I’m sorry Sydney, its not you – its me…. …Wait…. No. Its you. Its definitely you. Its always been you! haha Byeeeeeee

As you read this I am making my way across the country as I leave Sydney and New South Wales where I have made my home for the past 4 years, and am returning back to a slower life in South Australia. Of course this is the long awaited move – I am no longer working flying full time in Sydney, and am heading home to be with family during this difficult little while and exploring potentially doing some part time engineering work as I try to ‘de-tangle’ my brain from the high stress work environment I have come from.

I am blown away by the growth of my assets this month – a slight correction with the crypto but strong growth with the website portfolio as I secured more deals and ongoing revenue, general growth of the share market and my superannuation annuity as I reached another salary increment. This will be a brief update with just the facts, so check out the pod (dropping Friday) for more info.

Monthly Question from the Captain;

Probably the biggest thing I am trying to suss out this month and probably over the next is the value of CHESS sponsorship and using a HIN over more modern custodial based arrangements. I don’t claim to be an expert on either – so if you have any knowledge or opinions on either please let me know in the comments or on the socials.

CaptainFI is reader supported, which means we may be paid when you visit links to partner or featured sites

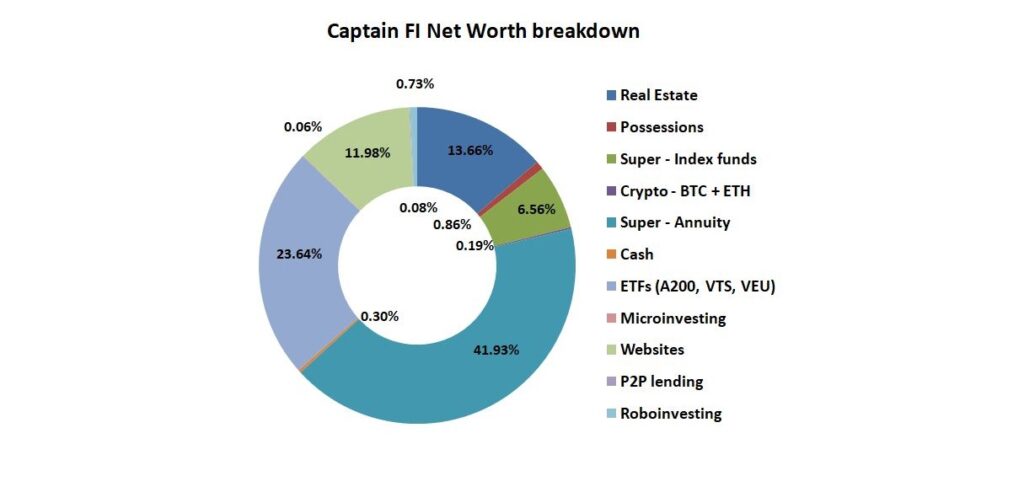

CaptainFI Total Net Worth

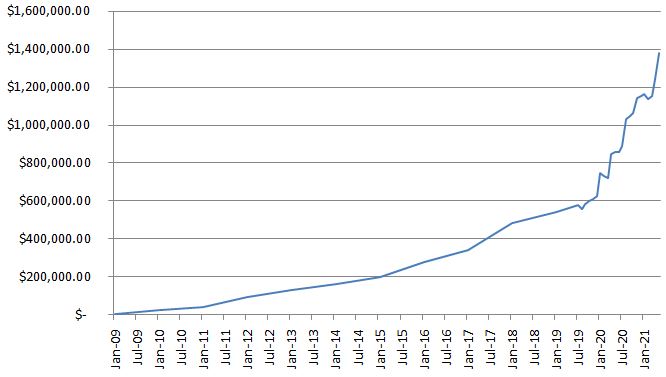

CaptainFI Financial progression

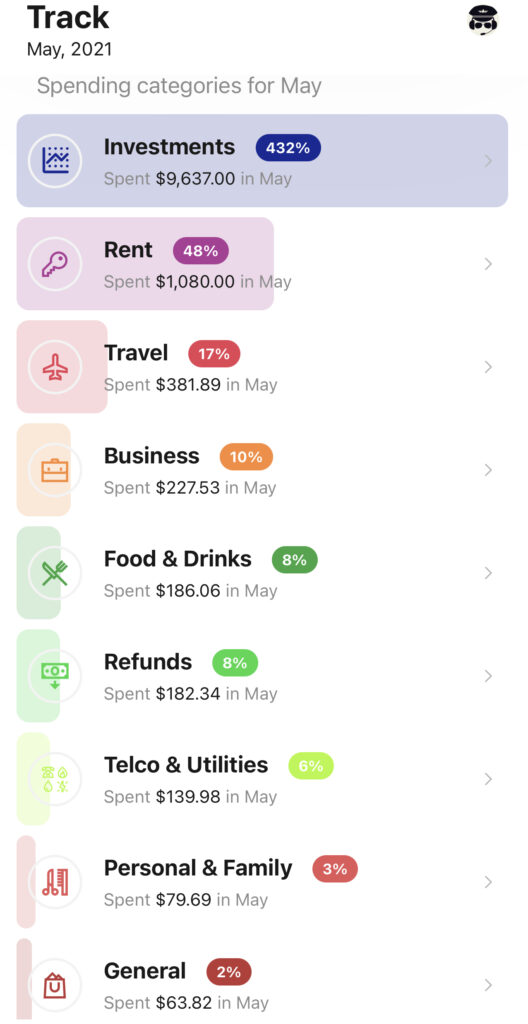

Captain FI Monthly Spending

I recently opened up my bank account for a weekly Money diary interview on Savings.com.au which was a bit confronting but I’m totally glad I did so!

I haven’t been as transparent with my spending over the last bunch of net worth updates because to be honest, I kinda wanted the privacy and I felt a little attacked when people called me out on some ‘non-FI’ spending I did. But everyone had been asking me how much I spent and how I tracked my expenses. So here we go….

I’ve partnered with WeMoney for this segment to show you how I have been tracking my spending lately – so yes, I am working with them (Hellooooo Financial Independence back up since I stopping flying) but notwithstanding our partnership it’s a really nifty app. I’ll also be posting regularly over in the WeMoney Community feature, so check in on the app if you want to see some unique Financial Independence content.

Overall, the app did a very good job of tracking my monthly expenses. I took this screenshot today (31st of May) and there were still a couple of things missing (rent payment and another investment transfer) but I wasn’t bothered about chasing them up because I more just cared about the actual little expenses. I then just flick through these tabs to suss out where I have spent my money which is an important reflection. May was also a spendy month so no judgement please haha.

I have done an in depth review of WeMoney and how it works so be sure to check that out if you want to learn more about how you can improve your finances for free by using WeMoney.

Captain FI Investments

My investments are now split between seven main investment ‘areas’. I decided to start reporting on the progression and performance of each of my investments separately so we can find the best way to Financial Independence once and for all.

- Financial Independence ETF Portfolio (Global, US and AUS Index fund ETFs)

- Hands-free Automated Investing (Roboadvisors)

- Cryptocurrency

- Microinvesting

- Real Estate

- Peer to Peer lending

- Website Portfolio (Online businesses)

For the record, my inner bias is that I think the first and the last will perform the best – but we will see over time how this unfolds. I don’t like over-thinking the investment stuff too much – so I plan to just provide a brief update each month on each investment class and what it is doing.

Note I am also considering getting some Gold and Silver ETFs

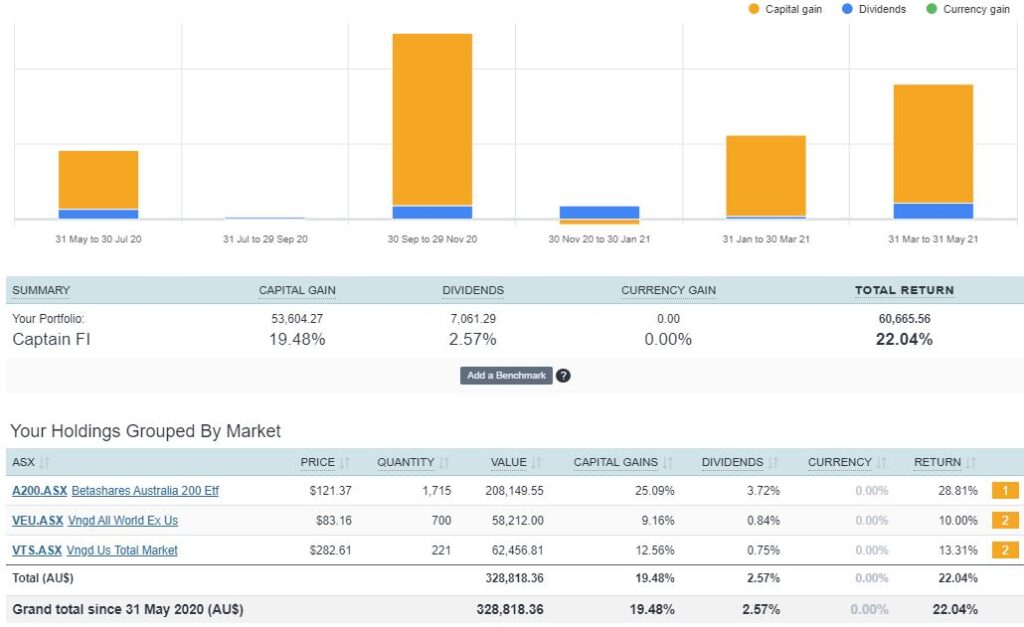

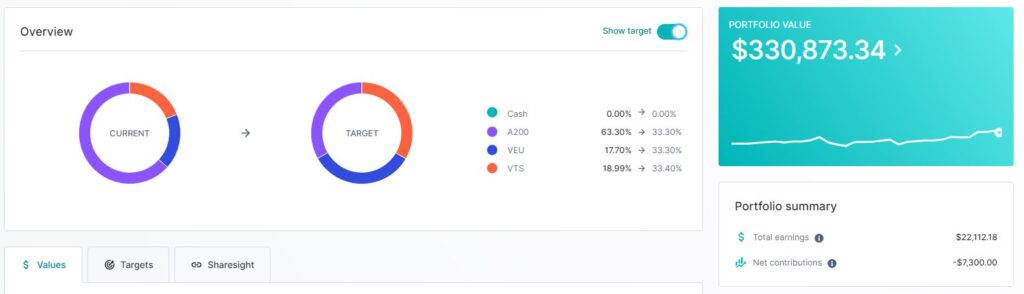

Financial Independence ETF Portfolio

My Financial Independence ETF Portfolio is a simple, low-fee passive portfolio which is split between three index tracking Exchanged Traded Index Funds (ETFs):

- I now have this portfolio fully automated through Pearler which has been a huge gamechanger for me and a massive weight off my mind

- I track my share portfolio using Sharesight, which means my accounting is also completely hands free using the Pearler API plugin.

- This means I pretty much only need to log in to confirm all the trades and dividends over the year when needed for my tax return, however I also choose to log in each month to produce these monthly updates for you guys.

- I have had questions about the tax efficiency of VTS and VEU due to the double tax or withholding tax drag because they are US domiciled funds. This is something I will be looking into. My limited understanding at the moment is that this tax drag creates an ‘effective MER’ of closer to 0.5% which might mean there may be a lower cost alternative that is better than these ETFs – something I will be investigating.

Portfolio vs Target – Pearler chart

I am still heavy on Australian shares through the A200 fund because I was chasing the franked dividend yields for a baseline level of income stability for Financial Independence. I am now working to balance this home bias concentration risk by an automated purchasing of VTS and VEU through Pearler.

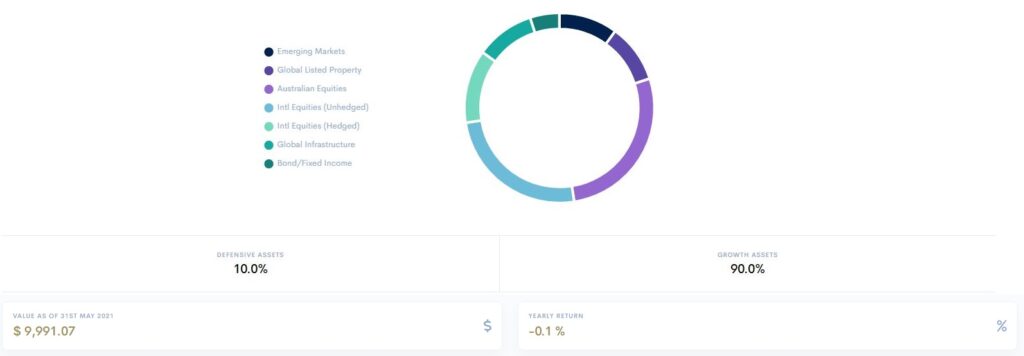

Hands-free Automated Investing Portfolio

The Hands-free Automated Investing Portfolio is a combination of the two largest Online investment advisors in Australia – Stockspot and SixPark. I think they are both pretty damn good, and to stay accountable I wanted to hedge my bets with an investment in both. This way I can analyse the performance of each against one another – comparing the results of asset allocation, and Chris Brycki’s choice to diversify with gold, against Pat Garratts’ choice to diversify with property and infrastructure.

Stockspot

After a successful trial with the Stockspot roboadvisor platform where they allocated me the Topaz portfolio (which is their most aggressive portfolio), I have increased the balance to $10K and am letting it compound away.

If you want to learn more about Stockspot, check out the dedicated review I did on Stockspot – which I will be keeping updated with all the lessons from my personal use trial.

SixPark

This was a new investment for the month, mirroring the investment I made into Stockspot. This way I can compare the performance of the two.

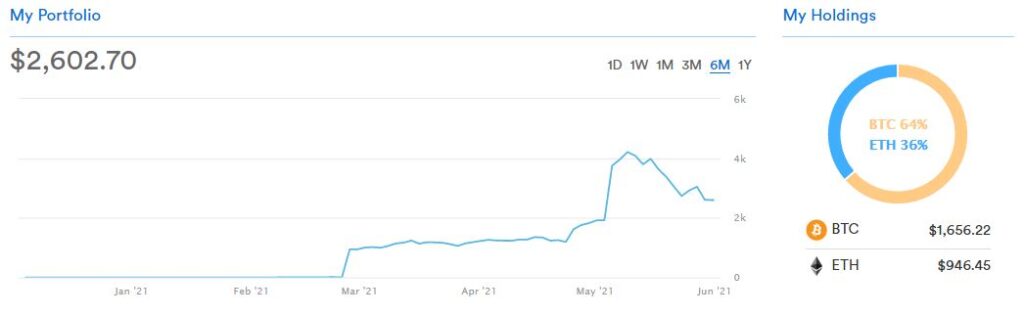

Cryptocurrency Portfolio

Crypto had a bit of a roller coaster recently – I added $2,000 and it seemed to go down pretty much right after, so that was a bit annoying. Oh well – glad I’m diversified and these movements have brought me back to my target split of 2:1 BTC:ETH.

I did a podcast episode on Bitcoin with Stephan Livera if you are interested to learn more about it, but I’ve since been bombarded with emails telling me he is a ‘Bitcoin Maxi’ (which is kind of like the fundamental Christian evangelists of the crypto world) and I need to learn more about alt-coins. I thought he sounded pretty knowledgeable though and everything he said made sense.

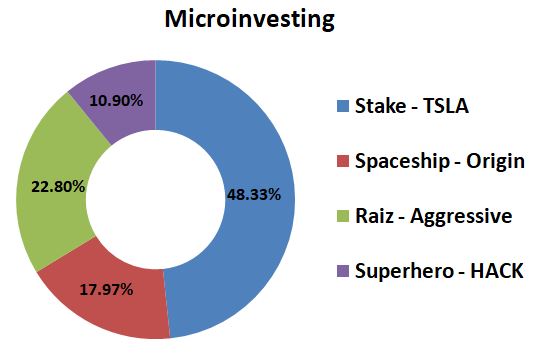

Micro-investing Portfolio

I have been playing with microinvesting platforms mainly just as research for the blog, because I want to see how they all stack up against each other. Its not strictly speaking a true comparison though because they don’t hold the same investments at all. Really it is just a bit of fun stuffing around with them, and gives me some more background knowledge for when people ask me about how to get started investing using microinvesting platforms.

Stake Invest

I just decided to go all in on Tesla through Stake, and it has seemed to go pretty good. Went down a bunch but thankfully started to recover. Best not to look at it.

Raiz Invest

Raiz aggressive portfolio – good split of ETFs, and a cheap option for small-ish balances at only $3.50 per month. To be honest the fee’s are more than my investment return, but any round up and the occasional affiliate click sign up bonus usually more than covers any fees.

Superhero Trading

I didn’t do any trading on Superhero this month, just left my HACK shares to do their thing. I might have a look at some ethical ETFs on superhero over the next few months

Spaceship Voyager Invest

Spaceship Origin portfolio: Top 100 Global Blue chip ETF. This seems to be going alright but If I am honest, for a speculative punt I should have probably gone for the Universe portfolio which seems to be having insanely high gains – I am hoping the origin portfolio might be more stable.

Plenti P2P lending

Plenti Peer to Peer lending account. I have it all set to auto reinvest and over time it should slowly grow, but it is good to know that I can either switch the auto invest off and have that drop into my account within a month, or I can just forfeit monthly interest and do an early withdrawal of whatever is on loan in case I ever need to quickly access the cash.

Plenti got a facelift this month, so it looks more aesthetically pleasing. I was also pleased to see the balance grow somewhat, and may have to raid this cash when I get to Adelaide to stump up for a new apartment bond.

Investment property

I currently have a $370K IO mortgage attached to it, which means the equity position is roughly $190K or 34%, or put another way the LVR is 66% which is comfortably below the 80% figure and will ensure I can refinance to a much lower rate when tenanted (construction loan is 4% interest only and I am trying to get something closer to 2% when finished). I feel comfortable with this level of debt as I could liquidate shares and pay it off, or alternatively if I worked hard I know I could pay it off within a few years.

Rental appraisals from the broker and builder are IVO $550 per week but of course I don’t trust that. The bank seems happy to enough to lend against that. Scouting the neighbourhood shows 80’s built freestanding 4bdr homes going for $500 per week, and newer 4bdr homes renting for $700 per week.

Now mine is just a 3 bdr duplex, but it is brand new with luxury finishing so I am assuming the real rental return will be at worst case at least $500 per week or $2000 per month. An interest only 30 year loan at 2.2% with fees this is approximately $350 per fortnight or $700 per month. But before you think this is making me $1300 per month on cash-flow, we have to factor in rates, insurance, wear and tear and property management fees. Of course, we also get to deduct some tax depreciation which is nice. All in all, it works out to be something like

Income

- + $2000 in rental income

- + $150 in depreciation tax credits (Roughly $5,000 tax depreciation each year)

Sub-Total: $2150

Expenses

- – $700 mortgage (2.2% Interest only)

- – $200 property management fees (10%)

- – $120 council rates (inc. storm water)

- – $150 land lord insurance

- – $466 property maintenance (1% of the house value annually)

Sub-Total: $1,636

Positive cash flow: $513 per month

When switching to a standard Principle and Interest mortgage, the mortgage calculator shows it actually doubles the repayment to $1400 per month ($700 per fortnight), which actually makes it a negative cash flow of $186 per month or nearly $50 per week. Currently the plan is to go for interest only, but I am on the fence about maybe just going P+I to pay down the debt. I am obviously hoping these figures are overly conservative, and I am able to rent it out for more, and that the fee’s are less.

Unsure how leaving flying will affect my serviceability for the refinance at the end of the year (most likely will reduce it) however the websites are cash-flowing nicely and I will hopefully have some financial statements to provide the bank which might put them in a better mood.

I am also considering my next move – purchasing the acreage in the hills as a PPOR. This will likely be somewhere around the $500K+ mark for sized properties I am interested in, so more than likely I will get a mortgage and try and pay it off as soon as I can.

Online Business (websites)

Websites have been going so good this month. The average cash-flows have increased thanks to some awesome deals and I have got some of them revalued based on current niche multiples. This is still very conservative but the estimate was just shy of $167,000 for the combined portfolio of 5 sites. I am looking at buying some more sites soon, and will be putting up reviews on some of the most common M&A / website classified sites.

Pretty cool to think that in around 2 years I built an asset worth $167,000, which each month pays thousands of semi-passive income into my business – which I can then either use to reinvest and buy more sites, or I can pay myself a dividend – Which is exactly what I did this month as I transferred myself a $5,000 payment from the company into my personal account.

I have done a pretty comprehensive review of the eBusiness institute as well as interviewed Matt and Liz Raad about this on the podcast about online business and websites if you want to learn more about this lucrative side hustle. They provide a free introductory course for CaptainFI readers.

I have also recently spoken to Liz Raad again on the pod, and will be releasing this as soon as the editing is finished.

Cash / emergency fund

Upped it to $5000 just to be sure during the move.

Early Retirement

Whilst I have well and truly reached Financial Independence based on my current lifestyle, I am looking forward to dropping down to 2 days a week in my new non-flying role where I can experience some of the benefits of ‘Semi-retirement’.

Whilst the internet early retirement police will probably be quick to point out that this “isn’t FIRE” because I am still doing part time work and I’m making income from my websites, I don’t really mind and I am happy with the concept of ‘Semi-retirement’ for now. I don’t think I could sit around all day and not do anything, anyway. My ADHD brain would explode!

I am still working towards my ‘Family FI’ goal of $6,000 per month (after tax), however I have distanced myself somewhat from thinking about the future too hard and am more just trying to focus on enjoying the now rather than imagining the future.

When looking at the investment trust structure, to earn $6,000 per month after tax it will more or less take $6,800 of gross portfolio income. I am sitting at around $5000 out of the $6,800 ‘passive’ income goal, or about 71% of the way to ‘Family FI’, and most of that is coming from the website portfolio.

My ‘Family FI’ is actually over double my ‘Single FI’ figure, so I am fully aware that I have reached my FI number, but still want to continue slowly working towards ‘Family FI’ by adding to this and the other websites, as well as a small amount of earned income. Thankfully, the investments have well and truly started to snowball, and hopefully they will continue to grow and put me closer to ‘Family FI’ even with a reduced earned income.

For more information on how I am planning for Early Retirement you can read my dedicated transition to retirement financial planning process article.

Captain FI net worth progression

The net worth progression graph is rather crudely constructed in Excel, but still demonstrates the ‘somewhat exponential’ journey over the past 13 years.

| Date | Net worth | Difference | Saving Rate | Notes | |

| Jan 09 | $5,000.00 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK | |

| Jan 10 | $24,000 | +$19,000 | ? | Estimate NW | LINK |

| Jan 11 | $40,000 | +$16,000 | ? | Estimate NW | LINK |

| Jan 12 | $92,000 | +$50,000 | ? | Estimate NW | LINK |

| Jan 13 | $130,000.00 | +$38,000 | ? | Estimate NW | LINK |

| Jan 14 | $161,000.00 | +$31,000 | ? | Estimate NW | LINK |

| Jan 15 | $200,000.00 | +$39,000 | ? | Estimate NW | LINK |

| Jan 16 | $281,000.00 | +$81,000 | ? | Estimate NW | LINK |

| Jan 17 | $340,000.00 | +$59,000 | ? | Estimate NW | LINK |

| Jan 18 | $482,000.00 | +$142,000 | ? | Estimate NW | LINK |

| Jan 19 | $542,000.00 | +$60,000 | ? | Estimate NW | LINK |

| Jul 19 | $578,900.00 | +$36,900 | 84% | Finally began tracking NW this like a proper adult. | |

| Aug 19 | $560,100.00 | -$18,800.00 (-3.2%) | 78% | Share market slight correction, Ok savings. | |

| Sep 19 | $584,744.88 | $24,644.88 | 72% | Share market rebound, savings rate not so good. | LINK |

| Oct 19 | $600,386.00 | $15,641.12 | 84% | Good saving this month. Normal salary, plus allowances, dividends from index funds, tax refund, eBay selling and was working abroad in asia where things are cheap. | LINK |

| Nov 19 | $612,917.21 | $12,531.21 | 76% | Falling short of my savings goal of 80%. Mostly domestic legs this month with higher costs. Also invested in hydroponics. | LINK |

| Dec 19 | $625,350.00 | $12,432.79 | 76% | Good savings of cash (for development) and investment, however higher spending due to Christmas period (Travel and Gifting). | LINK |

| Jan 20 | $865,212.00 | $239,862.00 | 55% | Super settlement was a HUGE boost to NW. $9K growth from stock market. Expensive month lots with lots of unexpected bills – weddings, travel, Booking flights, fines etc. | LINK |

| Feb 20 | $851,802.0 | -$16,592 (-1.9%) | 52% | Large increase in spending on myself this month, still managed to tuck away $5K to put into shares and property. Corona Virus market scare resulted in a correction and gave NW a small negative trend. Time in the market not Timing the market! Became Single again. | LINK |

| Mar 20 | $819, 354.6 | -$31,806.95 (-3.7%) | 80% | Another small step backwards in the NW due to the ‘corona crash’ in full swing. FIRE Portfolio of ETF/LICs down about 15% this month, however due to high savings rate and structure of my superannuation annuity the NW is only down 3.7%. Savings rate good at 80%, higher than usual income (with some slightly higher spending, too). Picking up shares on discount – this is the best outcome for someone in the accumulation phase with good income! | LINK |

| Apr 20 | $847,023 | +$27,668 | 85% | $11,000 in rebound of stock market capital prices alone (up 6%), plus first quarter dividends paid (heavily reduced due to banks withholding dividends). Great savings rate due to COVID-19 lock-down = no spend. Increased entrepreneurial efforts and selling down of physical possessions provided side hustle income. Two standard paychecks from flying activity; domestic day trips only so no allowances. All cash unfortunately had to go into the property development due to contract timing, I am chomping at the bit to buy some more index funds before they go back up in price too much – hence why I am selling most of my toys! | LINK |

| May 20 | $857,859 | +$10,836 | 92% | Some Great sales as I let go of my Super Sport Motorcycle, Some gym gear, expensive flying equipment and a few other various bits and bobs and invested this money. Flying still reduced, but increasing from April. The share market grew as I continued to make my fortnightly investments. I also wrote down the ‘value’ of some of my possessions (liabilities) such as my car, tools and furniture by around $10K to align them to market price (“tell him hes dreaming…!”). | LINK |

| June 20 | $858,650 | +$791 | 90% | Small Net Worth gain as I continue to declutter and simplify my life, despite being off work due to a family emergency. Share market not doing much. | LINK |

| July 20 | $888,218 | +$29,568 | 68% | Majority gain due to share market going back up, low spending due to being on the family farm and at home because of lock down. | LINK |

| Aug 20 | $1,029,293 | +$141,075 | 74% | Became a millionaire. Achieved this massive milestone I set out for myself in Dec 2019. Included unrealised gains in my property development as well as website business. Good savings rate due to not much spending, invested in Aus and total world shares. Investing in my web business. Starting to shift focus away from $$$ and more into looking after my mental health. | LINK |

| Sep 20 | S1,045,486 | +$16,193 | 60% | Officially took time off work for the rest of the year to be close and look after family during major operations. Continued to sell down physical possessions and work on digital business while at home. NW gain mainly due to valuation of websites. | LINK |

| Oct 20 | $1,064,399 | +$18,913 | 80% | Base income (retainer) and leave loading, dividend and websites provided income, as well as raiding my P2P lending capital. Significant bill for property due to design not meeting standards which effectively lowers my equity position, as well as fence being stolen. | LINK |

| Nov 20 | $1,143,433 | +$80,394 | 82% | Big gains came from share market growth (influencing both the Financial Independence share portfolio and Invested superannuation), Business gains (due to increased earnings) and a $30K boost to my annuity thanks to me logging in and checking the fine-print on the accumulation stats. I only invested around $7K. Insane that in one month, I accumulated nearly more net worth than I did in four years from 2009-2012 | LINK |

| Dec 20 | $1,152,920 | + $9,487.32 | 84% | Share market slight drop, Earnings from Business, Contract work, Selling possessions. No share market investments this month (oops! I forgot and money was tight). Invested a lot into the website business this month (way more than planned) and it is still running at a decent loss (plans to turn it cash flow positive in 3 months). | LINK |

| Jan 21 | $1,165,678 | +$12,757 | 79% | Great returns from the share market. Earnings from Business, Dividends, Flying wage, flipping items on consignment. Regular share contribution, investing in micro investing platforms, P2P lending, Investment property and big reinvestment into the business (still running at a loss) | LINK |

| Feb 21 | $1,135,272 | -$30,406 | 76% | Significant write down on property development due to council DA rejection and redesign requiring more money and creating less equity. Offset by small increase to Business value and investments. Simplified my investments and switched over to Pearler. | LINK |

| Mar 21 | $1,155,594 | +$20,322 | 71% | Continued investment into the portfolio as well as growth of investments and business. Gave my notice at work and looking for part time job at home for ‘Barista FI’ | LINK |

| Apr 21 | $1,242,220 | +$86,727 | 74% | Property development back on track | LINK |

| May 21 | $1,379,469 | +$137,248 | 72% | Massive gains in the website portfolio due to revaluation based on recent business income, big growth of superannuation due to annuity increasing (salary increment) and shares generally went up. Crypto went down by about 40% or so. |

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Hey Captain,

I’d be keen to understand your rationale for the equal weight mix of your share portfolio? Care to share? I understand that you’re a former Blueprinter and Barefoot fan, as am I. And the idiot grandson portfolio had VAS, which is similar to A200 plus your other two shares, but with different splits. I’m curious to know why you went equal weight.

Hey Jodie! Initially I was very overweight in Aus shares as I wanted the security of a decent level of passive dividend income, and also had the conformation bias of being Australian. As I have now got that security I wanted to diversify globally. I had thought initially something like 50 AUS, 25 US and 25 Global (ex US), however given the Australian market is only something like 2% of the global economy, I wanted to ramp this up. For now, 1/3 weighting is a really simple target and there isn’t much more thought put into than that! Eventually I would like to even be something like 80% global and 20% Australian!

Ok, Captain, thank you for your reply. It’s such an interesting topic – the split between Aussie shares and international. I see such a massive difference in opinions about this online.

My 18 yr old has a modest but growing share portfolio and we were talking about this the other day – the splits. She also studies Economic and Business at school (in Yr 12), so she’s pretty switched on. She wants growth now, not dividends, whereas my husband and I are in our early 50s, so our goal is to build a passive income via dividends.

Would you consider this topic as a future podcast with an expert, although I’m not sure who?

Yeah Jodie I think its a really important idea – I’ve tentatively got an expert lined up to talk about asset allocation which I’m really excited for. But I need to settle down in my new apartment and get my new recording studio all set up – got accepted today but waiting to get keys and then get the removalists to bring the stuff in. Super excited to record these next few episodes as well as get a few articles out which I’ve had in draft form for a while.

In general though, my race was to replace my income ASAP so I could be work optional, which I did through going heavier on dividends (and websites incidentally too), but capital growth is much more efficient usually for the accumulation stage. In general I think a mix works best, and you can go crazy trying to figure out what to aim for so why not just do both haha

Ok, great, thanks for your reply.

I’m looking forward to hearing that future podcast.

Enjoy setting up your new home!

Hey mate,

Firstly congrats on such a quick journey to FI, really accelerated the last 2 years as you said. I listened to your online websites podcast and although it is intriguing it sounds a bit complex and risky to me – but I wish you nothing but the best with it. Judging how well it’s worked for you so far, I’m sure you’ve looked into how sustainable it is long term.

My one point is that I think you are overly pessimistic on the Family FIRE number. I take it you are currently single and want a set income when you have a family. Sidestepping the discussion around the complexities of finding someone compatible to your lifestyle with your level of wealth for a second, your calculations do not seem to factor your future partner bringing anything to the table? If I was a betting person I can only imagine you will find someone with similar views/values and that would likely result in you finding someone at least partially on their journey to FI. Good for thought, just think you are in an even better place than you think you are.

Sorry to hear about your family situation. Super rough and great you can spend time with them now without worrying about money.

Hey Sam, Thanks for the kind words mate. Hopefully that is the case and I find someone wonderful who would be able to contribute to the family financially, but I enjoy the peace of mind and security knowing it isn’t a ‘mandatory’ on the criteria list, haha! With the website thing, I think the risk is if you leave it static for too long, your competitors begin to outrank you and you simply lose traffic and therefore profitability – so to keep your ‘investment’ (online website business) working well, you do need to ‘feed it’ content each week or so, and keep abreast of changes with SEO. I have started to wind back the effort on them so far and they continue to rank – but I will keep reporting back in and hopefully a long term trend will become apparent.

Understood, always nice to be independent! My FIRE plans are all with my partner and although I don’t think we will ever separate, the risk is always there.

Thanks for the insight re the websites and for creating great content. One side note is your Podcast although great has really quiet audio a lot of the time. Not sure if you can fix it, but compared to other podcasts I find I have to turn yours right up to hear what you and the guests are saying.

Working on it to try and fix 🙂