here is the chunk that is outside of super, or more specifically the chunk labelled ‘Stock’, because that is what is going to be giving me the majority of my income to live off. The Websites also provide a small income through Ad-sense and Affiliate income, and I have plans eventually to publish a book through the blog which may or may not make any money. Fingers crossed?!

Net Worth table

| Date | Net worth | Difference | Saving Rate | Notes | |

| Jul 19 | $578,900.00 | | 84% | Finally began tracking this like a proper adult. | |

| Aug 19 | $560,100.00 | -$18,800.00 (-3.2%) | 78% | Share market slight correction, Ok savings. | |

| Sep 19 | $584,744.88 | $24,644.88 | 72% | Share market rebound, savings rate not so good. | LINK |

| Oct 19 | $600,386.00 | $15,641.12 | 84% | Good saving this month. Normal salary, plus allowances, dividends from index funds, tax refund, eBay selling and was working abroad in asia where things are cheap. | LINK |

| Nov 19 | $612,917.21 | $12,531.21 | 76% | Falling short of my savings goal of 80%. Mostly domestic legs this month with higher costs. Also invested in hydroponics. | LINK |

| Dec 19 | $625,350.00 | $12,432.79 | 76% | Good savings of cash (for development) and investment, however higher spending due to Christmas period (Travel and Gifting). | LINK |

| Jan 20 | $865,212.00 | $239,862.00 | 55% | Super settlement was a HUGE boost to NW. $9K growth from stock market. Expensive month lots with lots of unexpected bills – weddings, travel, Booking flights, fines etc. | LINK |

| Feb 20 | $851,802.0 | -$16,592 (-1.9%) | 52% | Large increase in spending on myself this month, still managed to tuck away $5K to put into shares and property. Corona Virus market scare resulted in a correction and gave NW a small negative trend. Time in the market not Timing the market! | LINK |

| Mar 20 | $819, 354.6 | -$31,806.95 (-3.7%) | 80% | Another small step backwards in the NW due to the ‘corona crash’ in full swing. FIRE Portfolio of ETF/LICs down about 15% this month, however due to high savings rate and structure of my superannuation annuity the NW is only down 3.7%. Savings rate good at 80%, higher than usual income (with some slightly higher spending, too). Picking up shares on discount – this is the best outcome for someone in the accumulation phase with good income! | LINK |

| Apr 20 | $847,023 | +$27,668 | 85% | $11,000 in rebound of stock market capital prices alone (up 6%), plus first quarter dividends paid (heavily reduced due to banks withholding dividends). Great savings rate due to COVID-19 lock-down = no spend. Increased entrepreneurial efforts and selling down of physical possessions provided side hustle income. Two standard paychecks from flying activity; domestic day trips only so no allowances. All cash unfortunately had to go into the property development due to contract timing, I am chomping at the bit to buy some more index funds before they go back up in price too much – hence why I am selling most of my toys! | LINK |

| May 20 | $857,859 | +$10,836 | 92% | Some Great sales as I let go of my Super Sport Motorcycle, Some gym gear, expensive flying equipment and a few other various bits and bobs and invested this money. Flying still reduced, but increasing from April. The share market grew as I continued to make my fortnightly investments. I also wrote down the ‘value’ of some of my possessions (liabilities) such as my car, tools and furniture by around $10K to align them to market price (“tell him hes dreaming…!”). | LINK |

| June 20 | $858,650 | +$791 | 90% | Small Net Worth gain as I continue to declutter and simplify my life, despite being off work due to a family emergency. Share market not doing much. | LINK |

| July 20 | $888,218 | +$29,568 | 68% | Majority gain due to share market going back up, low spending due to being on the family farm and at home because of lock down. |

Get Financial Independence!

What did you think of the update? Let me know in the comments below!

Monthly question from the Captain

Have you ever tried Matched Betting? I have been reading about it lately and would love to hear if anyone has had any success stories!

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Its great to see someone finally put their money where their mouth is. I have always taken FIRE blogs with a pinch of salt as there are no stats to back them up. However, in the absence of a chart, can you expand on the percentage of your current net worth that came from savings and how much from invested growth?

I would like to better understand how the whole index LIC investment thing can actually fund retirement.

Hey Chris, thanks for taking time to comment mate and thats a great question. From the top of my head I don’t really know, but I would say if I am honest a lot of it just came from savings because I have only been ‘hardcore’ into FIRE for 3 years and then sort of saving and investing for about 2 years prior to that, so 5 years isnt really heaps of time for compounding. Im expecting the compounding gains to start to accelerate over the next few years (fingers crossed). For the LIC / ETF retirement stuff your on the right path mate just keep doing some digging around on the site – head to the ‘all articles’ page and start churning your way through the list. Also check out http://www.mrmoneymustache.com