My net worth went up in November 2020 by more than it did in nearly four years from 2009 to 2012. I am pretty gobsmacked to say the least, and this happened in a reduced income period where I still managed an 82% savings rate. Of the overall gain, less than 10% was due to actually investing. Whilst I am having some great success financially and in business, the battle on the home-front is just beginning….

November update

Well, November is over and its really starting to warm up in Australia. Christmas jingles are taking over, and I have been in full swing in ‘property maintenance and renovation’ mode at the family HQ. I am spending up big at Bunnings, and ‘Bunnings Girl’ always seems happy to see me at the checkout (she’s super cute btw, I am hoping all the supplies I am buying is somewhat impressing her!). Fences are going in, chook runs are being built, bathrooms are being re-done and other additions like another few 10,000L water tanks and another 5kW of solar arrays are going up.

I have had some success with my online business and websites that have been ticking along in the background, and all but 3 of my websites have continued to grow nicely. The other 3… well they need more content, and TLC. Do you think its better to split my efforts evenly across them, or focus on the sites that are booming?

It has been absolutely amazing spending the past 5 months with my family, especially given the struggles my parents are both having with their health. Unfortunately we have had some rather bad news this month with my Mum’s cancer coming back, which has really just knocked the wind out of our sails.

It was nearly 7 years ago to the day that she had received her previous bad news. We are gearing up to fight this battle again together, and thankfully this time we have the luxury of both Mum and I being debt free, with significant Emergency Funds and a growing stream of passive income to help take away some of the financial pressures. We can focus on the real important shit, which is proper medical treatment, rest, good quality and fresh whole food plant based meals, and quality family time.

Part of me knows this is the calm before the storm, so I am in overdrive to get all of the house projects finished before her therapy starts, so she has a nice, modern, functional and calm home.

I am also super conflicted about having to go back to work next year, and feel like I am gearing up to just abandon my family when I go back to Sydney and start working overseas again.

End of financial year tax return is still outstanding…

Yeah I can’t believe I still haven’t done this… when I get back to Sydney I will print my Sharesight tax summary for 2019-2020 financial year and take this down to the accountant. I think I will get at around $5K so this will be a welcome addition and will of course get invested straight away. This is just sheer laziness, and I should have brought my receipts and other tax paperwork with me when I left Sydney. My Bad – and you know what, now I miss out on the compounding effects of 6 months worth of growth on $5000 – with the market sky rocketing, I have probably cost myself over $1000 worth of lost gains due to this laziness.

Saving rate

My Saving rate in November across all of my accounts was 82%, considering the spending on business etc as a form of ‘saving and investing’. I am again, pretty astounded by this figure, given that I have been spending more freely and my income was lower than normal.

Income

Income was still low in November. I received increasing revenue from the website business, however this is now being treated as a separate entity and is now being treated like a business rather than a personal hobby for tax reasons. No dividends this month, but also worked on some other side hustles such as Matched Betting (I have a killer podcast and matched betting article coming up in the next month or so) as well as flipping items / selling things.

Spending

Spending in November was up again aghhh. I have been using WeMoney phone app to track my spending and budgeting, which is useful but also ‘helpfully’ reminds (read:shames!) me when I have gone over budget. As I have done this month. But not to worry! The WeMoney app isn’t perfect and I am still effectively testing it out and providing feedback to the team, but they have opened the platform up for anyone else who wants to use it. IMO its pretty good, but I still need to tweak the results to get the information I need.

As I mentioned over the past few updates and on social media, I am trying to care less on my spending and focus more on enjoying life. Now that both of my parents are battling cancer, it has put things into perspective. The past 5 months off work has been amazing to say the least, and I have one more month at home before I need to return to work.

In order to enjoy this time with the family, I have been caring less about spending and just enjoying the moment.

Investing decisions

This month I allocated $7,193 into the various investments, including into the investment property fund (which is a little tricky to do the net worth accounting for),

In total, $4693 went into Shares this month. The Majority went into Index fund ETFs, however I did also experiment with buying some Apple shares through the the Selfwealth US share trading beta. To be quite honest, I don’t like holding individual equities. I will be selling AAPL and pushing that money back across to my ASX based index funds – this little endeavor was mainly to help SelfWealth beta test their US share trading platform and will cost me about $33 in brokerage and transaction fees, so lets see whether I can break even if AAPL goes up (I’m not holding my breath). If you’re reading this SelfWealth – I want my $33 back haha!

- $2620 ASX:VEU bought on Selfwealth share trading

- $993 ASX:A200 bought on Pearler share trading

- (AUD) $950 NYSE:AAPL on Selfwealth US share trading

- (AUD) $130 NYSE:VTI bought on Stake US share trading.

Property

I paid $1,000 into the property project. Nothing special here, this is just my normal ‘build + mortgage’ commitment.

P2P lending

I did not do any P2P lending this month. Once I have some more surplus funds, Plenti Peer to Peer lending will be my P2P platform of choice.

Business

$1500 went back into the business. This month I invested in a bunch of tools which will help me to scale the business – such as project management subscriptions, social media management, hosting and podcast upgrades. I have also taken on a VA who has been amazing and is already pushing me to achieve more and expand. These costs are pretty much taking up all of the revenue, which is actually a smart thing in a start-up as it helps you scale quicker, but also means the business does not turn a profit – hence there is no issues with Capital Gains Tax etc when moving it into a company structure under a trust.

I actually have committed up to $4000 next month which exceeding revenue, so I will cover this with my personal money if required.

This section is where I talk about my Financial Independence Share Portfolio. This is mostly Exchage Traded Index Funds, and Listed Investment Companies. In my mind, I am building this ‘defensive’ asset (ironic, given most financial advisors say that shares are agressive’) as ‘insurance’ so I can then go ahead and invest in other, more risky ventures such as the websites and property development.

The aim of the Financial Independence portfolio is to provide a solid base of income to cover my cost of living from Early Retirement untill when I can get my superannuation ‘conventional retirement’ benefits – through a combination of dividend income and selling small parcels of shares (expecting roughly 4% dividend income, and then to sell 3% of the portfolio each year to supplement dividends).

The Financial Independence share portfolio is split across the three share trading platforms that I use (the link will take you to my dedicated review of each);

I track my share portfolio using Sharesight, which means my portfolio accounting is completely hands free. I have got automatic trade confirmation emails set up with SelfWealth, and am using the API plugin with Pearler. This means I pretty much just need to log in to confirm all the trades and dividends over the year when needed for my tax return, and also to produce these monthly updates for you guys. The following section contains Sharesight reports for;

- Monthly

- Rolling 12 months

- Since Inception (since I started tracking it with Sharesight).

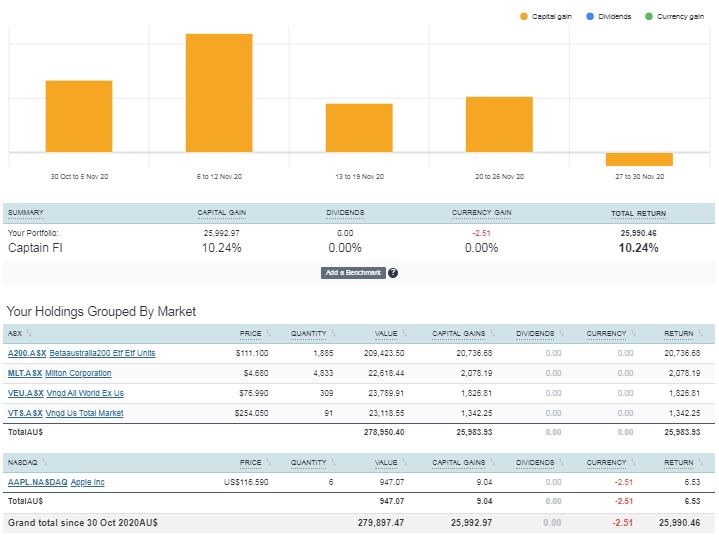

From the Sharesight reporting, November was a great month with markets continuing to bounce back from the earlier correction this year Spurred on by news of a COVID-19 vaccine, my holdings are up over 10%. Whilst we can’t expect to see this every month, it all evens out in the long term

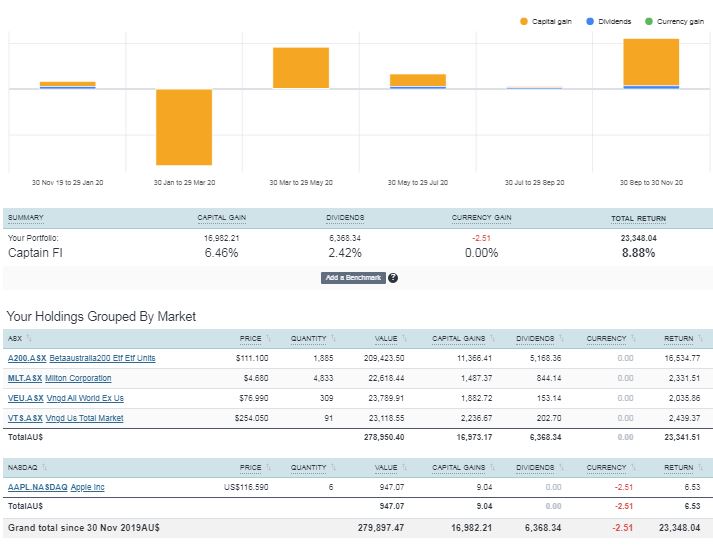

The rolling 12 month figure shows that despite the market correction in March, we are now well and truly back on the right side of the graph. Thanks to Quantitative Easing, and other Fiscal and Monetary policies, as well as general investor psychology, the market does what is always does over a long enough time period. It goes up…

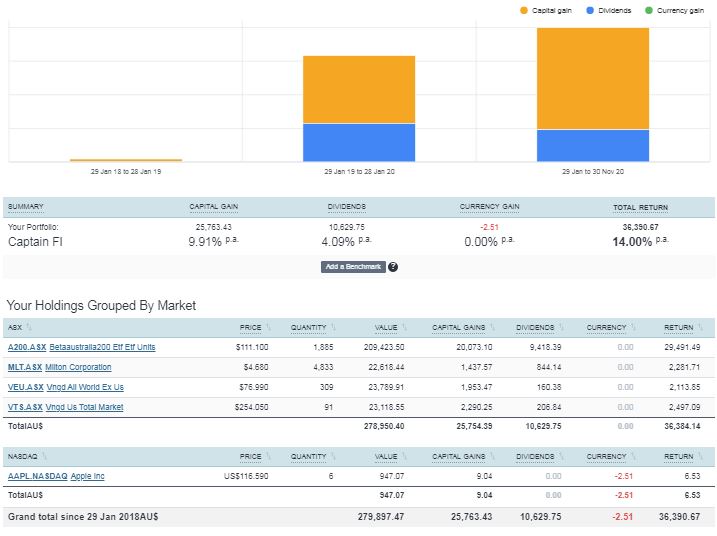

This is the total return since I started using Sharesight to track my portfolio, and switched to a core holding of A200, VTS and VEU complimented by LICs (currently Milton). Don’t let the returns on this graph fool you – it is only tracking open positions of my current portfolio of index funds. Remember when I said I previously had a nasty habbit of stock picking etc? Well this isn’t reflected in the chart. Actually, when I go back through all of my ‘Open and closed’ positions, this results in a total portfolio return since inception of 11% – which is amazing considering all the individual stock purchases I majorly stuffed up and lost money on (thankfully I was only stock picking with small amounts).

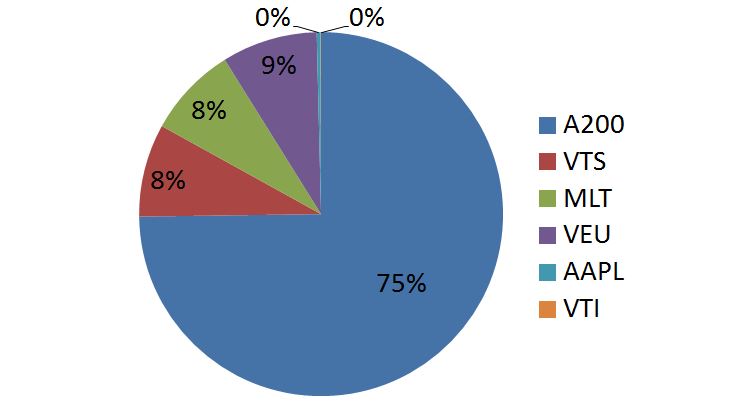

Pie chart

Because sometimes you just need a pie chart to visualize what a portfolio looks like.

Clearly I am overweight on Australian equities – taking on higher portfolio risk to chase franking credits and higher dividends to satisfy that ‘growing snowball of passive income’ itch.

Over time, I will expect to invest more into VTS and VEU to bring the split down to a more sensible level. Currently the target is to get 80:10:10 (AUS:US:World), and then going forward it will be to get it closer to 60:20:20. I am not ready to start selling to re-balance yet, and so all of my current ‘re-balancing efforts’ are from just trying to buy whatever is my lowest split. This becomes less and less effective as the Net Worth continues to increase.

Having said that, I still have some weird aversion to not buying aussie stocks and can’t help myself buying more A200 (probably because its my biggest holding and gives me the most dividends, so psychologically I am always wanting more of this).

Investment Property

There has been a resolution reached with the builders design stuff up… (funny as I type this it really dawned on me that perhaps builders should just be builders, and architects and designers should do the designing…). We have negotiated a deviation due to the windows and environmental points, the builders will pay half of the cost and I will pay half of the cost.

The next step for the IP1 is getting DA approved and pouring the slab, currently my best estimate is for DA in January and to pour in February. Obviously not ideal that the concrete pour is coincident with the bloody hottest part of the year – setting concrete does NOT like hot temperatures I remember that much from my engineering structures university lectures! (I am also somewhat experienced in mixing and pouring concrete for retaining walls, fencing and footpaths).

Other than that, no real updates here. I am still paying into the construction fund, however there isn’t a lot of expenses currently – I am just paying the interest only for the loan against the land, and paying things like rates and insurance etc. After DA the builder progress payments will start which means the construction loan will start getting drawn, and the monthly interest payments will increase.

To get ‘into the habit’ of paying more, I have been contributing extra into the mortgage account which has provided a small buffer in the account – however I can’t access this and therefore I don’t report it as ‘cash’ that I have. Not really sure how to factor this into the ‘net worth’ side of things, so I am not including this money. Essentially this will come down to a cash-flow equation once the property is complete and it should be producing a small positive cash flow.

P2P lending

Last month I withdrew my P2P funds from Plenti. This was because my budget was a bit tight and I needed to deploy those dollars. I also don’t really need any ‘Fixed Interest’ at the moment and if I am honest, it was more of an experiment than anything. I do like P2P lending because it gives me a higher interest that I would get from my online bank account, and investing in the long term markets can actually be a way to create your own income stream.

Having said that – you need to critically analyse the rate of return you are getting versus the risk versus the benefits you would get investing elsewhere – like into index funds. I have not written off P2P lending, and when I am making good income I will explore using Plenti for P2P lending again in the future, because they are the best P2P platform I have found and I have had a good experience with them so far.

Business portfolio

This has been a hot topic and the source of some great debates over the past month since I let this cat out of the bag. I also wrote a dedicated article about how I make money online, as well as interviewing Matt and Liz Raad from the eBusiness Institute on the CaptainFI podcast about online business and how I started and am growing mine.

After doing some of their free courses and seminars, I am now enrolled with them on their website and digital business courses which will save me quite a bit of time. I no longer need to go and research every little detail myself – I can just implement their suggestions, leverage their network and benefit from their mentoring.

I am currently running 5 websites – two which make money, and three which are in the ’embryonic’ stage which I am working on building content for and getting them to start ranking before I can monetise them.

Running websites in partnership can be very difficult, especially when both parties are really busy people. After some negotiation, my business partner and I decided it would be best if I was to ‘buy them out’ on one of our joint websites. I really valued the partnership and I was learning a lot from my partner, but ultimately it wasn’t really worth their time anymore as they were doing exceptionally well with their digital marketing agency and so needed to prioritise their time to that. Over the next few months I will be transitioning this site into my business portfolio and paying out the contract, and then focusing some more efforts into building up content, monetizing more and starting to outsource things on it more.

A massive pivot this month was hiring a VA contractor to help out with certain things in the business. Work has only just started but this will be great in managing workload, allowing the business to scale, and allowing me to focus on the part of the business that I really love (like writing and interviewing people). Things that my VA will be helping with will include;

- Social media strategy

- SEO content audit

- Proof reading and editing

- Buisness development: Communication, sales and managing affiliates and sponsors

Potentially in the future, they will also manage bringing in writers and working on a content plan. Currently I am doing this myself and with occaisonal help from a friend who runs a digital marketing agency.

Overall, $1500 went into the business in November, including a $4000 spending commitment over the next few months for things like accounting, VA work, tools and service upgrades. This means no income paid from the buisness to myself, because I am choosing to reinvest everything into scaling and upgrading for now. I am even happy to put more of my own money into this if needed.

This should see a much higher ROI than if I just invested it into index funds or property, and as a bonus, because I am not realising any gains yet and there is no income, there is also no taxation (except GST but that only kicks in when your making over $6250 per month which I am not).

My goal is to still turn over $10,000 per month by the end of this year. It might not happen, but I am still working towards securing sponsors and contracts to make it happen!

Retirement

I am still working toward my ‘Family FIRE’ goal of $6,000 per month. When looking at the future trust structure, to earn $6,000 per month after tax it will more or less take $6,800 of gross portfolio income. Currently, I am still conservatively at $3000 out of the $6,800 goal, or nearly half way to ‘Family FIRE’!

With my business growth, I am expecting to see average revenue increase and helping me to achieve this passive income goal. However, nothing is certain in business so I will of course eventually be distributing profits as a dividend to myself and family through my trust, and personally I will be reinvesting them into the more benign and safer environment of index funds to grow the passive income. I am also planning to put some of this towards buying an acreage on which I want to build the future family home on.

You can read my dedicated Transition to retirement Financial Planning process article here.

As a quick and dirty, I plan to live off a 7% draw-down of my Financial Independence Share Portfolio (4% dividend and 3% selling parcels of shares each year) from when I choose to start early retirement, through to when I am eligible to receive my superannuation lump sum payment and my annuity starts paying me.

So how do I value my superannuation? Well it is an interesting topic and up for debate (let me know your opinion!)

The invested portion is super easy – it is literally just all invested in shares (Australia and International shares) in index funds – if I contribute nothing more and let it tick away, I will have just under $1M by preservation age. To get to the $1.6M cap, I could either stuff in another $50K to super right now, or closer to $70K of contributions over the next 2 years or so (which I am on track to do and reach before FIRE thanks to compulsory 9.5% wage input).

My annuity is a pension that is indexed to CPI for life, and it is a bit trickier to value. Given that Australian average male life expectancy is 82 years, and I think I can erk out a few extra years based on my habits of weightlifting, having a (mostly) plant based diet and yearly comprehensive medicals. I think at least 30 years of the annuity payments is a safe bet. When I looked online and got some quotes for this, the prices ranged from 25x to 30x annual payments. Interestingly, the Australian Tax Office values my annuity much less, at only 12x annual value (I am not sure if this is counted towards my $1.6M super cap or not). I conservatively value my annuity at 25x annual payments, which coincidentally is also in line with the 4% rule from the Trinity Study regarding investment portfolio balances and retirement.

Captain FI Net worth November 2020

The Net Worth pie chart is a great visualization of my total financial portfolio breakdown. Weirdly enough, these splits seem to stay roughly the same, despite each sector growing at a different rate (bearing in mind these are rounded up to the closest percent for ease of visualisaton). Each

- Super – Annuity: $528K [Conservatively valued at 25x annual pension value]

- Shares (FI portfolio of ETFs + LICs): $280K

- Equity (Investment property): $196K

- Super – invested fund: $79K

- Business: $45K [although I would not sell it for anything less than $1M – and I am not even joking]

- Physical possessions (stuff that I own): $11K

- Cash / Bond: $3.5K

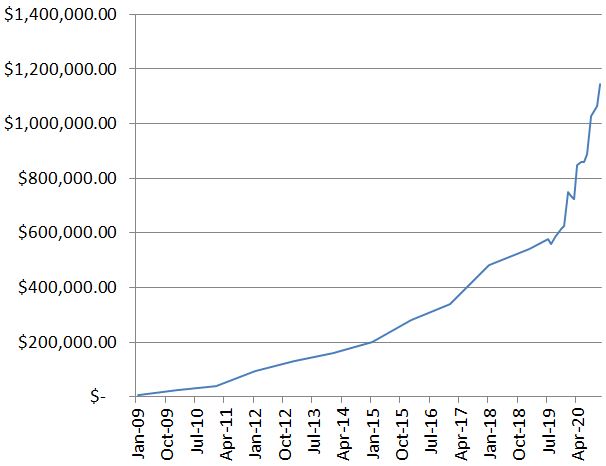

Captain FI Net Worth Progression

Tracking your Net Worth over time is one way to monitor and compare your progression to FIRE. A better way though, is to track your passive income – such as dividend income. Because that is what you are going to be using to live off if you do choose to retire early. Because of how I have my finances structured as an Australian investor with a significant amount invested in Superannuation, my NW number isn’t really all that reflective of my ability to FIRE, but I still think it is an important metric to track since its growth is representative of performance – the rate of change of net worth is more important than Net worth by itself, in my opinion.

CaptainFI Net Worth Progression – Graph

The Net worth progression graph is rather crudely constructed in Excel, but still demonstrates the ‘somewhat exponential’ journey over the past 12 years.

CaptainFI Net worth progression – table

I decided to include a Net worth table which provides a bit more information on my journey for anyone wanting to go back and see how individual years or months went at a quick glance.

| Date | Net worth | Difference | Saving Rate | Notes | |

| Jan 09 | $5,000.00 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK | |

| Jan 10 | $24,000 | +$19,000 | ? | Estimate NW | LINK |

| Jan 11 | $40,000 | +$16,000 | ? | Estimate NW | LINK |

| Jan 12 | $92,000 | +$50,000 | ? | Estimate NW | LINK |

| Jan 13 | $130,000.00 | +$38,000 | ? | Estimate NW | LINK |

| Jan 14 | $161,000.00 | +$31,000 | ? | Estimate NW | LINK |

| Jan 15 | $200,000.00 | +$39,000 | ? | Estimate NW | LINK |

| Jan 16 | $281,000.00 | +$81,000 | ? | Estimate NW | LINK |

| Jan 17 | $340,000.00 | +$59,000 | ? | Estimate NW | LINK |

| Jan 18 | $482,000.00 | +$142,000 | ? | Estimate NW | LINK |

| Jan 19 | $542,000.00 | +$60,000 | ? | Estimate NW | LINK |

| Jul 19 | $578,900.00 | +$36,900 | 84% | Finally began tracking NW this like a proper adult. | |

| Aug 19 | $560,100.00 | -$18,800.00 (-3.2%) | 78% | Share market slight correction, Ok savings. | |

| Sep 19 | $584,744.88 | $24,644.88 | 72% | Share market rebound, savings rate not so good. | LINK |

| Oct 19 | $600,386.00 | $15,641.12 | 84% | Good saving this month. Normal salary, plus allowances, dividends from index funds, tax refund, eBay selling and was working abroad in asia where things are cheap. | LINK |

| Nov 19 | $612,917.21 | $12,531.21 | 76% | Falling short of my savings goal of 80%. Mostly domestic legs this month with higher costs. Also invested in hydroponics. | LINK |

| Dec 19 | $625,350.00 | $12,432.79 | 76% | Good savings of cash (for development) and investment, however higher spending due to Christmas period (Travel and Gifting). | LINK |

| Jan 20 | $865,212.00 | $239,862.00 | 55% | Super settlement was a HUGE boost to NW. $9K growth from stock market. Expensive month lots with lots of unexpected bills – weddings, travel, Booking flights, fines etc. | LINK |

| Feb 20 | $851,802.0 | -$16,592 (-1.9%) | 52% | Large increase in spending on myself this month, still managed to tuck away $5K to put into shares and property. Corona Virus market scare resulted in a correction and gave NW a small negative trend. Time in the market not Timing the market! Became Single again. | LINK |

| Mar 20 | $819, 354.6 | -$31,806.95 (-3.7%) | 80% | Another small step backwards in the NW due to the ‘corona crash’ in full swing. FIRE Portfolio of ETF/LICs down about 15% this month, however due to high savings rate and structure of my superannuation annuity the NW is only down 3.7%. Savings rate good at 80%, higher than usual income (with some slightly higher spending, too). Picking up shares on discount – this is the best outcome for someone in the accumulation phase with good income! | LINK |

| Apr 20 | $847,023 | +$27,668 | 85% | $11,000 in rebound of stock market capital prices alone (up 6%), plus first quarter dividends paid (heavily reduced due to banks withholding dividends). Great savings rate due to COVID-19 lock-down = no spend. Increased entrepreneurial efforts and selling down of physical possessions provided side hustle income. Two standard paychecks from flying activity; domestic day trips only so no allowances. All cash unfortunately had to go into the property development due to contract timing, I am chomping at the bit to buy some more index funds before they go back up in price too much – hence why I am selling most of my toys! | LINK |

| May 20 | $857,859 | +$10,836 | 92% | Some Great sales as I let go of my Super Sport Motorcycle, Some gym gear, expensive flying equipment and a few other various bits and bobs and invested this money. Flying still reduced, but increasing from April. The share market grew as I continued to make my fortnightly investments. I also wrote down the ‘value’ of some of my possessions (liabilities) such as my car, tools and furniture by around $10K to align them to market price (“tell him hes dreaming…!”). | LINK |

| June 20 | $858,650 | +$791 | 90% | Small Net Worth gain as I continue to declutter and simplify my life, despite being off work due to a family emergency. Share market not doing much. | LINK |

| July 20 | $888,218 | +$29,568 | 68% | Majority gain due to share market going back up, low spending due to being on the family farm and at home because of lock down. | LINK |

| Aug 20 | $1,029,293 | +$141,075 | 74% | Became a millionaire. Achieved this massive milestone I set out for myself in Dec 2019. Included unrealised gains in my property development as well as website business. Good savings rate due to not much spending, invested in Aus and total world shares. Investing in my web business. Starting to shift focus away from $$$ and more into looking after my mental health. | LINK |

| Sep 20 | S1,045,486 | +$16,193 | 60% | Officially took time off work for the rest of the year to be close and look after family during major operations. Continued to sell down physical possessions and work on digital business while at home. NW gain mainly due to valuation of websites. | LINK |

| Oct 20 | $1,064,399 | +$18,913 | 80% | Base income (retainer) and leave loading, dividend and websites provided income, as well as raiding my P2P lending capital. Significant bill for property due to design not meeting standards which effectively lowers my equity position, as well as fence being stolen. | LINK |

| Nov 20 | $1,143,433 | +$80,394 | 82% | Big gains came from share market growth (influencing both the Financial Independence share portfolio and Invested superannuation), Business gains (due to increased earnings) and a $30K boost to my annuity thanks to me logging in and checking the fine-print on the accumulation stats. I only invested around $7K. Insane that in one month, I accumulated nearly more net worth than I did in four years from 2009-2012 |

Monthly question from the Captain

Have you thought about online buisness, and if you have, what has been your experience? I have been working on it slowly for about a year now and I am starting to see the returns slowly coming in.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

It’s funny reading you describe your LICs and ETFs as defensive assets! I think of my own holdings in AFI and VAS the same way… Cash and Bonds? Now they’re risky! 😆😆

Haha I guess it all comes down to time frame! AFI is a solid LIC, was my first holding and definitely on the radar for future ‘defensive’ purchases 😛

Love these reliable dividend machines that have good upside growth potential too from the increase in earnings potential they all have. Focusing my time into more riskier ventures, but a split of all future profit and revenue will get socked away into them !

I love reading your net worth posts. It was a great month for us, especially since I only started buying shares this year and our supers have rebounded nicely. I am working on funding my husbands retirement for the years before we can access our super at 60, which is coming up fast 🙂 Also you have the month wrong on your pie chart heading, reading October 2020 🙂

oops! Thanks for the correction Mel, I have fixed that up 🙂 November has been a great month for the market. So exciting to hear preservation age is coming up! Retirement will come up quick

Hi Capatin FI

Can I ask why you bought vti through stake rather than just vts?

What are the benefits of using stake over buying the US Stock market index thorugh an australian broker?

G’day Bo-Delle, To be honest it was more just to test the platform out. The owners of Stake saw my review and gave me USD $50 into my account to test it out and update the review with my findings, and to be honest it all worked pretty well. I would have certainly felt pretty unethical just snaking the money out and transferring it to my other broker to invest in VTS.

If I am honest, I think NDQ:VTI and ASX:VTS give me pretty much the same exposure.

VTS is a bit easier to manage right, because it is listed on the ASX and hence my registry (link or computershare I can’t remember) send me out letters and emails about it, wheras I am not sure what happens with Stake. Stake have done the W8 form on my behalf so I think dividends will just be taxed by the american IRS (at 15%) and then paid into my stake account, and then I think the Australian ATO will want their share of whats left (my marginal rate less 15% the Americans already withheld).

Going forward, because of this uncertainty and the economy of scale, I don’t think I will be buying any more VTI through Stake, and will just be purchasing VTS through my aussie brokers (either Selfwealth or Pearler because CHESS sponsored). Since stake has money in the account and its already been converted to USD and its brokerage free, I might stuff around with some ‘day trading’ or ‘speculative stocks’ and see how fast I can burn that account down to zero haha!